Quick Navigation

Report Overview

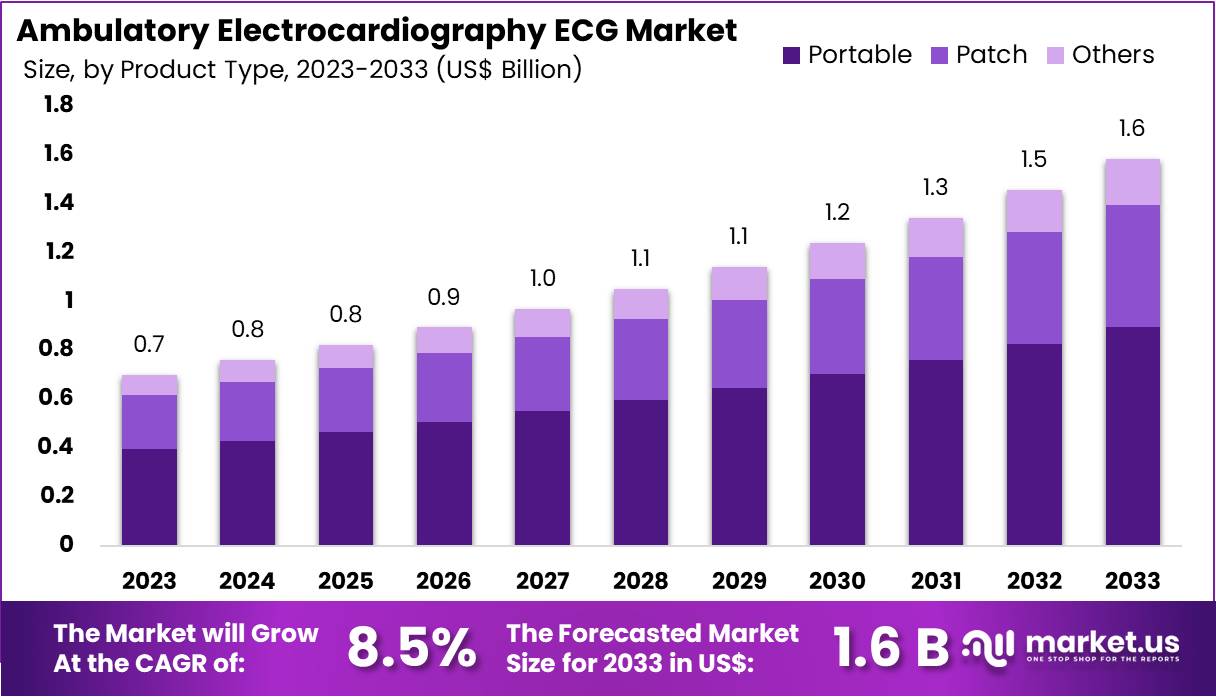

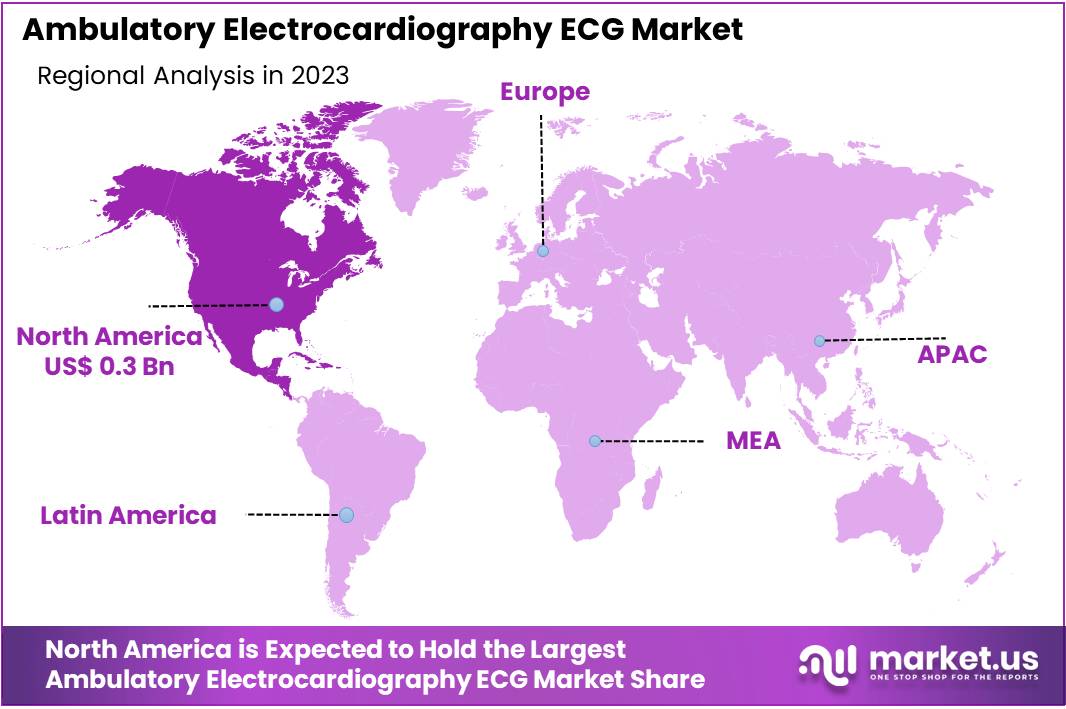

The Global Ambulatory Electrocardiography ECG Market size is expected to be worth around US$ 1.6 Billion by 2033, from US$ 0.7 Billion in 2023, growing at a CAGR of 8.5% during the forecast period from 2024 to 2033. North America dominated the market, accounting for over 39.4% of the share and achieving a market value of approximately US$ 0.3 billion for the year.

Increasing demand for continuous and real-time cardiac monitoring has significantly driven the growth of the ambulatory electrocardiography (ECG) market. Ambulatory ECG systems, such as Holter monitors and Mobile Cardiac Telemetry (MCT) devices, enable the monitoring of patients outside of clinical settings, offering physicians valuable insights into cardiac health over extended periods.

These systems are essential in diagnosing arrhythmias, monitoring post-operative patients, and assessing patients with chronic heart conditions. As the prevalence of cardiovascular diseases rises, healthcare providers are increasingly relying on ambulatory ECG devices to improve diagnostic accuracy and enhance patient management. The rise of remote patient monitoring solutions also creates new opportunities, allowing healthcare professionals to track patients’ cardiac conditions in real time, reducing hospital visits and enhancing care efficiency.

In May 2024, Vivalink introduced its all-in-one technological platform for Holter monitoring and MCT, offering a comprehensive remote cardiac monitoring solution. This innovation is expected to improve the efficiency and accuracy of cardiac care by providing seamless data integration for healthcare professionals. As the ambulatory ECG market continues to evolve, ongoing technological advancements promise more sophisticated, user-friendly, and cost-effective solutions for both patients and healthcare providers.

Key Takeaways

- In 2023, the market for ambulatory electrocardiography ECG generated a revenue of US$ 0.7 billion, with a CAGR of 8.5%, and is expected to reach US$ 1.6 billion by the year 2033.

- The product type segment is divided into portable, patch, and others, with portable taking the lead in 2023 with a market share of 56.7%.

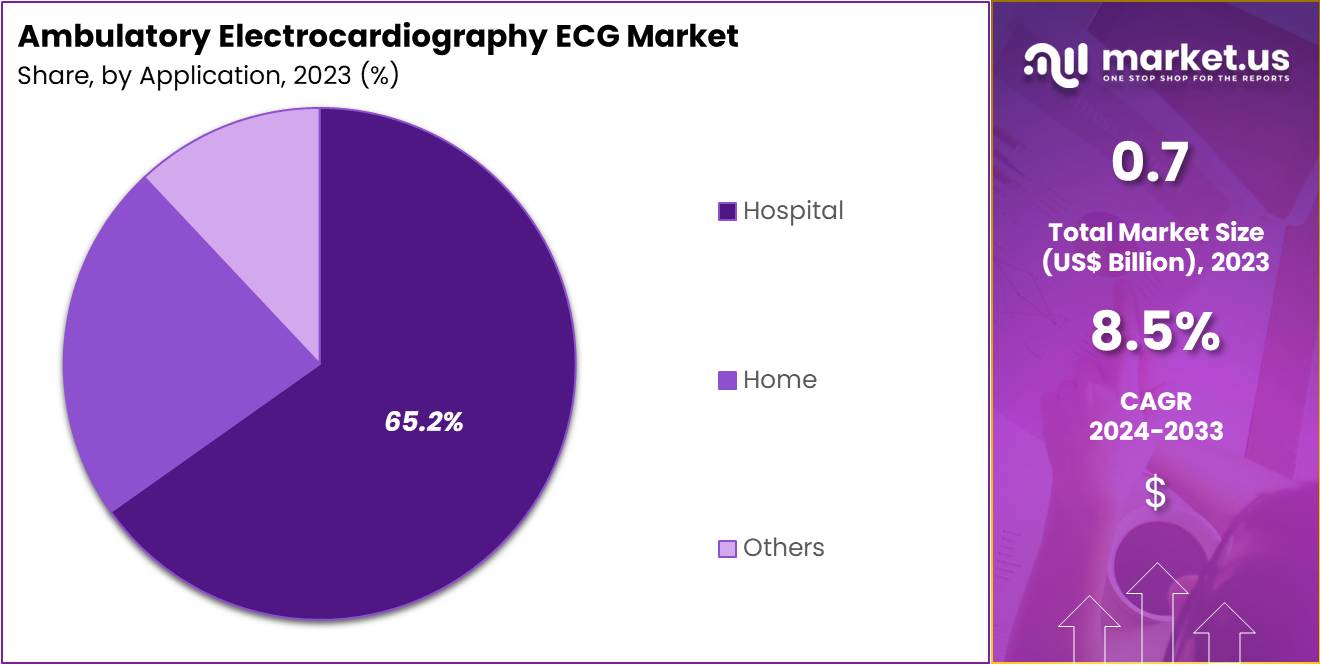

- Considering application, the market is divided into hospital, home, and others. Among these, hospital held a significant share of 65.2%.

- North America led the market by securing a market share of 39.4% in 2023.

Product Type Analysis

The portable segment led in 2023, claiming a market share of 56.7% owing to increasing demand for user-friendly, on-the-go monitoring solutions. Portable ECG devices offer greater convenience for patients and healthcare providers by enabling real-time monitoring outside of clinical settings. These devices are anticipated to become more prevalent as healthcare systems focus on remote patient monitoring and preventative care.

With the growing preference for mobile health (mHealth) solutions, the portable ECG segment is likely to benefit from technological advancements that improve the accuracy, battery life, and connectivity of these devices. The rise in chronic conditions such as heart disease and hypertension, which require continuous monitoring, is expected to further drive the demand for portable ECG devices. Additionally, as patients seek more flexibility and ease of use in managing their health, portable ECG devices are projected to gain wider acceptance in both home and clinical settings.

Application Analysis

The hospital held a significant share of 65.2% due to hospitals increasingly adopting advanced monitoring technologies to improve patient outcomes. Hospitals are expected to integrate ambulatory ECG systems to enhance the efficiency of diagnosing heart-related conditions, reduce in-hospital patient load, and improve early detection of arrhythmias or other cardiovascular issues.

The growing need for continuous monitoring of critical patients is anticipated to be a key driver for this segment. As healthcare providers focus on patient-centered care and the early diagnosis of cardiovascular diseases, the demand for ambulatory ECG systems in hospitals is likely to expand.

Additionally, hospitals are expected to adopt these systems to improve workflow efficiency and reduce healthcare costs by enabling remote monitoring of patients in a more flexible manner. The increasing healthcare infrastructure in emerging markets is also expected to contribute to the growth of this segment.

Key Market Segments

By Product Type

- Portable

- Patch

- Other

By Application

- Hospital

- Home

- Others

Drivers

Growing Prevalence of Cardiovascular Diseases Driving the Market

Growing prevalence of cardiovascular diseases (CVD) is significantly driving the ambulatory electrocardiography (ECG) market. The increasing number of individuals diagnosed with heart-related conditions has intensified the demand for continuous monitoring solutions to assess cardiac health outside of traditional hospital settings.

According to the National Institutes of Health, approximately 330 million individuals in China suffer from CVD, with many more at risk due to factors such as smoking, obesity, and physical inactivity. This surge in CVD cases is likely to increase the need for portable, efficient ECG devices to monitor patients in outpatient settings, offering early detection of arrhythmias and other cardiac abnormalities.

As awareness of cardiovascular health grows, patients and healthcare providers are expected to seek out ambulatory ECG solutions for long-term monitoring, creating a favorable environment for market expansion. Advances in ECG technology, alongside the rising demand for preventive healthcare, will further contribute to the market’s growth.

Restraints

Rising Limited Reimbursement and Insurance Coverage Restraining the Market

Rising concerns over limited reimbursement and insurance coverage are expected to restrain the growth of the ambulatory electrocardiography (ECG) market. High costs associated with continuous ECG monitoring devices could impede adoption, especially in regions where insurance plans provide minimal reimbursement for these diagnostic tools. Many patients may find it difficult to afford out-of-pocket expenses for long-term ECG monitoring, limiting market penetration.

The lack of standardized reimbursement policies for ambulatory ECG systems is likely to hamper the willingness of healthcare providers to invest in such technologies. As reimbursement structures remain restrictive, especially in emerging markets, the adoption of these systems is projected to face barriers. This constraint could slow down the adoption of ambulatory ECG devices, particularly in lower-income demographics where access to advanced healthcare technologies is already limited.

Opportunities

Increasing Integration of AI Presents Opportunity for the Market

Increasing integration of artificial intelligence (AI) presents a significant opportunity for growth in the ambulatory electrocardiography (ECG) market. AI technologies enable enhanced diagnostic accuracy, faster data analysis, and more reliable predictions, which are crucial for real-time monitoring of heart conditions. In June 2024, AliveCor unveiled the Kardia 12L ECG System along with its KAI 12L AI technology after receiving FDA approval.

This breakthrough system is the first of its kind to detect serious heart conditions, such as heart attacks, using a compact lead set. By integrating AI with portable ECG devices, AliveCor’s Kardia 12L provides accurate diagnostic results in a more efficient and accessible format. The ability to leverage AI for early detection of arrhythmias and other cardiac abnormalities is expected to drive demand for ambulatory ECG systems.

As AI continues to evolve, these innovations are likely to enhance the capabilities of portable ECG devices, making them an essential tool for healthcare providers and patients. The increasing use of AI in diagnostic systems will create a favorable environment for the market’s growth, particularly as healthcare professionals embrace more sophisticated, data-driven solutions.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors significantly influence the ambulatory electrocardiography (ECG) market. Economic slowdowns or recessions often result in tighter healthcare budgets, which can limit the affordability and adoption of advanced diagnostic tools, including ECG devices. Conversely, rising healthcare expenditure in emerging economies boosts market demand as more patients gain access to diagnostic services.

Geopolitical tensions and trade restrictions can disrupt supply chains, delaying product availability or increasing costs for manufacturers. On the positive side, advancements in healthcare infrastructure, particularly in developing nations, are expected to drive demand for portable and efficient diagnostic solutions. As technology continues to improve, ambulatory ECG systems are likely to play a key role in remote patient monitoring, contributing to long-term market growth.

Trends

Rising Partnerships and Collaborations Driving the Ambulatory ECG Market

Rising partnerships and collaborations are driving growth in the ambulatory electrocardiography (ECG) market. High demand for advanced ECG solutions has led to increased cooperation among healthcare technology companies, aiming to expand their portfolios and reach more customers. These collaborations often focus on integrating artificial intelligence (AI) and machine learning with ECG devices, enhancing diagnostic accuracy and ease of use.

In May 2024, OMRON Healthcare India formed a strategic partnership with AliveCor India, introducing AI-powered portable ECG technology. This collaboration enables OMRON to enhance its offerings in India, further expanding its leadership in the market for blood pressure monitors while tapping into the growing demand for advanced cardiac monitoring. The trend of strategic alliances is expected to accelerate innovation and broaden the availability of cutting-edge ambulatory ECG solutions.

Regional Analysis

North America is leading the Ambulatory Electrocardiography ECG Market

North America held the highest revenue share of 39.4% in the ambulatory ECG market. This dominance is attributed to the growing adoption of wearable cardiac monitoring devices and advancements in telemedicine. A key milestone in the region was HeartBeam, Inc.’s secondary offering in May 2023, which raised $23.2 million. This funding supports the development of advanced ECG systems like HeartBeam AIMIGo, slated for commercialization in 2024. The system reflects the shift toward accessible and patient-friendly cardiac care solutions, meeting the needs of evolving healthcare systems.

The rising prevalence of cardiovascular diseases, coupled with an aging population, has fueled demand for continuous heart health monitoring. Patients increasingly seek real-time solutions outside traditional clinical settings. Mobile health technologies and cloud-based analytics are enhancing the accuracy and usability of ambulatory ECG systems. These advancements simplify cardiac monitoring for both patients and healthcare providers. The convenience of remote monitoring ensures better disease management and early detection of critical conditions.

Healthcare systems across North America are focusing on remote monitoring and early diagnosis. This trend supports the expansion of ambulatory ECG solutions. Real-time monitoring tools reduce hospital visits and improve patient outcomes. Cloud-enabled technologies streamline data collection and analysis, making systems more efficient. Such advancements are reshaping cardiac care, offering greater convenience for patients. As a result, the ambulatory ECG market is expected to grow significantly in the coming years, driven by innovation and increasing healthcare priorities.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to The ambulatory ECG market in Asia Pacific is projected to experience strong growth during the forecast period. The increasing burden of cardiovascular diseases across countries like India and China, combined with improving healthcare infrastructure, is expected to drive demand for advanced diagnostic tools. In particular, wearable ECG devices are anticipated to see wide adoption due to their convenience and effectiveness in remote patient monitoring.

As public health awareness grows, particularly in urban areas, the demand for cost-effective and non-invasive monitoring solutions is likely to rise. Countries in the region, such as Japan, have already made significant strides in integrating telemedicine into their healthcare systems, which will further enhance the adoption of ambulatory ECG technologies. Additionally, collaborations between healthcare providers and technology firms are expected to accelerate innovation and improve accessibility to high-quality cardiovascular care in the region.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The ambulatory electrocardiography (ECG) market is driven by major players focusing on innovative product development and strategic initiatives. Companies prioritize technological advancements to enhance their competitive positioning. The development of portable, wireless, and high-precision ECG devices has improved diagnostic accuracy and patient convenience. These devices enable continuous monitoring outside traditional healthcare settings, meeting the growing demand for real-time heart health monitoring. Such innovations align with the market’s shift toward patient-centric solutions and ensure better disease management and early detection.

Key players emphasize integrating advanced software and AI algorithms into their devices. These technologies allow for real-time data analysis and predictive insights, supporting early detection of cardiac conditions. AI-powered platforms also improve the efficiency of data interpretation for healthcare providers. By embedding intelligent software into ECG systems, companies deliver superior diagnostic capabilities. These advancements enhance the usability of ambulatory ECG devices for both clinicians and patients, fostering growth in this rapidly evolving market.

Strategic partnerships play a crucial role in expanding market reach. Collaborations with hospitals, clinics, and research institutions drive the adoption of ambulatory ECG solutions. Companies also target emerging markets with cost-effective and user-friendly devices for remote monitoring. These efforts support the broader accessibility of advanced ECG technologies worldwide. By focusing on affordability and scalability, players in the market address the needs of diverse healthcare systems while capitalizing on untapped growth opportunities.

Philips Healthcare is a prominent player in the ambulatory ECG market. Its Philips IntelliVue ECG system supports remote monitoring with high-quality data analysis. The company integrates artificial intelligence and cloud-based platforms into its devices, enhancing data management and decision-making processes. Philips also invests in research and partnerships with healthcare providers to improve product functionality and accuracy. By promoting telemedicine solutions and expanding its global presence, Philips remains at the forefront of the ambulatory ECG market, delivering advanced and reliable diagnostic solutions.

Top Key Players in the Ambulatory Electrocardiography ECG Market

- Spacelabs Healthcare

- Philips Healthcare

- Nihon Kohden

- Mindray Medical

- iRhythm Technologies, Inc.

- Hill-Rom

- GE Healthcare

- Dozee

- Compumed

Recent Developments

- In October 2023, Dozee partnered with Wellysis, a spin-off of Samsung’s SDS Digital Health division, to introduce the FDA-approved S-Patch Ex ECG monitoring system for ambulatory use. This device, which includes a wireless ECG patch for continuous heart rhythm tracking, is coupled with an advanced analytical platform for real-time data processing.

- In August 2024, iRhythm Technologies, Inc. launched its Zio monitor and long-term continuous ambulatory monitoring ECG service in Austria, Spain, the Netherlands, and Switzerland. This expansion offers patients and healthcare providers in these regions enhanced access to accurate and continuous heart rhythm monitoring solutions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | US$ 0.7 billion |

| Forecast Revenue (2033) | US$ 1.6 billion |

| CAGR (2024-2033) | 8.5% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Portable, Patch, and Others), By Application (Hospital, Home, and Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Spacelabs Healthcare, Philips Healthcare, Nihon Kohden, Mindray Medical, iRhythm Technologies, Inc., Hill-Rom, GE Healthcare, Dozee, and Compumed. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |