Quick Navigation

Report Overview

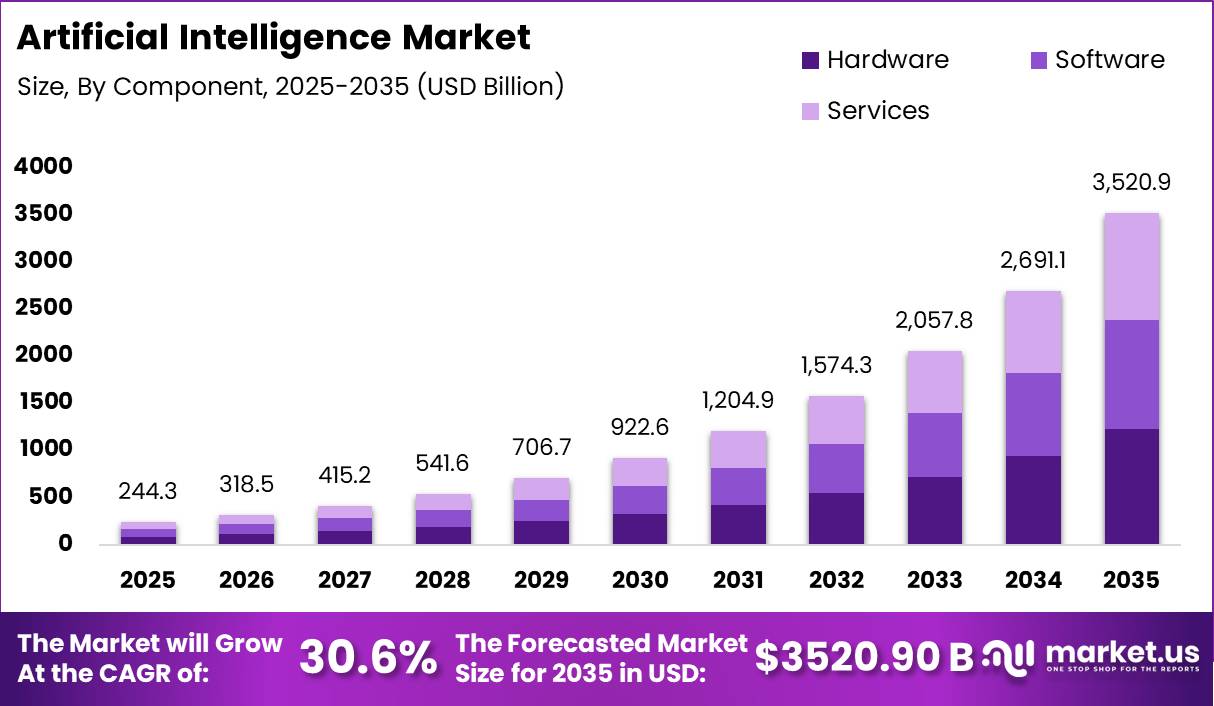

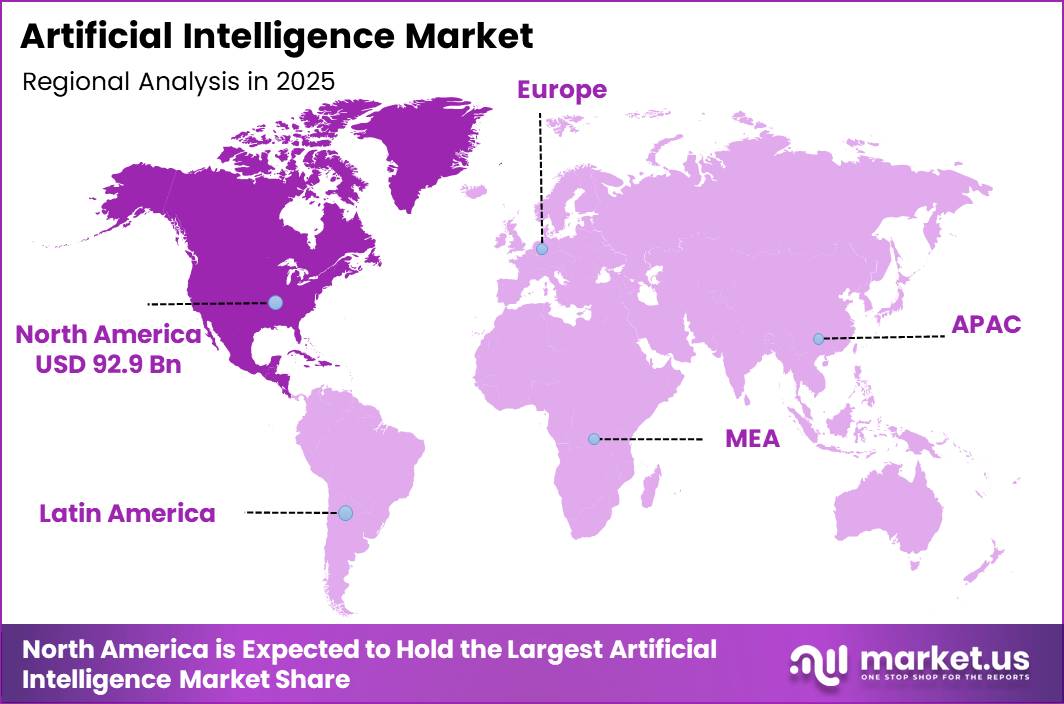

In 2025, the Artificial Intelligence Market was valued at USD 244.3 billion. The market is projected to grow at a CAGR of 30.6% during 2026–2035, reaching approximately USD 3520.9 billion by 2035. North America dominated the global market in 2025, accounting for more than 38.0% of the total market share and generating approximately USD 92.9 billion in revenue.

This expansion is supported by rising AI adoption and investment across major industries, particularly in North America. In 2024, private AI investment in the United States reached USD 109.1 billion, nearly 12 times higher than China’s USD 9.3 billion. This investment is accelerating the development of AI software, cloud platforms, data centres, and computing infrastructure. Global spending on AI infrastructure increased from USD 153 billion in 2024 to USD 318 billion in 2025 and is expected to reach USD 487 billion in 2026.

Emerging economies are also strengthening their AI capabilities. India’s IndiaAI Mission was launched with an allocation of INR 10,372 crore, equivalent to about USD 1.2 billion, while cumulative private AI investment in India reached USD 11.1 billion between 2013 and 2024. With more than 30–40% of businesses worldwide already using AI in at least one function, wider adoption across healthcare, manufacturing, transport, and public services is expected to support long-term market growth.

Key Takeaway

- The Global Artificial Intelligence Market reached USD 244.3 billion in 2025 and is projected to grow at a 30.6% CAGR, reaching USD 3,520.9 billion by 2035.

- Hardware dominated the component segment with a 35% share, driven by rising demand for AI chips, servers, memory, and networking infrastructure.

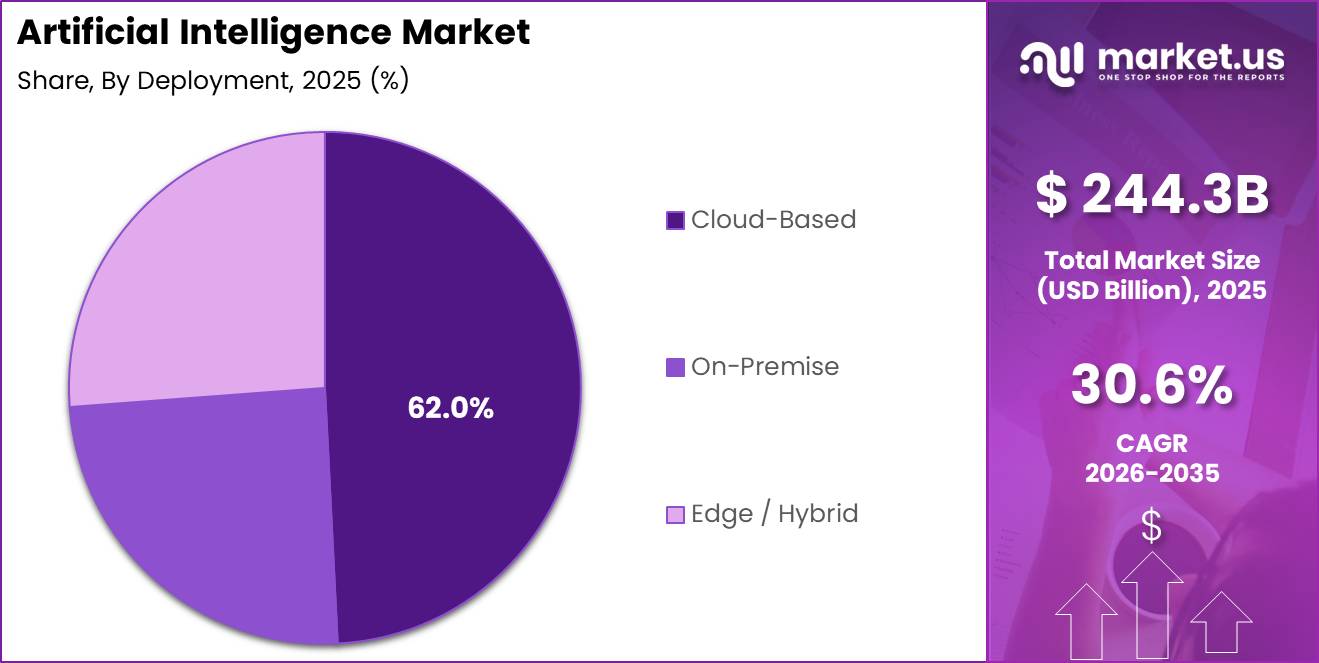

- Cloud-based deployment accounted for a leading 62% share, supported by flexible access to computing power without heavy upfront infrastructure investment.

- Machine Learning held a dominant 38% share, supported by broad adoption across banking, manufacturing, healthcare, retail, and professional services.

- BFSI led the end-user segment with a 20% share, driven by AI use in fraud detection, credit scoring, trading, compliance, and risk management.

- North America led the global AI market in 2025 with a 38.0% share, generating approximately USD 92.9 billion in revenue.

By Component

Hardware held the dominant position in the AI market with a 35% share, supported by the growing need for high-performance chips, servers, memory, and networking equipment. AI models used for language processing, image recognition, and real-time decision-making require advanced computing infrastructure to operate at scale. According to the Semiconductor Industry Association, global semiconductor sales reached USD 627.6 billion in 2024, while logic chip sales, including AI accelerators such as GPUs, increased by 81%.

The U.S. Department of Commerce also committed USD 39 billion in manufacturing incentives under the CHIPS and Science Act, supporting more than USD 450 billion in announced private semiconductor investments across 28 U.S. states by mid-2024. Electronics manufacturing represented 58% of U.S. manufacturing construction, reaching an annualized USD 135 billion in June 2024.

Software is the fastest-growing component because companies can expand AI use through platforms, APIs, machine-learning tools, automation systems, and enterprise applications without repeatedly investing in physical infrastructure. McKinsey’s 2025 survey also showed that most measurable business value came from generative AI, automation, and analytics software. In 2025, AI represented about 61% of global venture capital investment value, supporting continued growth in scalable, subscription-based AI software.

By Deployment

Cloud-based deployment held the dominant position in the AI market with a 62% share, mainly because it allows organizations to access advanced computing power without spending tens of millions of dollars on dedicated GPU infrastructure. Companies can use cloud-based AI resources on demand and pay according to actual usage, making AI adoption more affordable and flexible. Global cloud infrastructure spending reached USD 95.3 billion, increasing by 22% year over year.

AWS, Microsoft Azure, and Google Cloud collectively accounted for 65% of the market. Amazon, Microsoft, Google, and Meta invested a combined USD 248 billion in capital expenditure during 2024, with spending projected to exceed USD 300 billion in 2025, largely supporting AI-focused data centers and cloud infrastructure.

Public cloud AI is expected to remain the fastest-growing sub-segment because it provides ready-to-use models, APIs, development tools, and computing capacity with limited technical investment. Small and medium-sized enterprises, which represent more than 90% of businesses worldwide, can deploy AI applications without maintaining private infrastructure or large IT teams.

By Technology

Machine Learning held the dominant position in the AI technology market with a 38% share, supported by its wide use across banking, manufacturing, healthcare, retail, and professional services. ML enables AI systems to identify patterns, make predictions, classify information, and improve decisions using large datasets. According to the OECD’s 2025 report, firm-level machine learning adoption reached 6.1% in the United States, with strong usage across information technology, finance, and professional services.

In 2024, the World Health Organization also highlighted the use of ML by the Philippine Health Insurance Corporation for insurance fraud detection, claims analysis, and administrative efficiency. WIPO reported that 54,000 generative AI patent families were filed between 2014 and 2023, with more than 25% submitted in 2023 alone. Most of these innovations were based on machine learning and deep learning systems, showing the technology’s central role in AI development.

Natural Language Processing is the fastest-growing technology segment because it enables machines to understand, process, and generate human language. OECD data showed that the share of firms actively using AI increased from 8.7% in 2023 to 14.2% in 2024 and reached 20.2% in 2025. Conversational AI and text analytics remained common starting points for business adoption.

In 2026, WIPO reported that large language models became the largest generative AI patent category in 2025. GenAI inventions doubled from 18,862 in 2024 to 37,808 in 2025, reflecting rising NLP adoption across healthcare, legal services, finance, compliance, and customer support.

By End User

The BFSI sector held the dominant position in the AI market with a 20% share, supported by its high dependence on data, automation, security, and regulatory compliance. Banks, financial institutions, and insurance companies use AI for fraud detection, credit assessment, algorithmic trading, anti-money laundering, customer verification, risk monitoring, document processing, and client services.

The Financial Stability Board reported in 2024 that AI was increasingly used across financial institutions for compliance, trade execution, document summarisation, and internal operations. The sector manages an estimated USD 120 trillion in global assets under management, creating strong demand for AI systems that improve accuracy, reduce costs, and support faster decisions.

Healthcare and life sciences are expected to be the fastest-growing end-user segment as AI adoption expands across medical imaging, diagnostics, patient monitoring, drug development, and administrative work. According to the World Health Organization, global healthcare spending per person increased by more than 60% between 2000 and 2022. The WHO’s expenditure database covers 195 countries, showing the broad scale of healthcare investment.

In January 2025, the U.S. Food and Drug Administration issued draft guidance on using AI in regulatory decision-making for medicines and biological products. By December 2025, it had qualified its first AI-based drug-development tool. OECD data also showed that 82% of member countries offered digital health services in 2024, compared with 79% in 2023.

Key Market Segments

By Component

- Hardware

- AI Chips/GPUs

- Edge AI Devices

- Networking Hardware

- Software

- ML Platforms

- AI Applications

- AI Developer Tools

- Services

- Consulting

- Integration Services

- Managed Services

By Deployment

- Cloud-Based

- Public Cloud AI

- Private Cloud AI

- On-Premise

- Edge / Hybrid

- Edge Devices

- Hybrid Infrastructure

By Technology

- Machine Learning

- Deep Learning

- Supervised Learning

- Reinforcement Learning

- Natural Language Processing

- Large Language Models

- NLU / NLG

- Computer Vision

- Image Recognition

- Video Analytics

- Robotics & Automation

- Other AI Technologies

By End User

- BFSI

- Healthcare & Life Sciences

- Diagnostics AI

- Drug Discovery AI

- Retail & E-commerce

- Manufacturing

- IT & Telecom

- Automotive

- Government & Defense

- Energy & Utilities

- Others

Geopolitical Impact Analysis

Geopolitical tensions are increasing costs and extending delivery times across the AI supply chain, including semiconductor wafers, GPUs, servers, networking equipment, and cloud infrastructure. Shipping disruptions in the Red Sea and Suez Canal have increased average time at sea by around 9%, as vessels are rerouted through the Cape of Good Hope.

UNCTAD simulations indicate that higher freight rates caused by disruptions in the Red Sea and Panama Canal could increase global consumer prices by 0.6% by the end of 2025. These additional costs may directly affect the landed prices of AI servers, data-centre components, and networking systems. +

Meanwhile, continuing trade tensions between the United States and China maintain the risk of 25% tariffs on selected Chinese technology exports, including semiconductor-related products, which could create sudden increases in AI hardware prices.

Energy market uncertainty is adding further pressure. Since early 2024, renewed tensions in the Middle East have added an estimated USD 10–15 per barrel risk premium to oil price scenarios. Higher oil prices increase marine fuel, transport, and electricity costs for energy-intensive industries. This affects semiconductor fabrication plants, where advanced manufacturing can consume several thousand kWh per wafer, as well as hyperscale data centres.

Regional Analysis

North America dominated the global artificial intelligence market with around 38.0% share, generating approximately USD 92.9 billion in revenue. Its leadership is supported by early technology adoption, strong venture capital funding, advanced cloud infrastructure, and the presence of major technology companies. Growing AI use across BFSI, healthcare, retail, and manufacturing continues to support regional demand.

Europe remains an important market due to rising digitalization across industrial, automotive, healthcare, and public-sector activities. Clearer AI regulations are also encouraging companies to adopt secure, transparent, and enterprise-grade AI solutions.

Asia Pacific is expected to be the fastest-growing region, driven by rapid digital transformation, expanding 5G and cloud infrastructure, and government-supported AI programs. Rising internet use, e-commerce growth, and increasing adoption across China, India, Japan, and South Korea are strengthening demand in finance, telecom, manufacturing, and public services.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Market Dynamics

Drivers

| Driver | (~) % CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Generative AI Enterprise Adoption & SaaS Monetization Shift | +4.8% | North America, Western Europe, Southeast Asia | Short term (≤ 2 years) |

| Sovereign AI & National Government AI Investment Programs | +3.5% | India, EU, Middle East, Japan, South Korea | Short term (≤ 2 years) |

| Agentic AI & Multi-Agent Workflow Automation | +3.2% | Global, led by North America | Short term (≤ 2 years) |

| AI Semiconductor Infrastructure Buildout (GPU/HBM Demand) | +2.9% | Global, concentrated in US, Taiwan, South Korea | Short term (≤ 2 years) |

| AI Integration Across Healthcare, Finance & Manufacturing Verticals | +2.4% | Global, high-impact in US, EU, China | Medium term (2–4 years) |

| 5G & Edge Infrastructure Enabling Real-Time AI Inference | +1.8% | Asia Pacific, North America, EU | Medium term (2–4 years) |

Generative AI Enterprise Adoption & SaaS Monetization Shift

The migration from exploratory AI pilots to production-grade, enterprise-wide deployment is the single most powerful current driver compressing time-to-value cycles and permanently restructuring vendor business models. By Q1 2026, 72% of enterprises globally reported at least one AI workload running in production, up from isolated proofs-of-concept that dominated through early 2024, and measured ROI on those deployments reached a 5.8× average return within 14 months of go-live, according to McKinsey survey data.

This performance proof point triggered a decisive shift in monetization architecture: vendors that previously sold perpetual or seat-licensed software are rapidly converting to consumption-based SaaS, embedding AI inference as a billable API layer; in the AI-created SaaS segment alone, the machine learning subsegment commanded a 42.3% share of revenues in 2026 with the public cloud delivery tier capturing 55.8% of that segment.

The upstream commercial impact is equally material: global enterprise AI spending crossed $301 billion in 2026, up from $223 billion in 2025, with AI software alone accounting for roughly $157 billion a concentration ratio that signals platform-layer lock-in effects are already materializing.

Restraints

| Restraint | (~) % CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU AI Act Full Enforcement & High-Risk System Compliance Costs | -2.8% | European Union, EEA, and all non-EU exporters serving EU citizens | Short term (≤ 2 years) |

| Advanced AI Chip Export Controls & Geopolitical Trade Restrictions | -2.3% | China, Middle East, Southeast Asia; supply side in US & Taiwan | Short term (≤ 2 years) |

| Capital Cost & CapEx Intensity of AI Data Center Infrastructure | -1.9% | Global; most acute for mid-tier enterprises and emerging markets | Medium term (2–4 years) |

| Data Privacy Regulation Fragmentation (GDPR, DPDP Act, CCPA, PIPL) | -1.6% | EU, India, US California, China | Medium term (2–4 years) |

| Intellectual Property & AI-Generated Content Legal Uncertainty | -1.1% | Global; most litigated in US, UK, EU | Short term (≤ 2 years) |

EU AI Act Full Enforcement & High-Risk System Compliance Costs

The EU AI Act has created a significant compliance burden that may delay the launch of certain AI products across the European market. Prohibited AI practices became enforceable in February 2025, while obligations for General Purpose AI models started on 2 August 2025.

Penalties for non-compliance are substantial and apply to both EU and non-EU providers serving European customers. Violations involving prohibited practices can result in fines of up to EUR 35 million or 7% of global annual turnover, whichever is higher.

Non-compliance involving high-risk systems can attract penalties of up to EUR 15 million or 3% of global turnover, while transparency violations may lead to fines of up to EUR 7.5 million or 1% of turnover. A company generating EUR 500 million annually could therefore face maximum exposure of EUR 35 million for a serious infringement.

AI vendors must now invest in conformity assessments, third-party audits, technical documentation, incident-reporting systems, post-market surveillance, and machine-readable synthetic-content marking under Article 50. These measures may increase product development costs by an estimated 8%–15% for high-risk applications.

Challenges

| Challenge | (~) % CAGR | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Global AI Talent Supply Deficit | -2.6% | Global; most acute in India, Southeast Asia, LATAM, Africa | Long term (≥ 4 years) |

| AI Hallucination & Model Trust Barrier | -2.1% | Global; critical in healthcare, finance, legal verticals | Medium term (2–4 years) |

| AI Energy & Power Infrastructure Strain | -1.8% | US, EU, India; data center hub geographies | Long term (≥ 4 years) |

| Advanced Node Semiconductor Supply Tightness | -1.5% | Global; sourcing concentrated in Taiwan, South Korea, US | Medium term (2–4 years) |

| Model Bias, Explainability & Governance Debt | -1.2% | Global; regulatory focus in EU, US, UK | Long term (≥ 4 years) |

Global AI Talent Supply Deficit

The shortage of qualified AI professionals remains one of the strongest barriers to market growth, as it slows both product development and enterprise deployment. As of 2026, global AI talent demand exceeded qualified supply by a 3.2:1 ratio, with more than 1.6 million open positions competing for approximately 518,000 qualified candidates.

Rising salaries further increase operating costs for AI companies. Entry-level professionals earn between USD 120,000 and USD 150,000, while mid-level machine learning engineers receive approximately USD 180,000–250,000.

Senior AI specialists can command total compensation of USD 300,000–600,000. These compensation levels are nearly 67% higher than comparable traditional software roles, while AI wages increased by around 38% year over year. Critical skills such as LLM development, MLOps, and AI ethics record demand scores above 85/100, compared with supply scores below 35/100.

Companies are responding through higher compensation, specialized external teams, and long-term employee training programs. However, these measures can reduce operating margins by an estimated 4–7 percentage points compared with conventional software businesses. Government programs are also expanding, including India’s ₹10,300 crore IndiaAI Mission, which supports workforce development and infrastructure through 38,000 deployed GPUs.

Opportunities

| Opportunity | (~) % CAGR | Geographic Relevance | Execution Window |

|---|---|---|---|

| Domain-Specific Small Language Model (SLM) Commercialization | +3.8% | Global; especially strong in EU, India, Japan for regulated verticals | Short term (≤ 2 years) |

| Edge AI Deployment in Industrial IoT & Healthcare | +3.1% | Asia Pacific, North America, EU manufacturing & hospital clusters | Medium term (2–4 years) |

| AI-Native Financial Services & InsurTech Expansion | +2.5% | North America, EU, India, Southeast Asia | Medium term (2–4 years) |

| Sovereign AI Platform & Localized LLM Build-Out | +2.2% | India, Middle East (UAE, Saudi Arabia), ASEAN, Brazil | Medium term (2–4 years) |

| AI Governance, Audit & Compliance-as-a-Service (CaaS) | +1.6% | EU, US, UK, India | Short term (≤ 2 years) |

| Multimodal AI for Retail, Media & Creative Industries | +1.4% | North America, East Asia, EU | Long term (≥ 4 years) |

Domain-Specific Small Language Model (SLM) Commercialization

This opportunity remains largely untapped because AI investment and vendor strategies during 2024–2025 were mainly focused on developing large general-purpose language models. The economic advantage is strong, as running a 7 billion-parameter small language model can cost 10–30 times less per inference than using a 70–175 billion-parameter large language model.

Models such as Phi-3 Mini with 3.8 billion parameters, Llama 3.2 with 3 billion parameters, and Mistral with 7 billion parameters are delivering domain-specific performance comparable to models nearly ten times larger. With improved quantization and fine-tuning techniques, hallucination rates in sub-7 billion-parameter models can be reduced to below 1% for clearly defined tasks.

Small language models also support on-device and on-premises deployment, reducing cloud dependence, data-residency concerns, and per-token API costs. This enables vendors to use subscription or software-licensing models that may improve gross margins by an estimated 15–25 percentage points compared with cloud-inference resale models. Under the EU AI Act, a documented and auditable on-premises model is also easier to assess than a general-purpose model trained using around 10²⁵ FLOPs.

Key Players Analysis

Tier-1 competition in the artificial intelligence market is led by major cloud providers and AI hardware companies. NVIDIA controls around 80–85% of the data-center GPU market and generates more than USD 100 billion annually from its data-center business. Microsoft reported Microsoft Cloud revenue of USD 168 billion in FY2025, up 23%, while Azure revenue reached USD 75 billion, increasing 34%. AI services contributed 13 percentage points to Azure’s 31% growth and expanded 157% year over year in one quarter.

Google Cloud recorded USD 15.1 billion in quarterly revenue, up 35%, with a USD 155 billion backlog. More recent quarterly revenue reached USD 20 billion, rising 63%, while backlog approached USD 460 billion. AWS generated USD 35.6 billion in Q4 2025 sales, up 24%, and USD 12.5 billion in operating income. Together, these Tier-1 companies account for more than 60% of monetized AI infrastructure and platform revenue.

Tier-2 companies compete through specialized software, data platforms, enterprise applications, and regional ecosystems. IBM, SAP, and Salesforce integrate AI into multi-billion-dollar cloud subscription businesses.

Palantir generated approximately USD 4.4 billion in FY2025 revenue, including USD 2.4 billion from government customers, up 53%, and USD 2.0 billion from commercial clients, up 60%. Its U.S. commercial revenue increased 109% to USD 1.5 billion. Baidu reported RMB 20 billion, or nearly USD 2.8 billion, in 2025 AI cloud infrastructure revenue, rising 34%. Intel, Meta, and OpenAI are also expanding their AI positions.

Top Key Players in the Market

- NVIDIA Corporation

- Microsoft Corporation

- Alphabet (Google)

- Amazon Web Services

- IBM Corporation

- Meta AI

- Baidu Inc.

- OpenAI

- Salesforce Inc.

- Intel Corporation

- SAP SE

- Palantir Technologies

Recent Developments

- In June 2026, Salesforce signed a definitive agreement to acquire Fin for approximately USD 3.6 billion. Fin’s agentic AI platform serves more than 30,000 customers and can resolve complex service requests across chat, email, WhatsApp, SMS, phone, and Slack. The acquisition is expected to strengthen Salesforce’s position in AI-powered customer service and expand its Agentforce capabilities.

- In July 2026, SAP completed the acquisition of Dremio to strengthen its enterprise data and agentic AI capabilities. Dremio’s data lakehouse technology enables businesses to process analytical and AI workloads in real time without moving large volumes of data. SAP also issued a EUR 3.5 billion multi-tranche Eurobond to support recent acquisitions and broader AI-related investments.

- In July 2026, Meta projected capital expenditure of USD 115–135 billion for 2026, compared with USD 72.22 billion in 2025. The sharp increase is mainly linked to AI servers, computing infrastructure, and the expansion of Meta Superintelligence Labs. Meta is also developing a gigawatt-scale AI data-center campus in Louisiana through a USD 27 billion joint venture with Blue Owl.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 244.35 Billion |

| Forecast Revenue (2035) | USD 3520.9 Billion |

| CAGR (2026-2035) | 30.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Hardware, Software, Services), By Deployment (Cloud-Based, On-Premise, Edge/Hybrid), By Technology (Machine Learning, Natural Language Processing, Computer Vision, Robotics & Automation, Other AI Technologies), By End User (BFSI, Healthcare & Life Sciences, Retail & E-commerce, Manufacturing, IT & Telecom, Automotive, Government & Defense, Energy & Utilities, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | NVIDIA Corporation, Microsoft Corporation, Alphabet (Google), Amazon Web Services, IBM Corporation, Meta AI, Baidu Inc., OpenAI, Salesforce Inc., Intel Corporation, SAP SE, Palantir Technologies |

| Customization Scope | Customization for segments and region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |

Market")