Quick Navigation

Report Overview

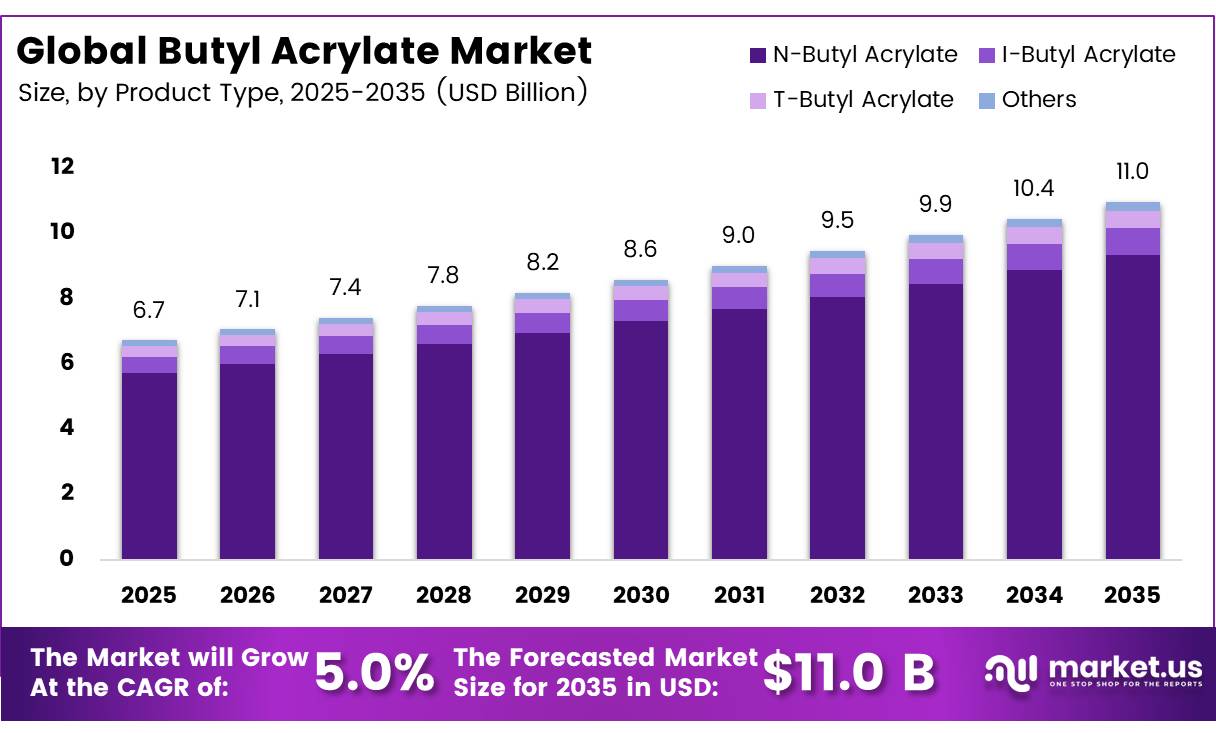

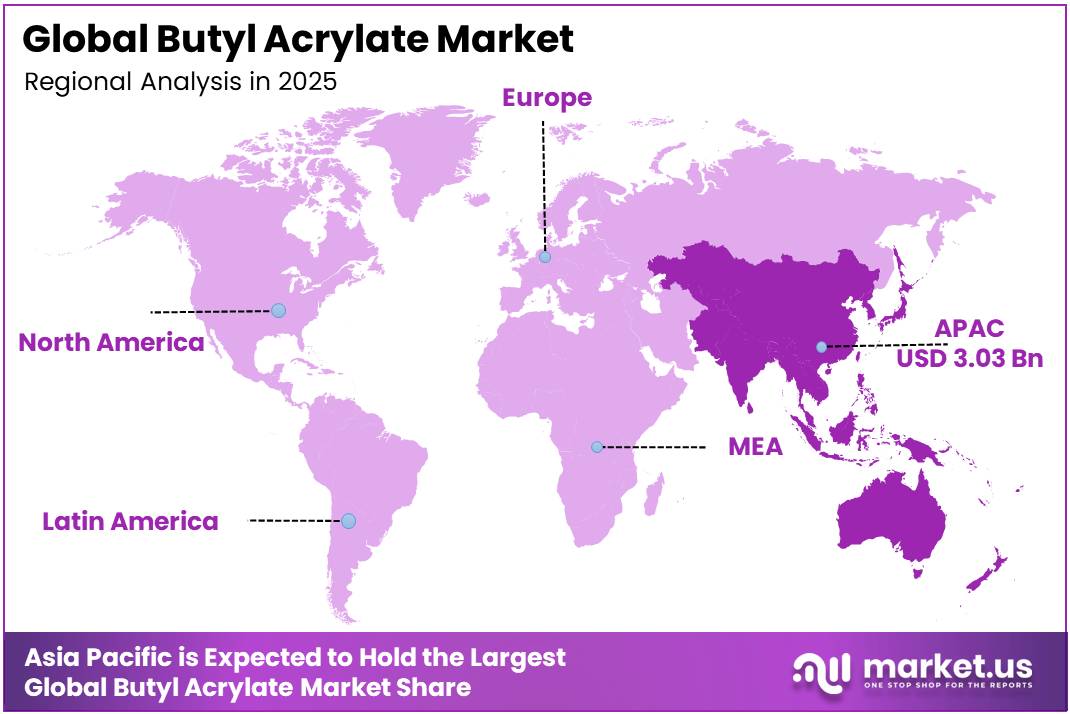

In 2025, the Global Butyl Acrylate Market was valued at USD 6.7 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 5.0%, reaching about USD 11.0 billion by 2035. In 2025, Asia Pacific led the market, achieving over 45.1% share with a revenue of USD 3.03 Billion.

Butyl acrylate is an important acrylic ester widely used in the production of water-based coatings, adhesives, sealants, textiles, plastics, and construction materials. The chemical is valued for its flexibility, weather resistance, adhesion properties, and ability to improve the performance of polymer formulations. Industrial demand is closely linked to growth in construction, automotive manufacturing, packaging, and infrastructure development. The industrial landscape for butyl acrylate is supported by rising production of paints and coatings, which remains one of the largest application segments for acrylic chemistry.

- According to the World Coatings Council’s Global Market Analysis, the global paints and coatings industry reached approximately 48.9 billion liters in 2024 and was valued at around US$202 billion, reflecting sustained demand for acrylic monomers such as butyl acrylate used in architectural, industrial, and protective coating formulations.

Key Takeaways

- The Global Butyl Acrylate Market was valued at USD 6.7 billion in 2025.

- The market is projected to grow at a CAGR of 5.0% and is estimated to reach USD 11.0 billion by 2035.

- On the basis of product type, N-Butyl dominated the Butyl Acrylate market, constituting 85.1% of the total market share.

- Based on the purity, the Common Purity (>99%) dominated the Butyl Acrylate market, with a substantial market share of around 85.4%.

- Based on the Applications, paints & coatings led the market, comprising 55.6% of the total market.

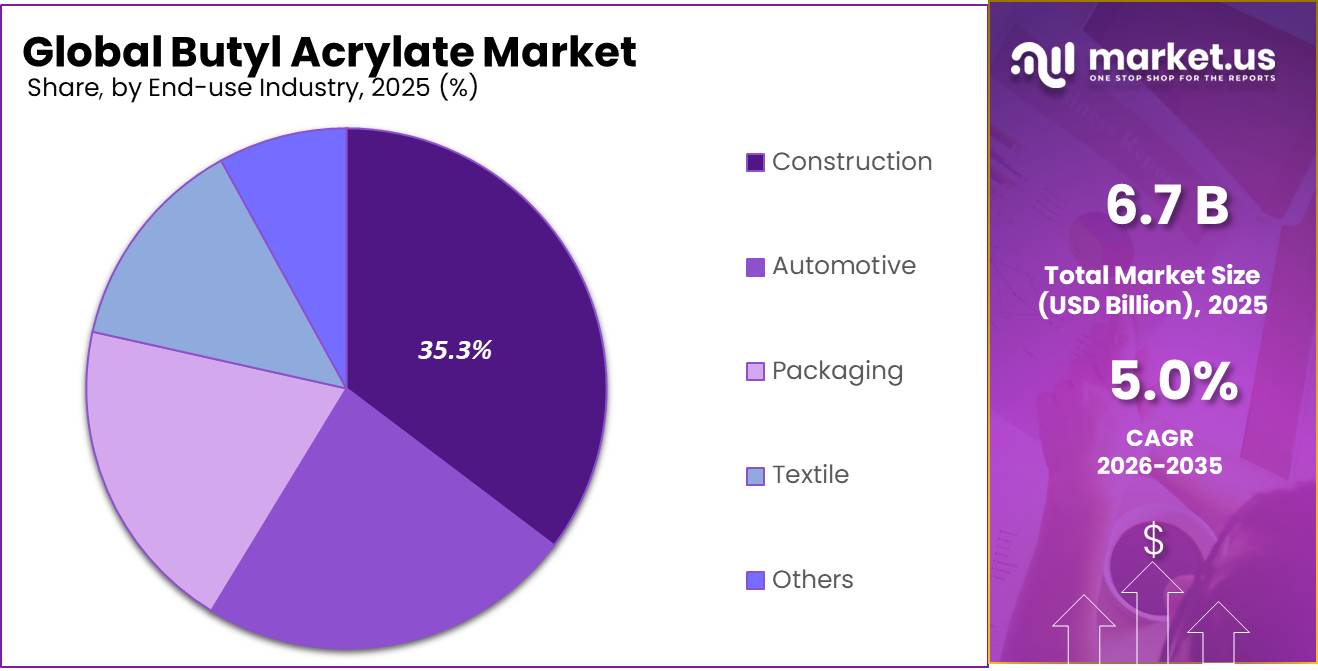

- Among the End Use, the Construction is the most considerable within the Butyl Acrylate market, accounting for around 35.3% of the revenue.

- In 2025, the Asia Pacific was the most dominant region in the Butyl Acrylate market, accounting for 45.1% of the total global consumption.

The European Commission’s Green Deal and industrial decarbonization programs are accelerating the adoption of environmentally friendly coating technologies and high-performance materials. Meanwhile, the U.S. Department of Energy has announced billions of dollars in funding for clean manufacturing and industrial modernization projects, encouraging innovation in specialty chemicals and polymer production.

The increasing preference for waterborne coatings, lightweight automotive components, high-performance adhesives, and durable packaging materials is expected to create long-term opportunities for butyl acrylate producers. As industrial production, urbanization, and sustainable construction continue to expand globally, the industry is expected to maintain a positive growth trajectory supported by strong downstream demand and ongoing technological advancements.

Butyl Acrylate Market Segment

Product Type Analysis

N-Butyl Acrylate represents dominant segment in the Butyl Acrylate Market

In 2025, N-Butyl Acrylate held a dominant market position, capturing more than an 85.1% share of the global Butyl Acrylate market. Its leading position was supported by extensive usage across paints, coatings, adhesives, sealants, textiles, and construction materials. The product is widely preferred because it offers excellent flexibility, durability, weather resistance, and adhesion performance, making it suitable for a wide range of industrial applications.

I-Butyl Acrylate is the fastest growing segment in the Butyl Acrylate market during 2025 and 2026. Growth has been supported by increasing use in specialty coatings, pressure-sensitive adhesives, and advanced polymer formulations that require enhanced performance characteristics. The segment is gaining attention from manufacturers seeking materials with improved flexibility, chemical resistance, and formulation versatility. Rising development of high-value industrial products and specialty chemical applications has further contributed to demand growth.

Purity Analysis

Common Purity (>99%)) Are the Most Widely Used Purity.

In 2025, Common Purity (>99%) held a dominant market position, capturing more than an 85.4% share of the Butyl Acrylate market. Its strong market presence was driven by extensive use across paints, coatings, adhesives, sealants, and general-purpose polymer manufacturing. Manufacturers continued to prefer this purity grade because it delivers reliable performance while maintaining cost efficiency for large-scale industrial applications. The grade remained the standard choice for high-volume production processes where consistent quality and operational efficiency were key requirements.

High Purity (>99.5%) is the fastest growing segment in the Butyl Acrylate market during 2025 and 2026. Growth is being supported by increasing demand from specialty coatings, advanced adhesives, high-performance polymers, and other applications that require tighter quality specifications. End users are showing greater interest in premium-grade materials to improve product consistency and meet stringent performance requirements. The segment is also benefiting from ongoing advancements in chemical processing and the growing focus on high-value industrial products.

Application Analysis

Paints and Coatings is a significant application .

In 2025, Paints and Coatings held a dominant market position, capturing more than a 55.6% share of the Butyl Acrylate market. The segment’s leadership was supported by the extensive use of butyl acrylate in architectural, decorative, industrial, and protective coating formulations. Manufacturers continued to utilize the material because it enhances flexibility, durability, weather resistance, and surface adhesion in coating products. Rising construction activities, infrastructure upgrades, and renovation projects across various regions further contributed to steady demand.

Adhesives and Sealants is the fastest growing segment in the Butyl Acrylate market during 2025 and 2026. Growth is being driven by increasing use of high-performance bonding materials across construction, packaging, automotive, and consumer goods industries. Butyl acrylate is widely valued in adhesive and sealant formulations for providing flexibility, strong bonding strength, and long-term durability. Manufacturers are increasingly adopting advanced adhesive technologies as a replacement for traditional fastening methods in several industrial processes.

End-Use Industry Analysis

Butyl Acrylate Are Mostly Utilized in Construction.

In 2025, Construction held a dominant market position, capturing more than a 35.3% share of the Butyl Acrylate market. The segment maintained its leadership due to the widespread use of butyl acrylate in architectural coatings, waterproofing materials, sealants, adhesives, and other building products. The material is highly valued for its durability, flexibility, weather resistance, and strong bonding properties, making it suitable for both residential and commercial construction projects.

Automotive is the fastest growing segment in the Butyl Acrylate market during 2025 and 2026. Growth is being fueled by the increasing use of advanced coatings, adhesives, sealants, and specialty polymer materials in vehicle manufacturing. Automakers are focusing on lightweight designs, improved durability, and enhanced vehicle performance, which has increased the demand for acrylic-based materials. Butyl acrylate plays an important role in automotive coating systems by providing flexibility, impact resistance, and long-lasting surface protection.

Key Market Segments

By Product Type

- N-Butyl Acrylate

- I-Butyl Acrylate

- T-Butyl Acrylate

- Others

By Purity

- Common Purity (>99%)

- High Purity (>99.5%)

By Application

- Paints and Coatings

- Adhesives and Sealants

- Textiles

- Plastic Additives

- Chemical Synthesis

- Others

By End-Use Industry

- Construction

- Automotive

- Packaging

- Textile

- Others

Driver Analysis

Waterborne coatings shift

Butyl acrylate remains structurally tied to coatings because EPA product-use categories place the substance in paints, coatings, primers, sealants, and related architectural formulations, which means every policy or procurement shift toward lower-emission, waterborne, and higher-durability coating systems directly lifts butyl acrylate consumption intensity in downstream latex and acrylic binder systems.

In practical commercial terms, this driver supports mix-shift from solvent-heavy formulations toward emulsion systems where butyl acrylate improves flexibility, film formation, adhesion, and weatherability, allowing formulators to meet performance targets without fully sacrificing low-temperature application properties; that is why this driver is assigned the highest incremental CAGR effect at about +1.4 percentage points.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Waterborne coatings shift | +1.4% | North America core, EU, China, India urban corridors | Medium term (2-4 years) |

| Construction chemicals pull | +1.1% | APAC core, Middle East build-out, North America spill-over | Short term (≤ 2 years) |

| Adhesives & packaging conversion | +0.9% | North America, EU, ASEAN manufacturing belts | Medium term (2-4 years) |

| Supply-chain normalization in acrylates | +0.8% | China export base, US import market, EU balancing zones | Short term (≤ 2 years) |

| Regulatory-compliance driven reformulation | +0.7% | EU core, US specialty applications, advanced Asia markets | Medium term (2-4 years) |

| Asset flexibility after US air-rule reset | +0.5% | United States core, North America derivatives chain | Short term (≤ 2 years) |

Restraint Analysis

Hazard-compliance burden

A third restraint is regulatory and stewardship cost, since ECHA’s chemical profile for butyl acrylate shows harmonized classification including Skin Irrit. 2, Eye Irrit. 2, STOT SE 3, and Skin Sens. 1, while OECD and related occupational reviews continue to note irritation and sensitization concerns plus workplace concentration controls such as a 2 ml/m3 MAK value in Germany, all of which raise documentation, labeling, storage, PPE, and exposure-control requirements across the value chain.

The burden becomes more commercially significant in 2026 because from 1 July 2026 ECHA starts publishing notifier names in the C&L Inventory unless confidentiality justifications were submitted by 30 June 2026, increasing scrutiny of classification choices and effectively raising the cost of weak dossier governance. The practical result is not demand destruction in absolute terms but slower customer onboarding, higher compliance overhead per SKU, and more reformulation work for small and mid-sized downstream users, which together justify a modeled -0.9 percentage-point reduction in CAGR, most visible in the EU and highly regulated specialty applications.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acrylic ester trade case | -1.3% | EU core, US-China-Saudi-South Africa export lanes | Short term (≤ 2 years) |

| Feedstock-cost volatility | -1.1% | North America core, EU import base, APAC corridors | Short term (≤ 2 years) |

| Hazard-compliance burden | -0.9% | EU core, North America specialty chain, advanced Asia | Medium term (2-4 years) |

| Weak chemical operating rates | -0.8% | North America core, EU manufacturing belt | Short term (≤ 2 years) |

| Energy and utility inflation | -0.7% | Europe core, North America spill-over, Northeast Asia | Medium term (2-4 years) |

| Insurance and handling friction | -0.5% | Global traded market, ports and storage hubs | Medium term (2-4 years) |

Opportunity Analysis

Roll-up of niche acrylic formulators

This is an opportunity because industry growth today is still largely driven by broad end-use demand, whereas the untapped upside comes from changing the value-capture point through M&A or distribution-led roll-ups of niche formulators in coatings, sealants, and adhesives that already know how to convert BA into specialized systems. The economic logic is strengthened by the scale of end-market fragmentation and public construction/retrofit volume: U.S. private construction alone was running at $1,639.7 billion annualized in April 2026, residential at $909.9 billion, and public construction at $532.7 billion, which supports many small regional formulators but also leaves room for consolidation and cross-selling.

For a monomer supplier, buying or partnering with downstream formulators can increase wallet share per customer by 1.5x to 3x, protect against commodity price cycles, and improve EBITDA resilience through formulation, application testing, and local specification access; that is why a seemingly modest +0.6 percentage-point CAGR upside can still be highly attractive on a risk-adjusted basis, because the margin capture often exceeds the tonnage gain.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Biobased BA premium grades | +1.6% | North America core, EU specialty markets, Japan-Korea | Medium term (2-4 years) |

| Renovation-grade binder systems | +1.3% | EU core, North America retrofit belt, developed APAC | Medium term (2-4 years) |

| Battery-adjacent adhesive entry | +1.1% | North America core, EU cell corridors, Northeast Asia | Short term (≤ 2 years) |

| Low-migration packaging systems | +0.9% | EU, North America food-contact chain, ASEAN export hubs | Medium term (2-4 years) |

| Compliance-as-a-product model | +0.7% | EU core, advanced Asia, global multinationals | Short term (≤ 2 years) |

| Roll-up of niche acrylic formulators | +0.6% | North America, EU, India specialty pockets | Medium term (2-4 years) |

Challenges Analysis

Volatile QC compliance cycles

The first systemic challenge is the on–off pattern of quality‑control enforcement in key importing markets, which does not freeze current sales but creates recurring friction and planning noise: India’s Ministry of Chemicals and Fertilizers temporarily suspended mandatory compliance with the n‑Butyl Acrylate (Quality Control) Order, 2021 from 10 April to 10 July 2026 via S.O. 1854(E), explicitly citing global supply chain disruptions and the need to ensure uninterrupted availability for industrial users, and BIS-standard conformity is expected to be reinstated after that window.

This kind of policy oscillation forces producers and traders to maintain dual documentation tracks, revalidate buyers after each regulatory inflection, hold buffer inventories ahead of re‑tightening, and keep contract tenors short, adding 3 to 7 days to normal shipment‑to‑release cycles and lifting working‑capital requirements by 5% to 10% for smaller distributors that must bridge uncertain QC enforcement periods. Over a 2‑4 year horizon, the result is an estimated -1.1 percentage‑point CAGR friction drag as BA suppliers divert management bandwidth to navigating compliance cycles, accept sub‑optimal asset utilization to hedge regulatory timing risk, and face occasional customer hesitation about committing to local manufacturing projects when standards regimes appear volatile rather than consistently predictable.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Volatile QC compliance cycles | -1.1% | India, APAC logistics corridors | Medium term (2-4 years) |

| TSCA new-chemical burden | -1.0% | US regulatory hubs, North America core | Long term (≥ 4 years) |

| Regulatory capacity strain | -0.9% | US, EU oversight bodies | Long term (≥ 4 years) |

| China overcapacity exposure | -0.8% | Global traded market, EU import hubs | Medium term (2-4 years) |

| Logistics and supply fragility | -0.7% | APAC–EU–India corridors | Medium term (2-4 years) |

| Skills and safety enforcement gap | -0.6% | Emerging manufacturing belts | Long term (≥ 4 years) |

Geopolitical Impact Analysis

Ongoing Middle East Tensions and Trade Disruptions Reshape Butyl Acrylate Supply Chains.

The current Butyl Acrylate market is experiencing the effects of ongoing geopolitical tensions, particularly the conflict in the Middle East and continued disruptions across major global shipping routes. Since butyl acrylate is produced from petrochemical feedstocks, any instability affecting crude oil and downstream chemical supply chains has a direct impact on production costs and market dynamics. Concerns over energy security and transportation risks have increased uncertainty for chemical manufacturers and buyers worldwide.

The disruption of shipping activities in and around key maritime corridors has led to longer transit times, higher freight costs, and occasional delays in raw material deliveries. As a result, several chemical producers have adjusted procurement strategies by increasing inventory levels and diversifying sourcing locations to reduce supply risks. These actions have helped maintain supply continuity but have also increased operational expenses.

Regional Analysis

Asia-Pacific Leads the Butyl Acrylate Market with Strong Industrial and Manufacturing Demand.

In 2025, Asia-Pacific held the dominant position in the global Butyl Acrylate market, accounting for 45.1% of the total market and reaching a value of USD 3.03 billion. The region’s leadership is supported by its large-scale chemical manufacturing base, expanding construction activities, and strong demand from coatings, adhesives, sealants, textiles, and automotive industries. Countries across the region continue to invest heavily in infrastructure development, industrial production, and urban expansion, creating sustained consumption of acrylic-based materials.

North America is expected to witness the fastest growth in the global Butyl Acrylate market during the forecast period, supported by increasing demand from the construction, automotive, packaging, and specialty coatings industries. The United States remains the primary growth engine in the region, driven by rising investments in infrastructure modernization and industrial manufacturing. North America is positioned to achieve robust growth and expand its share in the global Butyl Acrylate market over the coming years.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global Butyl Acrylate market exhibits a moderately consolidated and oligopolistic structure, where a small group of large chemical manufacturers accounts for a significant share of global production. High capital investment requirements, complex production processes, and the need for secure raw material supply create barriers for new entrants, allowing established companies to maintain strong market positions.

Among the leading participants, BASF SE, The Dow Chemical Company, and Arkema S.A. remain some of the most influential global players in the Butyl Acrylate industry. These companies operate extensive manufacturing networks and serve a broad range of end-use sectors worldwide. Their competitive strength comes from strong research capabilities, large-scale production facilities, and continuous investments in sustainable chemical solutions.

The Major Players In The Industry

- BASF SE

- The Dow Chemical Company

- Arkema S.A.

- Nippon Shokubai Co., Ltd.

- Mitsubishi Chemical Group Corporation

- LG Chem Ltd.

- Sasol Limited

- Wanhua Chemical Group Co., Ltd.

- Formosa Plastics Corporation

- SIBUR Holding PAO

- Evonik Industries AG

- China Petroleum and Chemical Corporation (Sinopec)

- PetroChina Company Limited

- Shanghai Huayi Acrylic Acid Co., Ltd.

- Zhejiang Satellite Petrochemical Co., Ltd.

- Synthomer Plc

- TOAGOSEI Co., Ltd.

- Jiangsu Jurong Chemical Co., Ltd.

- Shenyang Chemical Co., Ltd.

- Kaitai Industrial Co., Ltd.

- Others

Key Development

- In July 2025, BASF completed mechanical work on its acrylic acid and butyl acrylate plants at the Zhanjiang Verbund site in China. The site is part of BASF’s EUR 10 billion investment plan and supports long-term acrylic monomer supply in Asia.

- In March 2026, Zhejiang Satellite Petrochemical started planned maintenance for its 270,000-ton acrylic acid plant and 200,000-ton butyl acrylate plant. This routine turnaround helped maintain long-term supply consistency and production performance across the value chain for downstream applications like paints, coatings, adhesives, sealants, and construction chemicals.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 6.7 Bn |

| Forecast Revenue (2035) | USD 11.0 Bn |

| CAGR (2026-2035) | 5.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (N-Butyl Acrylate, I-Butyl Acrylate, T-Butyl Acrylate, and Others), By Purity (Common Purity (>99%) and High Purity (>99.5%)), By Application (Paints and Coatings, Adhesives and Sealants, Textiles, Plastic Additives, Chemical Synthesis, and Others), By End-Use Industry (Construction, Automotive, Packaging, Textile, and Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | BASF SE, The Dow Chemical Company, Arkema S.A., Nippon Shokubai Co., Ltd., Mitsubishi Chemical Group Corporation, LG Chem Ltd., Sasol Limited, Wanhua Chemical Group Co., Ltd., Formosa Plastics Corporation, SIBUR Holding PAO, Evonik Industries AG, China Petroleum and Chemical Corporation (Sinopec), PetroChina Company Limited, Shanghai Huayi Acrylic Acid Co., Ltd., Zhejiang Satellite Petrochemical Co., Ltd., Synthomer Plc, TOAGOSEI Co., Ltd., Jiangsu Jurong Chemical Co., Ltd., Shenyang Chemical Co., Ltd., Kaitai Industrial Co., Ltd., Others. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |