Global Automotive Ethernet Market Size, Share, Growth Analysis Component (Hardware, Software, Services), Bandwidth (1 Gbps, 10 Mbps, 100 Mbps, 2.5/5/10 Gbps), Vehicle (Passenger Cars, Commercial Vehicles), Application (ADAS, Infotainment, Powertrain, Chassis, Others), Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 179767

- Number of Pages: 302

- Format:

-

keyboard_arrow_up

Quick Navigation

Market Overview

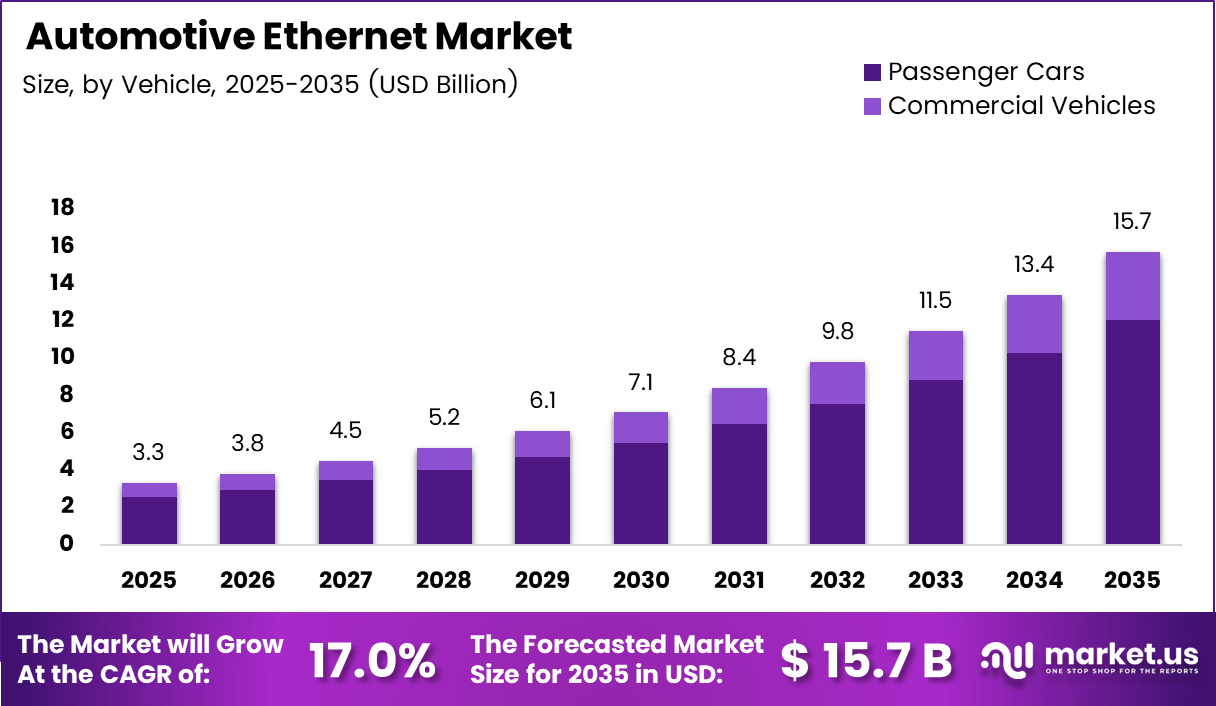

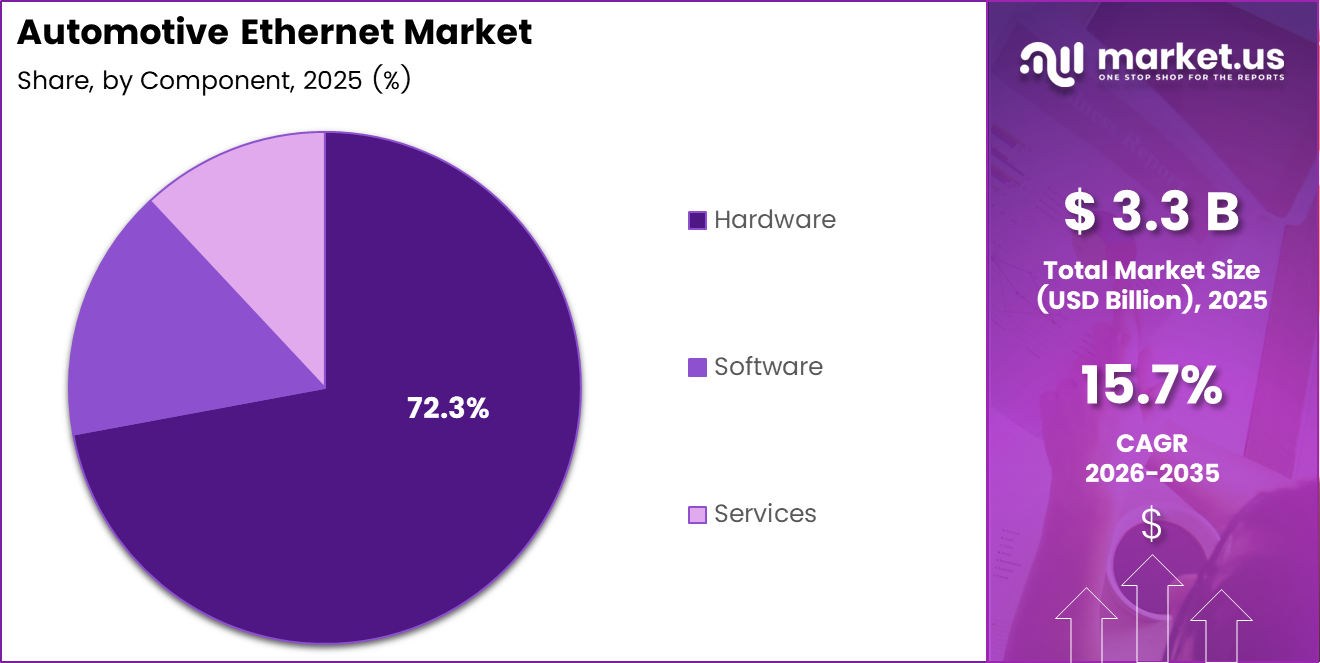

Global Automotive Ethernet Market size is expected to be worth around USD 15.7 Billion by 2035 from USD 3.3 Billion in 2025, growing at a CAGR of 17.0% during the forecast period 2026 to 2035.

Automotive Ethernet is a high-speed, in-vehicle communication technology that enables fast and reliable data transfer between electronic control units. It replaces older protocols such as CAN and LIN with a more scalable network. Moreover, it supports the growing data demands of modern vehicles.

The market is expanding rapidly as vehicles become more connected, autonomous, and software-defined. Automotive Ethernet supports high-bandwidth applications such as ADAS, infotainment, and real-time diagnostics. Consequently, automakers are integrating it into both passenger cars and commercial vehicles at an increasing pace.

Government regulations around vehicle safety, emissions, and connected infrastructure are pushing automakers to upgrade in-vehicle networks. Regulatory bodies in North America, Europe, and Asia Pacific are mandating advanced safety systems. Therefore, OEMs are investing heavily in Ethernet-based architectures to comply with these requirements.

The shift toward electric vehicles and zonal architectures is also creating strong demand for lightweight, high-speed networking. Automotive Ethernet reduces cabling weight and lowers installation costs significantly. Additionally, the rise of over-the-air software updates requires reliable, high-bandwidth communication networks in every new vehicle model.

According to the Institute of Electrical and Electronics Engineers (IEEE), standards such as 100BASE-T1, 1000BASE-T1, and Multi-Gigabit Ethernet (IEEE 802.3ch) operating at 2.5 Gbps, 5 Gbps, and 10 Gbps are now shaping the industry framework. These standards are enabling faster and more secure in-vehicle networks.

According to Prodigy Techno, the 100BASE-T1 automotive Ethernet solution reduces cabling weight by around 30% compared to shielded cabling and delivers connectivity cost savings of up to 80%. This makes it a highly attractive solution for EV manufacturers focused on range and efficiency.

Key Takeaways

- The global Automotive Ethernet Market is valued at USD 3.3 Billion in 2025.

- The market is projected to reach USD 15.7 Billion by 2035, growing at a CAGR of 17.0%.

- By Component, Hardware dominates with a 72.3% market share in 2025.

- By Bandwidth, the 1 Gbps segment holds the largest share at 43.8%.

- By Vehicle, Passenger Cars account for 76.9% of the market.

- By Application, ADAS leads with a 41.6% market share.

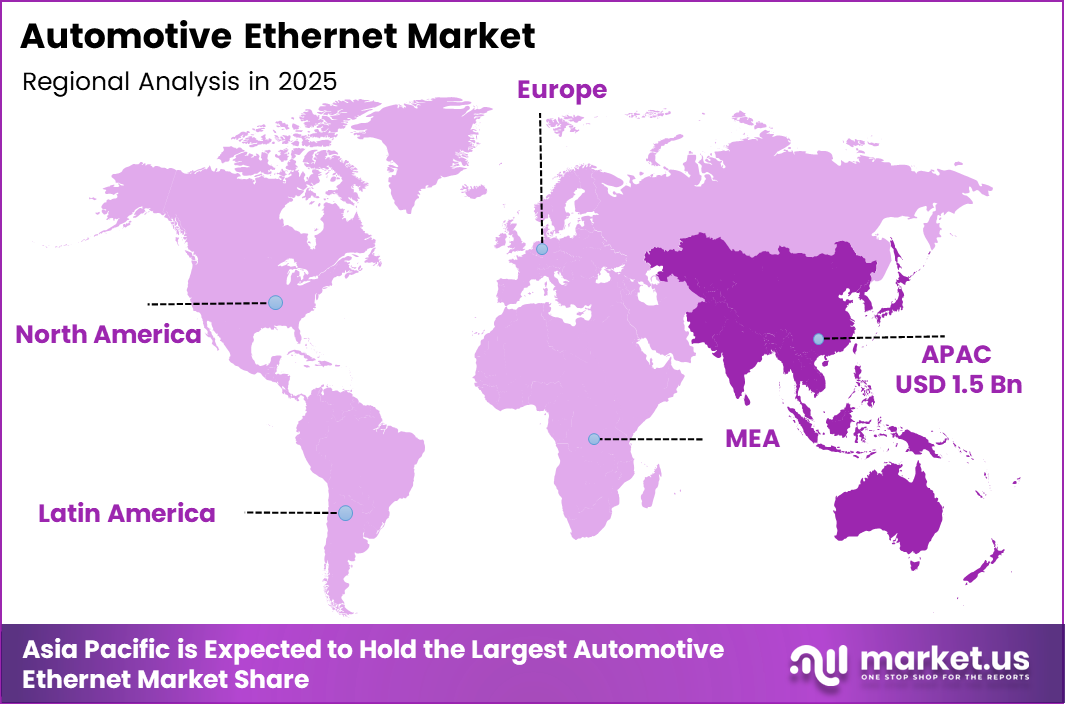

- Asia Pacific dominates the regional landscape with a 47.50% share, valued at USD 1.5 Billion.

Component Analysis

Hardware dominates with 72.3% due to high demand for PHYs, switches, and controllers across vehicle platforms.

In 2025, Hardware held a dominant market position in the Component segment of the Automotive Ethernet Market, with a 72.3% share. Hardware components such as Ethernet PHYs, switches, and transceivers form the physical backbone of in-vehicle networks. Moreover, the rapid rollout of zonal architectures and ADAS systems is driving consistent hardware procurement across global OEMs.

Software is gaining momentum as vehicles shift toward software-defined architectures requiring advanced network management tools. Middleware, protocol stacks, and diagnostic software are increasingly essential for managing complex Ethernet networks. Additionally, OTA update capabilities and real-time monitoring functions are expanding the role of software in automotive Ethernet deployments.

Services represent a growing segment covering testing, integration, and consulting support for Ethernet implementation. As Tier-1 and Tier-2 suppliers transition from legacy protocols, professional services are becoming critical. Consequently, service providers are offering specialized support for compliance with IEEE standards and vehicle-level network validation requirements.

Bandwidth Analysis

1 Gbps dominates with 43.8% due to its balance of speed, cost, and compatibility with current ADAS architectures.

In 2025, 1 Gbps held a dominant market position in the Bandwidth segment of the Automotive Ethernet Market, with a 43.8% share. This bandwidth level effectively supports camera-based ADAS, gateway functions, and backbone connections. Moreover, its compatibility with existing automotive Ethernet standards makes it the preferred choice among OEMs and Tier-1 suppliers globally.

10 Mbps bandwidth, primarily through the 10BASE-T1S standard, is widely used for cost-sensitive and low-power sensor networks. It is ideal for connecting simple actuators and body control modules within zonal architectures. Therefore, it remains relevant for in-vehicle networks requiring minimal data throughput and energy consumption.

100 Mbps Ethernet serves mid-tier automotive applications such as infotainment gateways and selected powertrain control units. It delivers higher bandwidth and improved reliability compared to legacy in-vehicle networks. This makes it an efficient and cost-effective upgrade path from traditional CAN-based systems.

2.5/5/10 Gbps Ethernet is emerging for next-generation ADAS and autonomous driving platforms.It supports the transmission of massive data volumes from cameras, LiDAR, radar, and other high-resolution sensors. This ultra-fast network performance is critical for real-time sensor fusion, decision-making, and vehicle intelligence.

Vehicle Analysis

Passenger Cars dominate with 76.9% due to high production volumes and growing feature-rich vehicle demand.

In 2025, Passenger Cars held a dominant market position in the Vehicle segment of the Automotive Ethernet Market, with a 76.9% share. The integration of advanced infotainment, safety, and connectivity features in passenger vehicles is driving Ethernet adoption rapidly. Moreover, the global push toward EVs and connected cars is accelerating network upgrades across all passenger car segments.

Commercial Vehicles represent a growing opportunity as fleet operators and logistics companies demand smarter and more connected trucks and buses. Ethernet enables real-time vehicle diagnostics, fleet tracking, and safety system integration. Consequently, commercial vehicle OEMs are beginning to adopt scalable Ethernet architectures to meet evolving regulatory and operational demands in key global markets.

Application Analysis

ADAS dominates with 41.6% due to high bandwidth requirements of camera, radar, and lidar sensor systems.

In 2025, ADAS held a dominant market position in the Application segment of the Automotive Ethernet Market, with a 41.6% share. ADAS systems require rapid, reliable data transfer between sensors, ECUs, and processors. Moreover, the expansion of Level 2 and Level 3 autonomous driving features is making high-speed Ethernet a fundamental requirement for modern vehicle development.

Infotainment systems are driving significant Ethernet adoption due to growing demand for high-definition displays, audio streaming, and connected services. In-vehicle multimedia and navigation systems require consistent, low-latency bandwidth. Additionally, passenger expectations for seamless digital experiences are pushing automakers to implement robust Ethernet backbones for infotainment systems.

Powertrain systems are adopting Ethernet to improve control, diagnostics, and data exchange. Real-time communication between engine, transmission, and drivetrain components enhances efficiency. Ethernet also supports advanced monitoring and predictive maintenance of powertrain systems.

Chassis systems are transitioning to Ethernet for faster and more reliable control communication. Real-time data exchange improves braking, steering, and suspension responsiveness. Ethernet enables precise coordination for vehicle stability and dynamic performance.

Other vehicle domains, including body control and lighting systems, are progressively adopting Ethernet connectivity. This shift supports seamless integration of multiple electronic functions within centralized vehicle architectures. As networks converge, Ethernet enables unified, high-speed communication across diverse automotive subsystems.

Key Market Segments

By Component

- Hardware

- Software

- Services

By Bandwidth

- 1 Gbps

- 10 Mbps

- 100 Mbps

- 2.5/5/10 Gbps

By Vehicle

- Passenger Cars

- Commercial Vehicles

By Application

- ADAS

- Infotainment

- Powertrain

- Chassis

- Others

Drivers

Rising Data Bandwidth Demand from ADAS and Connected Vehicle Architectures Drives Market Growth

Modern vehicles require massive data throughput to support ADAS, autonomous driving, and high-resolution displays. Legacy communication protocols such as CAN and LIN cannot meet these demands. Consequently, OEMs are transitioning to automotive Ethernet, which offers significantly higher bandwidth and the scalability needed for next-generation vehicle platforms.

The shift toward zonal vehicle architecture is replacing traditional domain-based networks with centralized Ethernet backbones. This transition reduces wiring complexity and overall vehicle weight. Moreover, zonal controllers rely on Ethernet to aggregate data from multiple sensors and ECUs, making high-speed in-vehicle networking an essential part of modern automotive design.

OEM focus on lightweight wiring is directly supporting Ethernet adoption, especially in electric vehicles where weight reduction improves driving range. Additionally, the rapid integration of high-resolution infotainment systems and in-vehicle displays demands continuous, high-bandwidth connectivity. Therefore, automotive Ethernet has become a critical enabler of both efficiency and passenger experience in new vehicle models.

Restraints

High Transition Costs and Limited Supplier Expertise Restrain Automotive Ethernet Adoption

Transitioning from legacy CAN and LIN protocols to automotive Ethernet involves significant investment in hardware, software, and infrastructure. Many Tier-2 and Tier-3 suppliers lack the resources to upgrade production lines and testing facilities quickly. Consequently, the cost barrier is slowing full-scale adoption, especially among smaller suppliers operating on tight margins.

Limited automotive Ethernet expertise across the broader supplier base is a key challenge. Many engineers and technicians are trained on legacy protocols and require retraining to handle Ethernet-based systems. Moreover, the complexity of Ethernet standards compliance adds engineering overhead that smaller organizations struggle to manage without dedicated development teams or external support.

Additionally, integrating automotive Ethernet into existing vehicle platforms requires extensive testing and validation against IEEE and OEM-specific standards. This process is time-consuming and costly. Therefore, vehicle programs with tight development timelines often delay full Ethernet migration, creating a transitional gap that temporarily limits market penetration across certain vehicle segments and supply chain tiers.

Growth Factors

Software-Defined Vehicles and EV Expansion Accelerate Automotive Ethernet Market Growth

The expansion of software-defined vehicles is creating strong demand for high-speed in-car communication networks. These vehicles rely on continuous software updates, real-time diagnostics, and centralized compute platforms. Moreover, automotive Ethernet provides the bandwidth and reliability required to support dynamic software environments and over-the-air update capabilities across the full vehicle lifecycle.

Rapid adoption of Ethernet in electric and connected vehicles is a major growth driver. EVs require efficient, lightweight networks to manage battery systems, motor controllers, and advanced driver assistance features. Additionally, connected vehicle platforms depend on fast, secure data exchange between onboard systems and cloud services, making automotive Ethernet a foundational technology for next-generation EV architectures.

Standardization of multi-gigabit automotive Ethernet is enabling broader adoption across new vehicle platforms. IEEE standards such as 802.3ch operating at 2.5 Gbps, 5 Gbps, and 10 Gbps provide a clear framework for OEMs and suppliers. Consequently, emerging demand for OTA updates and real-time diagnostics is further reinforcing the business case for upgrading to scalable Ethernet-based vehicle networks.

Emerging Trends

Multi-Gig Ethernet, Zonal Controllers, and AI Integration Reshape the Automotive Network Landscape

The deployment of 10BASE-T1S and multi-gigabit Ethernet technologies is accelerating across new vehicle programs globally. These standards enable cost-effective, high-speed connectivity for diverse in-vehicle applications. Moreover, 10BASE-T1S is specifically gaining traction in low-bandwidth sensor networks, while multi-gig solutions are being adopted for backbone and ADAS applications requiring extreme throughput.

Zonal controllers using Ethernet backbone networks are transforming how vehicles manage data and communication. This architecture consolidates multiple domain controllers into fewer, more powerful zonal units connected by Ethernet. Additionally, the approach reduces wiring harness complexity significantly, lowers vehicle weight, and improves scalability for future software and hardware updates throughout the vehicle’s lifetime.

The convergence of automotive Ethernet with AI-driven sensor fusion systems is an emerging and critical trend. Autonomous driving platforms require low-latency data aggregation from cameras, radar, and lidar. Furthermore, rising collaboration between OEMs and semiconductor vendors is accelerating the development of integrated Ethernet solutions that support AI workloads directly within the vehicle’s high-speed communication infrastructure.

Regional Analysis

Asia Pacific Dominates the Automotive Ethernet Market with a Market Share of 47.50%, Valued at USD 1.5 Billion

Asia Pacific leads the global Automotive Ethernet Market with a dominant share of 47.50%, valued at USD 1.5 Billion in 2025. The region benefits from high automotive production volumes in China, Japan, South Korea, and India. Moreover, strong government support for EV adoption and connected vehicle infrastructure is driving rapid deployment of advanced in-vehicle networking technologies across the region.

North America Automotive Ethernet Market Trends

North America holds a significant share driven by strong OEM investment in autonomous and connected vehicle platforms. The United States is home to leading semiconductor vendors and automotive technology developers advancing Ethernet adoption. Additionally, federal safety mandates and the growing EV market are pushing automakers to upgrade in-vehicle communication networks toward high-speed Ethernet architectures.

Europe Automotive Ethernet Market Trends

Europe is a mature and innovation-driven market for automotive Ethernet, supported by strict vehicle safety regulations and strong OEM presence. Germany, France, and the UK lead adoption through active investment in ADAS and electrification programs. Furthermore, European standardization bodies are actively collaborating with IEEE to align automotive Ethernet compliance requirements across the regional supply chain.

Middle East and Africa Automotive Ethernet Market Trends

The Middle East and Africa market is at an early stage of automotive Ethernet adoption but shows steady growth potential. Rising vehicle imports, smart city initiatives, and increasing connected vehicle awareness are creating demand. Moreover, GCC countries are investing in transportation infrastructure upgrades that indirectly support the deployment of advanced automotive communication technologies in the region.

Latin America Automotive Ethernet Market Trends

Latin America presents a developing opportunity for automotive Ethernet, with Brazil and Mexico leading regional automotive production. OEM assembly plants in the region are beginning to adopt Ethernet-based architectures aligned with global vehicle platforms. Consequently, as EV penetration grows and safety regulations strengthen, demand for high-speed in-vehicle networking solutions is expected to rise steadily across Latin America.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Broadcom Inc. is a leading force in the automotive Ethernet semiconductor space, offering a broad portfolio of PHY and switch solutions designed for in-vehicle networks. The company’s automotive-grade products support speeds from 100 Mbps to 10 Gbps. Moreover, Broadcom’s deep integration with OEM and Tier-1 ecosystems positions it as a critical enabler of zonal Ethernet architectures globally.

Microchip Technology Inc. delivers a comprehensive range of automotive Ethernet controllers, PHYs, and protocol stacks that support multiple IEEE standards. The company focuses on providing end-to-end solutions for both legacy migration and next-generation vehicle platforms. Additionally, Microchip’s strong support for 10BASE-T1S makes it highly relevant for the growing single-pair Ethernet sensor network segment.

Marvell Technology Inc. has established a strong position in automotive Ethernet with advanced multi-gigabit PHY and switch products. The company’s solutions target high-bandwidth applications including ADAS and centralized computing architectures. However, following the acquisition of its automotive Ethernet business by Infineon in August 2025, the competitive dynamics within this segment have undergone a notable structural shift.

NXP Semiconductors N.V. is a key player offering integrated automotive Ethernet solutions combining PHYs, switches, and microcontrollers for connected vehicle applications. The company’s acquisition of Aviva Links in December 2024 for USD 242.5 million further strengthens its SerDes and high-speed networking capabilities. Consequently, NXP is well-positioned to address the growing demand for multi-gig Ethernet in next-generation vehicles.

Key Players

- Broadcom Inc.

- Microchip Technology Inc.

- Marvell Technology Inc.

- NXP Semiconductors N.V.

- Texas Instruments Inc.

- Cadence Design Systems, Inc.

- Keysight Technologies Inc.

- STMicroelectronics NV

- Analog Devices Inc.

- Realtek Semiconductor Corp.

Recent Developments

- August 2025 – Infineon Technologies successfully completed the acquisition of Marvell’s Automotive Ethernet business, consolidating a major portfolio of automotive-grade PHY and switch products. This strategic move significantly strengthens Infineon’s position in the high-speed in-vehicle networking market and expands its BRIGHTLANE product offering across global OEM platforms.

- December 2024 – NXP Semiconductors announced the acquisition of US-based SerDes startup Aviva Links for USD 242.5 million in cash. This deal enhances NXP’s high-speed connectivity capabilities and supports its roadmap for multi-gigabit automotive Ethernet solutions targeting next-generation ADAS and software-defined vehicle architectures.

Report Scope

Report Features Description Market Value (2025) USD 3.3 Billion Forecast Revenue (2035) USD 15.7 Billion CAGR (2026-2035) 17.0% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered Component (Hardware, Software, Services), Bandwidth (1 Gbps, 10 Mbps, 100 Mbps, 2.5/5/10 Gbps), Vehicle (Passenger Cars, Commercial Vehicles), Application (ADAS, Infotainment, Powertrain, Chassis, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Broadcom Inc., Microchip Technology Inc., Marvell Technology Inc., NXP Semiconductors N.V., Texas Instruments Inc., Cadence Design Systems Inc., Keysight Technologies Inc., STMicroelectronics NV, Analog Devices Inc., Realtek Semiconductor Corp. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Broadcom Inc.

- Microchip Technology Inc.

- Marvell Technology Inc.

- NXP Semiconductors N.V.

- Texas Instruments Inc.

- Cadence Design Systems, Inc.

- Keysight Technologies Inc.

- STMicroelectronics NV

- Analog Devices Inc.

- Realtek Semiconductor Corp.

Our Clients

- 179767

- Feb 2026