Global Blood Product Market By Product Type (Red Blood Cells, Platelets, and Others), By Application (Blood Station, Hospital, and Others), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2034

- Published date: July 2025

- Report ID: 152965

- Number of Pages: 290

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

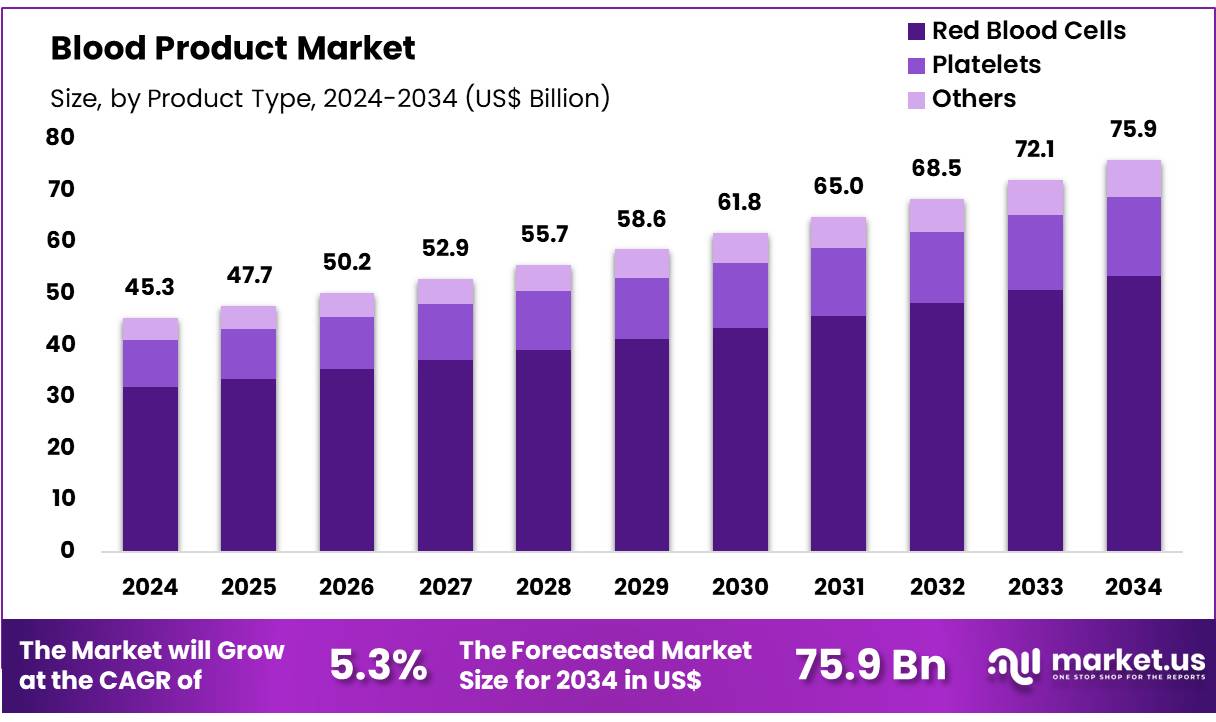

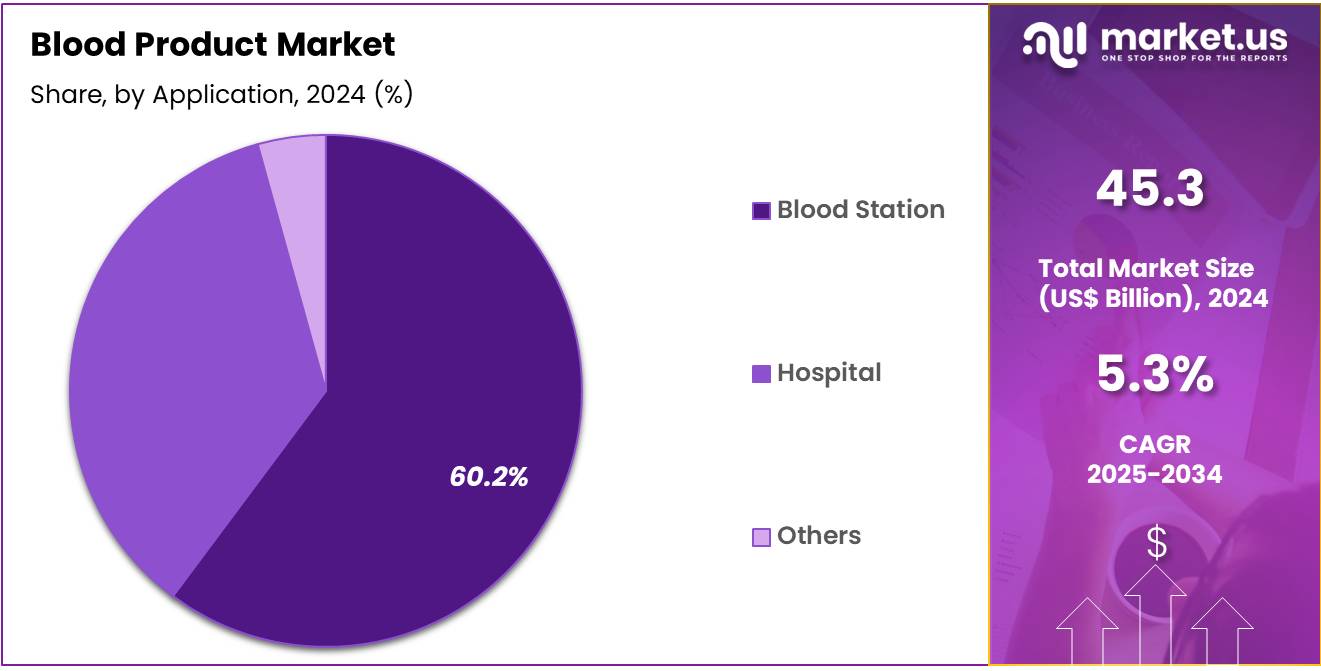

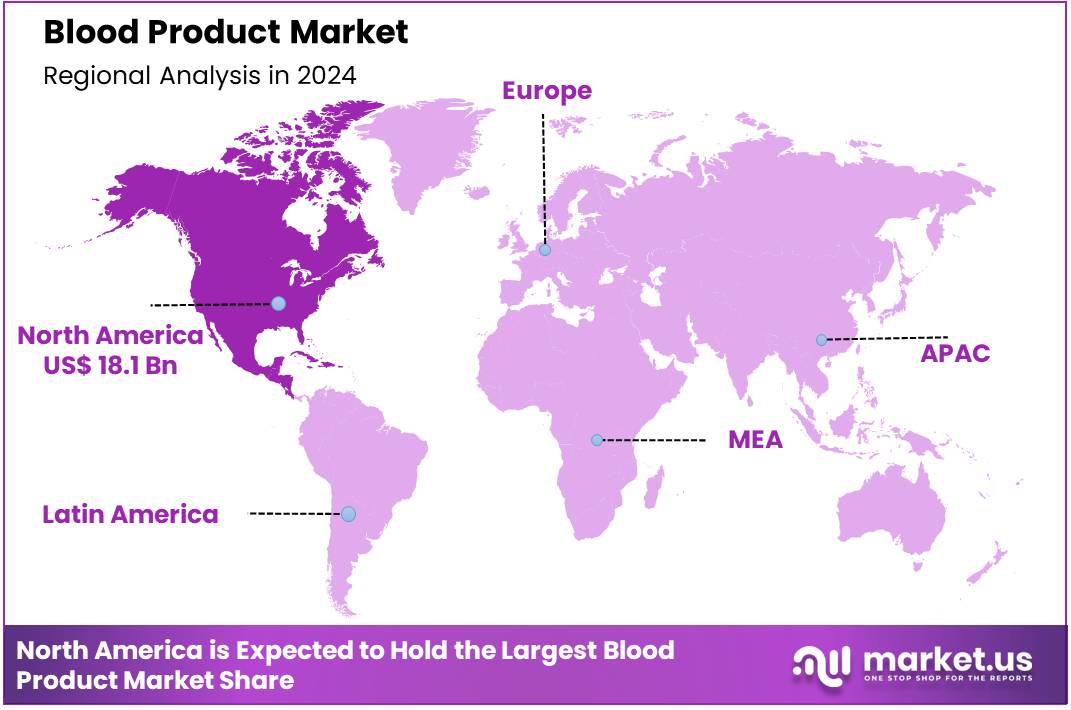

Global Blood Product Market size is expected to be worth around US$ 75.9 Billion by 2034 from US$ 45.3 Billion in 2024, growing at a CAGR of 5.3% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 39.9% share with a revenue of US$ 18.1 Billion.

Increasing demand for blood products due to the rising prevalence of chronic diseases, surgical procedures, and trauma is driving the growth of the blood product market. Blood products, including red blood cells, plasma, platelets, and clotting factors, are essential for treating conditions such as anemia, hemophilia, cancer, and bleeding disorders. The growing number of surgeries, trauma cases, and medical conditions requiring regular blood transfusions has significantly expanded the market’s reach.

Additionally, advances in blood storage and transfusion technology have improved the efficiency and safety of blood product usage, enhancing patient outcomes. The market benefits from the increasing focus on improving blood donation and collection systems to meet global healthcare needs. The Héma-Québec 2023–2024 annual report highlights the distribution of 453,376 stable products, 26,963 plasma donations, 300,478 blood products, and 48,376 blood donations, reflecting the ongoing demand for blood products to support patient care.

As the number of blood donations continues to rise, healthcare systems are able to enhance their supply of blood products, ensuring better management of critical patients. Recent trends also include innovations in plasma-derived therapies, such as immunoglobulins and clotting factors, which provide targeted treatments for rare and chronic diseases.

The development of artificial blood substitutes and more efficient plasma collection methods offers significant opportunities for growth, creating a more sustainable supply chain for blood products. With increasing demand and continuous innovation, the blood product market is poised for further advancements in both treatment options and donation management systems.

Key Takeaways

- In 2024, the market for blood product generated a revenue of US$ 45.3 billion, with a CAGR of 5.3%, and is expected to reach US$ 75.9 billion by the year 2034.

- The product type segment is divided into red blood cells, platelets, and others, with red blood cells taking the lead in 2023 with a market share of 70.4%.

- Considering application, the market is divided into blood station, hospital, and others. Among these, blood station held a significant share of 60.2%.

- North America led the market by securing a market share of 39.9% in 2023.

Product Type Analysis

Red blood cells (RBCs) dominate the blood product market, holding a significant share of 70.4%. This segment’s growth is expected to continue due to the high demand for RBC transfusions, particularly in patients undergoing surgeries, trauma victims, and individuals with anemia or other blood disorders. The increasing prevalence of chronic diseases, including cancer, cardiovascular diseases, and chronic kidney diseases, is anticipated to drive RBC demand as these conditions often result in anemia and require regular blood transfusions.

Furthermore, the growing global awareness of the importance of blood donations is projected to increase the supply of RBCs, supporting the segment’s growth. The advances in blood collection techniques and improved blood storage methods are expected to enhance RBC availability and help manage supply shortages more effectively.

Additionally, the rising number of aging populations, particularly in developed countries, is likely to increase the need for RBC transfusions, further fueling the segment’s expansion. As healthcare systems globally focus more on improving patient care and safety during surgeries and treatments, the demand for red blood cells is expected to remain strong in the foreseeable future.

Application Analysis

Blood stations hold a dominant share of 60.2% in the blood product market. This segment’s growth is expected to be driven by the critical role that blood stations play in the collection, processing, and distribution of blood products. Blood stations are likely to continue expanding as they remain the primary source for blood collection, ensuring a steady supply for hospitals and healthcare facilities.

The increasing number of road accidents, surgeries, and emergency medical treatments requiring blood transfusions is projected to increase the reliance on blood stations for meeting demand. Additionally, the rising focus on voluntary blood donations, especially in developing regions, is anticipated to support the growth of blood stations. The advancement of blood donation programs and the increasing integration of blood stations with healthcare networks is expected to facilitate the effective distribution of blood products.

As governments and non-governmental organizations continue to promote blood donation awareness campaigns, blood stations are expected to play an even larger role in ensuring a consistent and safe blood supply. The segment is projected to see continued growth as healthcare systems enhance their infrastructure to manage blood collection and distribution more effectively.

Key Market Segments

By Product Type

- Red Blood Cells

- Platelets

- Others

By Application

- Blood Station

- Hospital

- Others

Drivers

Increasing Demand from Surgical Procedures and Trauma Cases is Driving the Market

The increasing global incidence of complex surgical procedures and a rise in trauma cases are a primary driver propelling the demand for blood products. Major surgeries, including organ transplants, cardiac operations, and extensive orthopedic procedures, frequently necessitate blood transfusions to compensate for blood loss and maintain patient stability.

Similarly, severe trauma resulting from accidents, natural disasters, or conflict demands immediate and often substantial quantities of blood products including whole blood, red blood cells, platelets, and plasma to manage hemorrhage and stabilize patients. The expanding elderly population, which often requires more complex medical interventions, further contributes to this escalating demand.

For instance, the US National Center for Biotechnology Information (NCBI) StatPearls, in a June 2023 update, highlighted that approximately 15 million units of blood are transfused annually in the United States, supporting various medical needs, including surgery and trauma. This consistent and critical need for blood products across a wide spectrum of medical emergencies and planned procedures ensures a steady and growing demand for these life-saving components, driving the market forward.

Restraints

Challenges in Blood Donor Recruitment and Retention are Restraining the Market

Significant challenges in effectively recruiting and retaining blood donors, particularly volunteer non-remunerated donors, pose a considerable restraint on the blood product market. The supply of blood products is entirely dependent on human donations, making the market highly sensitive to donor turnout and the demographic shifts within donor populations.

Factors such as donor fatigue, lack of awareness about the constant need for blood, fear of needles, and busy lifestyles contribute to declining donor rates in many regions. Public health crises can also significantly disrupt collection efforts, as seen during recent global events. For example, a March 2025 article in the International Journal of Research in Industrial Engineering, analyzing the US blood donation problem, stated that while 62% of the US population is eligible to donate blood, only 3% actually do so each year.

The article also noted a 10-year trend of declining blood donations in the US, with a significant 62.5% decline in donations from individuals in the 16-18 age group from 2019 to 2021. This persistent struggle to maintain a sufficient and stable donor base directly impacts the availability of blood for transfusion, creating shortages that can affect patient care and limit the overall capacity of the blood product market.

Opportunities

Advancements in Blood Processing and Pathogen Reduction Technologies are Creating Growth Opportunities

Ongoing advancements in blood processing techniques and the development of sophisticated pathogen reduction technologies (PRTs) are creating significant growth opportunities within the blood product market. These innovations enhance the safety, quality, and efficacy of blood components, making transfusions safer and more reliable. Modern processing methods allow for more efficient separation and storage of individual blood components (red blood cells, platelets, plasma), optimizing their therapeutic use and extending their shelf life.

Pathogen reduction technologies are designed to inactivate a broad spectrum of viruses, bacteria, and parasites that might be present in donated blood, thereby significantly reducing the risk of transfusion-transmitted infections. For example, the US Food and Drug Administration (FDA) regularly updates its guidance on blood product safety and approves new technologies.

In January 2023, the FDA approved the first-ever blood screening test for Babesia parasites, highlighting continuous efforts to enhance donor screening and improve blood safety. These advancements foster greater confidence in the safety of transfused blood products among healthcare providers and patients, encourage broader clinical application, and enable more efficient utilization of donated blood units, ultimately driving innovation and growth within the market.

Impact of Macroeconomic / Geopolitical Factors

Global economic volatility, including inflationary pressures and shifts in national healthcare funding priorities, significantly influences the blood product market. The complex infrastructure required for blood collection, processing, testing, and storage, including specialized equipment, trained personnel, and stringent quality control is sensitive to rising operational costs. Sustained inflation can increase expenses for utilities, labor, and medical supplies, directly impacting the budgets of blood banks and transfusion services worldwide.

For example, the World Health Organization (WHO) “Global Health Expenditure Database” continually tracks national health spending, revealing that economic downturns often lead to fiscal tightening, potentially impacting public funding allocated to blood services. Furthermore, geopolitical events, such as widespread conflicts or humanitarian crises, can divert significant financial resources towards emergency response efforts, sometimes at the expense of routine healthcare services.

This shift in funding can strain blood product supply in affected regions and contribute to global imbalances. However, these challenges also compel governments and international organizations to prioritize the resilience and self-sufficiency of national blood supply systems, leading to strategic investments in local collection and processing capabilities. This fosters greater stability and ensures continued access to essential blood products even amidst global uncertainties.

Evolving US trade policies, including the strategic application of tariffs, are actively shaping the blood product market by influencing the cost of critical supplies and incentivizing domestic infrastructure investment. While finished blood products themselves are typically not subjected to high tariffs due to their life-saving nature, duties on imported components, specialized laboratory equipment, or certain medical consumables used in blood collection, processing, and testing can increase operational costs for US blood banks and transfusion centers.

Data from the US Census Bureau for 2023 shows that imports of medical instruments and supplies, categories that can include equipment for blood product handling, amounted to over US$100 billion, indicating the scale of cross-border trade where tariffs could impact various inputs. This rise in input costs can compel blood service organizations to manage increased expenses, potentially straining their budgets or leading to higher service fees for hospitals.

Conversely, the focus of US trade policy and other government initiatives on strengthening domestic supply chains for essential medical resources encourages investment in US-based blood collection and processing infrastructure. This strategic push promotes self-sufficiency, reduces reliance on potentially volatile international supply chains for critical components, and enhances the overall resilience and security of the US blood product supply, ensuring continued availability for patients.

Latest Trends

Increased Focus on Point-of-Care Blood Typing and Cross-Matching is a Recent Trend

A prominent recent trend significantly impacting the blood product market in 2024 and continuing into 2025 is the increased focus on developing and implementing point-of-care (POC) blood typing and cross-matching solutions. This trend aims to rapidly determine blood compatibility at or near the patient’s bedside, especially in emergency and critical care settings where immediate transfusions are vital and traditional laboratory-based testing can cause delays.

POC devices utilize advanced microfluidic technologies and highly specific reagents to provide quick and accurate blood group identification and compatibility testing, streamlining the transfusion process and potentially improving patient outcomes by reducing time to transfusion. While full regulatory approvals for widespread POC cross-matching are still evolving, significant advancements in rapid blood typing are already in use.

For instance, a 2024 publication in the journal Transfusion discussed ongoing research and validation of novel rapid blood typing technologies, indicating a strong push towards immediate results. This shift towards decentralized and rapid testing capabilities represents a crucial evolution in transfusion medicine, enhancing efficiency and responsiveness in acute care situations, thereby driving innovation in the delivery and utilization of blood products.

Regional Analysis

North America is leading the Blood Product Market

North America dominated the market with the highest revenue share of 39.9% owing to increasing demand for transfusions in complex surgical procedures, managing chronic diseases, and treating trauma cases, alongside a significant recovery in plasma collection volumes. The American Red Cross, a major supplier in the US, annually supplies 6.5 million blood products to hospitals, indicating a consistent and high volume of need.

In Canada, Canadian Blood Services reported that in 2023–2024, it met or exceeded targets for prompt delivery of blood components, filling over 98% of hospital orders for red blood cells within 24 hours. This sustained demand is further supported by an aging population and increasing prevalence of conditions requiring blood product support. Plasma collection, crucial for manufacturing various therapeutic products, saw significant recovery.

CSL Behring, a prominent global manufacturer, reported that its CSL Behring segment’s total revenue increased by 10% for the half-year ended December 31, 2024, with strong growth across all geographies, particularly for immunoglobulin products, which saw a 15% increase.

Similarly, Grifols, another key player, reported that its Biopharma revenue in the first quarter of 2025 reached EUR 1,521 million (approximately US$1,784.69 million), reflecting a 9.6% year-over-year growth at constant currency, largely driven by increased immunoglobulin sales in its core markets, including North America. These figures underscore the market’s expansion, fueled by both consistent clinical need and successful efforts to enhance supply.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to improving healthcare infrastructure, increasing awareness of various medical conditions requiring blood components, and rising patient populations, coupled with active government initiatives to enhance blood collection and processing capabilities. Countries across the region are investing in modernizing their healthcare systems, which directly supports the increased utilization of blood components and derivatives.

For instance, China witnessed a record high in voluntary blood donations in 2023, with a total of 16.99 million donations, marking a 5.9% increase from 2022, as reported by China’s National Health Commission. This growing donor base directly contributes to a more stable and accessible supply of blood components. In India, while detailed national statistics for 2023-2024 are still emerging, the Indian Council of Medical Research (ICMR) continues to drive advancements in public health and clinical care, which includes supporting blood transfusion services.

Major global manufacturers are actively expanding their presence and offerings in Asia Pacific. Takeda, for example, reported that its Plasma-Derived Therapies (PDT) segment posted JPY 784.2 billion in revenue globally, reflecting a 16.3% increase in its fiscal year 2024 (ended March 31, 2025), driven by rising global demand for immunoglobulin products, with Asia (excluding Japan) seeing an increase of 10.8% in overall revenue. This strategic focus by pharmaceutical companies, combined with governmental efforts to improve blood safety and availability, is projected to significantly accelerate the growth of the market across Asia Pacific.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the blood product market implement several strategies to fuel growth and strengthen their market presence. They focus on expanding product offerings by developing new treatments and improving existing blood-based therapies for conditions such as anemia, hemophilia, and blood clotting disorders. Companies invest in state-of-the-art manufacturing technologies and expand production capabilities to meet rising global demand.

Strategic acquisitions and partnerships with healthcare providers enable them to increase market access and enhance research capabilities. Additionally, they prioritize geographical expansion, particularly targeting emerging markets where healthcare infrastructure is improving. Increased awareness campaigns and collaborations with government health organizations play a crucial role in ensuring higher blood product usage.

One key player, Grifols, is a global leader in the development and production of blood-based therapies. Specializing in immunoglobulins, clotting factors, and albumin, Grifols is at the forefront of providing life-saving treatments for rare and chronic conditions.

The company continually invests in research and development to innovate and enhance its product offerings, maintaining a strong global presence with a network of manufacturing facilities. Grifols’ commitment to improving patient outcomes and expanding access to its therapies ensures its continued leadership in the market.

Recent Developments

- In October 2024, Terumo Blood and Cell Technologies (Terumo BCT), a global leader in blood management solutions, launched the Reveos Automated Blood Processing System in the United States. This system is designed to support blood centers in managing platelet and blood supplies more efficiently while improving workforce productivity.

- In February 2023, the US Department of Defense’s Defense Advanced Research Projects Agency (DARPA) allocated $46 million to support the development of a shelf-stable, field-deployable whole blood substitute. This technology is intended to aid trauma victims when donated blood is unavailable.

Top Key Players

- Terumo Blood and Cell Technologies

- Takeda

- Octapharma AG

- Kedrion SpA

- Grifols

- CSL

- BPL

- Baxter

Report Scope

Report Features Description Market Value (2024) US$ 45.3 Billion Forecast Revenue (2034) US$ 75.9 Billion CAGR (2025-2034) 5.3% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product Type (Red Blood Cells, Platelets, and Others), By Application (Blood Station, Hospital, and Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Terumo Blood and Cell Technologies, Takeda, Octapharma AG, Kedrion SpA, Grifols, CSL, BPL, and Baxter. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Terumo Blood and Cell Technologies

- Takeda

- Octapharma AG

- Kedrion SpA

- Grifols

- CSL

- BPL

- Baxter

Our Clients

- 152965

- July 2025