Quick Navigation

- Report Overview

- Key Takeaways

- Drug Class Analysis

- Indication Analysis

- Route of Administration Analysis

- Distribution Channel Analysis

- Drug Type Analysis

- Age Group Analysis

- Key Market Segments

- Driver

- Challenge

- Restraints

- Opportunity

- Geopolitical Impact Analysis

- Regional Analysis

- Key Players Analysis

- Key Development

- Report Scope

Report Overview

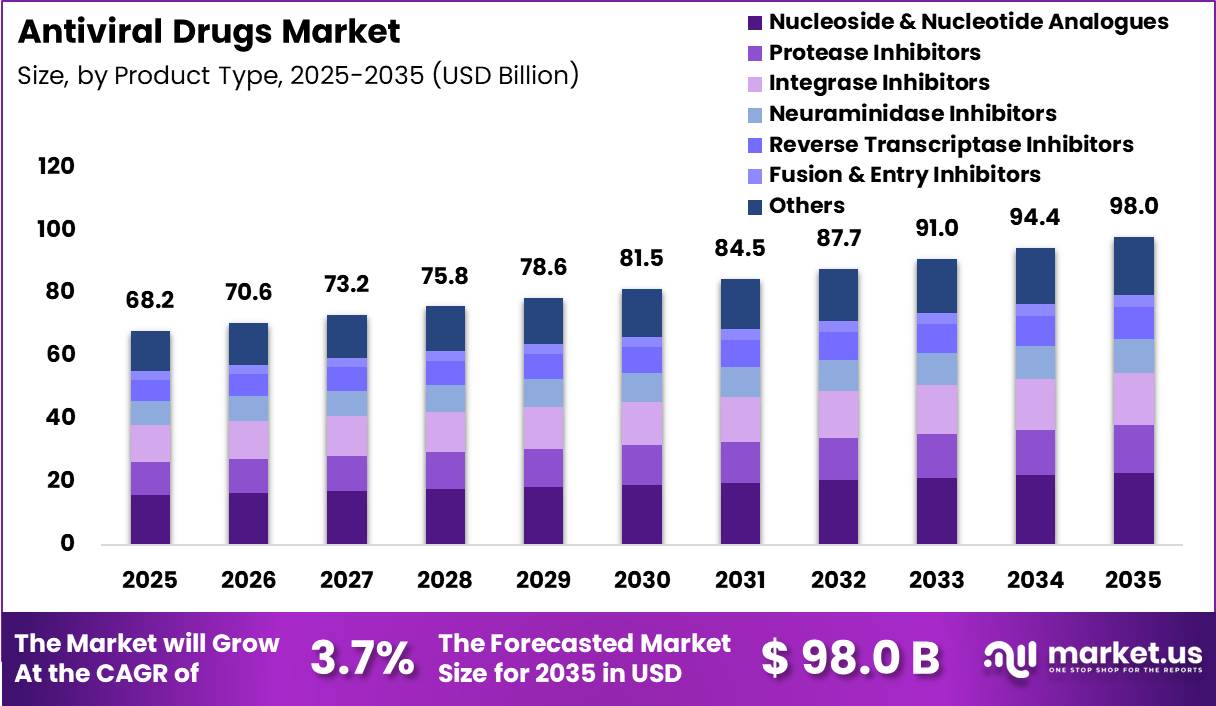

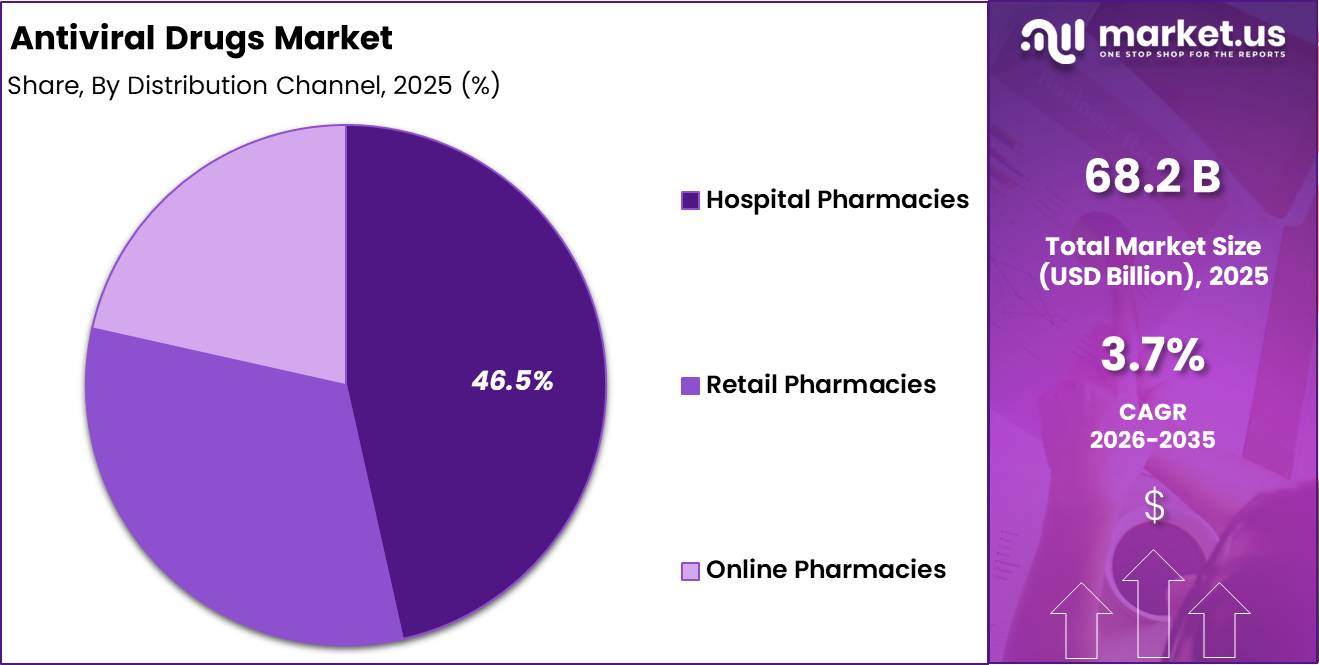

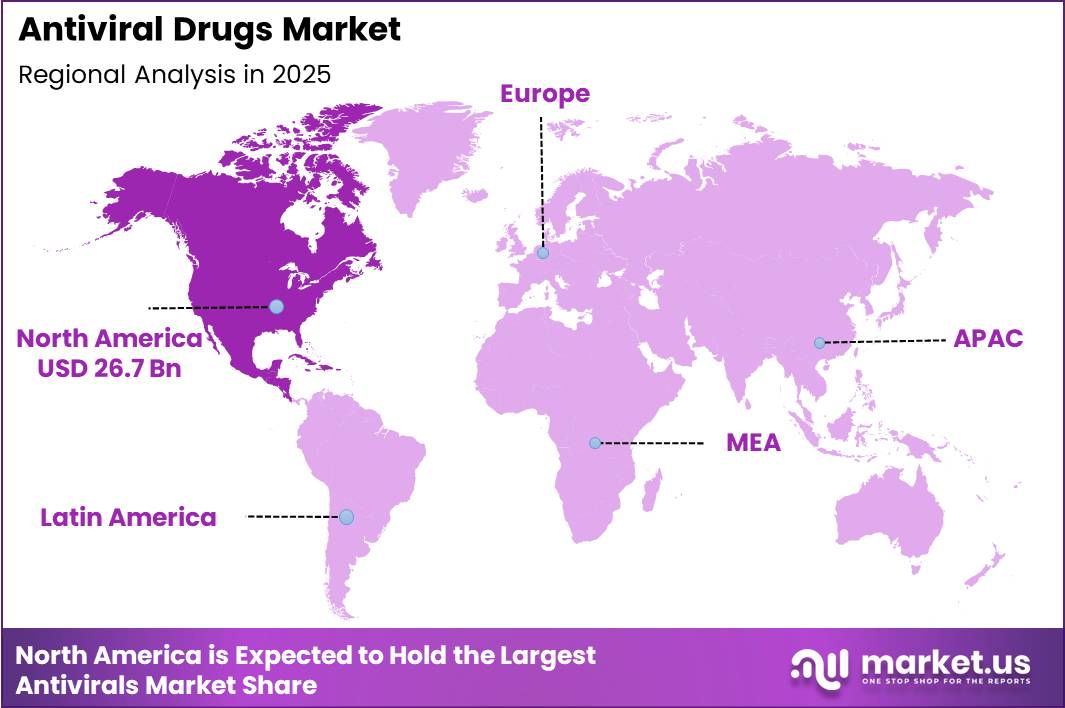

Global Antiviral Drugs Market size is expected to be worth around US$ 98.0 Billion by 2035 from US$ 68.2 Billion in 2025, growing at a CAGR of 3.7% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 39.2% share, holding US$ 26.72 Billion in revenue.

This market growth is primarily driven by the rising global burden of viral diseases that require long-term or recurring antiviral treatment. According to the World Health Organization (WHO), around 40.8 million people were living with HIV in 2024, with 31.6 million receiving antiretroviral therapy (ART). HIV patients require lifelong treatment, making ART one of the largest and most stable sources of demand for antiviral drugs.

The WHO Global Hepatitis Report 2024 also states that 254 million people are living with chronic hepatitis B, while only 10 million are receiving antiviral treatment, highlighting a significant treatment gap. In addition, hepatitis B and C cause around 1.3 million deaths annually. Seasonal influenza further strengthens demand, with nearly 1 billion infections, 3–5 million severe cases, and 290,000–650,000 respiratory deaths reported each year. These disease burdens continue to support demand for antiretrovirals, hepatitis therapies, and influenza antiviral drugs.

North America accounted for 39.2% of the global market, generating US$ 26.72 billion in 2025, supported by high healthcare spending and strong access to antiviral therapies. According to the U.S. National Institutes of Health (NIH), U.S. prescription drug spending reached US$576.9 billion in 2021, increasing by 7.7% year over year.

UNAIDS reports that the number of people receiving ART increased from 7.7 million in 2010 to 32.1 million by the end of 2025, reflecting a more than fourfold increase in antiviral drug use. The WHO also estimates that 846 million people aged 15–49 are living with genital herpes (HSV-1 or HSV-2), with around 42 million new infections each year, creating recurring demand for antiviral prescriptions.

In addition, approximately 33 million RSV-associated acute lower respiratory illness episodes occur annually in children under five, supporting the adoption of new antiviral and preventive therapies. These factors continue to provide a strong foundation for long-term market growth.

Key Takeaways

- Market Size: The global Antiviral drugs market was valued at US$ 68.2 billion in 2025.

- Market Share: The market is projected to grow at a CAGR of 3.7% and is estimated to reach US$ 98 billion by 2035.

- Drug Class Analysis: On the basis of drug class, Nucleoside & Nucleotide Analogues dominated the global antiviral drugs market, constituting 23.4% of the total market share.

- Indication Analysis: Human Immunodeficiency Virus (HIV) held the largest market share, accounting for 35.4% of the global antiviral drugs market.

- Route of Administration Analysis: The oral segment dominated the market, representing 72.3% of the total market share.

- Distribution Channel Analysis: hospital pharmacies led the market, contributing 46.5% of the overall market revenue.

- Drug Type Analysis: Branded drugs dominated the antiviral drugs market, accounting for 62.3% of the total market share.

- Age Group Analysis: The adult segment held the largest share, representing 71.2% of the global antiviral drugs market.

- Regional Analysis: In 2025, North America emerged as the dominant regional market, accounting for 39.2% of the global antiviral drugs market revenue.

Drug Class Analysis

Nucleoside and Nucleotide Analogues Antivirals drug class represents dominant Segment in the Market.

Nucleoside and nucleotide analogues (NAs) held a dominant 23.4% share of the global antiviral drugs market in 2025, mainly because they are the foundation of treatment for HIV, hepatitis B (HBV), and hepatitis C (HCV). These drugs work by blocking viral DNA or RNA replication through inhibition of viral polymerases and reverse transcriptases.

According to the WHO, the globally recommended first-line HIV regimen, TLD (Tenofovir + Lamivudine + Dolutegravir), includes two nucleoside/nucleotide analogues, tenofovir and lamivudine, and has become the standard treatment across many low- and middle-income countries. For chronic hepatitis B, WHO recommends tenofovir disoproxil fumarate (TDF) and entecavir as first-line therapies, with tenofovir achieving viral suppression in more than 90% of treatment-adherent patients after 3 years.

In hepatitis C treatment, around 12.7 million patients received nucleotide-based direct-acting antivirals such as sofosbuvir between 2014 and 2023, curing approximately 21% of global HCV infections. By mid-2023, 145 countries, representing 91% of all countries worldwide, had approved at least one sofosbuvir-based therapy. Their broad use across these major viral diseases continues to support the leading position of nucleoside and nucleotide analogues.

Integrase inhibitors are projected to register the fastest growth during the forecast period due to the rapid global adoption of dolutegravir (DTG)-based HIV treatment. The WHO recommends DTG-based regimens as both first-line and second-line therapy for all patient groups, including pregnant women, because of their higher effectiveness and lower risk of drug resistance.

Program data from low- and middle-income countries show that more than 95% of adults receiving DTG-based treatment achieve viral suppression within 6 to 24 months. In comparison, viral suppression reached only 61% among patients treated with efavirenz, while DTG-based regimens achieved 81% in comparable settings.

By the end of 2018, about 3.9 million patients across 61 developing countries had already switched to generic dolutegravir treatment, and the transition continues across many additional countries. Integrase inhibitors also offer a higher genetic barrier to resistance, making them more reliable in regions with limited viral load monitoring. The continued expansion of TLD programs across Africa, Asia, and Latin America is expected to drive sustained demand for integrase inhibitors through 2035.

Indication Analysis

HIV Retains the Largest Share in the Global Antiviral Drugs Market.

HIV accounted for 35.4% of the global antiviral drugs market in 2025, driven by the lifelong need for antiretroviral therapy (ART). Unlike many viral diseases, HIV has no cure, requiring every diagnosed patient to remain on daily antiviral treatment for life. This creates stable and recurring demand for antiviral drugs.

According to The Global Fund, it invested US$27.6 billion in HIV programs between 2002 and June 2025, while 25.6 million people received ART across supported countries in 2024. In addition, the United States has contributed US$28.76 billion to The Global Fund through PEPFAR, highlighting the strong institutional support for HIV treatment worldwide.

Despite progress, 1.3 million new HIV infections were reported in 2024, continuously expanding the treatment population. Furthermore, only 55% of the 1.4 million children living with HIV are receiving treatment, indicating significant unmet demand. As every newly diagnosed patient requires lifelong antiviral therapy, continued funding and treatment expansion are expected to sustain strong market demand.

Hepatitis B is expected to witness the fastest growth in the antiviral drugs market due to its large untreated patient population. According to the WHO, around 240 million people were living with chronic hepatitis B in 2024, but only 10 million, or 4.3%, were receiving antiviral treatment, leaving a treatment gap of 95.7%.

The WHO’s updated 2024 hepatitis B treatment guidelines have expanded patient eligibility, allowing millions of additional patients to qualify for therapy. At the same time, only 65 million people, or 27% of those infected, are aware of their hepatitis B status, creating substantial opportunities through expanded screening programs.

Hepatitis B causes approximately 1.1 million deaths each year, mainly from liver cirrhosis and liver cancer. The WHO Western Pacific and African regions account for 102 million and 64 million chronic hepatitis B cases, respectively. Increasing diagnosis, broader treatment access, and government-led disease control programs are expected to drive strong growth in hepatitis B antiviral demand through 2035.

Route of Administration Analysis

Oral Administration Leads Through Convenience and High Patient Compliance.

Oral administration dominated the antiviral drugs market in 2025, accounting for 72.3% of total revenue, mainly because it is the preferred treatment method for chronic viral diseases such as HIV and hepatitis. Once-daily oral tablets allow patients to receive long-term treatment at home, reducing the need for hospital visits.

The WHO recommends 3 to 6 months of multi-month dispensing (MMD) for stable HIV patients, enabling medicines to be supplied through pharmacies, community health centers, or home delivery. A clinical trial published in The Lancet found that 6-month oral ART dispensing was as effective as standard care while improving patient retention by 9.1% points.

In addition, studies from the NIH show that single-tablet oral regimens increase the likelihood of achieving 95% or higher treatment adherence by 63% compared with multi-pill therapies. For hepatitis C, oral direct-acting antivirals (DAAs) deliver real-world adherence rates of 84.8%, while patients maintaining more than 50% adherence achieve a 99% sustained virologic response. High patient compliance, strong clinical outcomes, and convenient home-based treatment continue to strengthen the leadership of oral antiviral formulations.

The injectable segment is projected to record the fastest growth during the forecast period, supported by increasing adoption of long-acting injectable (LAI) therapies for HIV. According to the WHO, nearly 24% of HIV patients experience poor adherence to daily oral medicines, creating strong demand for monthly and bi-monthly injectable options.

Clinical Phase III studies have shown that long-acting cabotegravir + rilpivirine injections provide virological outcomes that are non-inferior to daily oral therapy. Demand is also increasing for injectable antivirals used in hospitals to treat severe RSV, CMV, and drug-resistant influenza infections, supporting continued growth of the injectable segment through 2035.

Distribution Channel Analysis

Hospital Pharmacies Held a Major Share of the Antiviral Drugs Market.

Hospital pharmacies accounted for the largest 46.5% share of the global antiviral drugs market in 2025, driven by their central role in dispensing high-value antiviral therapies that require specialist supervision. Treatments for cytomegalovirus (CMV), severe influenza, respiratory syncytial virus (RSV), and post-transplant infections are mainly administered in hospitals because they require IV infusion, continuous patient monitoring, and expert clinical care. Demand is increasing alongside the growth in organ transplantation.

According to the Global Observatory on Donation and Transplantation (GODT), a record 173,727 solid organ transplants were performed worldwide in 2024, representing a 2% year-on-year increase. Every transplant patient requires antiviral prophylaxis, such as valganciclovir or letermovir, for at least 3 to 6 months after surgery.

In addition, the U.S. Centers for Medicare & Medicaid Services (CMS) reported that U.S. hospital care spending reached US$1.6 trillion in 2024, accounting for nearly one-third of total national healthcare spending, while hospitals contributed 40% of healthcare spending growth between 2022 and 2024. The OECD Health at a Glance 2023 also shows that hospital pharmaceutical spending is typically 20% or more higher than retail pharmaceutical spending, supporting the strong position of hospital pharmacies in antiviral drug distribution.

The online pharmacy segment is projected to register the fastest growth during the forecast period, supported by the rapid expansion of digital healthcare services after the COVID-19 pandemic. Governments across developed and emerging economies have expanded e-prescription systems and digital pharmacy regulations to improve medicine access.

According to the World Health Organization (WHO), digital health services play an important role in improving access to medicines and long-term treatment adherence. Patients with stable HIV, hepatitis B, and herpes who no longer require hospital monitoring increasingly prefer online pharmacies for convenient and cost-effective antiviral refills.

Rising internet access, smartphone adoption, and digital healthcare infrastructure across Asia, Latin America, and Africa are expected to further accelerate the growth of online antiviral drug distribution through 2035.

Drug Type Analysis

Branded drugs dominated the global antiviral drugs market, accounting for 62.3% of the market share in 2025. This leadership is supported by strong investments in research, clinical trials, and the development of innovative antiviral therapies for diseases with limited or no cure.

According to the International Federation of Pharmaceutical Manufacturers & Associations (IFPMA), the pharmaceutical industry’s R&D activities contributed US$ 227 billion to global GDP in 2022, representing 30% of the sector’s direct economic contribution. In 2024, PhRMA member companies invested US$ 104 billion in R&D. The U.S. Congressional Budget Office (CBO) estimates that developing a new drug costs between US$ 0.8 billion and US$2.3 billion, supporting premium pricing and patent protection for branded medicines.

These advantages are especially important for advanced therapies such as long-acting HIV injectables, next-generation hepatitis B treatments, and new RSV prevention drugs, where generic alternatives are still unavailable. According to IFPMA, more than 12,900 medicines were in clinical development globally in 2025, with antiviral therapies representing a significant share of the pipeline, supporting continued growth of the branded segment.

The generic antiviral drugs segment is expected to record the fastest growth during the forecast period due to expanding access to affordable medicines. The Medicines Patent Pool (MPP), supported by UNITAID, has signed voluntary licensing agreements covering 13 HIV antiretroviral medicines and multiple hepatitis C therapies, allowing generic manufacturers to supply these products across 105+ low- and middle-income countries.

In May 2026, MPP and Roche signed a new agreement to expand generic access to influenza antivirals in these markets. As governments and public health programs continue to increase treatment coverage for HIV, hepatitis B, and hepatitis C across Asia, Africa, and Latin America, demand for lower-cost generic antiviral medicines is expected to rise steadily through 2035.

Age Group Analysis

Market Demand Was Primarily Driven by the Large Adult Patient Population.

Adults accounted for 71.2% of the global antiviral drugs market in 2025, driven by the high prevalence of chronic viral diseases among the adult population. HIV, hepatitis B, hepatitis C, and genital herpes mainly affect people aged 15–49 years, creating sustained demand for long-term antiviral therapy.

According to UNAIDS, 39.4 million of the 40.8 million people living with HIV globally in 2024 were adults aged 15 years and older, while only 1.4 million were children under 14, meaning about 97% of HIV patients requiring lifelong antiretroviral therapy (ART) are adults.

The WHO recommends direct-acting antiviral (DAA) therapy for all adults aged 18 years and older with hepatitis C, while the U.S. CDC reports the highest infection rates in the 30–39-year age group. The WHO also estimates that 50 million people are living with chronic hepatitis C worldwide, with a large share being adults of working age.

In addition, US$18.7 billion was invested in AIDS response programs in low- and middle-income countries at the end of 2024, with most funding directed toward adult treatment. The high burden of chronic viral diseases, lifelong treatment requirements, and continued global healthcare funding firmly establish adults as the largest consumers of antiviral drugs.

The geriatric segment is projected to register the fastest growth due to rapid population aging and higher vulnerability to viral infections. According to the WHO, the global population aged 60 years and older will increase from 1 billion in 2020 to 1.4 billion by 2030 and 2.1 billion by 2050, while the population aged 80+ will reach 426 million.

UNFPA reports that people aged 65 years and older represented 10.3% of the global population in 2024, up from 5.5% in 1974, and this share is expected to reach 20.7% by 2074. Older adults are more susceptible to viral reactivation, particularly herpes zoster (shingles).

According to a study published in Eurosurveillance, the lifetime risk of shingles reaches 42% by age 85, and incidence rates are three times higher among people aged 65 years and older than in younger adults. Each episode typically requires antiviral drugs such as acyclovir or valacyclovir. As elderly populations continue to grow across Asia, Latin America, and Africa, demand for antiviral therapies in the geriatric population is expected to increase steadily through 2035.

Key Market Segments

Drug Class

- Nucleoside & Nucleotide Analogues

- Protease Inhibitors

- Integrase Inhibitors

- Neuraminidase Inhibitors

- Reverse Transcriptase Inhibitors

- Fusion & Entry Inhibitors

- Polymerase Inhibitors

- Others

Indication

- Human Immunodeficiency Virus (HIV)

- Hepatitis B

- Hepatitis C

- Influenza

- Herpes Simplex Virus (HSV)

- Cytomegalovirus (CMV)

- Respiratory Syncytial Virus (RSV)

- COVID-19

- Others

Route of Administration

- Oral

- Injectable

- Topical

- Inhalation

Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

Drug Type

- Branded Drugs

- Generic Drugs

Age Group

- Pediatric

- Adult

- Geriatric

Driver

HIV ART Scale-Up and Lifecycle Optimization as a Structural Growth Driver

HIV remains the largest and most resilient antiviral revenue pool due to its uniquely large treated population and the need for lifelong, continuously optimized therapy rather than episodic care. According to the World Health Organization, an estimated 40.8 million people were living with HIV at the end of 2024, with 31.6 million already receiving antiretroviral therapy and 73% achieving viral suppression.

A further 5.2 million people remain undiagnosed or not yet linked to treatment, creating a built-in volume runway even before any shift toward premium regimens is considered.As incidence has declined by roughly 40% versus 2010, market growth is now driven less by new infections and more by regimen optimization across an expanding, stable patient base. WHO’s 2026 guidance reinforces the transition toward better tolerated, lower pill-burden, and more durable regimens, supporting both large public-sector tenders in Africa and Asia and higher-value branded uptake in the U.S., EU, and Japan, where adherence and long-term cost containment are critical.

Overall, this dynamic expands the recurring treatment pool, lengthens lifetime therapy duration, and enables value-accretive switching from legacy oral combinations to optimized and long-acting formats, structurally supporting sustained CAGR in the global antiviral market.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| HIV ART scale-up and lifecycle optimization | +2.2% | North America core, Sub-Saharan Africa, EU5, India, South Africa, Latin America urban systems | Medium term (2-4 years) |

| Hepatitis B/C elimination funding and treatment expansion | +1.9% | China, India, Southeast Asia, Africa, Middle East, U.S. high-burden cohorts | Medium term (2-4 years) |

| Respiratory antiviral preparedness and stockpile renewal | +1.4% | U.S., Japan, EU, South Korea, Australia, selected Gulf states | Short term (≤ 2 years) |

| Long-acting and simplified regimen adoption | +1.6% | U.S., Western Europe, Japan, urban APAC specialty centers | Medium term (2-4 years) |

| Resistance surveillance driving regimen switches | +1.1% | Global HIV programs, Africa, Asia-Pacific, tertiary care markets in U.S./EU | Short term (≤ 2 years) |

| Testing expansion converting undiagnosed burden to treated demand | +1.7% | Africa, Western Pacific, India, Indonesia, U.S. screening-linked systems | Long term (≥ 4 years) |

Challenge

Clinical Development Cycle Complexity in Antivirals

Antiviral development is structurally more complex and time-intensive than many chronic-care therapies due to the interaction of epidemiology, evolving regulatory expectations, and demanding trial logistics. For novel agents targeting emerging or pandemic-prone pathogens, Phase II–III programs often require multi-country enrollment, event-driven endpoints, and adaptive designs, extending total development timelines to roughly 8–10 years from discovery to approval.

Late-stage program costs commonly reach USD 400–800 million per asset, reflecting the need for large safety databases, resistance monitoring, and special-population studies.Additional delays arise from variable disease incidence that complicates trial powering, as well as changing regulatory guidance on endpoints, real-world evidence, and post-marketing commitments, which can add 12–24 months after initial authorization.

Sponsors must also invest in compliant digital and data-management infrastructure, increasing per-trial costs by an estimated 15–25%.While platform trials, shared control arms, and AI-assisted design are being used to improve efficiency, regulatory heterogeneity and risk aversion around infectious-disease endpoints are likely to keep antiviral development cycles elevated into the early 2030s. This prolonged, capital-intensive process raises hurdle rates and limits new market entries, reducing potential market CAGR by approximately 1.0 % point.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Fragile API sourcing networks | -1.4% | North America, EU, APAC hubs | Medium term (2–4 years) |

| Escalating antiviral resistance risk | -1.1% | Global, high-burden infection belts | Long term (≥ 4 years) |

| Clinical development cycle complexity | -1.0% | US, EU, Japan, major EMs | Long term (≥ 4 years) |

| Cold-chain and last-mile logistics strain | -0.8% | Emerging markets, rural corridors | Medium term (2–4 years) |

| Skilled antiviral R&D talent gap | -0.7% | North America core, EU research hubs | Long term (≥ 4 years) |

| Data, surveillance, and stewardship fragmentation | -0.6% | Global, LMIC health systems | Medium term (2–4 years) |

Restraints

Antiviral Resistance and Suboptimal Stewardship as a Structural Restraint

Evolving resistance patterns and uneven stewardship practices represent a growing structural drag on antiviral market growth, even though headline resistance rates for many front-line agents remain low. The World Health Organization has consistently warned that all current antiretrovirals are vulnerable to partial or complete loss of activity as resistant strains emerge. Similarly, Centers for Disease Control and Prevention surveillance shows that resistance to newer influenza antivirals typically remains below 2% in most seasons, yet modeling suggests a 26–34 % risk of widespread resistant transmission if use is not tightly managed.

From a health-system perspective, aggressive deployment of a single antiviral mechanism can substantially reduce morbidity and mortality, but it also increases the probability of resistance emergence. As a result, clinical guidelines increasingly restrict use to defined high-risk cohorts or recommend combination strategies, raising treatment costs while limiting volume.

For manufacturers, this shifts utilization away from broad population coverage toward narrower indications, shrinking addressable patient pools by an estimated 20–30% versus naive epidemiological assumptions and shortening effective commercial lifecycles as real-world resistance data accumulate 5–7 years post-launch.

In parallel, surveillance, resistance testing, and stewardship requirements add 5–10% to infectious-disease service costs, constraining payer budgets and reinforcing reliance on older generics. Collectively, tighter stewardship, smaller eligible populations, and eventual efficacy erosion reduce global antiviral market CAGR by roughly 1 % point compared with a stable-susceptibility scenario.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic API & fill-finish shortages | -2.2% | US, EU, India, global | Short–Medium |

| Heightened regulatory scrutiny & safety risk | -1.6% | US, EU, Japan | Medium |

| Cost inflation in complex biologic antivirals | -1.4% | US, EU, APAC | Short–Medium |

| Antiviral resistance & suboptimal stewardship | -1.1% | Global, LMIC focus | Medium–Long |

| Geopolitical & trade exposure in pharma supply chains | -0.9% | US, EU, APAC corridors | Medium–Long |

| Payer pressure and access controls | -0.8% | US, EU, selected EM | Short–Medium |

Opportunity

Expansion into Underserved Hepatitis C and B Care as a White Space Growth Opportunity

Expansion into underserved hepatitis C and B care pathways represents a major white space opportunity, as global treatment access remains far below epidemiological need despite highly effective therapies. The World Health Organization estimates that around 47 million people were living with chronic hepatitis C in 2024, alongside tens of millions with chronic hepatitis B, yet annual treatment volumes capture only a small share of this population.

Even modest progress bringing 30 to 40 % of currently untreated patients into care by 2035 would unlock an addressable opportunity exceeding USD 15 to 20 billion across antivirals and associated services.The commercial upside is concentrated in Africa, South East Asia, and Eastern Mediterranean middle income markets, where tiered or generic pricing can position DAA courses at USD 80 to 200 while maintaining sustainable margins due to low manufacturing costs and scale efficiencies.

Strategic partnerships with governments and global health agencies to deploy simplified screening algorithms and one stop hepatitis care models can reduce patient drop off by 30 to 40 % and lower pathway costs by 15 to 25 %, creating more predictable demand for DAAs and nucleos t ide analogues.

Because baseline market forecasts largely reflect mature, high income settings, aggressive expansion into underserved populations supported by pooled procurement and outcome based financing could add roughly 1.8 % points to antiviral market CAGR over the medium term, while also reducing long run liver disease burden and enabling adjacent revenues in monitoring, adherence, and digital health tools.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Subscription-based antiviral access models | +2.0% | North America, EU, urban APAC | Short term (≤ 2 years) |

| Integrated antiviral–diagnostics platforms | +2.3% | EU, APAC emerging, Latin America | Medium term (2-4 years) |

| Expansion into underserved hepatitis C and B care | +1.8% | Africa, South-East Asia, EM Eastern Mediterranean | Medium term (2-4 years) |

| Digital adherence and resistance management suites | +1.5% | North America core, EU, high-income APAC | Short term (≤ 2 years) |

| Pandemic-ready broad-spectrum antiviral portfolios | +2.8% | Global, with focus on G20 | Long term (≥ 4 years) |

| Value-based contracting for high-cost antivirals | +1.7% | North America, EU, select LATAM | Medium term (2-4 years) |

Geopolitical Impact Analysis

Trade Policy Shifts and Supply Chain Localization Are Influencing Global Antiviral Drugs Market Dynamics.

The global antiviral drugs market is facing increasing pressure from two major geopolitical challenges: new pharmaceutical tariffs and continued disruption of the Red Sea shipping route. Under a U.S. Executive Order issued on April 2, 2026 under Section 232 of the Trade Expansion Act, patented pharmaceutical products and their active pharmaceutical ingredients (APIs) will face a 100% ad valorem tariff from July 31, 2026 for large manufacturers.

A temporary 20% onshoring tariff will gradually rise to 100% by April 2, 2030. This policy is significant because about 53% of patented pharmaceutical products sold in the U.S. are manufactured outside the country. According to the Atlantic Council, China supplied 39.9% of U.S. pharmaceutical imports by volume in 2024 and remains a major supplier of key starting materials (KSMs) used to produce antiviral APIs.

India, the world’s second-largest API producer and a leading manufacturer of generic antivirals such as tenofovir, lamivudine, and sofosbuvir, is also subject to a 20% U.S. tariff on antiviral API exports. India imports about Rs 377 billion (US$4.5 billion) worth of APIs and bulk drugs each year, with nearly 70% sourced from China.

This creates a double cost burden, as higher-priced Chinese raw materials increase manufacturing costs in India, while export tariffs further raise prices in the U.S. market. According to The Lancet, these trade measures are expected to reduce the affordability and accessibility of antiviral medicines, particularly in price-sensitive markets.

The antiviral supply chain is also being affected by continued disruption in the Red Sea-Bab el-Mandeb shipping corridor. According to UNCTAD, container traffic through the Suez Canal declined sharply following attacks on commercial vessels. The International Transport Forum (ITF/OECD) reported that Far East-Europe container freight rates increased by 220% between December 2023 and early 2024.

The U.S. Energy Information Administration (EIA) estimates that rerouting ships around the Cape of Good Hope adds approximately 10–15 days to each voyage. By April 2026, Suez Canal traffic remained 70–90% below historical levels, while Asia-to-U.S. East Coast transit times were 8–12 days longer and freight costs remained 15–25% above pre-crisis levels. These disruptions have increased the landed cost of APIs, intermediates, and finished antiviral drugs shipped from India and China to Europe and North America.

Industry supply chain analysis also indicates that nearly 20% of Europe’s pharmaceutical shipments were delayed in early 2025, increasing the risk of supply shortages for chronic antiviral therapies such as antiretroviral therapy (ART), where treatment interruptions can reduce patient adherence and contribute to antiviral drug resistance.

Regional Analysis

North America Held the Largest Share of the Global Antiviral Drugs Market.

In 2025, North America dominated the global antiviral drugs market in 2025, accounting for 39.2% of the total market share. The region’s leadership is primarily attributed to its advanced healthcare infrastructure, high healthcare expenditure, and widespread access to antiviral therapies. A significant share of antiviral demand is generated from the United States, where substantial investments are made in infectious disease management, pharmaceutical innovation, and public health programs.

In addition, well-established screening and diagnostic systems support early disease detection and timely treatment initiation, contributing to higher antiviral therapy adoption rates. Moreover, ongoing efforts to manage HIV, hepatitis, influenza, COVID-19, and other viral infections continue to drive demand for antiviral therapies, reinforcing North America’s dominant position in the global antiviral drugs market.

Europe is a substantial market for antivirals, because to well-established healthcare systems, strong government-sponsored disease prevention programs, and widespread access to antiviral medicines. Asia Pacific is predicted to develop the fastest over the forecast period, owing to its huge population base, increasing prevalence of viral infections, improved healthcare infrastructure, and rising healthcare expenditure in countries like as China and India.

Latin America is seeing stable growth as a result of improved healthcare access and increased investment in infectious disease management. Meanwhile, the Middle East and Africa region is progressively expanding, aided by improved healthcare facilities, expanded public health activities, and increased attempts to improve access to antiviral medications.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Global Antiviral Drugs Market is moderately consolidated, with a few global pharmaceutical corporations accounting for a sizable portion of total market sales. Companies with well-established antiviral portfolios, strong intellectual property holdings, significant R&D capabilities, and global distribution networks dominate the market. The market has high entry hurdles due to stringent regulatory regulations, long medication development delays, and major expenditure required for antiviral research and clinical trials.

As a result, major companies have strong competitive positions thanks to established product portfolios and long-standing connections with healthcare providers and government health agencies. Furthermore, market share is increasingly determined by the ability to discover novel medicines, obtain regulatory clearances, broaden therapeutic indications, and improve worldwide commercialization skills.

Gilead Sciences, Inc. remains one of the leading players in the market, supported by its strong position in HIV and viral hepatitis therapies and continued focus on innovative antiviral solutions. Merck & Co., Inc. maintains a substantial market presence through its broad infectious disease portfolio and ongoing investments in antiviral research and development. These companies compete through product innovation, strategic collaborations, regulatory approvals, and portfolio expansion, while continued investments in next-generation antiviral therapies are expected to further shape the competitive landscape of the global antiviral drug market.

Top Key Players

- Gilead Sciences

- Pfizer Inc.

- Merck & Co. (MSD)

- Roche Holding AG

- Johnson & Johnson

- AbbVie Inc.

- Novartis AG

- Lonza Group AG

- Catalent, Inc.

- Cytiva (Danaher)

- Samsung Biologics

- Thermo Fisher Scientific

- Bayer AG

- Bristol Myers Squibb

- Other Key Players

Key Development

- In June 2025, Merck & Co., Inc. received U.S. FDA approval for ENFLONSIA (clesrovimab) for the prevention of RSV lower respiratory tract disease in infants. The approval strengthened the company’s infectious disease portfolio and expanded prevention options for RSV management through a single-dose, season-long protective therapy.

- In June 2025, Gilead Sciences Inc. received U.S. FDA approval for Yeztugo (lenacapavir) for HIV prevention. The long-acting therapy provides six months of protection per dose, supporting improved treatment adherence and advancing innovation in antiviral disease prevention.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 68.2 Billion |

| Forecast Revenue (2035) | US$ 98 Billion |

| CAGR (2026-2035) | 3.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Drug Class (Nucleoside & Nucleotide Analogues, Protease Inhibitors, Integrase Inhibitors, Neuraminidase Inhibitors, Reverse Transcriptase Inhibitors, Fusion & Entry Inhibitors, Polymerase Inhibitors, and Others), By Indication (Human Immunodeficiency Virus (HIV), Hepatitis B, Hepatitis C, Influenza, Herpes Simplex Virus (HSV), Cytomegalovirus (CMV), Respiratory Syncytial Virus (RSV), COVID-19, and Others), By Route of Administration (Oral, Injectable, Topical, and Inhalation), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and Online Pharmacies), By Drug Type (Branded Drugs and Generic Drugs), By Age Group (Pediatric, Adult, and Geriatric). |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Gilead Sciences, Pfizer Inc., Merck & Co. (MSD), Roche Holding AG, Johnson & Johnson, AbbVie Inc., Novartis AG, Lonza Group AG, Catalent, Inc., Cytiva (Danaher), Samsung Biologics, Thermo Fisher Scientific, Bayer AG, Bristol Myers Squibb, and Other Key Players. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |