Quick Navigation

Report Overview

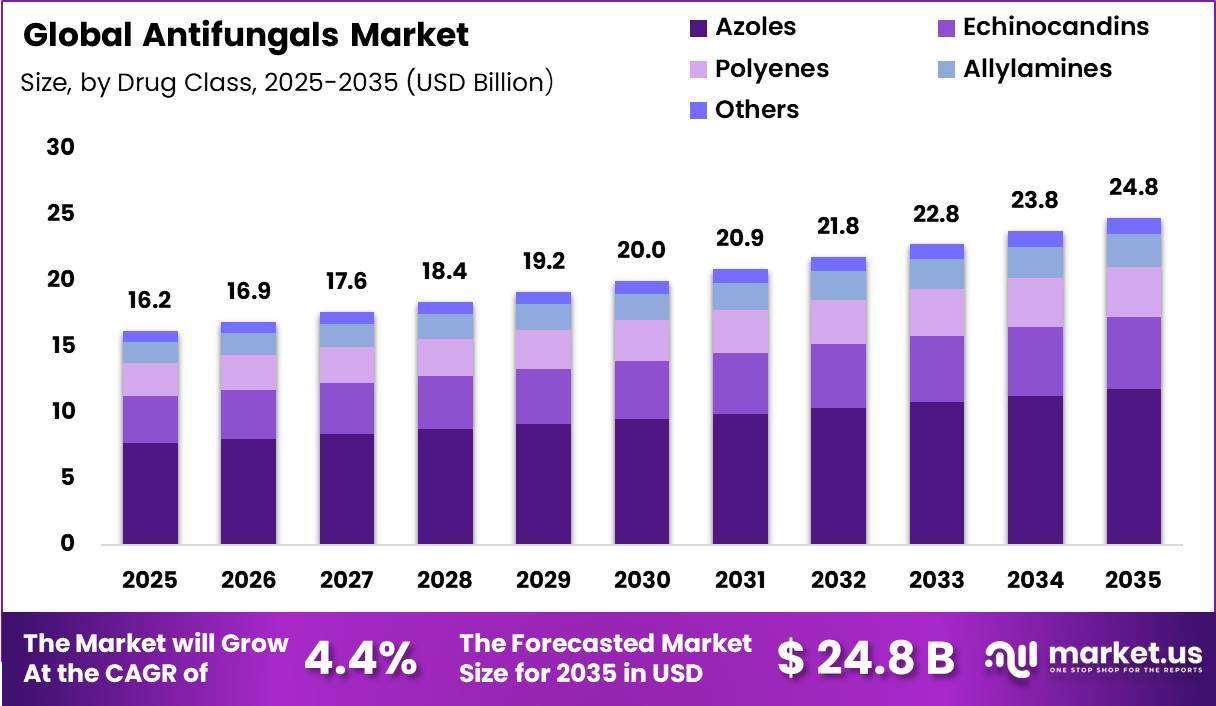

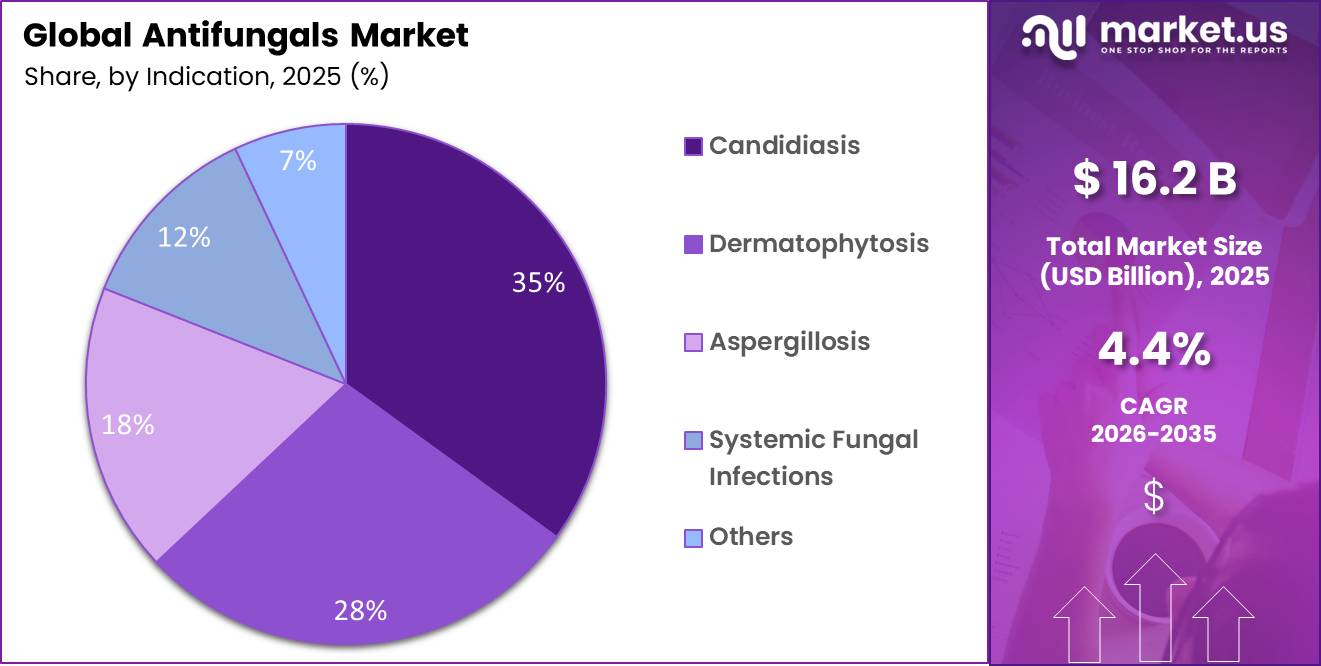

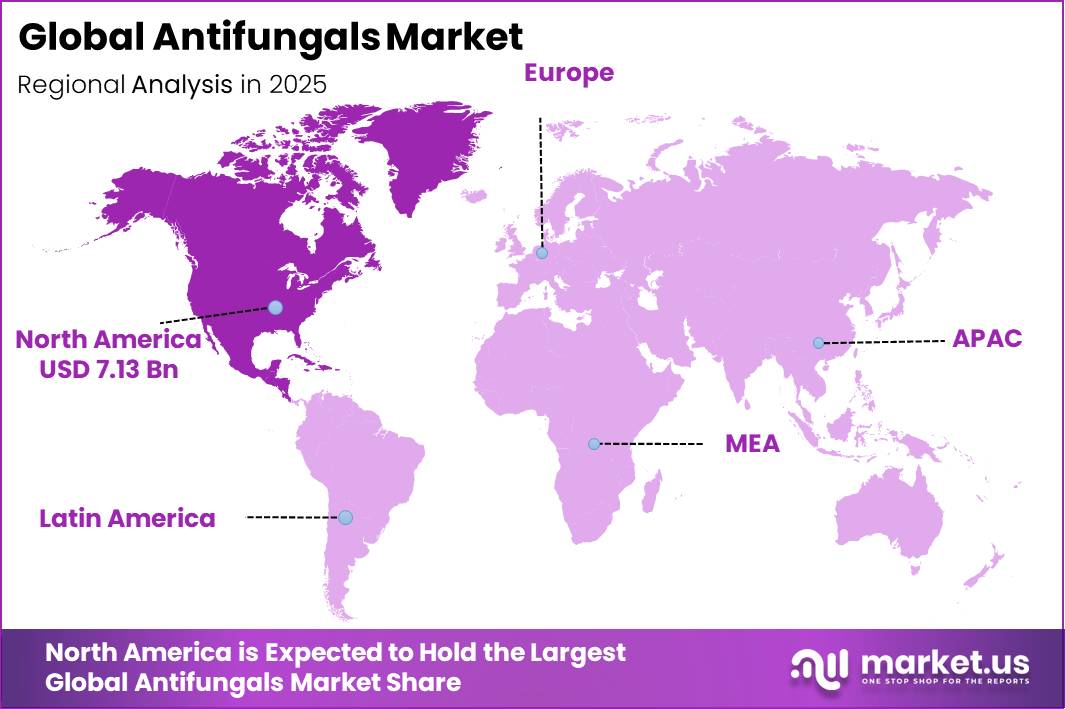

Global Antifungals Market size is expected to be worth around US$ 24.8 Billion by 2035 from US$ 16.2 Billion in 2025, growing at a CAGR of 4.4% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 44.1% share with a revenue of US$ 7.13 Billion.

The Antifungals market is a global pharmaceutical sector encompassing therapeutics designed to eliminate fungal pathogens or inhibit their growth and administered to treat fungal infections affecting skin, nails, mucous membranes, and internal organs across healthy patient populations worldwide. Fungal infections are a recognised and growing public health threat.

- According to data from the U.S. Centers for Disease Control and Prevention (CDC), clinical cases of the multi-drug resistant fungus Candida auris reached 6,304 in 2024, demonstrating an explosive surge from last years. CDC data from 2026 indicates that over 95% resistant to fluconazole, 15% resistant to amphotericin B, and 1% resistant to echinocandins.

The Antifungals market is driven by the escalating prevalence of hospital-acquired fungal infections and immunocompromised patient populations. The primary moving power behind the market is the critical clinical necessity to counteract escalating resistance against traditional treatments. Conversely, stringent regulatory assessment frameworks and high capital requirements for clinical drug development act as primary market restraints.

The market scope covers small-molecule chemical formulations and next-generation large-molecule biologics segmented by technology, alongside volume and dosage capacities spanning topical, oral, and intravenous administrations. The future market outlook is defined by strong alignment with artificial intelligence integration to accelerate diagnostic sequencing, predict mutation pathways, and optimize the structural screening of novel antimycotic compounds.

AI-powered antifungal susceptibility prediction platforms and digital diagnostic tools are being integrated into hospital infection management workflows, improving treatment selection speed and reducing empirical therapy failure rates.

Key Takeaways

- Market Size: Global Antifungals Market size is expected to be worth around US$ 24.8 Billion by 2035 from US$ 16.2 Billion in 2025.

- Market Share: The market is growing at a CAGR of 4.4% during the forecast period from 2026 to 2035.

- Drug Class Analysis: Azoles represent the dominant drug class segment holding a 47.6% market share which shows the high reliance on standard synthetic compounds.

- Indication Analysis: Candidiasis is the leading indication treated accounting for 35.0% of the market highlighting a widespread clinical need for yeast infection treatments.

- Route of Administration Analysis: Topical administration is the most dominant Route of Administration method at 42.0% proving that localized surface applications remain preferred over invasive options.

- Distribution Channel Analysis: Hospital Pharmacies serve as the dominant distribution channel with a 45.0% share indicating that major product volume moves through institutional care facilities.

- Regional Analysis: North America constitutes the largest regional market controlling 44.1% of the segment share driven by advanced healthcare infrastructure and higher spending power.

Drug Class Analysis

Azoles represents dominant Segment in the Market.

In 2025, Azoles accounted for a leading 47.6% share of the Antifungals market by drug class, due to their broad-spectrum antifungal activity, availability in both oral and intravenous formulations. Azoles inhibit ergosterol synthesis the primary fungal cell membrane component making them effective across a wide range of fungal pathogens.

Broad label approvals across multiple fungal indications, off-patent generic availability maintaining market volume, WHO recognition of azole-resistant pathogens as a priority public health concern, and extensive clinical experience across hospital and community prescribing are the primary structural determinants of Azoles segment dominance.

For instance, in December 2023, Cresemba (isavuconazonium sulfate), an azole antifungal, received expanded FDA approval for use in pediatric patients aged 1 year and older for the treatment of invasive aspergillosis and invasive mucormycosis, reinforcing its clinical utility in severe invasive fungal infections.

Echinocandins segment represents the fastest-growing drug class segment within the market scope. These therapies are currently recommended as the standard first-line intervention for most forms of invasive candidiasis. This includes highly resilient Candida auris infections where they remain the only class maintaining low resistance rates. Growth within this scope is determined by rising immunocompromised patient populations and a strong hospital formulary preference for their active fungicidal mechanism over fungistatic alternatives.

Indication Analysis

Candidiasis held Majority Share of the Market.

In 2025, Candidiasis accounted for a leading 35.0% share of the Antifungals market, due to Candida species position as the most common cause of invasive fungal infections globally affecting impacts individuals with weakened immune systems, surgical patients, ICU populations, and individuals receiving broad-spectrum antibiotics.

Candida auris alone reached 6,304 clinical cases in the United States in 2024 rising every year since 2016 with invasive Candida auris infections carrying crude mortality rates of 30%–72% by CDC, 2025. High global candidiasis incidence across both community and healthcare settings, expanding immunocompromised patient populations, escalating Candida auris case counts in hospital settings, and broad prescribing of oral fluconazole and topical azoles for vaginal candidiasis are the primary structural determinants.

Systemic Fungal Infections are the fastest-growing indication segment. Invasive fungal infections cause an estimated 1.5 million deaths annually globally with mortality exceeding that of malaria in many estimates driven by expanding populations from HIV, organ transplantation, and cancer chemotherapy by NIH/PMC, 2025. Between 2026 and 2035, systemic fungal infection antifungal demand is projected to grow alongside increasing antifungal resistance requiring more intensive treatment regimens.

Route of Administration Analysis

Topical is Most Widely Used Route of Administration.

In 2025, topical antifungals accounted for a leading 42.0% share of the market, driven by the high global prevalence of superficial fungal infections such as dermatophytosis, tinea infections, and cutaneous candidiasis. Their dominance is supported by easy self-application, localized drug delivery with minimal systemic exposure, low cost, OTC availability, and strong patient compliance in outpatient and primary care settings worldwide.

Oral antifungals represent the fastest-growing route of administration due to increasing demand for systemic treatment of moderate to severe fungal infections and step-down therapy from hospital-based intravenous care. Growth is supported by expanding immunocompromised patient populations, improved bioavailability of newer oral formulations, rising outpatient management trends, and the need for effective long-term therapy in recurrent and resistant fungal infections.

Distribution Channel Analysis

Antifungals Are Mostly Utilized in the Hospital Pharmacies.

In 2025, Hospital Pharmacies accounted for a leading 45% share of the Antifungals market. This dominance is due to the concentration of severe fungal infection management where parenteral echinocandin and azole therapies require hospital pharmacy dispensing, therapeutic drug monitoring, and specialist infectious disease physician oversight.

Intravenous antifungal administration requirements, hospital formulary management policies, therapeutic drug monitoring requirements for azole plasma concentration monitoring are the primary structural determinants.

Online pharmacies represent the fastest-growing distribution channel for antifungals, supported by rising telemedicine adoption, expanding e-prescription systems, and increasing consumer access to topical and oral treatments for superficial fungal infections. Growth is driven by convenience, improved digital healthcare infrastructure, and regulatory support for e-pharmacy platforms across developed and emerging markets, enabling wider access to community-based antifungal therapies.

Key Market Segments

By Drug Class

- Azoles

- Echinocandins

- Polyenes

- Allylamines

- Others

By Indication

- Candidiasis

- Dermatophytosis

- Aspergillosis

- Systemic Fungal Infections

- Others

By Route of Administration

- Topical

- Oral

- Parenteral

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies & Drug Stores

- Online Pharmacies

- Others

Drivers

Resistance Led Therapy Escalation in Antifungals

Antifungal resistance is increasingly shifting treatment from low cost first line regimens toward higher value salvage and combination therapies, expanding revenue per treated case even when patient volumes rise modestly. The Centers for Disease Control and Prevention reports that antimicrobial resistant fungal infections are increasing globally, while only three major antifungal classes are available in routine clinical use, structurally limiting substitution options and increasing dependence on newer or broader spectrum agents.

A key example is Candida auris, where CDC data show high resistance to fluconazole, substantial resistance to amphotericin B, and low resistance to echinocandins, alongside rising U.S. cases in 2024. This resistance profile drives earlier use of echinocandins, greater reliance on susceptibility testing, and increased use of combination or salvage therapies in hospital settings.

The World Health Organization has also classified multiple fungal pathogens as critical priorities, with mortality rates reaching up to 88 % in severe cases, reinforcing payer willingness to support higher cost therapies due to the consequences of treatment failure.

Commercially, this dynamic increases per case antifungal spend, accelerates uptake of newer agents, and shortens the lifecycle of older, low cost drugs. Even without major volume expansion, resistance driven escalation structurally raises market value by shifting treatment toward intensive, hospital based protocols and premium antifungal classes.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Resistance-led therapy escalation in Candida auris and invasive candidiasis | +1.6% | North America core, EU tertiary care, Gulf hospitals, APAC metro hospitals | Short term |

| Hospital-acquired fungal burden and high-cost inpatient episodes | +1.3% | North America core, EU, China, India urban tertiary centers, LatAm referral systems | Short term |

| New antifungal pipeline and class expansion beyond legacy azoles | +1.1% | US launch market, EU follow-on, Japan, China selective uptake | Medium term |

| Diagnostics gap driving broader empiric use and stewardship-linked procurement | +0.9% | LMICs, South Asia, Africa, Southeast Asia, public hospitals globally | Medium term |

| Immunocompromised patient pool expansion across oncology, transplant, ICU and biologics | +1.4% | US, EU5, Japan, China, South Korea, high-acuity private systems in India | Medium term |

| Public-health prioritization of fungal pathogens and surveillance funding | +0.8% | US federal/state systems, EU public health, WHO-linked LMIC programs | Long term |

Challenges

Escalating Antifungal Resistance as a Structural Growth Constraint

Rising antifungal resistance is reshaping treatment pathways and limiting the sector’s potential growth trajectory, with pathogens such as Candida auris, Aspergillus fumigatus, and azole-resistant Candida parapsilosis increasingly requiring higher-cost, second-line therapies.

The Centers for Disease Control and Prevention reports fluconazole resistance exceeding 90% in C. auris isolates, reinforcing a shift away from traditional first-line azoles toward echinocandins and combination regimens.This resistance pattern increases per-episode treatment costs by 40–70% and extends hospital stays by 3–5 days, while also pushing hospitals toward stricter antifungal stewardship and tighter formulary controls.

As a result, adoption of newer agents becomes more selective, and overall market expansion is partially offset by constrained utilization pathways.Operationally, variability in antifungal demand is increasing, with fluctuations in key drug classes rising significantly compared to pre-2019 baselines. This forces hospitals to maintain higher safety stock levels and complicates procurement planning, adding inefficiencies to hospital pharmacy operations.

From an industry perspective, manufacturers are increasingly required to integrate resistance surveillance, susceptibility testing partnerships, and stewardship-aligned clinical trial designs. This adds 2–3 years to development timelines and increases collaboration requirements with hospital systems, while also reshaping pipeline priorities toward resistance-resilient agents and optimized dosing strategies.Overall, escalating resistance compresses baseline antifungal growth potential, shifting the market toward higher-value but more tightly controlled usage patterns.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Escalating antifungal resistance | -1.3% | North America, EU, Asia-Pacific tertiary care | Long term (≥ 4 years) |

| Diagnostic latency and under-detection | -0.8% | Emerging markets, community hospitals | Medium term (2-4 years) |

| Complex sterile injectables supply chain | -1.0% | US, India, EU manufacturing hubs | Medium term (2-4 years) |

| Regulatory and quality compliance load | -0.7% | US, EU, India, Latin America | Long term (≥ 4 years) |

| Talent and stewardship capability gap | -0.6% | Global, especially low-resource settings | Long term (≥ 4 years) |

Restraints

Escalating Antifungal Resistance & Stewardship Pressure

Rising antifungal resistance is constraining market growth by reducing effective treatment options and tightening stewardship controls, even as fungal disease burden increases. CDC-linked data show Candida auris with fluconazole resistance above 90%, alongside meaningful resistance to amphotericin B and emerging multi-drug resistance, reinforcing reliance on limited remaining classes such as echinocandins.

At the same time, global antifungal use has increased steadily over the past decade, driven mainly by azoles, but stewardship policies are now limiting empiric use, tightening prophylaxis criteria, and requiring susceptibility-guided therapy. This is expected to reduce treatment volumes by 10–15% versus unconstrained demand scenarios.The combined effect of resistance and stewardship is shifting care toward more selective, higher-cost therapies while limiting broad-spectrum usage and slowing adoption.

Overall, this dynamic is estimated to reduce antifungal market CAGR by around 2 % points.Strategically, manufacturers are investing more in resistance surveillance, real-world evidence, and stewardship programs, but these efforts increase costs and extend commercialization timelines, while resistant strains continue to pressure peak-sales assumptions in high-burden hospital settings.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating antifungal resistance & stewardship pressure | -2.0% | North America, EU, high-burden APAC & LatAm | Medium term (2–4 years) |

| Under-utilization and access gaps in advanced systemic agents | -1.8% | Middle-income APAC, LatAm, Africa, parts of Eastern Europe | Long term (≥ 4 years) |

| Pricing, reimbursement and hospital budget constraints | -1.5% | North America core, EU, selected APAC hubs | Short–Medium term (≤ 4 years) |

| Regulatory risk and slow innovation throughput | -1.2% | Global, skewed to high-income R&D centres | Long term (≥ 4 years) |

| Manufacturing, formulation and supply-chain fragility | -1.0% | Global, with acute impact in LMIC hospital channels | Short–Medium term (≤ 4 years) |

| Safety-driven label changes and class-specific usage restrictions | -0.8% | North America, EU, global dermatology and primary care | Short term (≤ 2 years) |

Opportunitys

AMR-Focused Antifungal Portfolios as a High-Value Opportunity

AMR-targeted antifungal portfolios represent a structural opportunity to shift the market from broad-spectrum agents toward precision therapies designed for resistant pathogens such as Candida auris, azole-resistant Aspergillus, and multidrug-resistant Candida species. These infections are increasing globally, while treatment options remain limited due to the small number of systemic antifungal classes in routine use.

The World Health Organization pipeline review highlights 21 clinical and 22 preclinical antifungal candidates, but development is fragmented and few programs are explicitly designed as integrated “AMR franchises” targeting high-risk cohorts such as ICU, oncology, and transplant patients.

These groups carry the highest fungal burden and can support premium pricing and higher-margin therapies.By segmenting patients based on resistance risk and combining targeted antifungals with diagnostic, surveillance, and susceptibility services, companies can move from commodity drug models to bundled, high-value care offerings.

This could unlock an estimated USD 2–3 billion in incremental addressable market by 2035 (around 10–15% of projected antifungal spend), translating into roughly 2.5 % points of CAGR upside versus baseline forecasts.Overall, AMR-focused portfolios shift antifungal strategy toward precision, high-acuity use cases where resistance drives both clinical urgency and willingness to pay, replacing volume-driven growth with value-driven specialization.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| AMR-focused antifungal portfolios | +2.5% | North America, EU, APAC emerging | Medium term (2-4 years) |

| Companion diagnostics & stewardship platforms | +2.0% | North America core, EU, GCC | Medium term (2-4 years) |

| Long-acting & depot formulations | +1.8% | North America, EU, East Asia | Long term (≥ 4 years) |

| Agri–human antifungal convergence solutions | +1.5% | Latin America, APAC emerging | Long term (≥ 4 years) |

| Access-driven models for LMIC fungal burden | +2.2% | Sub-Saharan Africa, South Asia | Medium term (2-4 years) |

| Novel mechanism and virulence-targeting agents | +3.0% | Global tertiary care hubs | Long term (≥ 4 years) |

Geopolitical Impact Analysis

U.S.-China Trade Tensions and Supply Chain Pressures Are Creating Active Pharmaceutical Ingredient Cost Headwinds Across the Global Antifungals Market.

The Antifungals market is exposed to geopolitical supply chain risk through its dependence on active pharmaceutical ingredient manufacturing concentrated in India and China. Azoles the dominant drug class market revenue rely on chemical synthesis routes using raw materials and intermediates sourced across Asian manufacturing networks. Escalating U.S.-China trade tensions and tariff escalation are introducing cost pressure into API supply chains that flows through to finished antifungal product manufacturing costs. For generic antifungal manufacturers who compete on price across retail pharmacy and hospital formulary channels API cost inflation directly compresses margins and complicates multi-year hospital supply contract pricing.

Russia’s geopolitical isolation following the invasion of Ukraine has created additional pharmaceutical supply chain disruption in Eastern Europe and Central Asia regions where antifungal treatment access is already constrained by healthcare system resource limitations. Restricted pharmaceutical import channels and currency depreciation have reduced antifungal availability in affected markets leaving immunocompromised patient populations with limited treatment options precisely when resistance is escalating globally.

Regional Analysis

North America Held the Largest Share of the Global Antifungals Market.

In 2025, North America dominated the global Antifungals market, holding about 44.1% of total global revenue. This dominance is due to a high burden of immunocompromised patients, advanced hospital infrastructure, and widespread adoption of premium antifungal therapies such as echinocandins and next-generation azoles.

Strong regulatory support, high healthcare expenditure, and well-established infectious disease management protocols further reinforce the region’s leadership in antifungal treatment demand. Candida auris has emerged as a specific North American public health crisis with 6,304 clinical cases reported in the United States in 2024 alone, spreading across 39 states and generating sustained institutional antifungal demand at the highest clinical acuity level by CDC, 2024.

Europe is the second-largest market, supported by established antifungal prescribing practices, strong regulatory oversight from the European Medicines Agency, and increasing concerns over azole-resistant Aspergillus infections linked to agricultural fungicide exposure.

Asia Pacific is the fastest-growing regional market, driven by expanding patient populations with immunosuppressive conditions, rising cancer and transplant volumes, and improving access to hospital-based antifungal therapies in countries such as China and India, alongside ongoing healthcare infrastructure development.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global antifungals market exhibits a highly consolidated oligopolistic behavior. A small group of multinational giants controls the vast majority of global revenue through proprietary, high-value systemic treatments.

All five of the most significant antifungal market participants Merck, Pfizer, Astellas Pharma, GSK, and Johnson & Johnson dominate the hospital-grade segment with frontline brands, protected by high clinical development costs and strict regulatory barriers. Branded antifungal market each holding significant hospital formulary positions across North America, Europe, and Asia Pacific through established echinocandin, azole, and novel antifungal product portfolios.

Companies like Novartis AG, Bayer AG, Johnson & Johnson, and Glenmark Pharmaceuticals Ltd. compete intensely for volume. They focus on lower-margin topical treatments and off-patent formulas where standardized manufacturing allows many local players to survive. Diversified firms like GSK plc, Sanofi S.A., and Abbott Laboratories leverage strong regional supply chains to secure specialized clinical niches. This creates a dual market structure which is highly consolidated for critical systemic therapies but yet fragmented for everyday topical treatments.

Major Players In The Market

- Merck & Co., Inc.

- Pfizer Inc.

- Novartis AG

- Bayer AG

- Astellas Pharma Inc.

- GSK plc

- Sanofi S.A.

- Abbott Laboratories

- Johnson & Johnson

- Glenmark Pharmaceuticals Ltd.

- Others

Key Development

- In June 2026, Pfizer Inc. expanded its commercial partnership with Sinopharm to promote the antifungal therapy Diflucan (fluconazole) across China and collaborate on future launches in the country. The deal focuses on supply‑chain optimization, resource integration and stronger execution, reinforcing Pfizer’s antifungal footprint in one of the world’s largest pharma markets.

- In August 2025, Glenmark Pharmaceuticals’ US subsidiary announced the launch of micafungin, a therapeutic equivalent of Mycamine, in single‑dose vials for the US market from September 2025, expanding its institutional antifungal portfolio and targeting an estimated annual turnover of around USD 60 million.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 16.2 Billion |

| Forecast Revenue (2035) | US$ 24.8 Billion |

| CAGR (2026-2035) | 4.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Drug Class (Azoles, Echinocandins, Polyenes, Allylamines, Others), By Indication (Candidiasis, Dermatophytosis, Aspergillosis, Systemic Fungal Infections, Others), By Route of Administration (Topical, Oral, Parenteral), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies & Drug Stores, Online Pharmacies, Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Merck & Co., Inc., Pfizer Inc., Novartis AG, Bayer AG, Astellas Pharma Inc., GSK plc, Sanofi S.A., Abbott Laboratories, Johnson & Johnson, Glenmark Pharmaceuticals Ltd., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |