Quick Navigation

Report Overview

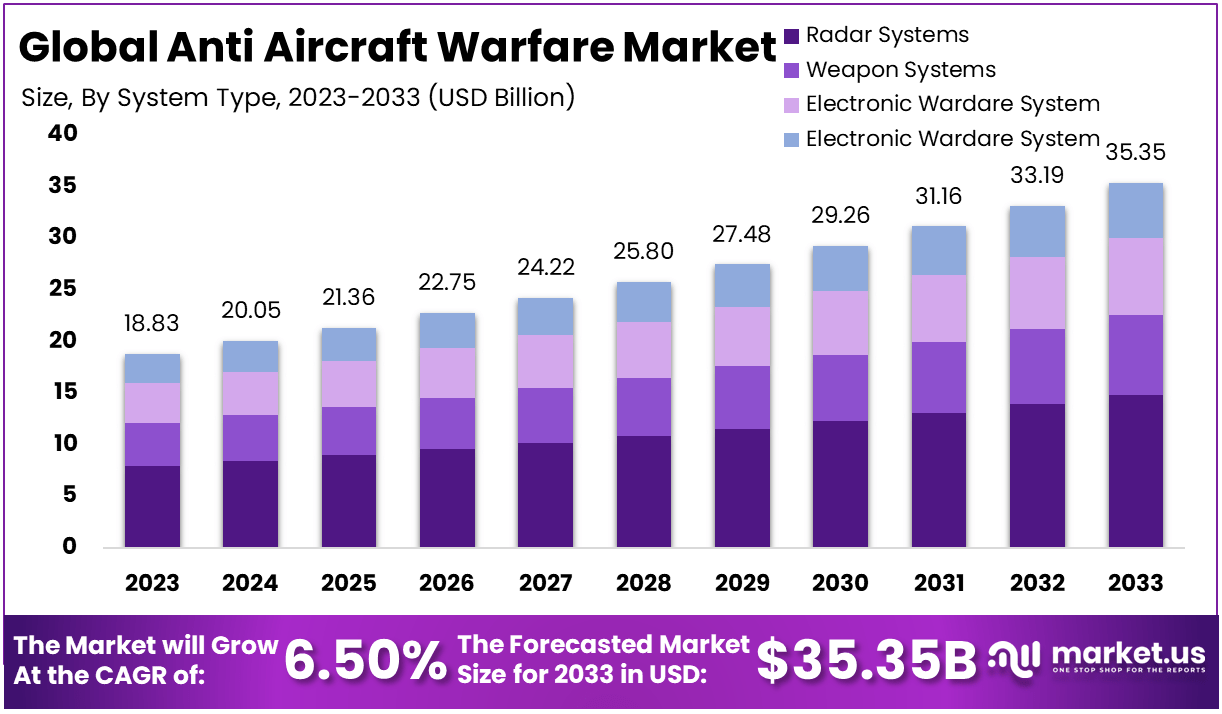

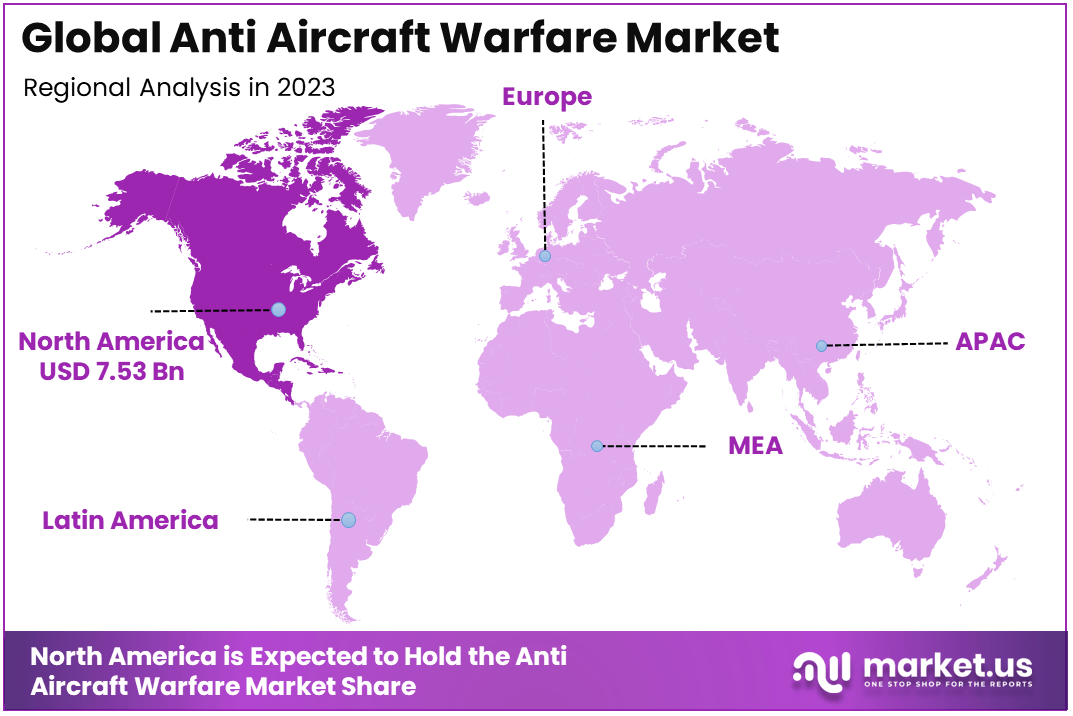

The Global Anti Aircraft Warfare Market size is expected to be worth around USD 35.35 Billion By 2033, from USD 18.83 Billion in 2023, growing at a CAGR of 6.50% during the forecast period from 2024 to 2033. In 2023, North America held a dominant market position, capturing more than a 40% share, holding USD 7.53 Billion in revenue.

Anti-aircraft warfare, also known as air defense, is a critical military strategy focused on countering aerial threats such as aircraft, drones, and missiles. It encompasses a range of tactics, systems, and technologies designed to detect, track, and neutralize airborne targets. These systems include surface-to-air missiles, anti-aircraft artillery, radar-guided weapons, and advanced laser systems.

Anti-aircraft warfare has evolved significantly over the years, with modern solutions leveraging automation, artificial intelligence, and real-time data analytics to enhance precision and operational efficiency. This domain plays a vital role in protecting military assets, civilian infrastructure, and national airspace from hostile incursions.

The anti-aircraft warfare market refers to the global industry involved in the development, production, and deployment of air defense systems and technologies. It includes key segments such as missile systems, radar technology, drones, and electronic warfare equipment. In 2023, the market witnessed significant growth due to increased geopolitical tensions, rising defense budgets, and advancements in military technology.

Nations across the globe are investing heavily in upgrading their air defense capabilities to counter the growing sophistication of aerial threats. The market is expected to expand further as innovations in hypersonic weapons and AI-driven solutions become more widespread, creating new opportunities for industry players.

The primary driving force behind the growth of the anti-aircraft warfare market is the increasing frequency of geopolitical conflicts and the rising need for robust national defense systems. According to the Stockholm International Peace Research Institute (SIPRI), global military spending reached a record $2.24 trillion in 2022, with a substantial portion allocated to air defense systems.

Additionally, the proliferation of unmanned aerial vehicles (UAVs) and hypersonic missiles has heightened the demand for advanced interception and tracking systems. Nations such as the United States, China, and India are actively modernizing their defense infrastructures, fueling market growth. For example, in 2023, the U.S. Department of Defense announced a $5 billion investment in next-generation missile defense systems.

The growing reliance on aerial assets in modern warfare has amplified the demand for anti-aircraft systems. Advanced fighter jets, stealth bombers, and unmanned drones have become integral to military operations, prompting nations to strengthen their air defense networks.

Demand is particularly high for integrated air and missile defense systems (IAMD) that combine radar, command-and-control systems, and interceptors for multi-layered protection. Emerging economies in Asia-Pacific and the Middle East are key contributors to this demand, as they seek to counter regional threats and modernize their military capabilities.

The rise of unmanned aerial threats and hypersonic missile technology presents significant opportunities for innovation in the anti-aircraft warfare market. Companies specializing in AI, machine learning, and autonomous systems are well-positioned to capitalize on this trend. The integration of AI into radar systems, for instance, allows for faster and more accurate target identification, enhancing situational awareness.

Additionally, the development of laser-based defense systems, such as directed energy weapons (DEWs), represents a promising avenue. According to a report by Lockheed Martin, investments in laser technology are expected to surpass $3 billion by 2025, offering lucrative opportunities for market players.

The anti-aircraft warfare market has seen rapid technological progress, with key advancements in radar systems, electronic warfare, and missile interception. The adoption of active electronically scanned array (AESA) radars has revolutionized target detection, providing greater range and accuracy. Additionally, AI-driven command-and-control systems now enable real-time data sharing and decision-making, reducing response times during critical operations.

Hypersonic missile defense is another focus area, with research efforts underway to develop systems capable of intercepting weapons traveling at speeds exceeding Mach 5. Furthermore, the use of 5G technology in military networks enhances communication and coordination among air defense assets, ensuring seamless operations.

Technological advancements are critical in driving this growth, particularly in missile defense systems and unmanned aerial systems (UAS). The increasing threat posed by UAS is a significant factor, as evidenced by reports of 181,166 registered drone pilots in the UK as of April 2022 and approximately 6,000 drone-related incidents reported to police within that year.

Additionally, the market’s dynamics are influenced by various segments; for instance, the weapon systems category is expected to capture about 39% of total revenue by the end of the forecast period. The medium-range anti-aircraft systems are projected to dominate sales, accounting for approximately 53.3% of total sales in 2023.

Key Takeaways

- Market Growth: The global anti-aircraft warfare market is projected to grow from USD 18.83 billion in 2023 to USD 35.35 billion in 2033, registering a CAGR of 6.50% during the forecast period.

- Dominant System Type: The Weapon Systems segment held the largest market share in 2023, accounting for 42%, driven by increasing investments in advanced missile and laser-based air defense technologies.

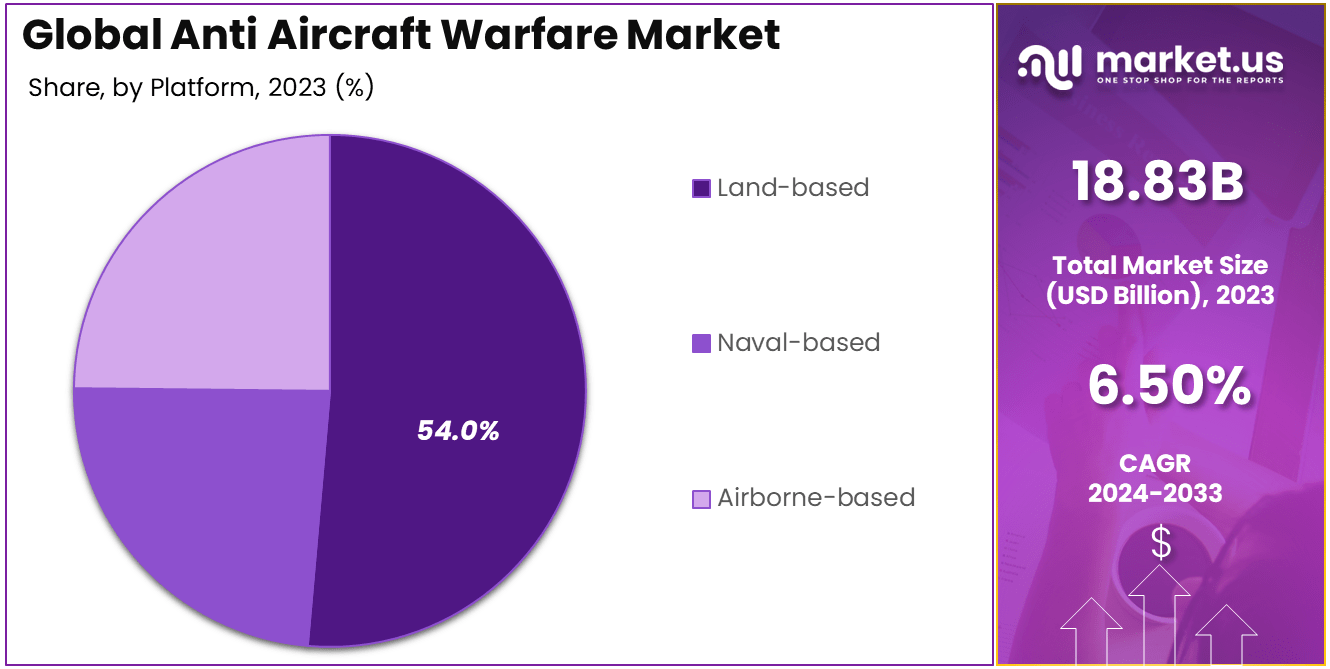

- Leading Platform: The Land-based platform dominated the market in 2023, capturing 54% of the share, attributed to its scalability, mobility, and critical role in military infrastructure modernization.

- Range Leadership: The Long-range (>150 km) segment accounted for 39% of the market in 2023, fueled by the growing need for multi-layered defense systems capable of countering hypersonic and long-range threats.

- Regional Dominance: North America led the global market in 2023, with a 40% share, reflecting USD 7.53 billion in revenue. This is supported by high defense spending and continued technological advancements in the U.S. defense sector.

By System Type

In 2023, the Weapon Systems segment held a dominant market position, capturing more than 42% of the market share. This leadership is attributed to the growing demand for advanced and multi-layered air defense solutions that can neutralize various threats, including unmanned aerial vehicles (UAVs), cruise missiles, and hypersonic missiles.

Countries worldwide are investing heavily in modern weapon systems to enhance their military capabilities in response to rising geopolitical tensions and evolving aerial threats. Weapon systems play a critical role in anti-aircraft warfare as they provide direct and immediate response capabilities against airborne threats.

These systems, which include missile defense systems, anti-aircraft guns, and laser-based weaponry, are designed to intercept and destroy enemy targets with high precision. For instance, the increasing deployment of advanced missile systems, such as the U.S. Patriot and THAAD systems, underscores the importance of weapon systems in ensuring national and regional security.

Additionally, advancements in directed-energy weapons, such as high-energy lasers, are further strengthening this segment’s dominance by offering cost-effective and reusable solutions for countering aerial threats. Another key factor driving the dominance of weapon systems is their integration with modern technologies, such as artificial intelligence and machine learning.

These technologies improve target identification, tracking, and decision-making, making weapon systems more efficient and reliable in dynamic combat scenarios. For example, countries like Israel have successfully implemented AI-enabled air defense systems, such as the Iron Dome, which has proven effective in intercepting incoming projectiles with high accuracy.

By Platform

In 2023, the Land-based segment held a dominant market position, capturing more than 54% of the market share. This segment’s leadership is attributed to the increasing deployment of ground-based air defense systems to safeguard critical infrastructure, military installations, and civilian areas from aerial threats.

Land-based platforms offer strategic advantages, including mobility, scalability, and long-range defense capabilities, making them a preferred choice for many defense forces worldwide. The dominance of the land-based segment is driven by the adoption of advanced missile defense systems such as the U.S. Patriot system, Russia’s S-400, and India’s Akash system.

These systems are specifically designed to counter a wide range of threats, including drones, cruise missiles, and ballistic missiles. Moreover, land-based platforms are equipped with sophisticated radar and sensor systems, allowing them to detect and neutralize threats over extensive ranges.

For instance, the S-400 system is capable of intercepting targets at distances of up to 400 kilometers, making it one of the most advanced land-based solutions available. Additionally, the land-based segment benefits from significant investments in defense modernization programs.

Governments globally are prioritizing the development and procurement of land-based air defense systems to enhance their military capabilities. For example, NATO countries are actively collaborating on programs like the European Sky Shield Initiative to deploy state-of-the-art land-based air defense systems across the continent. Such initiatives highlight the critical role of land-based platforms in ensuring national and regional security.

By Range

In 2023, the Long-range (over 150 km) segment held a dominant market position, capturing more than 39% of the total market share. This leadership can be attributed to the increasing need for advanced air defense systems capable of intercepting threats from long distances, ensuring national security and strategic military advantage.

The ability to counter threats such as ballistic missiles, hypersonic weapons, and high-altitude aircraft has made long-range systems a top priority for military forces worldwide. The dominance of the long-range segment is driven by the deployment of highly advanced missile systems like the S-400 by Russia, THAAD (Terminal High Altitude Area Defense) by the U.S., and HQ-9 by China.

These systems provide unparalleled defensive capabilities, including the ability to intercept threats before they reach critical targets. For instance, the U.S. THAAD system is designed to detect and intercept ballistic missiles at ranges exceeding 200 kilometers, providing a robust shield against aerial attacks.

Such systems are frequently procured by nations looking to enhance their long-range interception capabilities, further boosting the segment’s growth. Another critical factor supporting the long-range segment’s dominance is its effectiveness in addressing evolving aerial threats such as hypersonic missiles and advanced UAVs (unmanned aerial vehicles).

These threats often require sophisticated radar systems, extended-range interceptors, and real-time tracking capabilities, all of which are core features of long-range air defense systems. For example, Russia’s S-500 Prometey is equipped to counter hypersonic weapons at ranges beyond 600 kilometers, underlining the growing focus on long-range solutions.

Key Market Segments

By System Type

- Weapon Systems

- Radar Systems

- Electronic Warfare System

- Command and Control Systems

By Platform

- Land-based

- Naval-based

- Airborne-based

By Range

- Short-range (0-50 km)

- Medium-range (50-150 km)

- Long-range (>150 km)

Driving Factors

Increasing Geopolitical Tensions and Defense Modernization

The rising geopolitical tensions and regional conflicts have become significant drivers for the growth of the anti-aircraft warfare market. Nations are increasingly prioritizing defense modernization to counter threats posed by adversarial countries, particularly in regions like Asia-Pacific, the Middle East, and Eastern Europe.

With countries like India, China, and the U.S. ramping up defense spending, investments in advanced air defense systems have surged significantly. For instance, global defense expenditure reached USD 2.24 trillion in 2023, a significant portion of which is allocated to anti-aircraft and missile defense systems.

Emerging threats, including drones, ballistic missiles, and hypersonic weapons, have further emphasized the importance of robust air defense infrastructure. Long-range missile systems like THAAD (Terminal High Altitude Area Defense), Patriot Systems, and S-400 are in high demand, ensuring strategic superiority.

Moreover, international collaborations for technology transfer and joint development have contributed to market growth. For example, India’s defense collaboration with Russia for the S-400 systems highlights the growing focus on securing aerial borders and countering evolving threats. This focus has cemented defense modernization as a primary driver of the anti-aircraft warfare market.

Restraining Factors

High Procurement and Maintenance Costs

One of the key restraints limiting the growth of the anti-aircraft warfare market is the high cost associated with the procurement, deployment, and maintenance of advanced air defense systems. Modern long-range missile systems and radar platforms involve substantial investments, making them unaffordable for many developing nations.

For example, the cost of a single THAAD battery is estimated at USD 800 million. This price excludes operational and lifecycle maintenance expenses, which can further burden the defense budgets of nations with limited resources.

Additionally, the integration of these systems with existing defense infrastructure often requires significant investments in training personnel and upgrading related technologies. This complexity adds to the financial strain, deterring smaller countries or those with constrained budgets from adopting high-end anti-aircraft solutions.

For instance, while countries like the United States and China have vast budgets to support defense innovation, others in regions like Africa or Southeast Asia struggle to allocate funds, which can inhibit market penetration.

Growth Opportunities

Rise of Autonomous and AI-Driven Air Defense Systems

The emergence of autonomous systems and AI-driven air defense technologies presents a significant growth opportunity in the anti-aircraft warfare market. Autonomous air defense platforms powered by artificial intelligence can track, predict, and neutralize aerial threats in real time, reducing human intervention and improving response accuracy.

For instance, AI-integrated systems like Israel’s Iron Dome leverage real-time data analytics and machine learning to assess incoming threats, ensuring rapid interception. Furthermore, the increasing development of unmanned systems and drones has spurred the demand for autonomous counter-air platforms.

NATO’s recent focus on developing AI-powered radar systems highlights the growing emphasis on leveraging next-gen technologies. Companies and governments are increasingly collaborating to research and develop such systems. For instance, BAE Systems partnered with the UK Ministry of Defence to work on AI-enabled defense technologies, creating lucrative opportunities for market players.

Challenge Factors

Integration Complexity with Legacy Systems

A significant challenge faced by the anti-aircraft warfare market is the integration of modern systems with legacy platforms. Many nations rely on older air defense systems that are not compatible with current technologies, such as AI-powered radars or hypersonic missile interceptors.

This incompatibility creates hurdles in seamless upgrades, forcing countries to invest in entirely new systems, which is both time-consuming and costly. Moreover, nations like India and Turkey, which operate a mix of systems sourced from various countries, face additional challenges due to interoperability issues. For example, integrating Russian-made S-400 systems with U.S.-manufactured Patriot platforms requires complex modifications.

Such technical and logistical challenges can delay deployment and operational readiness, impacting the overall efficiency of national defense strategies. Addressing these integration challenges is critical for market growth.

Growth Factors

Rising Defense Expenditure and Geopolitical Tensions

The anti-aircraft warfare market is witnessing significant growth due to increasing defense budgets worldwide and heightened geopolitical tensions. With a substantial portion allocated to enhancing air defense capabilities.

Countries like the United States, China, and India are investing heavily in advanced anti-aircraft systems to counter evolving threats, including drones, hypersonic missiles, and ballistic weapons. This focus on modernizing military arsenals and securing aerial borders is driving the demand for sophisticated air defense technologies.

Emerging Trends

AI and Autonomous Air Defense Systems

The integration of artificial intelligence (AI) and autonomous systems is a key trend transforming the anti-aircraft warfare market. AI-driven platforms, such as Israel’s Iron Dome and Russia’s S-400, offer real-time threat detection, predictive analytics, and automated response mechanisms.

Additionally, the development of autonomous drone interceptors and hypersonic missile defense systems is gaining traction. Collaborations between governments and defense contractors, like BAE Systems and the UK Ministry of Defence, are accelerating advancements in next-gen air defense technologies.

Business Benefits

Enhanced Security and Strategic Superiority

Adopting advanced anti-aircraft warfare systems ensures robust national security and provides strategic advantages. These systems not only safeguard critical infrastructure but also enable nations to project power and deter adversarial threats effectively.

Modern air defense platforms improve response times, enhance situational awareness, and reduce dependency on manpower, thereby increasing operational efficiency. For defense contractors, the growing demand presents lucrative opportunities for long-term contracts and innovation in cutting-edge technologies.

Regional Analysis

In 2023, North America held a dominant market position in the anti-aircraft warfare market, capturing more than 40% market share, which equates to approximately USD 7.53 billion in revenue. The region’s leadership in this sector is attributed to its substantial defense budgets, advanced technological capabilities, and robust military modernization programs.

The United States, as the largest defense spender globally, accounted for the majority of this revenue. A significant portion of this was directed toward enhancing air defense capabilities, including anti-aircraft systems.

The presence of major defense contractors like Lockheed Martin, Raytheon Technologies, and Northrop Grumman further strengthens the region’s market position. These companies are actively developing and deploying cutting-edge anti-aircraft systems, including the Patriot missile defense system and the THAAD (Terminal High Altitude Area Defense) system, which are widely regarded as some of the most advanced technologies in the world.

Additionally, North America leads in the integration of artificial intelligence (AI) and advanced radar systems, making its air defense infrastructure both resilient and future-ready.

The region’s leadership is also driven by increased procurement initiatives and partnerships. For instance, in 2023, the U.S. Department of Defense announced multi-billion-dollar contracts for upgrading its anti-aircraft and missile defense systems to counter emerging threats like hypersonic missiles and drone swarms.

Furthermore, the North American Aerospace Defense Command (NORAD), a joint initiative between the U.S. and Canada, has been investing heavily in modernizing air surveillance and defense capabilities, contributing to the region’s dominance in the anti-aircraft warfare market.

Looking ahead, North America is expected to maintain its leadership position due to its focus on research and development, procurement of advanced systems, and strategic collaborations with global allies. The continued emphasis on countering evolving threats, coupled with consistent government support, positions North America as the hub for innovation and growth in the anti-aircraft warfare market.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

In 2024, BAE Systems expanded its leadership in the anti-aircraft warfare market through its acquisition of a cutting-edge radar technology company based in the United States. This acquisition aimed to enhance BAE’s capabilities in early detection and tracking of aerial threats, including hypersonic missiles.

Additionally, BAE Systems launched its advanced SkyGuard Air Defense System, which combines high-precision targeting and artificial intelligence to optimize interception capabilities. This development has positioned BAE Systems as a key innovator in delivering effective and scalable air defense solutions.

Israel Aerospace Industries (IAI) continues to dominate the market with its Barak MX Integrated Air Defense System, which offers customizable solutions for countering a wide range of airborne threats, including UAVs, missiles, and fighter jets.

In 2024, IAI announced a collaboration with an unnamed European defense agency to co-develop next-generation missile defense systems. This partnership emphasizes IAI’s global influence and commitment to advancing multi-layered air defense technologies. The company’s investments in R&D ensure it remains at the forefront of anti-aircraft warfare innovation.

Kongsberg Gruppen ASA strengthened its market presence in 2024 by launching its upgraded NASAMS (National Advanced Surface-to-Air Missile System) in partnership with Raytheon Technologies. The new version integrates advanced radar systems and real-time data-sharing technologies to improve the efficiency of countering modern aerial threats.

Kongsberg also entered a strategic merger with a leading European defense electronics firm, enabling the company to broaden its product offerings and expand its market reach, especially in NATO countries. This merger reflects Kongsberg’s commitment to enhancing its capabilities in the anti-aircraft defense domain.

Top Key Players in the Market

- BAE Systems

- Israel Aerospace Industries Ltd.

- Kongsberg Gruppen ASA

- Leonardo S.p.A.

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- Rafael Advanced Defense Systems Ltd.

- Raytheon Technologies Corporation

- Rheinmetall AG

- Thales Group

- Saab Group

- MBDA

- Diehl Defence

- Boeing

- Other Key Players

Recent Developments

- In 2024: Raytheon Technologies introduced an upgraded version of its Patriot Advanced Capability-3 (PAC-3) missile defense system with enhanced long-range capabilities and advanced tracking technologies.

- In 2024: Lockheed Martin successfully tested its Long-Range Discrimination Radar (LRDR) in conjunction with the Terminal High Altitude Area Defense (THAAD) system. The test demonstrated the capability to detect and intercept multiple threats simultaneously, including ballistic missiles and stealth drones.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 18.83 Bn |

| Forecast Revenue (2033) | USD 35.35 Bn |

| CAGR (2024-2033) | 6.50% |

| Largest Market | North America |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By System Type (Weapon Systems, Radar Systems, Electronic Warfare System, Command and Control Systems), By Platform (Land-based, Naval-based, Airborne-based), By Range (Short-range(0-50 km), Medium-range(50-150 km), Long-range (>150 km)) |

| Regional Analysis | North America (US, Canada), Europe (Germany, UK, Spain, Austria, Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, Thailand, Rest of Asia-Pacific), Latin America (Brazil), Middle East & Africa(South Africa, Saudi Arabia, United Arab Emirates) |

| Competitive Landscape | BAE Systems, Israel Aerospace Industries Ltd., Kongsberg Gruppen ASA, Leonardo S.p.A., Lockheed Martin Corporation, Northrop Grumman Corporation, Rafael Advanced Defense Systems Ltd., Raytheon Technologies Corporation, Rheinmetall AG, Thales Group, Saab Group, MBDA, Diehl Defence, Boeing, Other Key Players |

| Customization Scope | We will provide customization for segments and at the region/country level. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |