Global Carbamate Insecticide Market Size, Share, And Industry Analysis Report By Product Type (N-methyl Carbamates, N-aryl Carbamates), By Crop Type (Cereals and Grains, Oilseeds and Pulses, Fruits and Vegetables, Others), By Application (Foliar Spray, Soil Treatment, Seed Treatment, Post-Harvest Fumigation, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 180430

- Number of Pages: 354

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

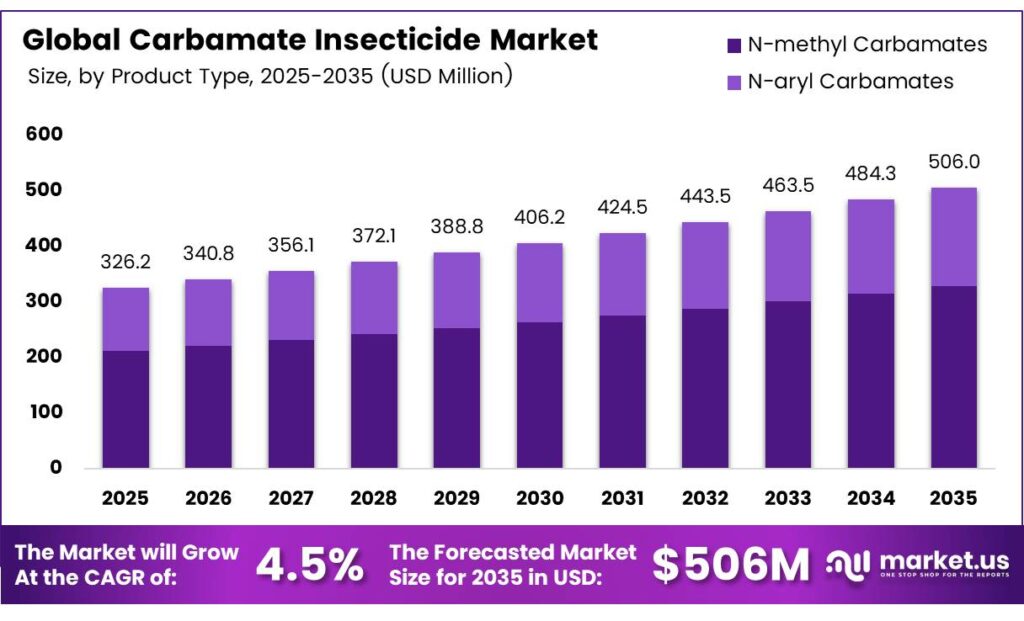

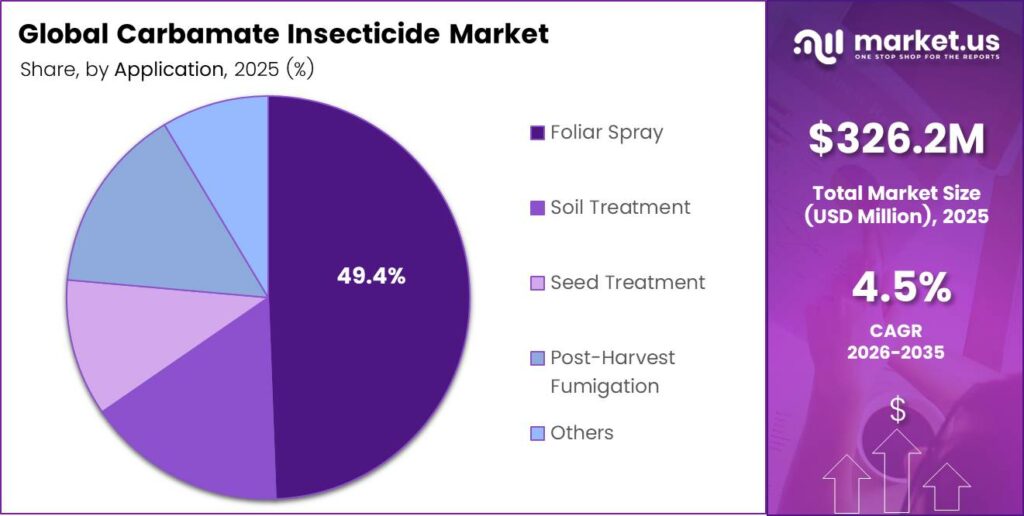

The Global Carbamate Insecticide Market size is expected to be worth around USD 506.0 million by 2035 from USD 326.1 million in 2025, growing at a CAGR of 4.5% during the forecast period 2026 to 2035.

The carbamate insecticide market covers a class of chemical compounds widely used in crop protection and public health pest control. These compounds inhibit acetylcholinesterase enzymes, disrupting nervous system function in target insects. Farmers and pest control operators rely on carbamates to manage a broad range of pest species across diverse agricultural and non-agricultural settings.

Carbamate insecticides serve a vital role in integrated pest management programs globally. Their broad-spectrum activity makes them suitable for cereals, oilseeds, fruits, and vegetables. Moreover, their well-established efficacy against resistant pest populations positions them as reliable rotation partners within structured resistance management frameworks recommended by regulatory agencies.

- Global trade data reflects strong demand for carbamate-related chemical compounds across all major regions. According to the World Integrated Trade Solution (WITS) based on UN Comtrade data, China exported $1,839,824.69 thousand of cyclic amides, including carbamates under HS 292429 in 2024, equal to 161,000,000 kilograms, confirming its position as the largest carbamate-related export hub in verified global trade.

Import demand reinforces the market’s global footprint across key agricultural regions. According to FAO’s latest verified regional trade release, the Americas imported 1.97 million tonnes of pesticides from other regions, the highest regional inbound volume recorded. This confirms that North and South American agricultural systems represent a critical and sustained demand base for insecticide producers, including carbamate suppliers.

Regulatory frameworks shape how carbamate products reach farmers and public health agencies. The EPA conducts ongoing registration reviews for the carbamate chemical class, requiring robust safety and efficacy data from manufacturers. However, these reviews also reinforce market confidence by validating carbamate products as scientifically supported crop protection tools under modern safety standards.

Key Takeaways

- The Global Carbamate Insecticide Market is valued at USD 326.1 million in 2025 and is projected to reach USD 506.0 million by 2035, at a CAGR of 4.5% during the forecast period 2026 to 2035.

- N-methyl Carbamates dominate with a 69.2% market share in 2025.

- Cereals and Grains hold the leading position with a 39.1% share.

- Foliar Spray leads with a 49.4% share of total application methods.

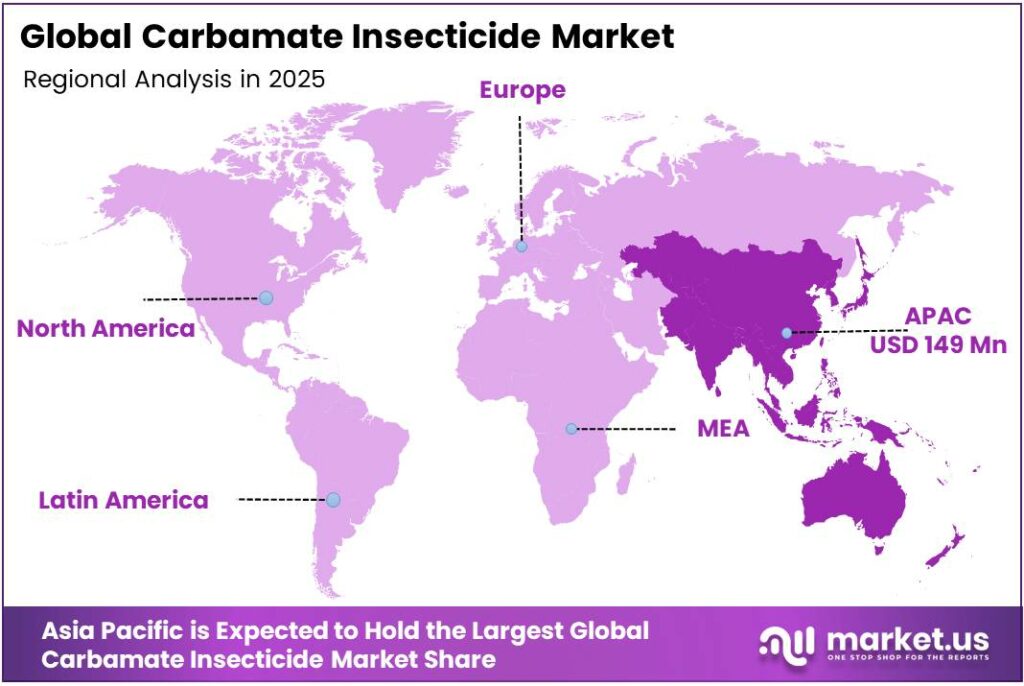

- Asia Pacific dominates the regional landscape with a 45.7% market share, valued at USD 149.0 million in 2025.

Product Type Analysis

N-methyl Carbamates dominate with 69.2% due to broad-spectrum efficacy and wide regulatory acceptance across major crop systems.

In 2025, N-methyl Carbamates held a dominant market position in the By Product Type segment of the Carbamate Insecticide Market, with a 69.2% share. This sub-segment benefits from proven acetylcholinesterase inhibition activity across a wide range of insect pests. Consequently, farmers in high-volume cereal, fruit, and vegetable production systems consistently select N-methyl carbamates as their primary chemical control option.

N-aryl Carbamates represent the remaining share in the product type segment and serve specialized applications within the market. These compounds target selective pest groups and find use in specific horticultural and public health contexts. Moreover, ongoing research into N-aryl carbamate formulations supports their role in resistance management rotation strategies where alternative modes of action are required.

Crop Type Analysis

Cereals and Grains dominate with 39.1% due to extensive global cultivation areas and high pest pressure requiring consistent insecticide programs.

In 2025, Cereals and Grains held a dominant market position in the By Crop Type segment of the Carbamate Insecticide Market, with a 39.1% share. This crop category covers wheat, rice, maize, and barley, all of which face persistent insect pest challenges globally. Therefore, farmers managing large-scale cereal production apply carbamate insecticides regularly within structured IPM rotation programs recommended by agricultural extension agencies.

Oilseeds and Pulses represent a significant crop type segment supported by growing global demand for soybean, canola, and legume production. Aphids, thrips, and pod-boring pests create consistent insecticide demand across these crops. Additionally, carbamate use in oilseed farming is supported by official pest management recommendations in major producing countries across the Asia Pacific and the Americas.

Fruits and Vegetables command a meaningful share of carbamate insecticide demand due to the high economic value of horticultural crops. Growers apply foliar sprays and soil treatments to protect produce quality and yield. However, residue monitoring requirements under programs such as the USDA Pesticide Data Program shape application practices and reinforce responsible use standards in this sensitive crop category.

Others include turf, ornamentals, and non-crop public health applications where carbamate insecticides serve important roles. Indoor residual spraying programs targeting pyrethroid-resistant malaria vectors represent a growing application within this category. Consequently, demand from public health agencies in Africa, Asia, and Latin America contributes incremental volume to this segment of the overall carbamate insecticide market.

Application Analysis

Foliar Spray dominates with 49.4% due to ease of application, rapid pest knockdown, and compatibility with standard agricultural equipment.

In 2025, Foliar Spray held a dominant market position in the By Application segment of the Carbamate Insecticide Market, with a 49.4% share. Farmers prefer this method because it delivers the active ingredient directly onto plant surfaces where feeding pests are active. Moreover, foliar spray applications integrate easily into existing mechanized farming systems across cereals, vegetables, and fruit crops worldwide.

Soil Treatment serves as an important application method for managing soil-dwelling pests, including nematodes, grubs, and root-feeding larvae. Growers apply carbamate-based soil treatments at planting to establish early-season protection. Additionally, soil treatment applications support USDA and FAO IPM recommendations in commodity crops where belowground pest populations threaten root systems and reduce yield potential.

Seed Treatment provides targeted early-stage crop protection by coating seeds with carbamate active ingredients before planting. This method delivers precise dosing while minimizing field-level environmental exposure. Consequently, seed treatment adoption continues to grow in markets where precision agriculture practices and reduced-volume pesticide application strategies gain traction among commercial growers.

Post-Harvest Fumigation uses carbamate-based compounds to protect stored grain and protect against insect infestation during warehousing and transport. This application supports food security objectives across developing and developed markets alike. Furthermore, Others in this segment cover specialty applications, including public health spraying programs and vector control operations targeting resistant mosquito populations.

Key Market Segments

By Product Type

- N-methyl Carbamates

- N-aryl Carbamates

By Crop Type

- Cereals and Grains

- Oilseeds and Pulses

- Fruits and Vegetables

- Others

By Application

- Foliar Spray

- Soil Treatment

- Seed Treatment

- Post-Harvest Fumigation

- Others

Emerging Trends

Resistance Management Mandates and Residue Monitoring Shape Carbamate Market Evolution

Regulatory agencies now require pesticide resistance management and IPM advisory language on all updated EPA carbamate product labels. This mandate signals a shift toward structured, science-based insecticide use across commercial farming systems. Consequently, agrochemical suppliers reformulate product positioning strategies to align with evolving label compliance requirements in major agricultural markets.

- Residue monitoring programs actively validate carbamate safety in food supply chains. The USDA Pesticide Data Program intensifies testing to confirm acceptable residue levels in commercially sold produce. Europe imported 1.96 million tonnes of pesticides from other regions, confirming its role as one of the two largest regional import markets, where stringent residue standards directly shape supplier compliance strategies.

Indoor residual spraying programs increasingly adopt carbamate insecticides to counter pyrethroid-resistant malaria vectors. Global health agencies prioritize carbamates as effective alternatives in multi-class resistant mosquito control campaigns. Moreover, industry-wide mode-of-action rotation stewardship programs incorporate carbamates to delay further resistance development, reinforcing their long-term relevance in both agricultural and public health insecticide portfolios.

Drivers

Escalating Insecticide Resistance and Broad-Spectrum Efficacy Drive Sustained Carbamate Demand

Farmers face increasing resistance among pest populations to organophosphates and pyrethroids across major commodity crops. USDA-supported IPM protocols specifically recommend carbamate rotation to manage this resistance challenge effectively. Therefore, agrochemical advisors and extension services actively prescribe carbamate-based programs as a scientifically validated component of sustainable pest management strategies.

- Carbamates deliver broad-spectrum acetylcholinesterase inhibition across diverse pest complexes in high-volume agricultural systems. The United States imported $390,149.25 thousand of acyclic amides, including carbamates under HS 292410 in 2024, equal to 87,351,000 kilograms, confirming strong and sustained American demand. This import volume reflects consistent grower reliance on carbamate active ingredients across domestic crop protection programs.

Integration of carbamates with semiochemical lures and attract-and-kill technologies strengthens their value within USDA ARS IPM protocols targeting invasive fruit flies. This combined application approach improves pest control precision while reducing total pesticide volumes applied per acre. Additionally, carbamates sustain a critical role in public health vector control programs due to their proven efficacy against multi-class resistant mosquito populations in tropical disease zones.

Restraints

Resistance Emergence and Regulatory Review Processes Challenge Market Stability for Carbamate Insecticides

Carbamate resistance emergence among Caribbean fruit fly populations presents a documented challenge to long-term product efficacy. USDA ARS resistance monitoring studies confirm low-level resistance development in these specific populations. Consequently, carbamate manufacturers face pressure to develop new formulations and resistance management strategies to maintain effectiveness in affected agricultural regions.

The EPA conducts ongoing registration review scheduling for the entire carbamate chemical class, requiring manufacturers to fulfill extensive data requirements. This review process demands significant financial and scientific resources from agrochemical companies. Moreover, delays in registration renewal create uncertainty in supply planning for distributors and growers who depend on specific carbamate active ingredients for their seasonal pest management programs.

These regulatory and resistance-related restraints collectively slow carbamate market momentum in certain geographies. Smaller manufacturers face disproportionate compliance burdens compared to large multinational agrochemical companies. However, well-resourced companies that maintain proactive regulatory engagement and resistance management investment continue to defend their carbamate product portfolios effectively within the evolving regulatory landscape.

Growth Factors

Innovation in Selective Formulations and Expanded IPM Adoption Accelerate Carbamate Market Expansion

Researchers actively develop selective mosquitocidal carbamates with low toxicity to non-target agricultural pests, creating superior resistance management tools. These next-generation formulations address growing demand from integrated pest management programs that balance efficacy with environmental stewardship objectives. Therefore, innovation in carbamate chemistry directly supports market expansion into public health and specialty agricultural segments.

- Reduced Agent Area Treatments in USDA rangeland grasshopper suppression programs extend carbamate field longevity across large-scale land management operations. Asia exported 2.4 million tonnes of pesticides to other regions, worth USD 11.4 billion, confirming Asia’s dominance as the global pesticide supply hub. This export volume highlights the region’s central role in supporting carbamate demand across all major importing markets.

State and federal extension IPM recommendations increasingly incorporate carbamates for managing resistant pest pressure in key commodities. Carbamate insect growth regulators such as fenoxycarb also attract research attention for interactions with plant brassinosteroid pathways, opening new crop protection applications. Consequently, these science-driven growth pathways broaden the commercial relevance of carbamate insecticides well beyond traditional foliar spray applications.

Regional Analysis

Asia Pacific Dominates the Carbamate Insecticide Market with a Market Share of 45.7%, Valued at USD 149.0 Million

Asia Pacific leads the global carbamate insecticide market with a 45.7% share, valued at USD 149.0 million in 2025. The region’s large-scale rice, cereal, and vegetable farming systems generate high and consistent insecticide demand. India plays a major role as a major carbamate supplier, driving regional and global trade flows.

North America represents a major demand center for carbamate insecticides driven by large-scale cereal, soybean, and specialty crop production. USDA IPM protocols and EPA-registered product portfolios support consistent carbamate adoption across commercial farming operations. Moreover, public health vector control programs in southern states create additional non-agricultural demand for carbamate active ingredients.

Europe maintains substantial carbamate insecticide demand despite stringent regulatory oversight from the European Food Safety Authority and national competent authorities. The region’s high-value horticultural and cereal sectors drive application volumes. However, ongoing regulatory reviews and residue monitoring requirements shape product registration timelines and influence formulation strategies for suppliers entering European agricultural markets.

The Middle East and Africa region drives carbamate demand primarily through public health vector control programs targeting malaria and other insect-borne diseases. Indoor residual spraying campaigns using carbamate active ingredients address growing pyrethroid resistance in sub-Saharan Africa. Furthermore, expanding irrigated agriculture in North Africa and the Gulf region creates incremental demand for carbamate-based crop protection programs.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

BASF SE operates one of the largest agricultural solutions platforms globally, with its crop protection portfolio covering insecticides, fungicides, and herbicides across all major geographies. Reflecting improved earnings quality. BASF’s regional sales mix of 39.8% North America positions it strongly in the highest-value carbamate-adjacent insecticide market.

FMC Corporation maintains a focused crop protection portfolio that spans insecticides, herbicides, and fungicides across major agricultural markets worldwide. FMC’s active investment in new active ingredient discovery and formulation innovation supports its competitive positioning in insecticide markets where resistance management drives product demand.

Syngenta delivers a comprehensive range of crop protection products, including insecticides relevant to the carbamate and adjacent chemical classes across global markets. The company’s integrated approach combining seeds, crop protection chemistry, and digital agronomy tools strengthens grower relationships. Moreover, Syngenta’s investment in sustainable agriculture platforms and IPM-compatible product lines aligns with evolving regulatory and market requirements in major crop protection markets.

Corteva Agriscience focuses on developing advanced crop protection solutions and seed technologies that support grower productivity across diverse agricultural systems. The company invests heavily in active ingredient discovery, with insecticide portfolios targeting key pest resistance challenges in cereals, oilseeds, and specialty crops. Additionally, Corteva’s collaboration with extension services and IPM advisory networks reinforces the scientific credibility of its crop protection recommendations.

Top Key Players in the Market

- BASF SE

- FMC Corporation

- Syngenta

- Corteva Agriscience

- Nufarm Limited

- Bayer AG

- Ningbo Sunjoy Cropscience Co., Ltd.

- United Phosphorus Ltd.

- Drexel Chemical Co.

- NACL Industries Ltd.

Recent Developments

- In 2025, FMC continues to offer Marshal 48 EC Insecticide, a systemic carbamate insecticide and nematicide containing Carbosulfan (carbamate) at 480 g/L (IRAC Group 1A). It targets pests such as Protostrophus, maize stalkborer, sorghum stalk borer, and cotton aphid on crops including maize, sorghum, sweet corn, and cotton.

- In 2025, Corteva offers LANNATE Insecticide (active ingredient: methomyl, a carbamate) as a registered insecticide in Canada (PCPA Registration No. 10868). The Safety Data Sheet confirms it as a carbamate pesticide with associated hazards (e.g., acute toxicity categories, transport as CARBAMATE PESTICIDE, SOLID, TOXIC).

Report Scope

Report Features Description Market Value (2025) USD 326.1 Million Forecast Revenue (2035) USD 506.0 Million CAGR (2026-2035) 4.5% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (N-methyl Carbamates, N-aryl Carbamates), By Crop Type (Cereals and Grains, Oilseeds and Pulses, Fruits and Vegetables, Others), By Application (Foliar Spray, Soil Treatment, Seed Treatment, Post-Harvest Fumigation, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape BASF SE, FMC Corporation, Syngenta, Corteva Agriscience, Nufarm Limited, Bayer AG, Ningbo Sunjoy Cropscience Co., Ltd., United Phosphorus Ltd., Drexel Chemical Co., NACL Industries Ltd. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Carbamate Insecticide MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Carbamate Insecticide MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- BASF SE

- FMC Corporation

- Syngenta

- Corteva Agriscience

- Nufarm Limited

- Bayer AG

- Ningbo Sunjoy Cropscience Co., Ltd.

- United Phosphorus Ltd.

- Drexel Chemical Co.

- NACL Industries Ltd.

Our Clients

- 180430

- March 2026