Quick Navigation

Report Overview

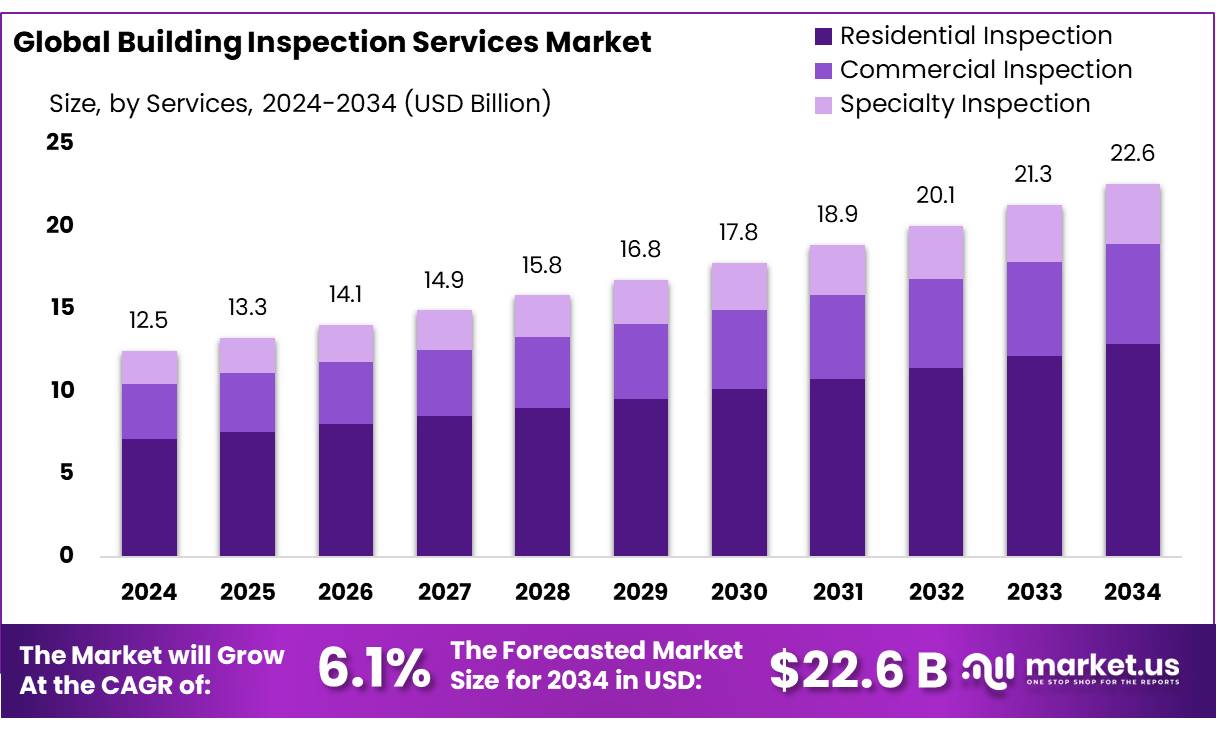

The Global Building Inspection Services Market size is expected to be worth around USD 22.6 Billion by 2034, from USD 12.5 Billion in 2024, growing at a CAGR of 6.1% during the forecast period from 2025 to 2034.

The global building inspection services market plays a pivotal role in ensuring the safety, compliance, and sustainability of infrastructure within the construction and real estate sectors. These services involve testing, inspection, and certification (TIC) to verify structural integrity, energy efficiency, and adherence to regulatory standards. As urbanization accelerates and sustainability becomes a priority, the demand for building inspection services is witnessing significant growth, particularly in industrial and commercial applications.

The industrial scenario reflects a dynamic landscape driven by global infrastructure development and energy efficiency mandates. According to the International Energy Agency (IEA), buildings account for approximately 30% of global final energy consumption and 26% of energy-related CO2 emissions in 2022, underscoring the need for inspections to enhance energy performance. In the United States, the Department of Energy (DOE) emphasizes decarbonizing buildings by 2050, with inspection services integral to validating energy-efficient technologies.

Key driving factors include regulatory compliance, technological advancements, and sustainability goals. Government initiatives, such as India’s National Infrastructure Pipeline (NIP) with $1.5 trillion allocated for 7,400 projects by 2025, mandate rigorous inspections to ensure safety and quality. The adoption of digital tools like drones and AI, noted in 37% of construction sites globally, enhances inspection precision and efficiency. Additionally, the shift toward proactive inspections, driven by the need to prevent costly repairs, is reshaping service models.

Future growth opportunities lie in integrating advanced technologies and addressing energy transition demands. The IEA projects that renewable energy capacity, including solar and wind, will require inspections for supporting infrastructure, with global additions reaching 560 GW in 2023. Smart city initiatives, such as India’s 100 Smart Cities project mandating 10% renewable energy use, create avenues for specialized inspections, organizations prioritize net-zero targets, building inspection services will expand into energy audits and retrofitting, ensuring compliance with evolving standards and fostering sustainable urban development.

Key Takeaways

- Building Inspection Services Market size is expected to be worth around USD 22.6 Billion by 2034, from USD 12.5 Billion in 2024, growing at a CAGR of 6.1%.

- Residential Inspection held a dominant market position, capturing more than a 57.3% share in the Building Inspection Services market.

- In-House Services held a dominant market position, capturing more than a 58.5% share in the Building Inspection Services market.

- Traditional Inspection held a dominant market position, capturing more than a 63.9% share in the Building Inspection Services market.

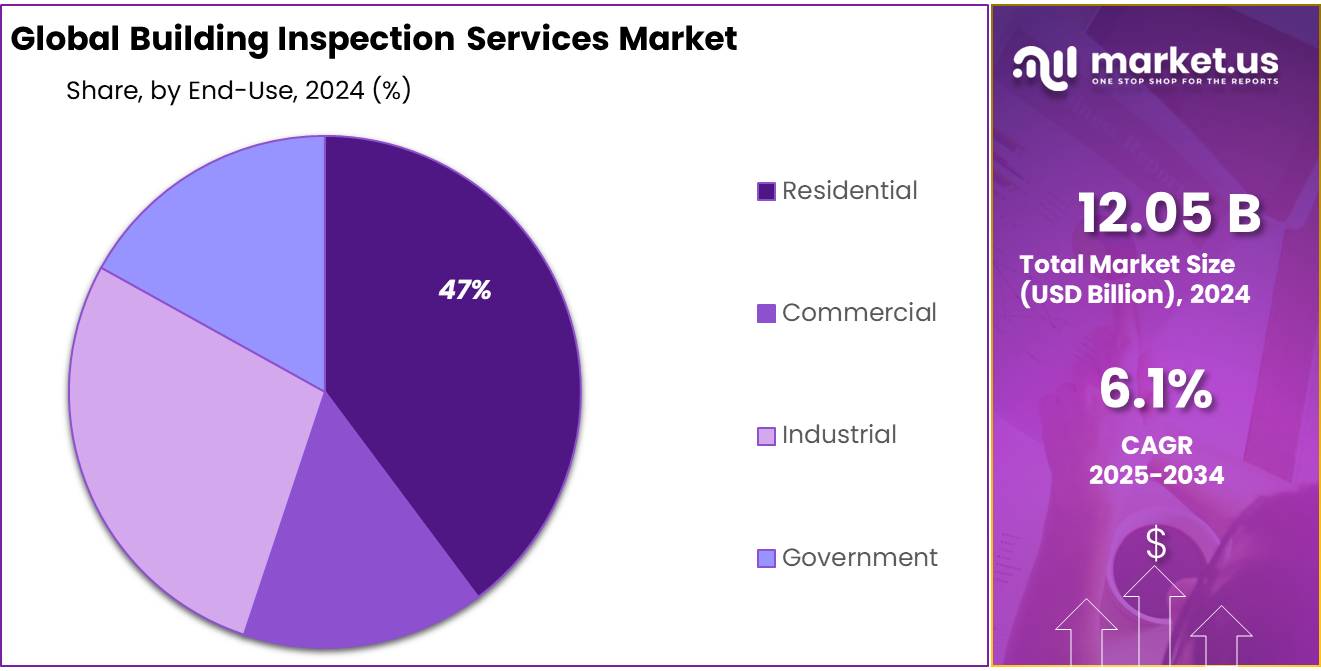

- Residential held a dominant market position, capturing more than a 47.7% share in the Building Inspection Services market.

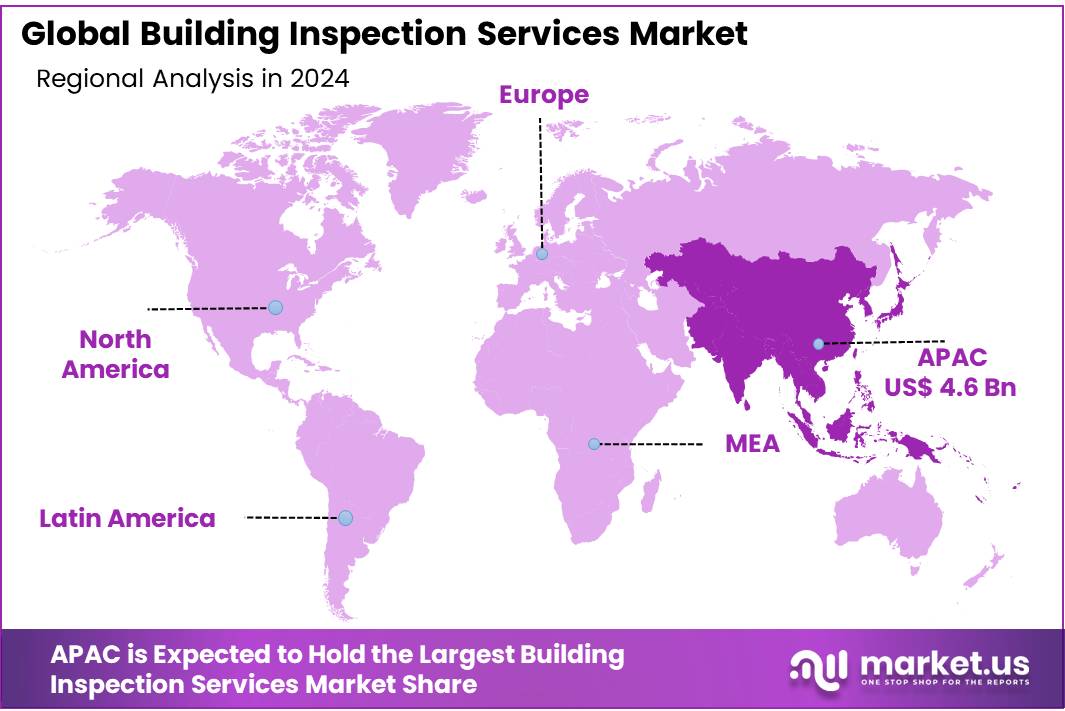

- Asia-Pacific (APAC) region emerged as the dominant force in the global building inspection services market, commanding a substantial 38.6% share, equivalent to approximately USD 4.6 billion.

By Services

Residential Inspection Captures 57.3% Share, Leading the Building Inspection Services Market

In 2024, Residential Inspection held a dominant market position, capturing more than a 57.3% share in the Building Inspection Services market. The segment’s prominence was driven by increasing awareness of property maintenance and regulatory compliance among homeowners, especially in urban areas. Rising property transactions further fueled demand for residential inspections, particularly in regions experiencing rapid urbanization and real estate development. Additionally, the focus on structural integrity assessments and safety checks contributed significantly to the segment’s substantial share. As property sales surged, the need for pre-sale inspections remained a critical factor, positioning residential inspection services as a key growth driver in the market.

By Sourcing Type

In-House Services Lead with 58.5% Share, Driving Market Growth

In 2024, In-House Services held a dominant market position, capturing more than a 58.5% share in the Building Inspection Services market. The segment’s leadership was largely attributed to businesses preferring to maintain control over inspection processes, ensuring compliance and consistency. Companies with extensive property portfolios prioritized in-house services to minimize third-party costs and maintain stringent quality checks. Additionally, the growing emphasis on regular building maintenance and safety assessments further bolstered the demand for in-house inspection teams. The rising trend of integrating digital tools for real-time reporting and data analysis also supported the segment’s substantial market share.

By Technology

Traditional Inspection Secures 63.9% Share, Maintaining Market Dominance

In 2024, Traditional Inspection held a dominant market position, capturing more than a 63.9% share in the Building Inspection Services market. The segment’s stronghold stemmed from its longstanding use, particularly in regions where manual assessments and on-site evaluations remain the norm. Many property owners and facility managers continued to rely on traditional inspection methods for their cost-effectiveness and established credibility. Additionally, the preference for physical, hands-on assessments for structural integrity and safety checks further reinforced the segment’s market share. Despite advancements in digital inspection tools, the trust and familiarity associated with traditional methods ensured its continued dominance in 2024.

By End Use

Residential Segment Commands 47.7% Share, Driving Inspection Services Market

In 2024, Residential held a dominant market position, capturing more than a 47.7% share in the Building Inspection Services market. The segment’s prominence was fueled by increasing housing projects and rising demand for property assessments, particularly in urban and suburban areas. Homebuyers and property investors prioritized residential inspections to identify potential structural issues and ensure compliance with safety standards. Additionally, the trend of purchasing second-hand homes and the emphasis on renovation projects further accelerated the demand for residential inspections. As property sales surged, the residential segment remained a key revenue driver for the overall inspection services market.

Key Market Segments

By Services

- Residential Inspection

- Pre-Listing Inspections

- Builder’s Warranty Inspections

- New Construction Inspections

- Pre-Closing Inspections

- Commercial Inspection

- Commercial Draw Inspections

- Retail or Office Space Inspections

- Special Purpose Facilities

- Others

- Specialty Inspection

- Sewer and Septic System Inspections

- Roof Inspections

- Lawn Irrigation Inspections

- Yearly Maintenance Inspection

- Others

By Sourcing Type

- In-House Services

- Outsourced Services

By Technology

- Traditional Inspection

- Drone Inspection

- Thermal Imaging Inspection

By End Use

- Residential

- Commercial

- Industrial

- Government

Drivers

Government-Mandated Safety Audits Propel Growth in Building Inspection Services

In 2024, the building inspection services market in India witnessed significant growth, largely driven by government initiatives aimed at enhancing structural safety. A pivotal development was the Lucknow Development Authority’s (LDA) decision to mandate safety and structural audits for aging high-rise buildings every ten years. This move came in response to the tragic collapse of Harmilap Tower in Transport Nagar, which resulted in eight fatalities. The audits, conducted by seven empanelled consultancy firms, focus on assessing risks, structural integrity, and fire safety protocols. Building owners are responsible for the audit costs and must address any identified safety concerns within a stipulated timeframe, failing which they face penalties.

These stringent regulations underscore a broader national emphasis on building safety and compliance. The Indian construction industry, contributing approximately 8% to the GDP and employing over 40 million people, is experiencing robust growth across residential and commercial sectors. Government initiatives like the National Infrastructure Pipeline and the Smart Cities Mission are further propelling this expansion.

As urbanization accelerates, with India’s urban population projected to reach 600 million by 2030, the demand for safe and compliant buildings becomes paramount. This demographic shift necessitates substantial investments in infrastructure, including residential, commercial, and industrial buildings. Consequently, building inspection services are becoming integral to ensuring the safety and integrity of these structures, aligning with the government’s vision for sustainable and secure urban development.

Restraints

Bureaucratic Delays and Regulatory Complexity Hamper Growth of Building Inspection Services

In 2024, the building inspection services sector in India faced significant challenges due to bureaucratic delays and complex regulatory frameworks. A notable example is the situation in Andhra Pradesh, where reforms intended to streamline building plan approvals by empowering Licensed Technical Personnel (LTPs) inadvertently led to a slowdown in the approval process. Under the new system, LTPs are solely responsible for designing, uploading, and monitoring construction projects, replacing the oversight role previously held by the town planning department.

However, the introduction of stringent accountability measures, including liability for legal actions in case of construction-related accidents, has caused hesitation among LTPs. Consequently, monthly building plan applications in the state’s 130 municipalities have drastically dropped from 300–400 to around 100 as of April 2025, reflecting a climate of uncertainty and reluctance among LTPs to operate under the new regulations .

This scenario underscores a broader issue within India’s construction industry: the complex and often contradictory regulatory environment. The industry is governed by a myriad of laws, regulations, and guidelines, including building codes, environmental regulations, land acquisition laws, and labor laws. These overlapping and sometimes conflicting regulations create a challenging landscape for developers and inspection service providers. The bureaucratic processes involved in obtaining necessary permits and approvals are notoriously slow and inefficient, leading to project delays and increased costs. Such an environment discourages innovation and the adoption of new technologies, as developers may be reluctant to navigate the additional regulatory hurdles associated with innovative construction methods .

Moreover, the lack of standardized regulations and quality control measures across different regions further complicates the situation. This inconsistency often results in construction projects being delayed, over budget, or of poor quality, thereby undermining the credibility of building inspection services. The absence of a unified regulatory framework hampers the ability of inspection service providers to operate effectively and deliver consistent quality across various projects .

Opportunity

Government-Led Infrastructure Initiatives Fuel Demand for Building Inspection Services

In 2024, India’s building inspection services market experienced significant growth, largely driven by government-led infrastructure initiatives. The construction industry in India is projected to grow by 11.2% to reach INR 25.31 trillion in 2024, indicating substantial growth potential. This surge in construction activities necessitates rigorous building inspections to ensure compliance with safety and quality standards.

Government programs such as the Smart Cities Mission and the Pradhan Mantri Awas Yojana (PMAY) have been instrumental in promoting infrastructure and affordable housing projects. These initiatives not only aim to enhance urban living but also mandate strict adherence to building codes and regulations, thereby increasing the demand for professional inspection services.

Furthermore, the Lucknow Development Authority (LDA) has initiated safety and structural audits for aging high-rise buildings in the city. Following the collapse of Harmilap Tower in Transport Nagar, which claimed eight lives, the LDA has made it mandatory for old buildings to undergo a safety audit every ten years. These audits, conducted by empanelled consultancy firms, assess risks, structural integrity, and fire safety protocols. Building owners are responsible for the audit costs and must address any identified safety concerns within a stipulated timeframe, failing which they face penalties.

These government-led initiatives underscore a broader national emphasis on building safety and compliance. As urbanization accelerates, with India’s urban population projected to reach 600 million by 2030, the demand for safe and compliant buildings becomes paramount. This demographic shift necessitates substantial investments in infrastructure, including residential, commercial, and industrial buildings. Consequently, building inspection services are becoming integral to ensuring the safety and integrity of these structures, aligning with the government’s vision for sustainable and secure urban development.

Trends

Embracing Smart Technologies: A New Era in Building Inspections

In 2024, the building inspection services market in India is witnessing a significant shift towards the adoption of smart technologies. This trend is driven by the need for more efficient, accurate, and comprehensive inspection processes in the face of rapid urbanization and infrastructure development.

One of the most notable advancements is the integration of drone technology and artificial intelligence (AI) into inspection services. Drones equipped with high-resolution cameras and sensors are now being utilized to conduct aerial surveys of buildings, allowing inspectors to access hard-to-reach areas and identify potential issues without the need for scaffolding or ladders. AI algorithms further enhance this process by analyzing the collected data to detect structural anomalies, material degradation, and other safety concerns with greater precision.

The Belagavi City Corporation (BCC) in Karnataka has recently demonstrated the use of a robotic inspection machine for underground drainage systems. This robot, costing approximately ₹27 lakh, employs cameras and sensors to detect blockages, leakages, and other pipeline issues, providing live internal visuals and preventing potential collapses. The implementation of such technology not only improves the efficiency of inspections but also enhances public health and sanitation by ensuring timely detection and management of drainage issues.

The Indian government’s emphasis on smart city initiatives and infrastructure modernization further supports this trend. By promoting the adoption of cutting-edge technologies in construction and inspection processes, these initiatives aim to enhance the quality and safety of buildings nationwide.

Regional Analysis

In 2024, the Asia-Pacific (APAC) region emerged as the dominant force in the global building inspection services market, commanding a substantial 38.6% share, equivalent to approximately USD 4.6 billion. This leadership is underpinned by rapid urbanization, significant infrastructure development, and stringent regulatory frameworks across key economies such as China, India, and Japan.

China’s aggressive urban expansion and infrastructure projects have necessitated rigorous building inspections to ensure compliance with safety standards. The country’s commitment to sustainable urban development has further amplified the demand for comprehensive inspection services.

In India, initiatives like the Smart Cities Mission and the Pradhan Mantri Awas Yojana (PMAY) have spurred construction activities, thereby increasing the need for building inspections to uphold quality and safety benchmarks. Japan’s focus on seismic resilience and aging infrastructure has also contributed to the heightened demand for inspection services.

Technological advancements are playing a pivotal role in transforming the building inspection landscape in APAC. The adoption of drones, artificial intelligence (AI), and Internet of Things (IoT) devices has enhanced the efficiency and accuracy of inspections, enabling real-time data collection and analysis. These innovations are particularly beneficial in densely populated urban areas, where traditional inspection methods may be challenging.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

SGS SA is a global leader in inspection, verification, testing, and certification services, playing a crucial role in the building inspection services market. The company leverages advanced technologies, including drones and AI, to conduct comprehensive building assessments. In 2024, SGS expanded its service portfolio, focusing on sustainable building inspections in key markets like APAC and Europe. The firm’s extensive network of offices and laboratories enhances its ability to provide consistent, reliable inspection services across diverse regions.

The Royal Institution of Chartered Surveyors (RICS) is a leading organization providing building inspection services with a strong emphasis on regulatory compliance and safety standards. In 2024, RICS continued to expand its digital inspection capabilities, integrating AI-driven software for precise structural assessments. The institution’s global reach and expertise in risk assessment make it a preferred partner for large-scale infrastructure projects, particularly in Europe and North America, where regulatory frameworks demand comprehensive building inspections.

Bureau Veritas is a prominent player in the building inspection services sector, specializing in quality, health, safety, and environmental assessments. In 2024, the firm introduced advanced digital inspection tools to streamline data collection and reporting processes. With a focus on regulatory compliance and risk management, Bureau Veritas operates extensively in Asia-Pacific and Europe, serving major infrastructure projects and high-rise developments, ensuring structural integrity and adherence to safety protocols.

Intertek provides comprehensive building inspection services, focusing on structural assessments, regulatory compliance, and quality assurance. In 2024, the company expanded its inspection services to include smart technologies like thermal imaging and drone surveillance for enhanced data accuracy. Intertek’s strategic partnerships with major construction firms and regulatory bodies in North America and Europe position it as a key player in the evolving building inspection landscape, addressing emerging safety concerns and regulatory mandates.

Top Key Players in the Market

- SGS SA

- RICS

- Bureau Veritas

- Intertek

- WSP Global

- AECOM

- Huxley Associates

- The Hartford

- AtkinsonNolandand Associates

- GHD Group

- TUV Rheinland

Recent Developments

In 2024, WSP Global Inc. solidified its position as a key player in the building inspection services market, reporting revenues of CAD 16.17 billion, up 11.98% from the previous year.

In 2024, Intertek Group plc reported a total revenue of £3,393.2 million, marking a 6.6% increase at constant currency compared to the previous year.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 12.5 Bn |

| Forecast Revenue (2034) | USD 22.6 Bn |

| CAGR (2025-2034) | 6.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Services (Residential Inspection, Commercial Inspection, Specialty Inspection), By Sourcing Type (In-House Services, Outsourced Services), By Technology (Traditional Inspection, Drone Inspection, Thermal Imaging Inspection), By End Use ( Residential, Commercial, Industrial, Government) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | SGS SA, RICS, Bureau Veritas, Intertek, WSP Global, AECOM, Huxley Associates, The Hartford, AtkinsonNolandand Associates, GHD Group, TUV Rheinland |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |