Global Butyl Glycol Market Size, Share, And Business Benefits By Function (Solvent, Coalescing Aid, Chemical Intermediate, Plasticizer), By Application (Paints and Coatings, Drilling Stabilizers, Dyes, Printing Inks, Metalworking Fluids, Others), By End-use (Building and Construction, Chemicals, Electrical and Electronics, Agriculture, Cleaning, Oil and Gas, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2025-2034

- Published date: November 2025

- Report ID: 164953

- Number of Pages: 287

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

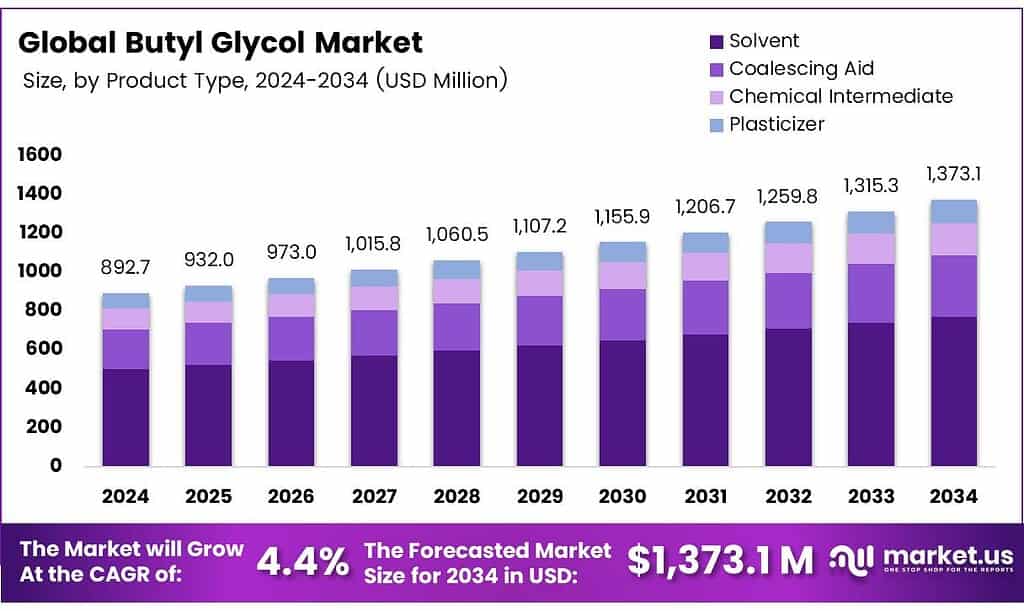

The Global Butyl Glycol Market size is expected to be worth around USD 1,373.1 Million by 2034, from USD 892.4 Million in 2024, growing at a CAGR of 4.4% during the forecast period from 2025 to 2034.

Butyl glycol, also known as 2-butoxyethanol, is a clear, colourless, oily liquid with the chemical formula C₆H₁₄O₂. It possesses a characteristic yet mild odour and is fully miscible with both water and common organic solvents. Commercially produced for decades, it finds its primary application in the paint industry, which accounts for approximately 75% of global consumption. Its low volatility makes it an ideal solvent for extending drying times of coatings while significantly improving their flow and overall finish.

Physically, butyl glycol presents as a clear and bright liquid, free from suspended matter, with a Platinum-Cobalt colour scale reading of 5. It contains minimal water content (285 mg/kg) and exhibits a density of 0.9002 kg/dm³ at 20°C, with a relative density of 0.9018 (20/20°C). The material achieves a purity of 99.4% B.G.E., with acidity measured at just 0.0026% as acetic acid.

Beyond paints, butyl glycol serves as an efficient flow improver in urea, melamine, and phenolic stoving finishes. It acts as a solvent in printing inks, textile dyes, hydraulic fluids, drilling and cutting oils, and is a major component of the oil spill dispersant Corexit 9527. As a chemical intermediate, it is a starting material for producing butyl glycol acetate, an excellent solvent in its own right, and various plasticisers through reaction with phthalic anhydride.

- Ethylene glycol is a colourless, odourless, sweet-tasting, viscous liquid widely recognised as the primary ingredient in antifreeze. It is also present in solvents, hydraulic brake fluids, de-icing solutions, detergents, lacquers, and polishes. Despite its innocuous appearance and taste, ethylene glycol poses severe health risks upon ingestion. The accepted minimum lethal dose for an adult is 100 mL (or 1–1.5 mL/kg).

Ethylene glycol itself is not inherently toxic; toxicity arises from its metabolic breakdown products. Alcohol dehydrogenase first oxidises it to glycoaldehyde, which aldehyde dehydrogenase quickly converts to glycolic acid. The subsequent slow conversion of glycolic acid to glyoxylic acid represents the rate-limiting step. Ultimately, the metabolism yields toxic end-products including oxalic acid, glycine, oxalomalic acid, and formic acid.

Key Takeaways

- The Global Butyl Glycol Market is expected to grow from USD 892.4 million in 2024 to USD 1,373.1 million by 2034 at a 4.4% CAGR (2025-2034).

- The Solvent segment dominates by function with a 56.3% share in 2024 due to superior solvency and a low evaporation rate.

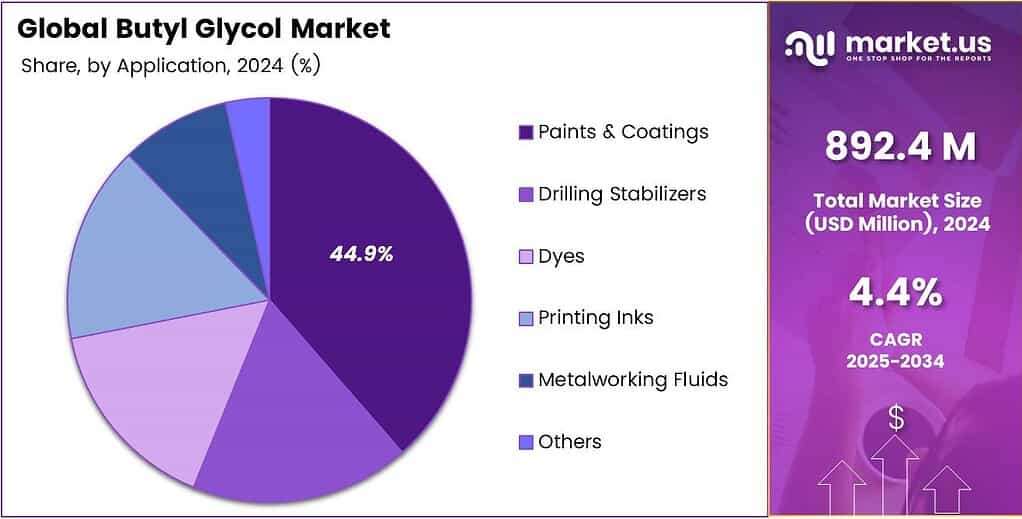

- Paints & Coatings lead applications with 44.9% market share in 2024, driven by urbanization and vehicle refinishing.

- Building & Construction is the top end-use segment at 33.2% share in 2024, fueled by mega projects in the Asia-Pacific and the Middle East.

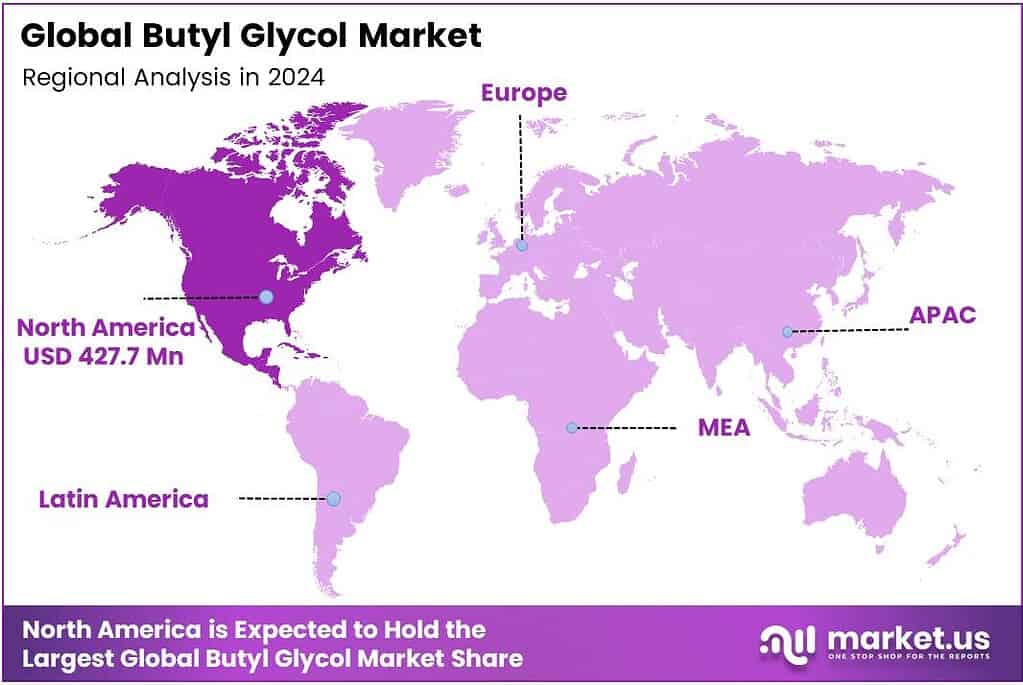

- North America commands 47.9% revenue share (USD 427.7 Mn) in 2024, led by a mature industrial base and advanced solvent formulations.

By Function Analysis

Solvent dominates with 56.3% due to its universal use across industries.

In 2024, Solvent held a dominant market position in the By Function Analysis segment of the Butyl Glycol Market, with a 56.3% share. This leadership stems from its excellent solvency power that dissolves resins, dyes, and oils effortlessly. Manufacturers prefer it in high-volume formulations, especially paints and inks, driving bulk consumption worldwide. Its low evaporation rate further boosts efficiency, keeping it ahead.

Coalescing Aid follows as a vital supporter in water-based coatings. It helps film formation at lower temperatures, reducing VOC emissions. Demand rises with eco-friendly regulations, yet it remains secondary to solvent applications. Chemical Intermediate plays a key role in producing esters and ethers.

Industries rely on it for downstream chemicals, but smaller volumes limit its share compared to direct-use functions. Plasticizer finds niche use in flexible PVC and adhesives. Though effective in improving workability, its limited scope keeps adoption lower than mainstream solvent roles.

By Application Analysis

Paints and Coatings dominate with 44.9% due to massive construction and automotive demand.

In 2024, Paints and Coatings held a dominant market position in the By Application Analysis segment of the Butyl Glycol Market, with a 44.9% share. Rising urbanization fuels architectural coatings, while vehicle refinishing adds volume. Its ability to control viscosity and improve flow makes it irreplaceable in both solvent-borne and water-borne systems.

Drilling Stabilizers gains traction in oilfield operations. It prevents shale swelling and maintains fluid stability under extreme conditions, supporting energy sector growth despite fluctuating crude prices. Dyes utilize butyl glycol for better color dispersion in textiles and printing inks. Steady demand from fashion and packaging keeps this segment active, though smaller than coatings.

By End-use Analysis

Building and Construction dominates with 33.2% powered by the global infrastructure boom.

In 2024, Building and Construction held a dominant market position in the By End-use Analysis segment of the Butyl Glycol Market, with a 33.2% share. Mega projects in the Asia-Pacific and the Middle East consume huge quantities of architectural paints, sealants, and floor coatings. Rapid urbanization and renovation trends sustain this lead year after year.

The chemicals sector uses it extensively for process solvents and intermediates. Specialty chemical manufacturers drive consistent offtake, forming a strong secondary base. Electrical and Electronics employs butyl glycol in cleaning formulations and circuit board coatings. Growth in consumer electronics supports steady demand, though volumes remain modest versus construction.

Key Market Segments

By Function

- Solvent

- Coalescing Aid

- Chemical Intermediate

- Plasticizer

By Application

- Paints and Coatings

- Drilling Stabilizers

- Dyes

- Printing Inks

- Metalworking Fluids

- Others

By End-use

- Building and Construction

- Chemicals

- Electrical and Electronics

- Agriculture

- Cleaning

- Oil and Gas

- Others

Emerging Trends

Shift toward Low-VOC & Water-borne Solvent Systems for Butyl Glycol in Coatings & Cleaning Applications

The increasing regulatory and market pressure is driving formulations toward low-volatile organic compound (VOC) and water-borne systems. This transition is significant because butyl glycol has historically been used as a high-performance solvent in coatings, inks, and cleaners thanks to its strong solvency power and compatibility. In the U.S., production of 2-butoxyethanol was estimated at approximately 408.5 million pounds.

Regulators are tightening limits on VOC content in coatings, which directly influences the solvent choices available to formulators. Solvent usage in decorative coatings was about 1.5 million tonnes annually, and stricter limits on VOC content were phased in. In U.S. jurisdictions such as the South Coast Air Quality Management District (SCAQMD), architectural flat coatings are aiming for VOC levels as low as 50 g/L.

- The U.S. Environmental Protection Agency (EPA) has documented significant reductions in facility releases of glycol ethers, with a 38% drop in on‐/off-site releases (from 26 million lb to 16 million lb) and a 55% drop in total waste managed (from 252 million lb to 113 million lb) for the category. This shows that implementation of source-reduction initiatives is well underway and that butyl glycol usage is being affected by these efforts.

Drivers

Expansion of Specialty Coatings & Cleaning Demand for Butyl Glycol

One of the strongest drivers behind the demand for solvents like 2‑Butoxyethanol (commonly referred to as butyl glycol) is the robust growth in specialty coatings and advanced cleaning applications. These end-uses benefit from butyl glycol’s strong solvency, wetting ability, and compatibility with water-borne systems, making it a preferred choice in high-performance applications.

- To put numbers on it: a detailed study reports that in Western Europe alone the total consumption of glycol ethers was 422 kilotonnes (kt), with the ethylene series accounting for 233 kt and the propylene series around 189 kt. Importantly, within that, surface coatings (as glycol ethers) made up 29% of the ethylene-series consumption (which would correspond to 67 kt) and 32% of the propylene-series 61 kt in the coatings segment.

It’s not simply about volume of general-use solvent, but about value and performance in specialty contexts. For companies tracking chemicals and materials, this is a meaningful lever: invest in solvent technologies that serve the reformulated coatings and cleaner markets, which in turn influence capacity, supply chains, and producer strategies.

Restraints

Tightening Exposure & VOC Rules Limit Butyl Glycol Use

The biggest restraint for butyl glycol (2-butoxyethanol) is the steady tightening of worker-exposure and VOC rules across major markets. Occupational limits make day-to-day formulations and plant operations harder, pushing buyers to consider lower-hazard substitutes. In the U.S., OSHA’s Permissible Exposure Limit (PEL) is 50 ppm (240 mg/m³) as an 8-hour TWA, while NIOSH’s Recommended Exposure Limit (REL) is far stricter at 5 ppm (24 mg/m³) with a skin notation meaning dermal uptake matters.

Beyond the plant floor, environment-facing policies are reshaping solvent choices. The EU’s coatings VOC framework sets category-specific g/L caps and mandatory VOC labelling, which relentlessly drives coatings producers toward water-borne and low-VOC systems less room for conventional glycol ether loads in many decorative and refinishing products.

- U.S. environmental programs add more pressure. EPA’s TRI and P2 data show companies have already cut glycol-ether releases by 38% (26 million lb → 16 million lb) and reduced production-related waste by 55% (252 million lb → 113 million lb), a clear signal that sustained source-reduction and substitution are underway. When large facilities redesign processes to meet these targets, upstream demand for classic solvent packages, including butyl glycol, gets squeezed.

Opportunity

Surge in Infrastructure & Urban Hygiene Projects Fueling Butyl Glycol Demand

The chemical solvent 2‑Butoxyethanol is seeing notable growth potential as global infrastructure, coatings, and sanitation initiatives ramp up. A key driver is the massive push in water-borne or low-VOC coatings used in building, industrial, and infrastructure projects, a space where butyl glycol remains relevant as a coalescent or performance solvent in reformulated systems.

Global vehicle production alone surpassed 92 million units in 2024, the International Organization of Motor Vehicle Manufacturers (OICA). Since every vehicle needs coatings, adhesives, sealants, and cleaning, this gives a sense of the underlying volume of downstream demand for advanced solvent systems that may use butyl glycol.

- On the broader infrastructure and hygiene front, about 57% of the world’s population, 4.6 billion people, used safely-managed sanitation services, meaning 3.5 billion people still lacked access, driving renovation, new builds, institutional cleaning, and coatings requirements in emerging markets. The United Nations Sustainable Development Goal 6 emphasises clean water and sanitation for all and encourages upgraded sanitation infrastructure.

Regional Analysis

North America leads with a 47.9% share and a USD 427.7 Million market value.

In 2024, North America held a dominant position in the global Butyl Glycol Market, accounting for 47.9% of total revenue, valued at USD 427.7 million. The region’s leadership stems from its mature industrial base, extensive coatings and cleaning manufacturing network, and ongoing technological advancements in solvent formulations.

The United States represents the key contributor within the region, supported by well-established sectors including construction, automotive, paints & coatings, and institutional cleaning. Butyl glycol serves as a critical solvent in water-borne coatings and surface cleaners, which are widely used across these industries for their excellent solvency, low volatility, and biodegradability.

The increasing adoption of eco-friendly coatings and low-VOC cleaning solutions further reinforces the regional market. Regulatory bodies such as the U.S. Environmental Protection Agency (EPA) and the Canadian Environmental Protection Act (CEPA) promote cleaner industrial practices, encouraging manufacturers to reformulate solvents while maintaining product performance.

Additionally, robust demand from automotive refinishing, industrial cleaners, and personal-care formulations continues to strengthen the market outlook. Local producers such as Dow, Eastman Chemical Company, and LyondellBasell Industries have expanded product lines, integrating butyl glycol into value-added formulations, further anchoring the region’s dominance.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

BASF is a dominant force in the butyl glycol market. Its strength lies in its integrated value chain, extensive production capacity, and worldwide distribution network. BASF leverages its strong R&D capabilities to serve diverse downstream sectors, including paints, coatings, and cleaning products. The company’s global presence and consistent product quality make it a preferred and reliable supplier for industrial customers.

Eastman Chemical Company is a major, technologically advanced producer of butyl glycol. The company differentiates itself through a focus on product purity, specialty applications, and sustainable solutions. Eastman’s robust manufacturing processes and strategic supply chain ensure consistent availability for key markets. It’s strong customer focus and ability to provide tailored solutions for high-performance coatings.

Dow is a pivotal player with a formidable position in the butyl glycol market, underpinned by its massive production scale and vertical integration. As a leading petrochemical company, Dow benefits from direct access to raw materials, ensuring a cost-efficient and stable supply. Its vast global infrastructure and strong brand reputation make it a go-to source for large-volume buyers in the construction.

Top Key Players in the Market

- BASF

- Eastman

- Dow Chemicals

- Asia Pacific Petrochemicals Co. Ltd.

- Anshika Polysurf Ltd.

- Nippon Nyukazai Co., Ltd.

- Sasol Ltd.

- Eastman Chemical Corporation

- INEOS

- Solventis Ltd

Recent Developments

- In 2024, BASF has made significant advancements in production capacities related to butyl glycol (2-butoxyethanol) precursors and downstream chemicals, primarily through its Zhanjiang Verbund site in China. Successful start-up of the butyl acrylate (BA), with mechanical completion of the steam cracker and all integrated petrochemical plants.

- In 2024, Eastman continues to produce and supply 2-butoxyethanol (Eastman EB Solvent) as a standard solvent for paints, coatings, and cleaners. Announced a price increase for NPG (neopentyl glycol) products, effective due to rising raw material and energy costs. NPG is used in coatings alongside glycol ethers, but not directly butyl glycol.

Report Scope

Report Features Description Market Value (2024) USD 892.4 Million Forecast Revenue (2034) USD 1,373.1 Million CAGR (2025-2034) 4.4% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Function (Solvent, Coalescing Aid, Chemical Intermediate, Plasticizer), By Application (Paints and Coatings, Drilling Stabilizers, Dyes, Printing Inks, Metalworking Fluids, Others), By End-use (Building and Construction, Chemicals, Electrical and Electronics, Agriculture, Cleaning, Oil and Gas, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape BASF, Eastman, Dow Chemicals, Asia Pacific Petrochemicals Co. Ltd., Anshika Polysurf Ltd., Nippon Nyukazai Co. Ltd., Sasol Ltd., Eastman Chemical Corporation, INEOS, Solventis Ltd Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- BASF

- Eastman

- Dow Chemicals

- Asia Pacific Petrochemicals Co. Ltd.

- Anshika Polysurf Ltd.

- Nippon Nyukazai Co., Ltd.

- Sasol Ltd.

- Eastman Chemical Corporation

- INEOS

- Solventis Ltd

Our Clients

- 164953

- November 2025