Global Artificial Tendons and Ligaments Market By Application (Knee Injuries, Shoulder Injuries, Foot and Ankle Injuries and Others) By End-use (Hospitals & Clinics and Ambulatory Surgery Centers) By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2024-2033

- Published date: Nov 2023

- Report ID: 65628

- Number of Pages: 216

- Format:

- keyboard_arrow_up

Quick Navigation

Report Overview

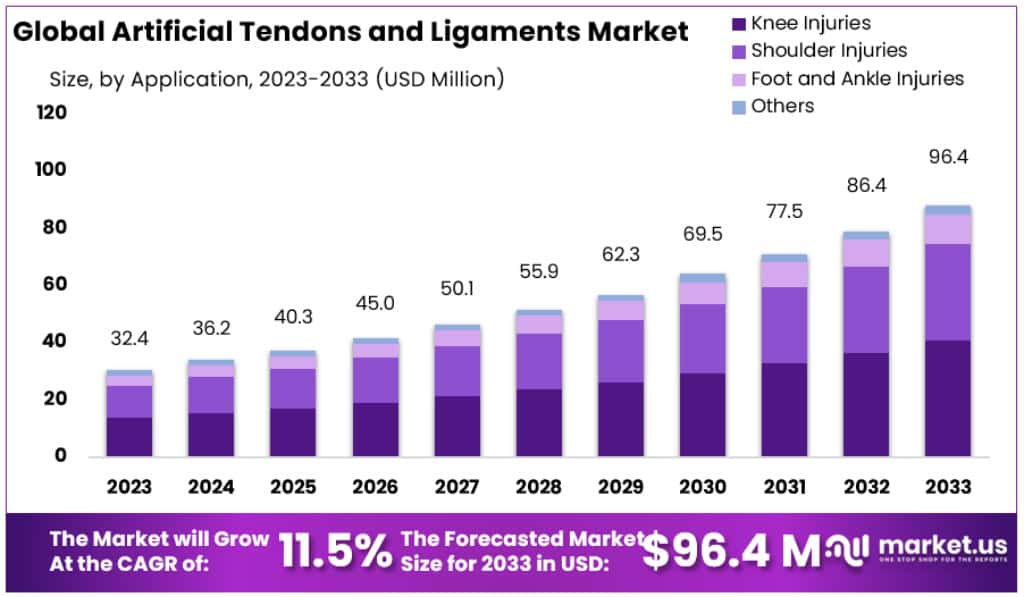

The Global Artificial Tendons and Ligaments Market size is expected to be worth around USD 96.4 Million by 2033, from USD 32.4 Million in 2023, growing at a CAGR of 11.5% during the forecast period from 2024 to 2033.

Artificial tendons and ligaments are devices used to replace damaged or missing tendons and ligaments, respectively. They are made from synthetic materials and have been developed to mimic the structure, strength, and durability of natural tendons and ligaments.

The increasing prevalence of injuries in sports drives this market. Sports injuries are often caused by improper equipment, bad training, improper practice, inadequate warm-up, stretching, or the absence of conditioning. Sports injuries commonly seen in athletes include groin pulls, hamstring strains, ACL tears, tennis elbow, and hamstring strains.

Key Takeaways

- The Artificial Tendons and Ligaments Market is expected to be worth USD 96.4 million by 2033, a significant increase from USD 32.4 million in 2023.

- The market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.5% from 2024 to 2033.

- Knee Injuries held the largest market share in 2023, accounting for over 42.5% of the market.

- Hospitals & Clinics dominated the market in 2023, with a share of more than 64%.

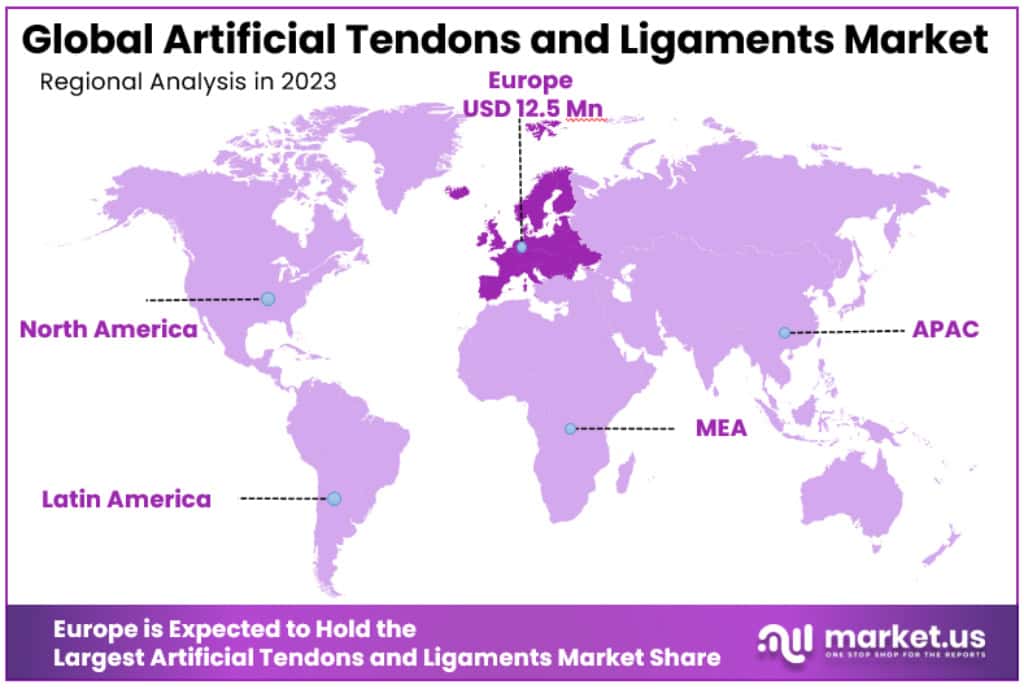

- Europe dominated the market in 2023, with a value of USD 12.5 million.

Application Analysis

Knee Injuries

In 2023, Knee Injuries held a dominant market position, capturing more than a 42.5% share. This significant portion is due to the high incidence of sports-related knee injuries and the aging population experiencing knee degeneration. Innovative artificial tendons and ligaments, offering better outcomes and quicker recovery, are driving this segment’s growth.

Shoulder Injuries

Shoulder injuries form another vital segment in the market. Although smaller than knee injuries, this segment benefits from increased awareness and improved surgical techniques. Athletes, particularly in sports involving overhead activities, frequently sustain shoulder injuries, boosting demand for advanced artificial solutions.

Foot and Ankle Injuries

The market for artificial tendons and ligaments for foot and ankle injuries is growing steadily. Factors such as lifestyle-related sports activities and accidents contribute to this trend. The foot and ankle segment, though not as large as knee injuries, is gaining traction due to improved success rates in surgeries and prosthetics.

Other Injuries

This segment includes injuries related to the hip, spine, and elbows, among others. While it holds a smaller share compared to knee and shoulder injuries, it shows potential for growth. Innovations in artificial tendons and ligaments, catering to a wider range of injuries, are expected to propel this segment in the coming years.

End-use Analysis

Hospitals & Clinics

In 2023, Hospitals & Clinics held a dominant market position, capturing more than a 64% share. This dominance is largely due to their comprehensive facilities and the trust patients place in them for complex procedures. Hospitals and clinics, equipped with advanced technologies and specialized staff, are the primary choice for tendon and ligament surgeries, driving their high market share.

Ambulatory Surgery CentersAmbulatory Surgery Centers (ASCs) are rapidly growing in this market. They are favored for their cost-effectiveness and convenience, especially for less complicated procedures. In 2023, ASCs have seen an increase in patient preference due to their efficiency, shorter waiting times, and the trend towards outpatient surgical procedures.

Кеу Маrkеt Ѕеgmеntѕ

By Application

- Knee Injuries

- Shoulder Injuries

- Foot and Ankle Injuries

- Others

By End-Use

- Hospitals & Clinics

- Ambulatory Surgery Centers

Driver

- Increased Sports Injuries: A key factor driving the market is the rise in sports-related injuries. These injuries often result from accidents, improper techniques, and insufficient warm-up or conditioning. Common sports injuries include tennis elbow, ankle sprains, and ACL tears. For example, in the U.S. and U.K., these injuries are increasingly prevalent due to the growing popularity of sports.

Restraint

- High Costs and Safety Concerns: The growth of the artificial tendons and ligaments market is limited by the high expenses associated with research and development, as well as safety and regulatory challenges. Healthcare providers often hesitate to use these products due to their high cost and the risks involved, like the possibility of inflammation in patients.

Opportunity

- Technological Advancements: Innovations in material and manufacturing techniques are creating new opportunities. These advancements lead to improved implant designs, offering better performance and durability. Increased investment in research and development, coupled with growing awareness, presents significant growth opportunities.

Challenge

- Regulatory and Cost Barriers: The complex manufacturing processes and stringent regulatory requirements create challenges. Additionally, the high cost of implants and time-consuming approval processes can hinder market growth.

Trends

- Knee Injuries Leading the Market: The segment dealing with knee injuries is expected to dominate the market. Factors contributing to this include an increase in sports participation and the discomfort caused by traditional surgical methods. For instance, Canada reports nearly 140,000 hip or knee replacements annually, with healthcare spending on knee replacement surgery exceeding USD 1.4 billion each year. Injuries from exercise equipment and bicycles also contribute significantly to this trend.

Regional Analysis

Europe is dominating Artificial Tendons and Ligaments Market Market with USD 12.5 million value in 2023. This was due to increasing consumer acceptance and better knowledge about artificial grafts for various sports injuries. The presence of major regional players will also stimulate market growth.

France, Germany, and the United Kingdom are Europe’s largest markets. They accounted for more than 59% of all income in 2018. Because more people participate in sports in Europe, this has resulted in increased Anterior Cruciate Ligament (ACL) ruptures.

According to a 2017 Health Economics Review paper, Germany treats approximately 30,000 ACL ruptures annually. As per a 2017 Health Economics Review paper, the hospital costs in Germany are US$129.61 million.

APAC is expected to experience significant market expansion over this forecast period. This industry is driven by significant investments in R&D by international market leaders and growing public awareness concerning artificial tendons, ligaments, and ACL surgeries. China and India are expected to expand at a rapid pace, however, Australia & Japan have established markets in this area. Orthopedic surgery involving the knee, ankle, and shoulder often uses autologous, allogenic ligaments. Despite the fact that LARS artificial ligament is widely used in Canada & other European countries, the U.S. FDA is yet to approve the same.

Key Regions and Countries

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Russia

- Spain

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- MEA

- GCC

- South Africa

- Israel

- Rest of MEA

Key Players Analysis

Corin Group, Xiros Ltd. (Neoligament), and Mathys AG Bettlach are three of the most notable industry players. To boost their respective market position, these businesses are now concentrating on growing their circulation networks, R&D facilities, and given geographic reach. They participate in conferences to display their goods and expand their clientele. Orthomed S.A.S., Arthrex Inc., Olympus, Cousin Biotech, FX Solutions, and Stryker Corporation are other key players in this market.

Маrkеt Кеу Рlауеrѕ

- Corin Group

- Xiros Ltd. (Neoligament)

- Mathys AG Bettlach

- Orthomed S.A.S.

- Arthrex Inc.

- Olympus

- Cousin Biotech

- Artelon

- Corin Groups

- F H Orthopedics

- fx solutions

- Mathys AG

- FX Solutions

- Integra Lifesciences Corporation

- Stryker Corporation

- Other Key Players

Recent Developments

- October 2023: Stryker Corporation announces the launch of its new LARS (Ligament Augmentation Reconstruction System) for anterior cruciate ligament (ACL) reconstruction. The LARS system is designed to provide a more natural and durable solution for ACL repair compared to traditional allograft tissues.

- September 2023: Arthrex, Inc. receives FDA clearance for its new GraftLink ACL Tightener system. The GraftLink system is a minimally invasive device that is used to tighten ACL grafts after surgery.

- August 2023: MTF Biologics, Inc. announces the completion of enrollment in its Phase 2 clinical trial of its novel tendon repair implant. The implant is made from a proprietary biomaterial that is designed to promote tendon healing.

- July 2023: Conventus Orthopedics, Inc. receives FDA clearance for its new Meniscus Repair Device. The device is designed to repair torn menisci, which are the cartilage-like cushions in the knee.

- June 2023: Smith & Nephew, Inc. launches its new RegenX Tendon allograft tissue. The RegenX Tendon is a tissue-engineered product that is designed to provide a more durable and effective solution for tendon repair compared to traditional allograft tissues.

- December 2022: CoNextions, Inc. announces that its CoNextions TR Tendon Repair System has received FDA clearance. The CoNextions TR system is a minimally invasive device that is used to repair ruptured tendons.

- November 2022: Ossur, Inc. launches its new LARS Ligament Augmentation Reconstruction System for ACL reconstruction.

Report Scope

Report Features Description Market Value (2023) USD 32.4 Million Forecast Revenue (2033) USD 96.4 Million CAGR (2024-2033) 11.5% Base Year for Estimation 2023 Historic Period 2017-2022 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Application (Knee Injuries, Shoulder Injuries, Foot and Ankle Injuries and Others) By End-use (Hospitals & Clinics and Ambulatory Surgery Centers) Regional Analysis North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Corin Group, Xiros Ltd. (Neoligament), Mathys AG Bettlach, Orthomed S.A.S., Arthrex Inc, Olympus, Cousin Biotech, Artelon, Corin Groups, F H Orthopedics, fx solutions, Mathys AG, FX Solutions, Integra Lifesciences Corporationm, Stryker Corporation and Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Artificial Tendons and Ligaments MarketPublished date: Nov 2023add_shopping_cartBuy Now get_appDownload Sample

Artificial Tendons and Ligaments MarketPublished date: Nov 2023add_shopping_cartBuy Now get_appDownload Sample - Corin Group

- Xiros Ltd. (Neoligament)

- Mathys AG Bettlach

- Orthomed S.A.S.

- Arthrex Inc.

- Olympus

- Cousin Biotech

- Artelon

- Corin Groups

- F H Orthopedics

- fx solutions

- Mathys AG

- FX Solutions

- Integra Lifesciences Corporation

- Stryker Corporation Company Profile

- Other Key Players

- settingsSettings

Our Clients

- 65628

- Nov 2023

| Single User $4,599 $3,499 USD / per unit save 24% | Multi User $5,999 $4,299 USD / per unit save 28% | Corporate User $7,299 $4,999 USD / per unit save 32% | |

|---|---|---|---|

| e-Access | |||

| Report Library Access | |||

| Data Set (Excel) | |||

| Company Profile Library Access | |||

| Interactive Dashboard | |||

| Free Custumization | No | up to 10 hrs work | up to 30 hrs work |

| Accessibility | 1 User | 2-5 User | Unlimited |

| Analyst Support | up to 20 hrs | up to 40 hrs | up to 50 hrs |

| Benefit | Up to 20% off on next purchase | Up to 25% off on next purchase | Up to 30% off on next purchase |

| Buy Now ($ 3,499) | Buy Now ($ 4,299) | Buy Now ($ 4,999) |