Quick Navigation

Report Overview

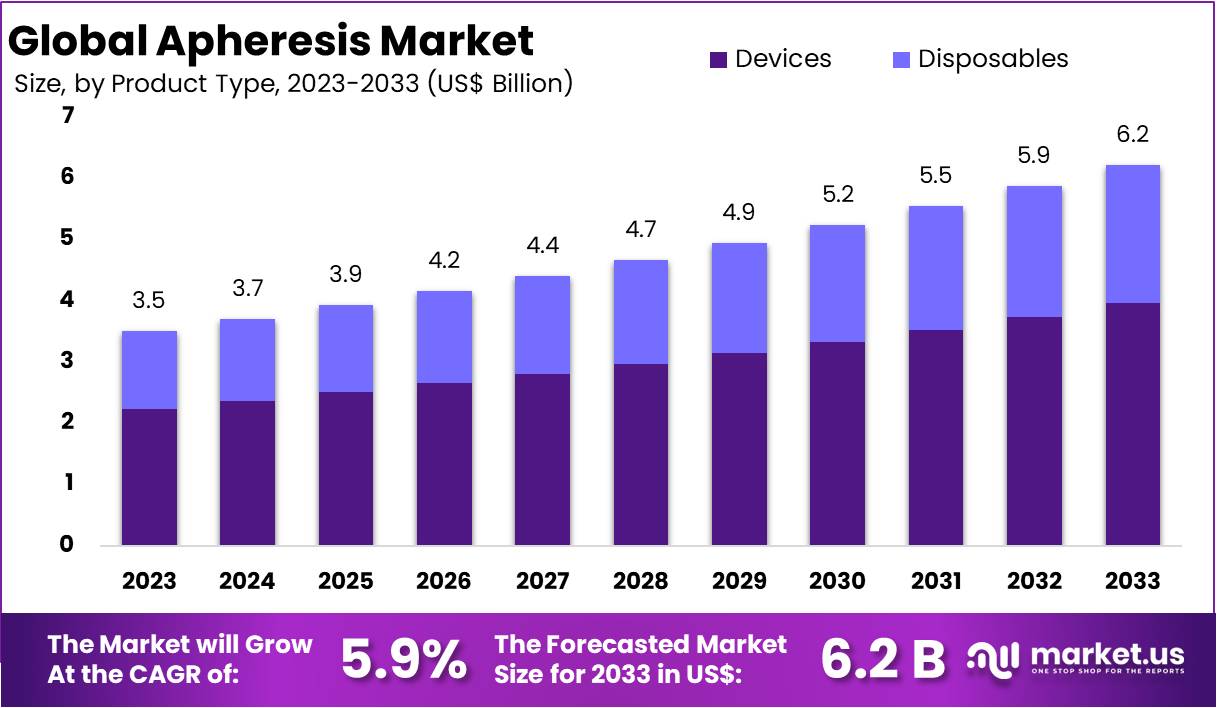

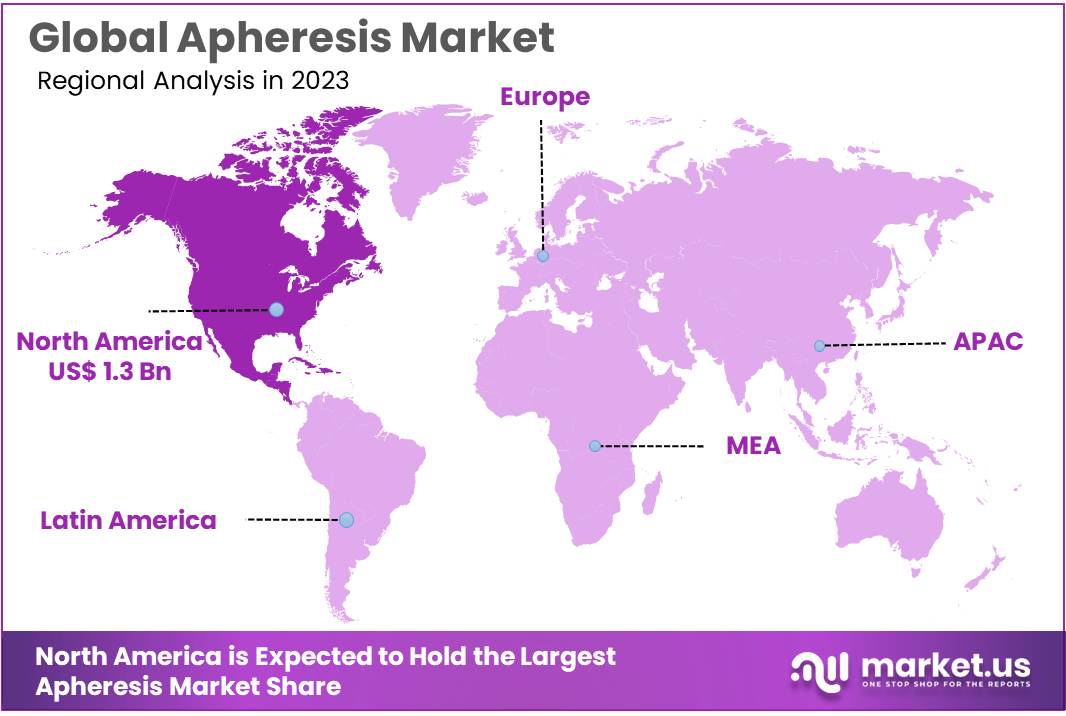

The Global Apheresis Market size is expected to be worth around US$ 6.2 Billion by 2033, from US$ 3.5 Billion in 2023, growing at a CAGR of 5.9% during the forecast period from 2024 to 2033. North America maintained a dominant position in the apheresis market, accounting for over 36.3% of the market share and a market value of US$ 1.3 billion.

Apheresis is a medical procedure that involves the separation and removal of specific components of a patient’s blood, such as plasma, platelets, white blood cells, and red blood cells. This procedure can be used for therapeutic purposes like plasma exchange, leukapheresis, and plateletpheresis. For instance, plasmapheresis is often used in autoimmune diseases like myasthenia gravis, while leukapheresis helps treat conditions like leukemia and lymphoma. Additionally, apheresis plays a crucial role in blood donation, particularly for the collection of plasma and platelets.

The global apheresis market is growing due to increasing demand for blood products and advancements in apheresis technologies. Innovations, such as more efficient and automated systems, are driving this growth. Apheresis devices and consumables are essential for therapeutic applications and blood collection. Additionally, the rising prevalence of blood disorders, autoimmune diseases, and cancer treatments has further fueled the demand for apheresis procedures. This trend is expected to continue in the coming years as more patients require these therapies.

Leukapheresis, a key component of apheresis, is widely used in cancer treatment, particularly in CAR-T (chimeric antigen receptor) cell therapy. This therapy is utilized to treat blood cancers like lymphomas and leukemia. A study by the HeartRhythm Journal indicated that approximately 240,185 leukapheresis procedures are performed annually in the U.S., with a significant rise in the number of procedures from 2016 to 2020. The growing demand for CAR-T therapies is a major driver of this increase, reflecting a broader trend in cancer treatment.

Moreover, apheresis is also used to treat conditions like hypergammaglobulinemia (HGV), which often occurs in patients with Waldenstrom macroglobulinemia (WM). According to a study published on NCBI, more than 30% of all WM patients develop HGV during their illness due to the highly viscous IgM pentamers. Myelomas, particularly IgA and IgG types, are the second leading cause of HGV, accounting for 25% and 5% of cases, respectively. This highlights the growing need for effective apheresis treatments in managing these conditions.

Recent studies have also demonstrated the benefits of apheresis in treating preeclampsia. A research study published in AHA Journals showed that using apheresis systems to deplete sFlt-1, a protein implicated in preeclampsia, prolonged gestation by approximately 15 days compared to 3-5 days in untreated patients. Such findings underline the potential of apheresis in improving patient outcomes across a variety of medical conditions, contributing to the expanding scope of its market applications.

The apheresis market is driven by technological innovations, the rising demand for blood products, and an increasing prevalence of blood disorders and cancers. According to recent studies, the therapeutic applications of apheresis are expanding across diverse medical fields, including cancer treatment and preeclampsia management. The global market for apheresis is expected to continue its growth trajectory, particularly in North America and Europe, where healthcare infrastructure is well developed.

Key Takeaways

- Market Growth: The global apheresis market is projected to reach US$ 6.2 billion by 2033, growing at a CAGR of 5.9% from 2024 to 2033.

- North America Dominance: North America holds over 36.3% of the market share in 2023, valued at US$ 1.3 billion, leading the global market.

- Device Segment: The Devices segment led the market with 63.7% share in 2023, essential for blood component separation and therapeutic apheresis.

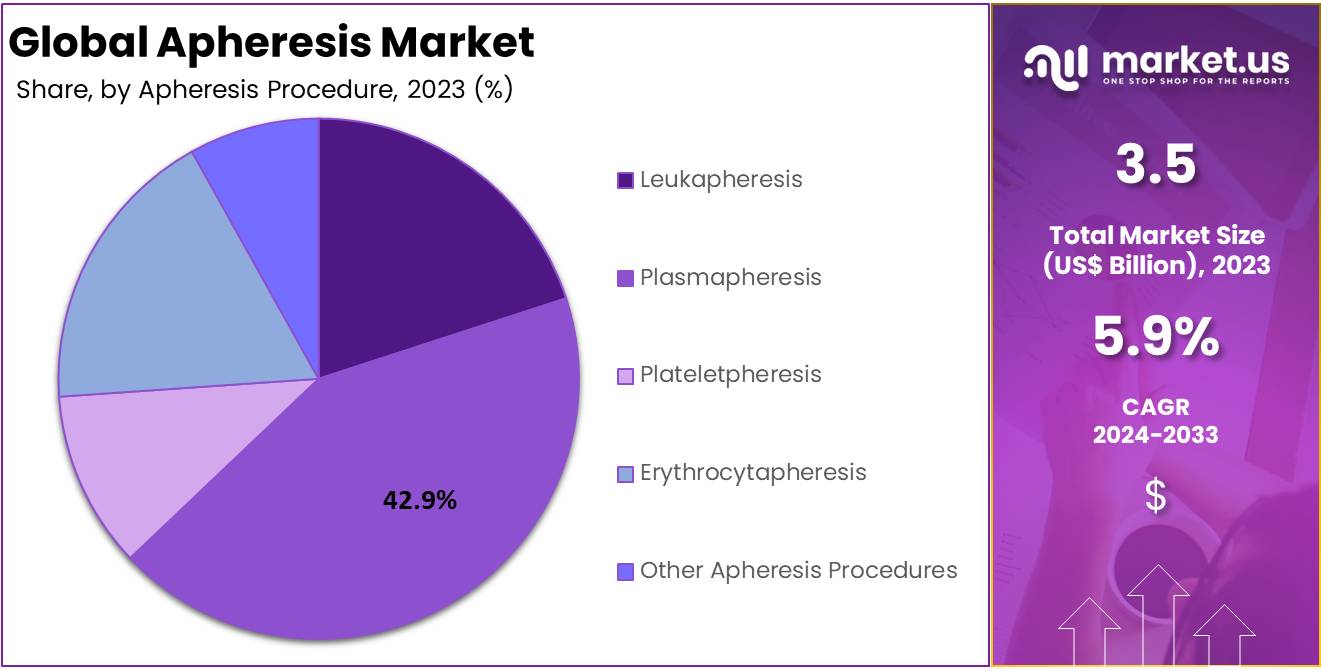

- Plasmapheresis Dominance: Plasmapheresis accounted for 42.9% of the market in 2023, widely used for treating autoimmune and chronic conditions like myasthenia gravis.

- Centrifugation Technology: Centrifugation remains the dominant technology, holding 66.2% of the market in 2023, known for effective blood component separation by density.

- Hematological Disorders: Apheresis for hematological disorders like leukemia and lymphoma captured 35.9% of the market in 2023, crucial for effective patient management.

- Neurological Applications: Apheresis is increasingly used for neurological and autoimmune disorders, such as multiple sclerosis and myasthenia gravis, improving patient outcomes.

- Rising Plasma Demand: The growing demand for source plasma is fueling market growth, driven by increased use of plasma-derived medicinal products.

- High Procedure Costs: High costs and complexity of apheresis limit accessibility, particularly in low-income regions, posing a challenge to market expansion.

- Technological Innovations: Ongoing innovations in apheresis devices, such as automated systems, promise improved efficiency, quicker procedures, and enhanced patient outcomes.

Product Type Analysis

In 2023, the Devices segment held a dominant position in the Product Type Segment of the Apheresis Market, capturing more than a 63.7% share. This segment’s leadership highlights its critical role in blood component separation. Devices are primarily used for therapeutic applications and blood donations, supporting treatments like plasma extraction and stem cell collection.

The demand for these devices stems from technological advancements that have increased the efficiency and safety of apheresis procedures. Hospitals and blood centers, as key users, depend on these devices for essential services such as plasma collection and leukapheresis. This need is fueled by a rise in chronic diseases and the ongoing requirement for blood components in therapy.

Further supporting the segment’s strength are regulatory approvals for innovative apheresis devices. These approvals allow new, advanced machines to enter the market, which are equipped with improved functionalities and offer better patient comfort during procedures. Such innovations ensure the devices meet the highest safety standards.

The future of the Devices segment appears robust, driven by continuous technological evolution and growing healthcare demands. As healthcare providers focus on treatment efficacy and patient safety, this segment is poised to maintain its market leadership. The ongoing development in apheresis technology suggests a trend of sustained growth and innovation.

Procedure Analysis

In 2023, the Plasmapheresis segment held a dominant position in the Procedure Segment of the Apheresis Market, capturing over 42.9% of the market share. This method is predominantly utilized to treat autoimmune disorders and chronic conditions like Guillain-Barre syndrome and myasthenia gravis. It is preferred for its efficiency in removing harmful substances from the plasma, offering quick relief to patients.

Leukapheresis follows closely behind in usage, mainly in oncology and bone marrow transplant scenarios. It is instrumental in selectively extracting white blood cells. This is especially beneficial for patients undergoing chemotherapy or managing leukocyte disorders, aiding their treatment process significantly.

Plateletpheresis and Erythrocytapheresis are smaller segments but equally essential. Plateletpheresis is crucial for gathering platelets for transfusions in patients with severe thrombocytopenia or during significant surgical operations. Erythrocytapheresis plays a key role in treating diseases such as sickle cell disease and polycythemia vera by reducing the risk of thrombosis.

The Other Apheresis Procedures category includes less common but vital techniques like lipid apheresis and stem cell harvesting. These specialized procedures highlight the adaptability and scope of apheresis technology in addressing diverse medical needs. They are critical for specific therapeutic requirements in modern healthcare.

Technology Analysis

In 2023, the centrifugation segment held a dominant market position in the technology segment of the Apheresis market, capturing more than a 66.2% share. This method is preferred for its effective separation of blood components. By spinning blood at high speeds, it segregates components based on density. This efficiency makes it a popular choice in healthcare settings for procedures like plasma and platelet collection.

Centrifugation is renowned for its reliability and rapid processing capabilities. Its widespread use in blood banks and hospitals underscores its importance. The technology supports critical medical treatments, ensuring a steady supply of necessary blood components. Its robust functionality cements its status as a foundational technology in the Apheresis market.

Membrane separation stands as an alternative technology within the Apheresis market. It differentiates itself by using a membrane filter to separate blood components by size, not density. This method is particularly beneficial for patients who undergo frequent treatments. It is known for being less harsh on blood cells compared to centrifugation, thus preserving cell integrity.

Despite its advantages, membrane separation has a smaller market share compared to centrifugation. This is largely due to centrifugation’s established presence and higher adoption rate in clinical environments. However, ongoing advancements in Apheresis technologies continue to improve both efficiency and safety, promising to reshape future market preferences and expand the use of gentler methods like membrane separation.

Application Analysis

In 2023, the Hematological Disorders segment held a dominant market position in the Application Segment of the Apheresis Market, capturing more than a 35.9% share. This segment’s leadership is due to the rising number of blood disorders that require the separation of blood components for treatment. Apheresis is essential in managing conditions like leukemia, lymphoma, and myeloma, where it can be critical for effective patient management.

The application of apheresis in neurological disorders is also noteworthy. It is employed in the treatment of autoimmune conditions that impact the nervous system, such as multiple sclerosis and myasthenia gravis. This method helps remove antibodies and other immune components that exacerbate these conditions. Consequently, apheresis can significantly enhance patient outcomes and overall well-being.

Autoimmune disorders benefit from apheresis too. It is utilized to extract pathogenic autoantibodies, immune complexes, and inflammatory mediators from the blood. This application is crucial for diseases like lupus and rheumatoid arthritis, where standard treatments may fall short. Directly targeting the immune system, apheresis offers a potential route to disease remission.

Apheresis applications extend to renal disorders by treating conditions like Goodpasture’s syndrome and hemolytic uremic syndrome. It removes harmful substances from the blood, protecting the kidneys from further damage. This illustrates apheresis’s critical role in saving lives in urgent care settings. Additionally, it is applied in various cardiovascular and metabolic disorders, demonstrating its broad utility as a therapeutic tool.

Key Market Segments

By Product Type

- Devices

- Disposables

By Apheresis Procedure

- Leukapheresis

- Plasmapheresis

- Plateletpheresis

- Erythrocytapheresis

- Other Apheresis Procedures

By Technology

- Centrifugation

- Membrane Separation

By Application

- Renal Disorders

- Hematological Disorders

- Neurological Disorders

- Autoimmune Disorders

- Other Applications

Drivers

Increasing Prevalence of Chronic Diseases

The prevalence of chronic diseases, such as cardiovascular conditions, diabetes, and neurological disorders, is a significant driver for the apheresis market. These ailments often require therapeutic apheresis, contributing to its heightened demand. For example, in the United States, heart disease and stroke lead to over 944,800 deaths annually, emphasizing the urgent need for effective management of blood components.

Moreover, the increasing incidence of chronic and autoimmune diseases worldwide, including sickle cell anemia, leukemia, and multiple sclerosis, necessitates therapeutic apheresis as part of the treatment regimen. According to studies, this rising healthcare burden supports a robust demand for apheresis services, reflecting the critical role of this technology in treatment protocols.

Additionally, the enhancement in healthcare awareness and accessibility to advanced medical treatments further catalyzes the apheresis market’s growth. For instance, improved healthcare infrastructure allows for more widespread use of these lifesaving procedures, ensuring patients receive the necessary care for managing complex chronic conditions. This trend underscores the growing importance of apheresis in contemporary medical practices.

Restraints

High Cost and Complexity of Procedures

The apheresis market faces significant restraints, primarily due to the high costs involved in the procedures. This factor makes it challenging for individuals in lower-income regions to access these necessary healthcare services. Additionally, the availability of these treatments is heavily dependent on voluntary donors, who provide the required blood components. This dependency can limit the accessibility of apheresis materials, affecting the overall efficacy and reach of the treatments in various regions.

According to a study by the Centers for Disease Control and Prevention, managing the systems associated with apheresis is complex and costly. For instance, the total healthcare expenses for epilepsy in the U.S. amounted to $13.4 billion in 2019, with $5.4 billion directly related to managing the condition itself. These economic burdens can restrict the widespread use and adoption of apheresis, especially in areas with fewer resources.

These economic challenges highlight the need for more affordable and accessible apheresis solutions, particularly for under-served communities. The reliance on voluntary donors further complicates the availability of apheresis, necessitating innovative approaches to enhance donor availability and reduce costs, ensuring broader access to these critical treatments.

Opportunities

Technological Advancements in Apheresis Procedures

Technological innovations in apheresis equipment signify a significant opportunity to enhance procedure safety and efficiency. Automated apheresis machines, for instance, have revolutionized how blood components are separated, offering higher precision and less manual intervention. According to a recent study by ‘RSC PUBLISHING’, automatic centrifugation notably increases the recovery of red blood cells to about 86-89% compared to manual methods, which show about 67-84% recovery.

Furthermore, advancements in operational modes reduce procedure times and minimize complications such as platelet loss. Automatic centrifugation, for example, reduces procedure time by nearly 20%, thus minimizing the risk associated with longer processing times. These technological advancements not only improve the efficiency but also expand the potential uses of apheresis in therapeutic settings and donor management.

With the global apheresis market projected to grow significantly, innovations in apheresis technologies are crucial for scaling up to meet the increasing demand efficiently. These improvements promise not only cost savings but also enhanced patient outcomes due to more reliable and quicker blood component separation.

Trends

Rising Demand for Source Plasma

The apheresis market is witnessing a significant trend with the rising demand for source plasma, fueled by the increasing need for plasma-derived medicinal products. As new therapeutic applications for plasma are identified and commercialized, this trend is poised to boost the market further. According to industry analysts, the expansion in plasma usage underscores a broader shift towards more specialized biomedical solutions, promising sustained growth in this sector.

Studies indicate that the global health consciousness surge is amplifying the demand for source plasma. The apheresis process, critical for extracting this plasma, is becoming increasingly vital as medical science discovers more applications for plasma in treatment regimens. This upward trajectory is expected to continue, supported by advancements in healthcare technologies and a growing awareness of the therapeutic benefits of plasma-derived products.

Economic factors and technological progress also play crucial roles in shaping the apheresis market. The complex interplay between medical needs and economic considerations presents both challenges and opportunities for growth. For instance, the need for efficient apheresis techniques is prompting investments in better technologies, which in turn may lead to more accessible and effective plasma collection methods, thereby benefiting the market at large.

Regional Analysis

In 2023, North America held a dominant market position in the apheresis market, capturing more than a 36.3% share and holding a US$ 1.3 billion market value for the year. This significant market share is largely due to the region’s advanced healthcare infrastructure. North America boasts some of the world’s leading hospitals and medical research facilities, which are fundamental in supporting the extensive use of apheresis procedures in clinical settings.

The high prevalence of chronic diseases like cancer and autoimmune disorders also plays a crucial role in driving the demand for apheresis services in this region. As these conditions require specialized treatment methods, apheresis becomes a key component of therapeutic protocols. This increases the reliance on and demand for apheresis technologies, ensuring steady market growth.

Further bolstering the market are supportive regulations and substantial funding from health authorities and governments in North America. These bodies actively promote the adoption of innovative medical treatments, including apheresis. Additionally, technological advancements spearheaded by leading medical technology firms in the region continuously enhance the effectiveness and scope of apheresis procedures.

Lastly, the awareness and availability of training programs for healthcare providers ensure skilled application of apheresis techniques. Comprehensive insurance coverage and high healthcare expenditure per capita also ensure broad access to these advanced treatments. Together, these elements sustain North America’s leading position in the global apheresis market.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In the Apheresis Market, Fresenius Kabi AG is a prominent figure, renowned for its robust portfolio of apheresis devices. The company is celebrated for maintaining high standards of quality and innovation, significantly enhancing patient care globally. Their devices are pivotal in providing reliable and efficient apheresis solutions, cementing their status in the market.

Terumo BCT Inc. and Haemonetics Corporation are also key contributors. Terumo BCT is noted for its technological advancements in blood component therapies, gaining trust for improving the safety and efficiency of blood collections. Meanwhile, Haemonetics is instrumental with its blood management systems, optimizing procedures in blood centers and hospitals alike.

Asahi Kasei Medical Co. Ltd. plays a crucial role with its advanced apheresis machines, which are essential in therapeutic apheresis and blood component separation. Their commitment to research in membrane technology significantly advances apheresis applications. PlasmaSat Inc., though smaller, is making significant strides with its specialized plasma collection solutions, addressing niche market needs effectively. Other key players drive regional market penetration and adapt to local demands, fueling the global expansion of the apheresis industry.

Market Key Players

- Fresenius Kabi AG

- Terumo BCT Inc.

- Haemonetics Corporation

- Asahi Kasei Medical Co. Ltd.

- PlasmaSat Inc.

- Cerus Corporation

- Cobe BCT (a division of Gambro)

- Baxter International Inc.

- Nihon Kohden Corporation

- Sorin Group (now part of LivaNova)

- Medica S.p.A.

- Other Key Players

Recent Developments

- In November 2024: Terumo Blood and Cell Technologies announced the creation of the Global Therapy Innovations business unit. This unit integrates expertise in therapeutic apheresis and cell and gene therapy to enhance patient care across the treatment journey. By leveraging data from platforms like the Spectra Optia™ Apheresis System, Quantum Flex™ Cell Expansion System, and FINIA™ Fill and Finish System, the company aims to advance standards of care and expand therapeutic possibilities.

- In December 2023: Haemonetics completed the acquisition of OpSens Inc., a cardiology-focused medical device company, for approximately USD $255 million. This strategic move aims to enhance Haemonetics’ hospital portfolio with innovative fiber optic sensor technology, potentially improving patient care in interventional cardiology.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 3.5 Billion |

| Forecast Revenue (2033) | USD 6.2 Billion |

| CAGR (2024-2033) | 5.9% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Devices, Disposables), By Apheresis Procedure (Leukapheresis, Plasmapheresis, Plateletpheresis, Erythrocytapheresis, Other Apheresis Procedures), By Technology (Centrifugation, Membrane Separation), By Application (Renal Disorders, Hematological Disorders, Neurological Disorders, Autoimmune Disorders, Other Applications) |

| Regional Analysis | North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA |

| Competitive Landscape | Fresenius Kabi AG, Terumo BCT Inc., Haemonetics Corporation, Asahi Kasei Medical Co. Ltd., PlasmaSat Inc., Cerus Corporation, Cobe BCT (a division of Gambro), Baxter International Inc., Nihon Kohden Corporation, Sorin Group (now part of LivaNova), Medica S.p.A., Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |