Australia Medical Cannabis Market By Source (Hemp and Marijuana), By Derivative (CBD, THC and Others), By Application (Chronic Pain, Cancer, Anxiety and Depression, Arthritis, Epilepsy and Others), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 180283

- Number of Pages: 288

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

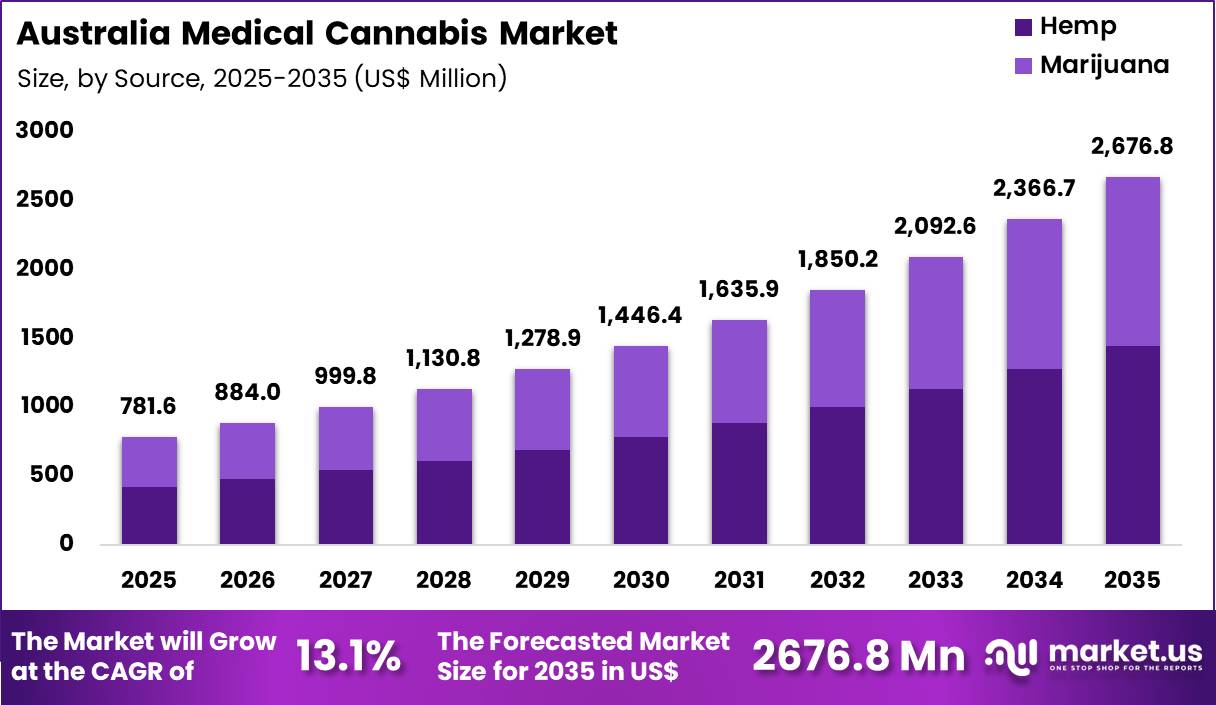

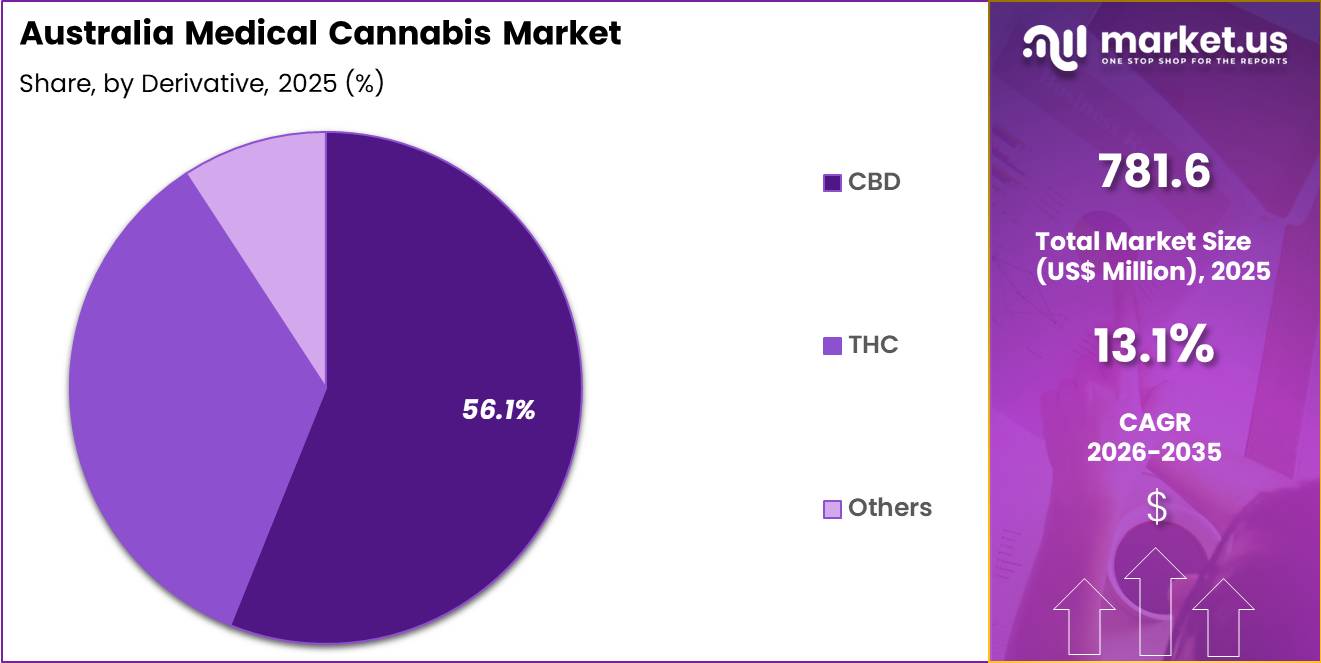

The Global Australia Medical Cannabis Market size is expected to be worth around US$ 2676.8 Million by 2035 from US$ 781.6 Million in 2025, growing at a CAGR of 13.1 during the forecast period 2026-2035.

Increasing acceptance of cannabinoid-based therapies accelerates the Australia Medical Cannabis market as patients and healthcare providers recognize its potential in managing chronic and complex conditions. Physicians prescribe medical cannabis for severe chronic pain in cancer patients, where THC and CBD combinations reduce opioid dependency and improve quality of life.

These products support epilepsy treatment by decreasing seizure frequency in refractory cases through CBD-dominant formulations. Neurologists apply medical cannabis to alleviate spasticity in multiple sclerosis patients, enhancing mobility and daily functioning.

Palliative care specialists utilize it to control nausea and vomiting induced by chemotherapy, allowing better tolerance of treatment regimens. Patients with anxiety disorders and PTSD benefit from balanced THC-CBD products that promote relaxation without significant psychoactive effects.

Manufacturers pursue opportunities to develop novel delivery methods such as oral oils, capsules, and vaporizers that improve bioavailability and patient adherence in long-term therapies. Developers advance research into new indications like inflammatory bowel disease and neurodegenerative disorders, broadening the therapeutic scope of medical cannabis.

These advancements facilitate integration with conventional treatments for multimodal pain management in fibromyalgia and arthritis. Opportunities emerge in personalized formulations based on patient genetics and symptom profiles.

Recent trends emphasize high-CBD low-THC products for pediatric epilepsy and non-psychoactive applications, alongside rigorous clinical trials that validate efficacy and safety. Companies focus on quality assurance and standardized dosing to build physician confidence and expand mainstream medical adoption.

Key Takeaways

- In 2025, the market generated a revenue of US$ 718.6 Million, with a CAGR of 13.1, and is expected to reach US$ 2676.8 Million by the year 2035.

- The source segment is divided into hemp and marijuana, with hemp taking the lead with a market share of 54.1%.

- Considering derivative, the market is divided into CBD, THC and others. Among these, CBD held a significant share of 56.1%.

- Furthermore, concerning the application segment, the market is segregated into chronic pain, cancer, anxiety and depression, arthritis, epilepsy and others. The chronic pain sector stands out as the dominant player, holding the largest revenue share of 51.8% in the market.

Source Analysis

Hemp accounted for 54.1% of growth within source and dominate the Australia medical cannabis market due to its regulatory flexibility and broader commercial acceptance. Authorities permit low-dose CBD products derived from hemp under structured access schemes, which supports steady market expansion.

Manufacturers increasingly focus on hemp cultivation to ensure compliance with low THC thresholds and quality standards. Segment growth is projected to strengthen as demand for plant-based wellness products increases across Australia.

Industrial-scale hemp farming improves raw material availability and reduces supply chain dependency. Producers leverage hemp’s versatility for both therapeutic formulations and wellness supplements. Demand is anticipated to rise as patients seek non-intoxicating alternatives for symptom management. Expanding domestic cultivation programs further reinforce hemp’s leading position in the market.

Derivative Analysis

CBD accounted for 56.1% of growth within derivatives and dominate due to its non-psychoactive profile and wide therapeutic acceptance. Healthcare professionals increasingly prescribe CBD-based formulations for pain, anxiety, and seizure-related conditions under regulated frameworks. Segment growth is expected to accelerate as clinical awareness and prescribing confidence improve among Australian practitioners.

CBD products align with consumer preference for treatments that avoid psychoactive effects. Pharmaceutical companies expand research initiatives to validate efficacy and dosing protocols. Demand is likely to increase as over-the-counter low-dose CBD pathways become more accessible.

Retail pharmacies and authorized prescribers promote CBD products for symptom management within controlled guidelines. Ongoing product innovation in oils, capsules, and topical forms strengthens adoption across multiple patient groups.

Application Analysis

Chronic pain accounted for 51.8% of growth within applications and dominate due to the rising prevalence of long-term musculoskeletal and neuropathic conditions in Australia. Patients increasingly explore cannabis-based therapies when conventional analgesics provide limited relief.

Segment growth is projected to strengthen as prescribers integrate medical cannabis into multidisciplinary pain management programs. Chronic pain patients seek alternatives that reduce reliance on opioids and other high-risk medications. Regulatory support under the Special Access Scheme facilitates patient enrollment and treatment continuity.

Demand is anticipated to expand as aging populations experience higher incidence of arthritis and degenerative disorders. Healthcare providers prioritize indivi

dualized dosing strategies to optimize symptom control. Increasing clinical data and patient-reported outcomes further reinforce chronic pain as the primary application segment.

dualized dosing strategies to optimize symptom control. Increasing clinical data and patient-reported outcomes further reinforce chronic pain as the primary application segment.Key Market Segments

By Source

- Hemp

- Marijuana

By Derivative

- CBD

- THC

- Others

By Application

- Chronic Pain

- Cancer

- Anxiety and Depression

- Arthritis

- Epilepsy

- Others

Drivers

Increasing Special Access Scheme Category B approvals is driving the market.

The Therapeutic Goods Administration documented a substantial rise in Special Access Scheme Category B approvals for unapproved medicinal cannabis products. This pathway enables faster access for patients with specific clinical needs under medical supervision. Approvals reached 177,762 during 2024 according to official TGA consultation documentation.

Such volume reflects heightened prescriber confidence and patient demand across chronic conditions. The growth builds upon earlier trends observed since 2020 when approvals stood at 57,711. Practitioners utilise the scheme to address unmet needs where registered alternatives remain limited.

Increased approvals directly stimulate supply chain activity among licensed importers and manufacturers. Patients gain broader therapeutic options through streamlined authorisation processes. The sustained elevation in approvals during the 2022-2025 interval underscores expanding integration of medicinal cannabis into Australian clinical practice. This driver sustains market expansion by validating therapeutic utility and encouraging ongoing product development.

Restraints

Limited registration of medicinal cannabis products on the Australian Register of Therapeutic Goods is restraining the market.

The Therapeutic Goods Administration maintains strict criteria for entry onto the Australian Register of Therapeutic Goods for medicinal cannabis products. Only two products hold registered status as of the latest regulatory overview. These consist of Epidyolex for specific epileptic conditions and Sativex for multiple sclerosis symptoms.

The overwhelming majority of available options therefore require unapproved pathways such as Special Access Scheme or Authorised Prescriber routes. This limitation creates administrative burdens for prescribers seeking consistent supply.

Pharmacists and distributors face added compliance requirements when handling unregistered items. Patients encounter variability in product quality assurance compared to fully registered medicines. The constraint slows broader adoption by conservative healthcare providers wary of regulatory complexities.

Supply stability remains vulnerable to import fluctuations under unapproved status. Overall, the restricted registration profile tempers full mainstream acceptance and infrastructure investment across the sector during the 2022-2025 period.

Opportunities

Achievement of net profit by key players is creating growth opportunities.

Little Green Pharma, a key player, documented a turnaround to positive financial performance within its Australian operations. The company recorded a net profit attributable to owners of $3,324,000 for the financial year ended 31 March 2025. This outcome reversed a loss of $8,152,000 reported for the financial year ended 31 March 2024.

Adjusted EBITDA improved to $2,893,000 from a negative $1,601,000 in the prior year. Such profitability provides capital for expanded research into new formulations and delivery systems. Opportunities emerge for enhanced marketing and prescriber education programmes. The strengthened balance sheet supports investment in quality assurance and supply chain optimisation.

Stakeholders benefit from greater confidence in long-term viability of domestic production. The achievement enables exploration of export pathways while maintaining Australian focus. This opportunity fosters innovation and scalability within the medicinal cannabis ecosystem throughout the 2024-2025 interval.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions influence the Australia medical cannabis market through patient affordability, private health coverage, and investment in cultivation and processing facilities. Inflation increases operating costs for indoor growing, energy consumption, compliance testing, and distribution, which raises product pricing for patients.

Higher interest rates limit access to expansion capital for licensed producers and dispensary networks. Geopolitical tensions affect global trade in cannabis genetics, extraction equipment, and pharmaceutical grade inputs, creating sourcing variability.

Current US tariffs on imported cultivation technology and specialized processing components increase equipment acquisition costs for Australian operators that rely on US suppliers. These pressures can slow facility upgrades and delay new product development.

At the same time, producers strengthen local supply chains and invest in domestic manufacturing capabilities to reduce external dependence. Growing physician acceptance and expanding patient access pathways continue to support steady and confident long term market growth.

Latest Trends

Record revenue growth in Australian medicinal cannabis sales is driving the market.

Little Green Pharma, a key player, documented robust expansion in its Australian revenue streams during the recent reporting period. Revenue from ordinary activities reached $36,841,000 for the financial year ended 31 March 2025. This represented a 42.8% increase from $25,803,000 achieved in the financial year ended 31 March 2024.

Australia-specific revenue totalled $30,097,000 in the 2025 financial year. The figure advanced from $22,475,000 recorded in the preceding year. The company attained a 52% compound annual growth rate across its Australian operations between the financial years ended 31 March 2022 and 2025.

Sales encompassed expanded offerings in oils, flower, and vaporiser formats. The performance aligns with rising clinical acceptance and patient uptake nationwide. Domestic cultivation adjustments further supported efficient fulfilment of demand. This trend signals accelerating commercial maturity and positions the sector for sustained advancement in 2025.

Key Players Analysis

Key participants in Australia’s medical cannabis market expand growth by strengthening prescriber education programs, improving patient onboarding through telehealth networks, and ensuring strict compliance with Therapeutic Goods Administration pathways to maintain regulatory confidence. They invest in GMP certified cultivation and manufacturing facilities to guarantee consistent product quality and reliable supply across pharmacies and authorized prescribers.

Companies diversify their portfolios with oils, capsules, and inhalation formats to address chronic pain, anxiety, and oncology related indications while tailoring formulations to physician preferences. Many operators also pursue export approvals to Europe and Asia to balance domestic demand with international revenue streams.

For example, Little Green Pharma, founded in 2016 and headquartered in Western Australia, operates vertically integrated cultivation and production facilities in Australia and Denmark, focusing on pharmaceutical grade cannabinoid products.

Through disciplined compliance management, strategic distribution partnerships, and product innovation, leading firms reinforce credibility with clinicians and position themselves for sustained commercial expansion.

Top Key Players

- Cann Group (Refinanced and debt-restructured in 2025)

- Zelira Therapeutics

- AusCann Group Holdings Ltd

- Bod Science

- Althea Group

- Little Green Pharma (Announced merger with Cannatrek in Jan 2026)

- Incannex Healthcare

- Vitura Health Limited (Formerly Cronos Australia)

- Bioxyne

- Green Farmers

- ECS Botanics

- Tasmanian Botanics

Recent Developments

- In 2026, Little Green Pharma (LGP) announced a transformational merger with Cannatrek to create a combined medicinal cannabis entity with pro forma revenues of approximately US$ 73.2 million (AUD 112 million). As per the merger filing, the new group will leverage GMP-certified manufacturing facilities in the US and Denmark to scale its export capabilities and consolidate its domestic market position.

- In 2026, Vitura Health Limited reported H1 FY2026 revenues of US$ 44.4 million (AUD 67.9 million), marking an 8.3% increase over the prior period. According to the company’s interim financial report, this growth was driven by a 10.6% rise in unit sales via its Canview distribution platform, which now hosts over 760 different medicinal cannabis products and 88 individual brands.

Report Scope

Report Features Description Market Value (2025) US$ 781.6 Million Forecast Revenue (2035) US$ 2676.8 Million CAGR (2026-2035) 13.1 Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Source (Hemp and Marijuana), By Derivative (CBD, THC and Others), By Application (Chronic Pain, Cancer, Anxiety and Depression, Arthritis, Epilepsy and Others) Competitive Landscape Cann Group, Zelira, AusCann, Bod Science, Althea, Little Green Pharma, Incannex, Vitura Health, Bioxyne, Green Farmers, ECS Botanics, Tasmanian Botanics Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Australia Medical Cannabis MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Australia Medical Cannabis MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Cann Group (Refinanced and debt-restructured in 2025)

- Zelira Therapeutics

- AusCann Group Holdings Ltd

- Bod Science

- Althea Group

- Little Green Pharma (Announced merger with Cannatrek in Jan 2026)

- Incannex Healthcare

- Vitura Health Limited (Formerly Cronos Australia)

- Bioxyne

- Green Farmers

- ECS Botanics

- Tasmanian Botanics

Our Clients

- 180283

- March 2026