Quick Navigation

Report Overview

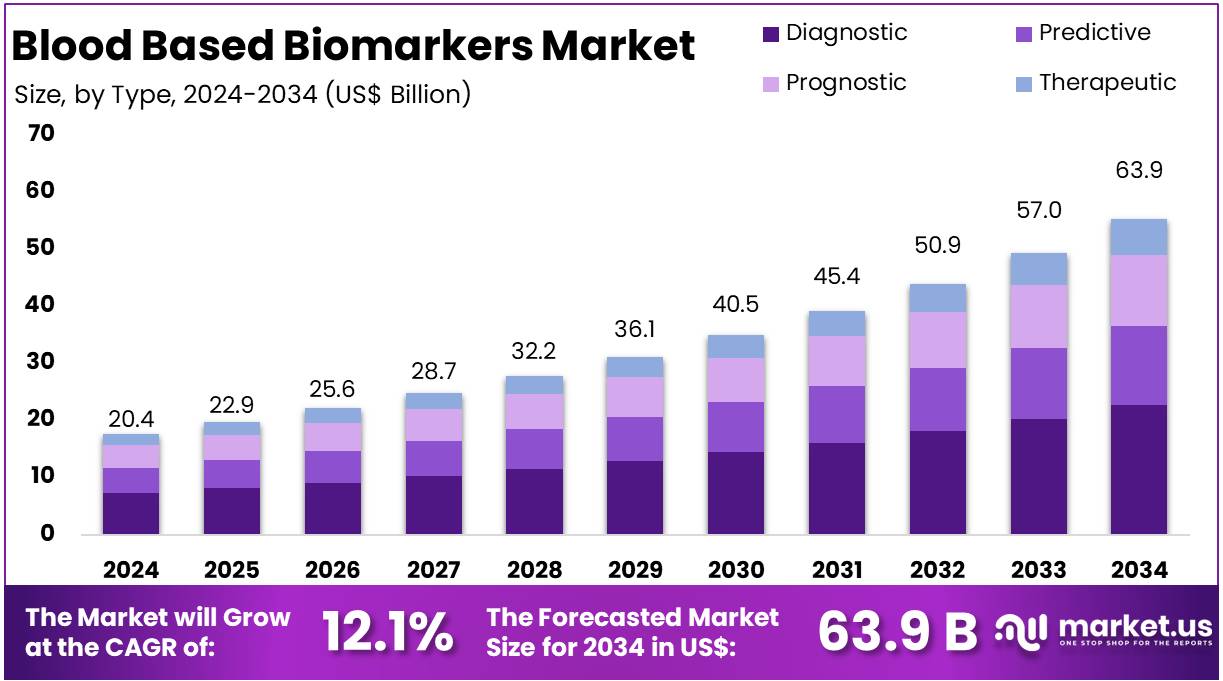

The Global Blood Based Biomarkers Market size is expected to be worth around US$ 63.9 Billion by 2034, from US$ 20.4 Billion in 2024, growing at a CAGR of 12.1% during the forecast period from 2025 to 2034. North America held a dominant market position, capturing more than a 43.6% share and holds US$ 8.8 Billion market value for the year.

Blood-based biomarkers are measurable biological substances in the blood that reflect normal or abnormal physiological conditions. These include proteins, nucleic acids, and metabolites. They are increasingly used for disease detection, monitoring, and treatment response assessment. One of the main advantages is their non-invasive nature. Unlike tissue biopsies, blood samples are easier and safer to collect. This allows for more frequent testing and broader adoption in clinical settings.

According to projections for 2024, the United States is expected to witness around 2,001,140 new cancer cases and 611,720 cancer-related deaths. This underscores the urgent need for early detection tools. Blood-based biomarkers play a vital role here. For example, Prostate-Specific Antigen (PSA) is widely used in prostate cancer screening, while CA-125 is commonly associated with ovarian cancer. Despite this, adherence to PSA testing remains low at 37.2%, compared to 66.3% for diabetes and 67.8% for dyslipidemia.

The growing popularity of liquid biopsy technologies has further boosted the demand for blood-based biomarkers. These techniques detect circulating tumor DNA (ctDNA) with high sensitivity, often between 0.1% and 1% mutant allele frequency. A clinical trial, STING protocol (NCT04932525), revealed that 51.8% of 542 advanced cancer patients showed ctDNA mutations only detectable via liquid biopsy, with a median variant allele frequency of 0.37. These tools are proving especially useful in identifying resistance mutations such as EGFR T790M.

Blood-based biomarkers also help monitor chronic and age-related conditions. With the global population aging, diseases like Alzheimer’s are on the rise. Biomarkers such as amyloid-beta and tau proteins are showing promise for early diagnosis. In cardiovascular care, troponin levels help detect heart attacks. In metabolic disorders, glucose and HbA1c are key indicators for diabetes. A 2024 study using 150 protein biomarkers achieved 93% accuracy in detecting stage 1 cancer in men and 84% in women, with 80% organ-specific localization.

Environmental health monitoring has also adopted blood-based biomarkers. For example, OSHA guidelines mandate blood lead level testing every six months for workers exposed to lead at or above 50 µg/m³. If levels exceed 40 µg/100 g of blood, monthly testing is required. In children, pyrethroid pesticide exposure was linked to oxidative stress markers like 8-OHdG and DNA methylation changes. A study of 440 urine samples highlighted the impact of azole pesticides like tebuconazole, which showed a 15.1% reduction in 3-mA per interquartile range increase.

The blood-based biomarker market is expanding due to rising disease burdens, aging populations, and technological advancements. Tools like MedGenome’s NGS assays, which profile multiple genes from just 10–20 ng of DNA, are helping personalize treatment. According to recent trends, early detection and cost-efficiency are driving wider adoption. As research continues, these biomarkers are set to play a central role in precision medicine and public health strategies.

Key Takeaways

- The global blood-based biomarkers market is projected to reach approximately US$ 63.9 billion by 2034, growing at a CAGR of 12.1% from 2025.

- In 2024, the market was valued at around US$ 20.4 billion, highlighting substantial growth potential over the forecast period.

- Diagnostic applications accounted for the largest share in 2024, representing over 35.5% of the total type segment in the blood-based biomarkers market.

- Hospitals and clinics dominated the end-use segment in 2024, holding a market share exceeding 46.3%, driven by high testing demand in clinical settings.

- North America emerged as the leading regional market in 2024, contributing more than 43.6% and generating US$ 8.8 billion in market value.

Type Analysis

In 2024, Diagnostic held a dominant market position in the Type Segment of Blood-Based Biomarkers, capturing more than a 35.5% share. This strong position is driven by the rising demand for early disease detection. Diagnostic biomarkers are widely used in identifying cancers, infections, and cardiovascular conditions. Their non-invasive nature supports patient acceptance. Advancements in molecular diagnostics have enhanced test accuracy. This has further boosted clinical adoption. Increased screening programs across regions are also supporting segment growth.

Predictive biomarkers emerged as the second leading segment. These biomarkers help evaluate the likelihood of disease occurrence. Their use is increasing in cancer risk assessment and personalized therapies. Predictive tools enable physicians to select the most effective treatment plans. Their growing role in clinical trials is enhancing their visibility. Demand is supported by advancements in genetic testing. Increasing focus on individualized care is contributing to segment growth. Pharmaceutical investments are also accelerating innovation in predictive testing.

Prognostic and therapeutic biomarkers also play key roles. Prognostic biomarkers estimate disease outcomes and progression. They are valuable in long-term disease monitoring. Their use is expanding in chronic and neurodegenerative conditions. Therapeutic biomarkers, though smaller in share, show promising growth. Their role in drug targeting and treatment optimization is gaining attention. Growth is supported by rising clinical trials and drug development programs. These segments benefit from ongoing research. Interest in precision medicine continues to drive future demand.

End Use Analysis

In 2024, Hospitals & Clinics held a dominant market position in the end use segment of blood-based biomarkers, capturing more than a 46.3% share. This segment benefited from the growing number of patients seeking diagnosis and treatment in clinical settings. The increasing need for early disease detection has led to a rise in biomarker usage. Hospitals are also adopting advanced diagnostic tools. This combination of factors has positioned hospitals and clinics as primary users of blood-based biomarkers.

Diagnostic Laboratories also held a significant portion of the market. Their growth has been supported by the rising demand for outsourced testing services. Many healthcare providers rely on these labs for faster and more cost-effective results. Advanced laboratory systems and high-throughput technologies further drive their adoption. As a result, diagnostic laboratories are becoming essential partners in disease diagnosis and monitoring through blood-based biomarkers.

Research & Academic Institutes contributed a smaller yet important share. Their focus lies in biomarker discovery and validation. These institutions benefit from growing research funding and collaboration with clinical centers. They play a critical role in translating lab findings into clinical applications. The Others segment, which includes home care settings and specialized clinics, is also emerging. Rising awareness of personalized medicine and portable diagnostics is expected to support growth across these alternative end-use settings.

Key Market Segments

By Type

- Diagnostic

- Predictive

- Prognostic

- Therapeutic

By End Use

- Hospitals & Clinics

- Diagnostic Laboratories

- Research & Academic Institutes

- Others

Drivers

Rising prevalence of chronic diseases and cancer

The growing number of chronic diseases has become a major concern worldwide. Conditions such as heart disease and neurodegenerative disorders are being reported more frequently. This rising prevalence has led to a greater focus on early detection and better disease management. As a result, blood-based biomarkers are being used more widely. These biomarkers help in identifying diseases at early stages. Early detection often leads to more effective treatment. It also helps in lowering long-term healthcare costs by reducing complications.

Cancer is another major factor driving the use of blood-based biomarkers. Different types of cancer are being diagnosed at alarming rates. These include breast cancer, lung cancer, and colorectal cancer, among others. Blood-based biomarkers play a key role in diagnosing these conditions early. They help in assessing the stage of cancer and predicting how it may progress. By doing so, they improve the chances of survival. Moreover, such biomarkers help doctors monitor the effectiveness of ongoing treatments.

The clinical benefits of blood-based biomarkers are significant. They assist in tailoring treatment plans based on a patient’s condition. This personalized approach leads to better health outcomes. In addition, it supports the efficient use of medical resources. Biomarkers also help in reducing the trial-and-error method of prescribing drugs. As a result, patients receive quicker relief and fewer side effects. The healthcare system benefits through cost savings and improved care delivery. Therefore, the demand for blood-based biomarkers continues to rise steadily.

Restraints

Lack Of Standardization And Regulatory Challenges

The lack of standardization in biomarker validation remains a major restraint in the market. Currently, no uniform protocols exist to ensure consistency across studies and laboratories. This leads to varying results, making it difficult to compare findings or establish reliability. Such inconsistencies hinder the clinical confidence needed for broad adoption. Without common testing guidelines, healthcare providers may hesitate to rely on these biomarkers. As a result, the potential for blood-based biomarkers in routine diagnostics remains largely untapped and underutilized in clinical practice.

Regulatory challenges further limit the commercial progress of blood-based biomarkers. The approval process for diagnostic tests is often lengthy and complex. Multiple regulatory bodies must review the clinical utility, safety, and accuracy of these tests. This leads to delays in bringing products to market. Startups and research organizations may face financial and operational burdens during this time. The lack of clear, streamlined pathways for approval discourages innovation and delays the entry of potentially life-saving diagnostic tools into healthcare systems.

Together, these issues restrict the commercialization and widespread use of blood-based biomarkers. The combined effect of inconsistent test results and regulatory delays weakens stakeholder confidence. Healthcare providers, investors, and developers are often cautious due to the uncertain outcomes and slow approval rates. This limited adoption not only affects market growth but also prevents patients from accessing advanced diagnostic options. To overcome these barriers, the industry must work toward harmonized validation standards and more transparent regulatory frameworks that support innovation and patient care.

Opportunities

Advancements In Liquid Biopsy Technologies

The market is experiencing strong growth due to advancements in liquid biopsy technologies. These platforms allow non-invasive testing using blood samples. This method reduces the need for traditional tissue biopsies. It also offers a safer and quicker alternative for patients. Through liquid biopsies, circulating tumor DNA (ctDNA) can be detected with precision. This capability is vital for early cancer diagnosis. It also plays a key role in monitoring disease progression. The rising demand for accurate and rapid diagnostic tools is fueling market expansion.

Liquid biopsy platforms support the detection of several biomarkers. These include ctDNA, exosomes, and other molecular indicators. Such technologies enable personalized treatment plans based on individual biomarker profiles. This has transformed clinical decision-making in oncology. Doctors can now adjust therapies in real time. This improves patient outcomes and minimizes side effects. Additionally, liquid biopsies are easier to repeat. This makes them useful for ongoing disease monitoring. As a result, their adoption is increasing across both research and clinical settings.

Beyond oncology, liquid biopsy technologies show potential in other fields. These include neurology, prenatal testing, and transplant medicine. Their broad applications create new market opportunities. Furthermore, ongoing innovation in sequencing and molecular diagnostics is enhancing their effectiveness. Startups and key players are investing heavily in R&D. This is driving the development of more sensitive and specific platforms. With continued technological progress, liquid biopsies are expected to play a larger role in precision medicine. The trend indicates steady market growth in the coming years.

Trends

Integration of artificial intelligence (AI) in biomarker discovery

The integration of artificial intelligence (AI) in biomarker discovery is emerging as a key trend in biomedical research. AI technologies, especially machine learning algorithms, are being widely adopted to identify novel biomarkers. These tools help analyze large and complex biological datasets with speed and precision. The automation of data processing reduces human error and saves time. As a result, researchers can uncover hidden patterns and associations that were previously difficult to detect. This shift is transforming traditional biomarker discovery methods.

AI-driven platforms are enhancing the accuracy of biomarker identification. These platforms use advanced algorithms to process genomic, proteomic, and clinical data. They help in identifying potential biomarkers that are specific to disease subtypes. This level of detail improves the understanding of disease mechanisms. Moreover, AI supports the early detection of diseases through predictive models. The use of AI ensures higher validation rates for biomarkers. This contributes to faster development of diagnostic and therapeutic tools.

The adoption of AI in biomarker research also boosts diagnostic precision. It enables researchers to develop more targeted and personalized approaches. This improves patient outcomes and reduces healthcare costs. In addition, AI streamlines clinical trials by identifying the right biomarkers for patient stratification. This helps in selecting suitable candidates for targeted therapies. As AI tools evolve, they are expected to play a larger role in drug discovery. Their continued use will drive innovation in precision medicine and improve the efficiency of clinical research.

Regional Analysis

In 2024, North America held a dominant market position, capturing more than a 43.6% share and held a market value of US$ 8.8 billion for the year. This growth is driven by the high adoption of advanced diagnostic tools. The region continues to lead in precision medicine and molecular diagnostics. Increased focus on early disease detection, especially in cancer, supports this trend. Non-invasive blood tests are widely preferred. Their ease of use and reliability boost demand across clinical settings.

Strong healthcare infrastructure in the U.S. and Canada supports market expansion. Hospitals and labs are well-equipped to perform biomarker-based diagnostics. These facilities are integrated with automated systems, enabling faster and more accurate testing. There is a steady increase in routine screening for chronic diseases. This trend favors the use of blood-based biomarkers. Patient awareness about preventive healthcare is also rising. This encourages regular testing and enhances market growth across key states.

Favorable reimbursement policies further enhance test accessibility. In both public and private health plans, many biomarker tests are covered. This reduces out-of-pocket costs and increases test uptake. Government initiatives support research in blood-based diagnostics. Investments are directed toward cancer detection and neurological disorder monitoring. These programs aim to reduce the overall healthcare burden. Insurance-driven preventive care models also promote early-stage diagnostics. Together, these factors create a strong demand for biomarker solutions.

Research institutions and clinical trial centers are heavily concentrated in North America. Their collaborations with biotechnology firms drive innovation. The FDA has shown faster approval processes for critical biomarker tests. This regulatory flexibility benefits market entry for new products. The region’s aging population is another key driver. Older adults are more likely to undergo routine screenings. This further increases demand for blood-based biomarkers. These factors are expected to sustain North America’s market dominance in the coming years.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The blood-based biomarkers market is characterized by the presence of several well-established global players, each contributing to market development through continuous innovation, strategic partnerships, and expansion of diagnostic capabilities. The competitive landscape is moderately fragmented, with companies emphasizing research and development, regulatory approvals, and commercialization strategies to strengthen their market positioning.

Abbott is a key player in the blood-based biomarkers market. Its broad diagnostics portfolio and strong global footprint support its leadership. Proprietary platforms such as ARCHITECT and Alinity have improved biomarker detection. These technologies are used in oncology, cardiology, and infectious disease diagnostics. Abbott’s focus on high-sensitivity assays has advanced its position, especially in cardiac biomarkers. The company’s continued investment in R&D reinforces its competitive edge. Its strategic direction aligns with the growing demand for accurate and rapid diagnostic solutions across major healthcare markets.

BIOMÉRIEUX maintains a strong position through its in-vitro diagnostics expertise. Its VIDAS and BIOFIRE platforms enable early detection, particularly in sepsis and infectious diseases. The company’s pipeline reflects a commitment to innovation in biomarker-based testing. Strategic collaborations with research institutes and healthcare providers have driven its growth. These partnerships help expand its presence in emerging markets. BIOMÉRIEUX also focuses on improving diagnostic accuracy. This has strengthened its reputation in both clinical and laboratory environments.

F. Hoffmann-La Roche Ltd., Siemens Healthineers, and Thermo Fisher Scientific are major contributors to market development. Roche focuses on personalized medicine with its Elecsys® product line. It integrates biomarker assays with companion diagnostics, especially in oncology. Siemens Healthineers emphasizes automation with platforms like Atellica Solution. These support high-throughput and scalable testing. Thermo Fisher advances biomarker discovery through immunoassays and proteomics. Its portfolio includes reagents, analyzers, and data tools. Acquisitions and research partnerships support its innovation in translational medicine. Together, these companies shape the future of blood-based diagnostics.

In addition to the aforementioned market leaders, several emerging and regional companies contribute to the competitive dynamics. These include bioMérieux SA, Quanterix Corporation, Bio-Rad Laboratories, Inc., Becton, Dickinson and Company, and Myriad Genetics, Inc. These players focus on niche applications, such as neurodegenerative disease biomarkers, liquid biopsies, and point-of-care diagnostics. Their involvement enhances innovation diversity and promotes technological differentiation in the market.

Market Key Players

- Abbott

- BIOMÉRIEUX

- F. Hoffmann-La Roche Ltd.

- Siemens Healthineers AG

- Thermo Fisher Scientific, Inc.

- Bio-Rad Laboratories Inc.

- Sysmex Corporation

- Nutech Cancer Biomarkers India Pvt Ltd

- Minomic

- Diadem srl

- Proteomedix

Recent Developments

- In April 2024: Abbott received FDA clearance for its i-STAT TBI cartridge, a handheld device designed to detect traumatic brain injury (TBI) biomarkers in blood samples within 15 minutes. This test simplifies the workflow by eliminating the need for centrifugation, making it suitable for point-of-care use in non-clinical settings, such as military operations. The device uses biomarkers glial fibrillary acidic protein (GFAP) and ubiquitin C-terminal hydrolase L1 (UCH-L1) to assess suspected TBIs, providing lab-quality results quickly and aiding in triage decisions.

- In August 2022: Thermo Fisher Scientific introduced the Ion Torrent Oncomine Myeloid MRD Assays (RUO), a next-generation sequencing (NGS)-based assay designed for research on measurable residual disease (MRD) in myeloid malignancies. This innovative platform is the first NGS-based test to simultaneously analyze DNA and RNA, offering highly sensitive MRD assessments using blood and bone marrow samples. The assay aims to enhance research capabilities in hematologic cancers.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 20.4 Billion |

| Forecast Revenue (2034) | US$ 63.9 Billion |

| CAGR (2025-2034) | 12.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Diagnostic, Predictive, Prognostic, Therapeutic), By End Use (Hospitals & Clinics, Diagnostic Laboratories, Research & Academic Institutes, Others) |

| Regional Analysis | North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA |

| Competitive Landscape | Abbott, BIOMÉRIEUX, F. Hoffmann-La Roche Ltd., Siemens Healthineers AG, Thermo Fisher Scientific, Inc., Bio-Rad Laboratories Inc., Sysmex Corporation, Nutech Cancer Biomarkers India Pvt Ltd, Minomic, Diadem srl, Proteomedix |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |