Quick Navigation

Report Overview

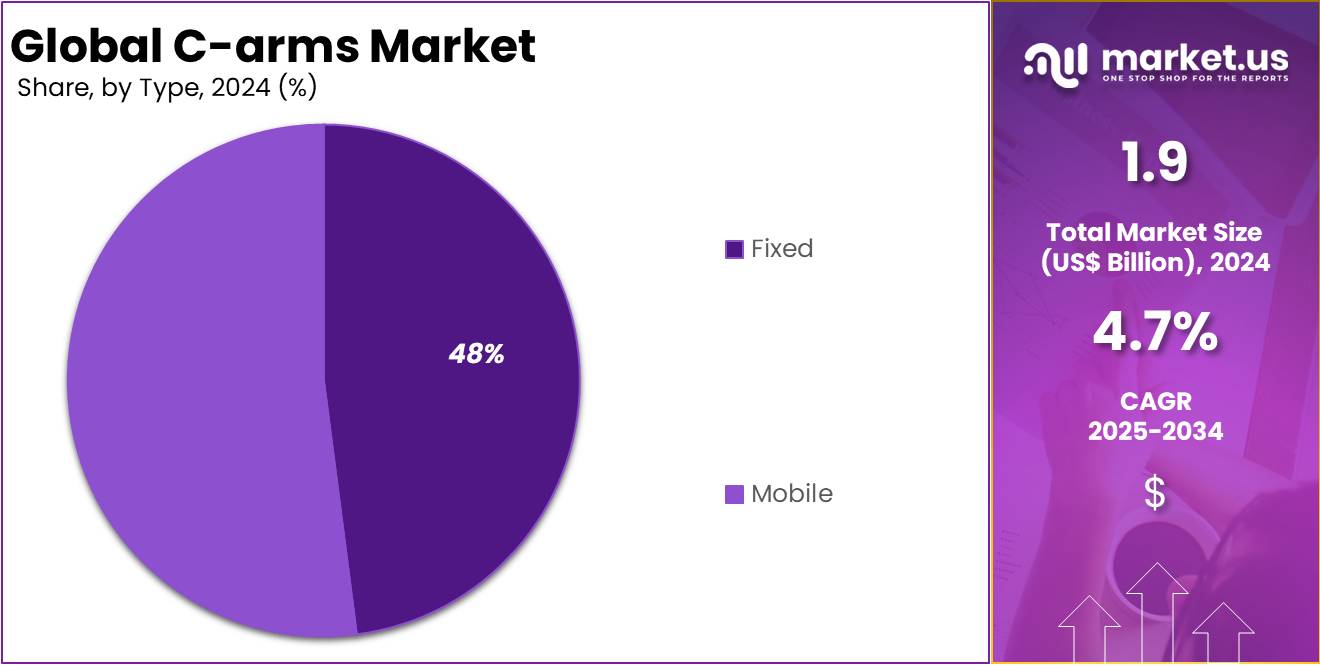

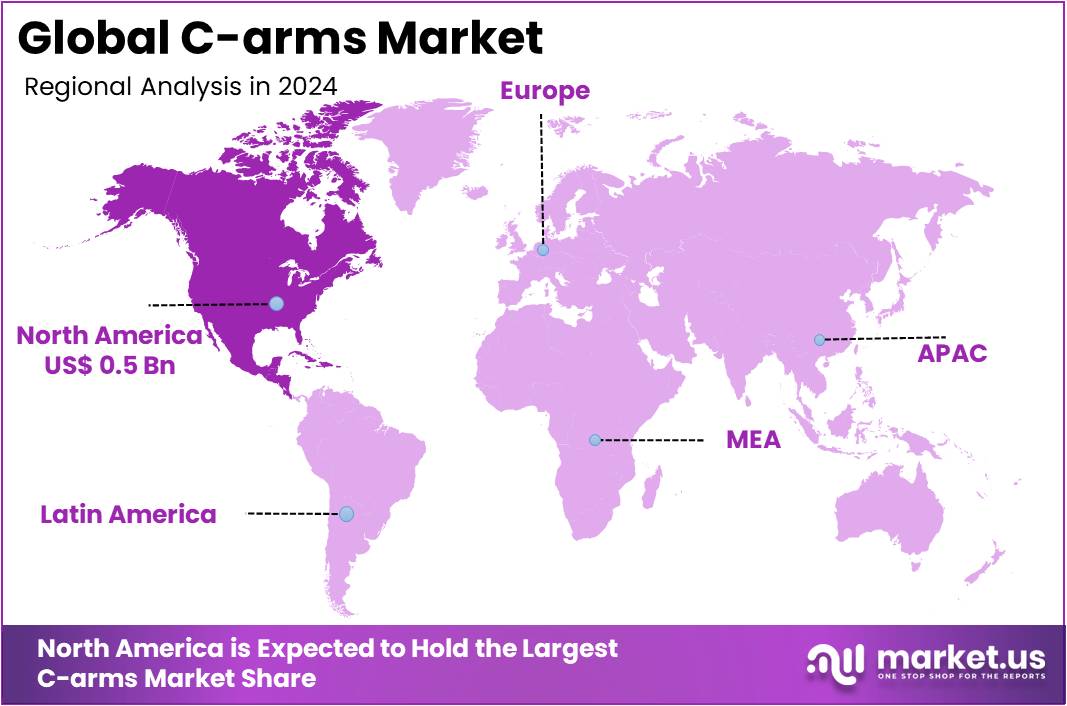

The Global C-arms Market Size is expected to be worth around US$ 3 Billion by 2034, from US$ 1.9 Billion in 2024, growing at a CAGR of 4.7% during the forecast period from 2025 to 2034. North America held a dominant market position, capturing more than a 31% share and holds US$ 0.5 Billion market value for the year.

The global C-arms market is experiencing significant growth driven by advancements in imaging technology and the increasing prevalence of chronic diseases requiring minimally invasive procedures. The demand for mobile C-arms is particularly rising due to their flexibility and wide application in orthopaedics, cardiology, and neurology.

Technological innovations, such as 3D imaging and AI-enabled systems, further enhance diagnostic accuracy and surgical precision, boosting market adoption. However, high equipment costs and stringent regulatory requirements pose challenges, particularly in developing regions with limited healthcare budgets. Additionally, the long lifecycle of C-arms reduces replacement frequency, slightly restraining market growth.

Moreover, collaborations between medical device manufacturers and healthcare providers are expanding access to advanced imaging systems in underserved regions, further driving market expansion.

Key Takeaways

- The global C-arms market was valued at USD 1.9 billion in 2024 and is anticipated to register substantial growth of USD 3.0 billion by 2034, with 4.7% CAGR.

- In 2024, the fixed segment took the lead in the global market, securing 48% of the total revenue share.

- The orthopaedics and trauma segment took the lead in the global market, securing 27% of the total revenue share.

- North America maintained its leading position in the global market with a share of over 31% of the total revenue.

Type Analysis

Based on type the market is fragmented into fixed and mobile. Amongst these, fixed dominated the global C-arms market capturing a significant market share of 48% in 2024. Fixed C-arms hold a significant share in the global C-arms market due to their advanced imaging capabilities and extensive applications in high-precision surgical and diagnostic procedures.

These systems are integral in hospitals and large healthcare facilities, where their superior image quality and reliability make them ideal for complex interventions such as cardiovascular, neurosurgical, and orthopaedic surgeries.

Their ability to provide continuous imaging during lengthy procedures and their integration with hybrid operating rooms further enhance their appeal. Technological advancements, including 3D imaging and real-time visualization, have solidified the dominance of fixed C-arms in delivering accurate diagnostics and better patient outcomes.

Application Analysis

The market is fragmented by application into orthopaedics and trauma, cardiology, neurology, gastroenterology, oncology, and others. Orthopaedics and trauma dominated the global C-arms market capturing a significant market share of 27% in 2024 due to the growing demand for advanced imaging solutions in minimally invasive and complex surgical procedures.

C-arms are widely used in orthopedic surgeries for fracture repairs, joint replacements, and spinal surgeries, providing real-time, high-resolution imaging to enhance surgical precision and reduce operating time. The increasing prevalence of musculoskeletal disorders, sports injuries, and road accidents has fuelled the need for reliable imaging systems in trauma care.

Mobile C-arms, with their flexibility and ease of use, have further boosted adoption in emergency and outpatient settings. According to statistics, Surgeons in the U.S. perform over 850,000 knee replacements and more than 450,000 hip replacements annually.

End Use Analysis

Based on end use the market is fragmented into hospitals, ambulatory surgical centers, and research institutions. Amongst these, hospitals dominated the global C-arms market capturing a significant market share of 46% in 2024 driven by their critical role in performing a wide range of diagnostic and surgical procedures requiring advanced imaging technologies. C-arms are indispensable in hospital settings for real-time imaging during orthopedic surgeries, cardiovascular interventions, and trauma care.

Their ability to provide precise, high-resolution images ensures better surgical outcomes, making them a preferred choice in hospitals. The growing prevalence of chronic diseases, such as cardiovascular and musculoskeletal disorders, has led to an increase in surgical procedures, further boosting the demand for C-arms. Additionally, the expansion of hospital infrastructure, particularly in emerging economies, and the integration of hybrid operating rooms are contributing to market growth.

Key Segments Analysis

By Type

- Fixed

- Mobile

- Full-Size C-arms

- Mini C-arms

By Application

- Orthopaedics and Trauma

- Cardiology

- Neurology

- Gastroenterology

- Oncology

- Others

By End Use

- Hospitals

- Ambulatory Surgical Centers

- Research Institutions

Drivers

Rising Prevalence of Chronic Diseases

The increasing prevalence of chronic diseases, such as cardiovascular disorders, cancer, and musculoskeletal conditions, is a significant driver of growth in the global C-arms market. These conditions often require advanced imaging technologies to facilitate accurate diagnosis, treatment planning, and surgical interventions, underscoring the critical role of C-arms in modern healthcare.

For instance, the rising incidence of coronary heart disease and circulatory disorders demands real-time imaging during complex procedures like angioplasties and stent placements. Similarly, the growing burden of orthopedic conditions, fueled by aging populations and lifestyle-related factors, has led to an increase in joint replacement and spinal surgeries that rely heavily on C-arms for precision.

- According to statistics published by the National Center for Chronic Disease Prevention and Health Promotion (NCCDPHP) in 2022, approximately six out of ten U.S. adults were affected by at least one chronic disease. Similarly, as per the U.K. Factsheet released in August 2022, 7.6 million people in the U.K. were living with heart or circulatory diseases. Among these, 2.3 million individuals were diagnosed with Coronary Heart Disease (CHD), including approximately 1.5 million men and 830,000 women.

Restraints

Refurbished Equipment may Limit Demand

Advancements in functionality and design, along with the continuous efforts of market players to introduce new products, have driven up the cost of C-arm systems. Many small and mid-sized healthcare facilities, with limited regular use of these systems, opt for more cost-effective options such as refurbished equipment. This preference has constrained the adoption of new imaging products. Additionally, the high cost of these systems, combined with the need for skilled professionals to operate them, has further restricted their adoption in low- and middle-income countries.

According to data from Block Imaging, Inc., as of January 2022, the market price for new ELITE CFD and CIOS ALPHA systems is over USD 200,000. In comparison, the refurbished models of these systems are priced around USD 70,000. This significant price difference often leads healthcare facilities to opt for the more economical refurbished options.

Opportunities

Technological Advancement

Technological advancements in the C-arms market are unlocking new growth opportunities by enhancing the efficiency, precision, and versatility of imaging systems. Innovations such as 3D imaging capabilities, AI-enabled systems, and improved radiation dose management have significantly improved the diagnostic and therapeutic utility of C-arms, driving their adoption in various medical procedures.

The integration of navigation systems and real-time imaging technologies is enabling greater accuracy in complex surgeries, such as spinal and cardiovascular interventions, thereby boosting demand. Mobile C-arms with compact designs and wireless connectivity are expanding their usability in outpatient settings and Ambulatory Surgery Centers (ASCs), further broadening their market scope.

- For example, in July 2022, Ziehm Imaging introduced the IGZO1 flat-panel detector for intraoperative imaging. This detector utilizes Indium Gallium Zinc Oxide (IGZO) technology, offering high-quality imaging while minimizing radiation dose levels.

Impact of macroeconomic factors / Geopolitical factors

Macroeconomic and geopolitical factors significantly influence the growth and dynamics of the C-arms market. Economic instability, inflation, and fluctuating exchange rates can affect healthcare budgets, particularly in developing nations, limiting investments in high-cost medical imaging equipment such as C-arms. Conversely, economic growth in emerging regions supports the expansion of healthcare infrastructure, driving demand for advanced imaging solutions.

Geopolitical tensions and trade restrictions can disrupt global supply chains, leading to delays in the production and distribution of C-arm systems. For example, shortages of critical raw materials or electronic components due to geopolitical conflicts can increase production costs and affect market pricing.

Trends

The C-arms market is evolving rapidly, driven by several key trends. One of the latest trends is the integration of Artificial Intelligence (AI) and Machine Learning (ML) for enhanced diagnostic accuracy and personalized treatment plans. These technologies enable apps to offer more precise symptom checkers, predictive analytics, and tailored health recommendations.

Another emerging trend is the expansion of telemedicine services, allowing users to consult healthcare professionals remotely, which has gained significant traction due to the ongoing demand for convenient, contactless care post-COVID-19. Additionally, the use of wearable devices and IoT (Internet of Things) integration is becoming more prevalent, enabling real-time health monitoring and data sharing between patients and healthcare providers. Mental health support through C-arms is also on the rise, addressing the growing need for psychological care.

Regional Analysis

In 2024, North America held a dominant position in the C-arms market, capturing more than a 31% share with a market value of US$ 0.5 billion. This prominence is largely due to the region’s advanced healthcare infrastructure. North American medical facilities extensively utilize cutting-edge imaging technologies, including C-arms, crucial for various diagnostic and surgical procedures. The high standard of healthcare services ensures broad adoption and integration of advanced medical equipment.

The region’s leadership is further supported by substantial healthcare expenditures. These investments focus not only on acquiring new equipment but also on updating existing technologies to enhance diagnostic and interventional capabilities. North America’s robust spending on healthcare facilitates the continual adoption of sophisticated technologies like C-arms, driving their market penetration and technological advancement.

North America also benefits from a strong presence of leading C-arms manufacturers and a supportive regulatory environment. This combination fosters rapid technological advancements and the availability of high-quality equipment. Additionally, the increasing demand for minimally invasive surgeries, driven by an aging population and the rising prevalence of chronic diseases, necessitates advanced imaging solutions. Such regulatory and demographic factors significantly contribute to maintaining North America’s leading position in the global C-arms market.

- For instance, in July 2022, FUJIFILM Holdings America Corporation launched the FDR Cross, a hybrid C-arm and X-ray solution that combines portable fluoroscopy and radiography imaging on a single platform. This innovation expanded FUJIFILM’s product portfolio and reinforced its market presence in the U.S.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The C-arms market is characterized by a diverse range of players, including established healthcare providers, tech companies, and startups, all vying to innovate and capture market share. Key players such as Amwell and Doctor on Demand offer comprehensive telemedicine services, including urgent care, with a focus on user-friendly interfaces, AI-driven diagnostics, and 24/7 access to healthcare professionals.

Emerging players are also leveraging advanced technologies like Artificial Intelligence, machine learning, and wearables to enhance diagnostic capabilities, improve patient outcomes, and increase app functionality. Additionally, partnerships between healthcare systems and tech companies are becoming common, as seen in collaborations like Cedars-Sinai’s launch of the Cedars-Sinai Connect mHealth app, which integrates AI for virtual care.

Allm Inc. is a leading provider of digital health solutions, focused on improving healthcare workflows and emergency response systems. The company specializes in developing healthcare communication platforms that enable real-time collaboration between healthcare providers, particularly in emergency and urgent care settings.

In addition, Twiage Solutions Inc. is a healthtech company focused on optimizing emergency medical response and Orthopaedics and Trauma care through digital solutions. Its platform, “Twiage,” provides real-time, secure communication between first responders, emergency medical technicians (EMTs), and hospitals, facilitating faster and more accurate patient information sharing.

Top Key Players in the C-arms Market

- GE Healthcare

- Koninklijke Philips N.V.

- Siemens Healthcare GmbH

- Canon Medical Systems Corporation

- Hologic, Inc.

- Shimadzu Corporation

- Ziehm Imaging GmbH

- FUJIFILM Corporation

- Genoray Co., Ltd.

- DMS Imaging

- Eurocolumbus s.r.l

Recent Developments

- In February 2024, Philips introduced the Philips Image Guided Therapy Mobile C-arm System 9000 – Zenition 90 Motorized. This system is designed to assist surgeons in delivering superior care to more patients.

- In June 2023, GE HealthCare formed a distribution partnership with DePuy Synthes, part of Johnson & Johnson’s orthopedics division. The agreement involves the integration of GE HealthCare’s OEC 3D Imaging System into DePuy Synthes’ broad product range, aiming to improve access for surgeons and patients throughout the U.S.

- In April 2022, Medtronic and GE HealthCare announced a partnership focused on meeting the unique needs of Ambulatory Surgery Centers (ASCs) and Office-Based Labs (OBLs). Through this collaboration, customers gain access to a wide range of products, tailored financial solutions, and exceptional service.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 1.9 billion |

| Forecast Revenue (2034) | US$ 3.0 billion |

| CAGR (2025-2034) | 4.7% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Fixed, Mobile), By Application (Orthopaedics and Orthopaedics and Trauma, Cardiology, Neurology, Gastroenterology, Oncology, and Others), By End Use (Hospitals, Ambulatory Surgical Centers, and Research Institutions). |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | GE Healthcare, Koninklijke Philips N.V., Siemens Healthcare GmbH, Canon Medical Systems Corporation, Hologic, Inc., Shimadzu Corporation, Ziehm Imaging GmbH, FUJIFILM Corporation, Genoray Co., Ltd., DMS Imaging, Eurocolumbus s.r.l. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |