Quick Navigation

Report Overview

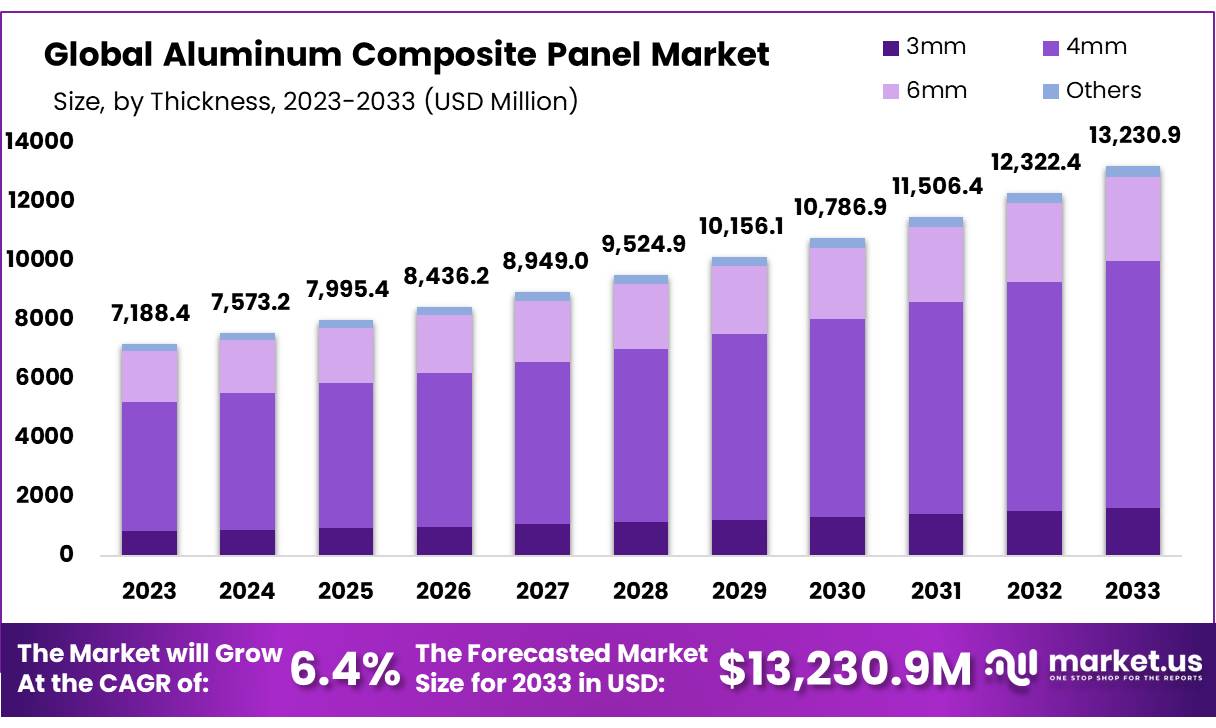

The Global Aluminum Composite Panel (ACP) Market size is expected to be worth around USD 13,230.9 Million by 2033, from USD 7,188.4 Million in 2023, growing at a CAGR of 6.4% during the forecast period from 2024 to 2033.

The Aluminum Composite Panel (ACP) market has seen substantial growth in recent years, driven by its extensive applications in the construction, transportation, and advertising industries. Aluminum composite panels consist of two thin layers of aluminum enclosing a non-aluminum core, which offers a combination of lightweight, durability, and aesthetic flexibility.

These panels are widely used in the construction of building facades, interior decoration, and signage due to their superior strength-to-weight ratio, weather resistance, and wide range of surface finishes.

ACPs are especially popular in modern architecture, where they are used to create sleek, contemporary designs that offer both functional and decorative benefits.

The global aluminum composite panel (ACP) market has seen substantial growth in recent years, driven by its widespread use in the construction industry, particularly in facade and cladding applications. The ACP market is projected to continue growing at a strong pace due to increasing demand for modern architectural solutions, urbanization, and a rising focus on sustainability.

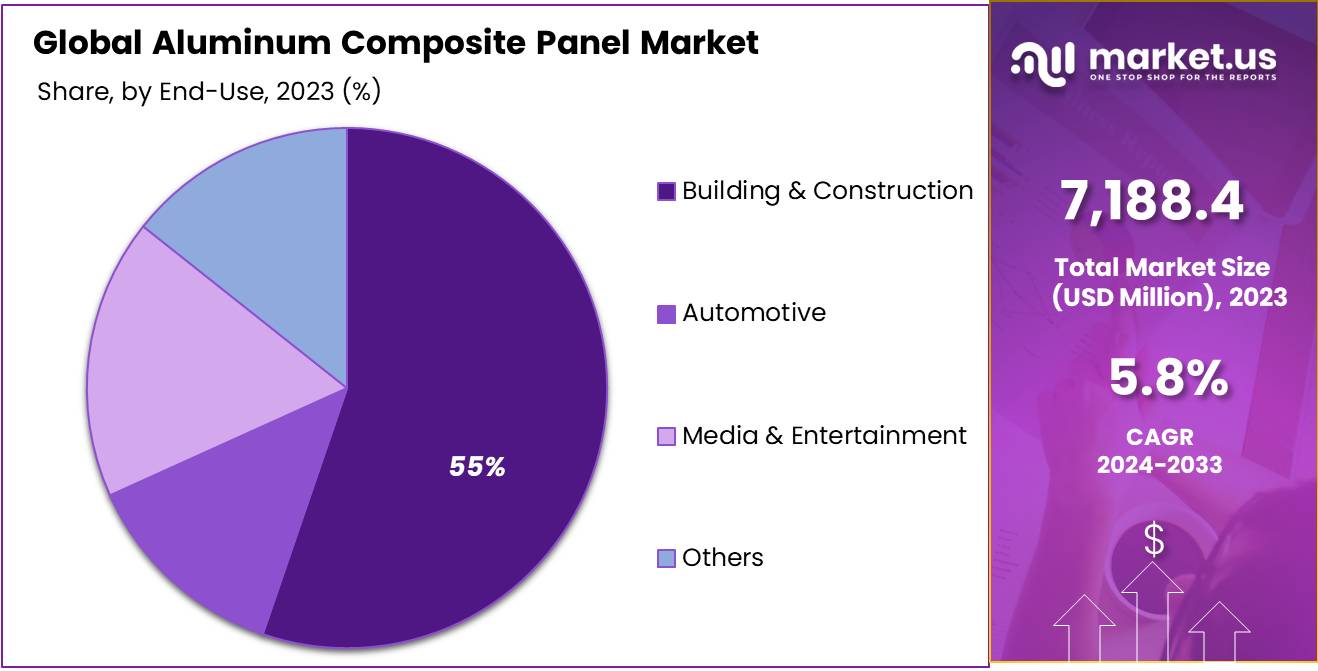

The global Aluminum Composite Panel (ACP) market continues to grow, with the construction industry being the largest end-user, accounting for approximately 50-55% of the demand in 2023. ACPs are primarily used in residential and commercial building projects, particularly for facades, walls, and interior applications.

The transportation sector, including automotive and public transport, represents about 15-20% of the market. Other industries such as signage and advertising contribute roughly 10-15%, while retail and interior applications make up the remainder of the market share.

Governments across the world are actively supporting the adoption of ACPs through various initiatives. In India, the Smart Cities Mission, with a budget of USD 15 billion for urban development, is allocating a portion of the funds to modernizing construction infrastructure using sustainable and fire-resistant materials like ACPs.

The European Union’s Green Deal and Circular Economy Action Plan have also encouraged the use of recyclable building materials, further driving the development of ACPs with improved sustainability features.

In 2023, the global export value of ACPs was approximately USD 4.5 billion. China led the market, contributing 40-45% of the global ACP trade, with exports valued at around USD 2 billion. India followed with USD 750 million in exports, mainly driven by demand from the Middle East and Africa. The European Union’s ACP exports were valued at around USD 500 million, with Germany and Italy being the key exporters.

Investments in ACP-related technologies and innovation reached over USD 350 million in 2023, with the majority directed towards enhancing the fire resistance and environmental sustainability of ACPs. Companies like Alubond USA and Arconic have made significant investments in R&D. In 2023, Alubond USA partnered with Alucoil, investing USD 50 million to expand its North American production capacity.

The trend of innovation continues with partnerships and acquisitions in the market. In 2023, Arconic entered a partnership with Kingspan Group to develop a new range of fire-resistant ACPs, investing USD 100 million. Alumax Industrial also acquired Metalbond to strengthen its presence in the U.S. market, focusing on sustainable ACP solutions. This merger is expected to generate USD 250 million in additional revenue by 2025.

Key Takeaways

- The global Aluminum Composite Panel (ACP) market was valued at US$ 7,188.4 million in 2023.

- The global Aluminum Composite Panel (ACP) market is projected to reach US$ 13,230.9 million by 2033.

- Among thickness, the 4mm thickness of aluminum composite panels held the majority of the revenue share at 61.2%.

- Among coating types, the Polyvinylidene Fluoride coating type of aluminum composite panels held the majority of the revenue share at 34.5%.

- Among categories, the fire retardant type of aluminum composite panels held the majority of the revenue share at 68.5%.

- Among these end-uses, building & construction accounted for the majority of the market share with 55.3%.

Thickness Analysis

ACPs with 4mm Thickness is Majorly Used Due To Its Affordability

The Aluminum Composite Panel (ACP) market is segmented based on thickness into 3mm, 4mm, 6mm, and others. Among these, the 4mm held the majority of revenue share in 2023, with a market share of 61.2%. The 4mm ACP panels are often more affordable than thicker alternatives, such as 6mm panels.

This price advantage makes them attractive to contractors, architects, and developers, particularly in price-sensitive markets, without sacrificing the strength and aesthetic appeal needed for most building facades. Over time, 4mm ACP panels have become an industry standard, leading to widespread adoption.

As a result, manufacturers and suppliers have optimized their production lines to meet the higher demand for 4mm panels, contributing to broader availability and lower prices. This has reinforced its dominance in the market.

Coating Type Analysis

Polyvinylidene Fluoride (PVDF) Coatings Are Suitable For Outdoor Applications and Have Resistance To Weathering Which Makes It a Popular Choice Among End-Users

The Aluminum Composite Panel (ACP) market is segmented based on coating type into polyester, polyvinylidene fluoride, polyethylene, laminating coating, oxide film, and others. Among these, the 4mm held the majority of revenue share in 2023, with a market share of 34.5%. PVDF coatings are known for their exceptional resistance to weathering, UV degradation, and environmental factors.

This makes them particularly suitable for outdoor applications where long-term exposure to harsh climates, pollution, and extreme temperatures can otherwise degrade the quality of materials. PVDF-coated ACPs maintain their color and finish for extended periods, which is a key requirement in building facades and exterior cladding.

The longevity and low maintenance requirements of PVDF-coated panels make them a cost-effective solution in the long run. Their resistance to fading, staining, and dirt accumulation reduces the need for frequent cleaning or re-coating, which appeals to building owners and developers looking for durable, low-maintenance solutions.

Category Analysis

Fire Retardant Aluminum Composite Panels Held Majority Of Revenue Share

The Aluminum Composite Panel (ACP) market is segmented based on category into fire retardant, anti-static, and anti-bacterial. Among these, the fire retardant held the majority of revenue share in 2023, with a market share of 68.5%.

The primary driver for the dominance of fire retardant ACPs is the increasing enforcement of building safety codes and fire regulations globally. In many countries, particularly in high-rise buildings, commercial structures, and public infrastructure, building codes now mandate the use of fire-resistant materials to prevent the spread of fire and protect lives and property.

Fire retardant ACPs help meet these stringent regulatory requirements, ensuring compliance with safety standards, which is a significant factor in their widespread adoption. The demand for fire-resistant materials has been steadily increasing as safety concerns become more prominent in the construction and architecture sectors.

High-profile fire incidents in buildings, especially those involving flammable cladding materials, have led to heightened awareness of the importance of fire safety. As a result, architects, developers, and building owners are prioritizing the use of fire retardant materials in new projects to mitigate risks, prevent potential hazards, and reduce insurance costs.

End-Use Analysis

Building & Construction Are the Major End-Users of Aluminum Composite Panel (ACP) Market

Based on end-uses, the market is segmented into building & construction, automotive, media and entertainment, and others. Among these end-uses, building & construction accounted for the majority of the market share with 55.3% due to several compelling factors that make ACPs particularly well-suited for applications within this industry. ACP panels are increasingly favored for their aesthetic appeal and durability, both of which are highly valued in the building and construction sector.

ACPs provide a sleek, modern appearance with a wide variety of finishes, colors, and textures, making them ideal for exterior facades, curtain walls, and architectural cladding. As design aesthetics have become a critical part of building projects, especially in commercial and high-rise residential structures, ACPs are increasingly specified by architects and designers.

The construction of commercial buildings, office complexes, shopping malls, hotels, and residential skyscrapers has driven the demand for ACPs in the building and construction industry. ACPs offer a lightweight, cost-effective alternative to traditional materials such as brick, stone, or solid metal panels, while also delivering superior thermal insulation and acoustic properties.

These benefits make ACPs an attractive solution for large-scale, high-performance building projects, both in urban centers and expanding suburban developments.

Key Market Segments

By Thickness

- 3mm

- 4mm

- 6mm

- Others

By Coating Type

- Polyester

- Polyvinylidene Fluoride

- Polyethylene

- Laminating Coating

- Oxide Film

- Others

By Category

- Fire Retardant

- Anti-static

- Anti-Bacterial

By End-Use

- Building & Construction

- Automotive

- Media & Entertainment

- Others

Drivers

Growing Focus on Sustainable Building Materials Is Anticipated to Boost the Market’s Growth

The growing focus on sustainable building materials is poised to significantly boost the Aluminum Composite Panel (ACP) market’s growth, driven by increasing demand for eco-friendly and energy-efficient construction solutions. As global construction practices shift towards sustainability, the building industry is prioritizing materials that minimize environmental impact while enhancing energy performance.

ACPs, particularly those with fire-retardant and insulated cores, offer excellent thermal insulation properties, which contribute to reducing the overall energy consumption of buildings.

By improving heat retention and minimizing the need for heating and cooling, ACPs help create energy-efficient buildings, a key objective in green building certification programs such as LEED (Leadership in Energy and Environmental Design). This makes ACPs an attractive option for architects and developers seeking to meet stringent energy performance standards.

Moreover, ACPs are made from recyclable materials, which align with the growing demand for circular economy principles in construction. The use of aluminum in ACPs, a highly recyclable material, supports sustainability initiatives by reducing resource depletion and encouraging material reuse at the end of the product’s lifecycle.

The lightweight nature of ACPs further contributes to reducing carbon footprints during transportation and installation, as less energy is required for handling and logistics compared to traditional building materials such as stone or concrete.

In addition to energy efficiency, the durability and long lifespan of ACPs—resistant to weathering, corrosion, and UV degradation—further enhance their appeal as sustainable construction materials. Buildings using ACPs require less frequent maintenance, leading to lower long-term environmental costs.

As governments and regulatory bodies tighten environmental standards and demand more sustainable building solutions, the adoption of ACPs is expected to increase, particularly in regions with ambitious sustainability goals.

Consequently, ACPs’ ability to meet environmental, regulatory, and performance standards will play a pivotal role in accelerating their adoption within the sustainable building materials market, ultimately driving the growth of the ACP market in the coming years.

Restraints

The Availability of Alternative Materials May Hinder the Growth of The ACPs

The availability of alternative materials presents a potential challenge to the growth of the Aluminum Composite Panel (ACP) market, as builders, architects, and developers are increasingly exploring other options for cladding and building facades. Several materials, such as fiberglass-reinforced panels (FRP), high-pressure laminates (HPL), stone, ceramic tiles, and glass, offer competing advantages that may impact ACP adoption.

For instance, materials such as HPL and FRP are known for their superior impact resistance and abrasion durability, which can be particularly appealing in high-traffic or industrial applications. While ACPs are valued for their aesthetic flexibility and ease of installation, alternative materials may offer superior performance in specific areas, such as fire resistance or weathering properties, which could limit ACPs’ appeal in certain markets.

In regions with particularly stringent fire safety standards, materials like ceramic tiles or stone may be preferred for their inherent non-combustibility, posing a direct challenge to the widespread adoption of fire-retardant ACPs.

Furthermore, some alternative materials, such as glass or fiber cement panels, provide a more premium aesthetic or greater design flexibility, allowing architects to experiment with different forms and textures.

These alternatives can provide a competitive edge for developers aiming for unique building facades or high-end, high-visibility projects. While ACPs offer aesthetic versatility, their design limitations—particularly regarding transparency or intricate shaping—might drive some projects towards these alternatives, especially in areas where design innovation is prioritized.

The cost competitiveness of alternative materials also plays a role in hindering ACP growth. Materials such as fiber cement can sometimes be more affordable, offering similar aesthetic qualities at a lower price point, especially for large-scale residential developments. As construction projects become increasingly cost-conscious, price-sensitive clients may opt for these alternatives, particularly in low-cost or emerging markets.

In summary, while ACPs remain a preferred choice in many segments, the availability of high-performance, aesthetically versatile, and often more affordable alternatives may slow the growth of the ACP market by diverting demand toward competing materials.

Opportunity

Innovation in Fire-Resistant Materials May Create Lucrative Opportunities For Emerging Manufacturers

Innovation in fire-resistant materials is expected to create significant opportunities for emerging manufacturers in the Aluminum Composite Panel (ACP) market, particularly as demand for safer and more durable building materials continues to rise.

As building codes around the world become more stringent, particularly in fire safety regulations, the need for advanced, fire-resistant ACPs is growing. Innovations that enhance the fire-resistant properties of ACPs, such as the development of non-combustible cores or advanced fire-retardant coatings, present a competitive advantage for emerging manufacturers seeking to differentiate themselves in an increasingly regulated market.

These innovations allow manufacturers to meet the stringent safety standards required for high-rise buildings, commercial complexes, and public infrastructure projects where fire safety is a top priority.

For emerging manufacturers, developing and introducing next-generation fire-resistant ACPs opens up lucrative market segments, particularly in regions with high demand for fire-safe construction materials. With increasing public awareness of fire hazards, coupled with growing concerns over high-profile fire incidents, there is a significant push from both the private and public sectors to adopt building materials that provide enhanced fire protection.

Manufacturers who can introduce more affordable, effective, and sustainable fire-resistant ACP solutions will be able to capture a larger share of this expanding market. Additionally, advancements in fire resistance are often accompanied by improvements in other performance characteristics such as thermal insulation, durability, and weather resistance, allowing emerging manufacturers to tap into a broader range of applications.

Fire-resistant ACPs that combine these attributes are particularly attractive to architects and developers involved in the construction of commercial buildings, hospitals, and schools, where safety concerns are paramount. Emerging manufacturers can also explore opportunities in sustainability-focused construction projects, where fire-resistant materials that are recyclable and energy-efficient are increasingly sought after.

Trends

Integration with Smart Technology

The integration of smart technology with Aluminum Composite Panel (ACPs) Market is emerging as a significant trend, driven by the increasing demand for smart buildings and intelligent architectural solutions. As the construction industry moves toward more advanced and connected environments, ACPs are being incorporated into smart façades that enhance building performance, energy efficiency, and user experience.

One key example of this integration is the development of solar panels embedded into ACPs or the inclusion of electrochromic coatings, which enable the panels to change color or opacity in response to environmental conditions, such as sunlight. This feature not only contributes to aesthetic appeal but also optimizes solar energy absorption, improving the building’s energy efficiency.

Moreover, ACPs are now being integrated with smart sensors that monitor and respond to factors like temperature, humidity, air quality, and light levels, which can adjust building systems such as heating, ventilation, and air conditioning (HVAC). This integration enables buildings to become more energy-efficient by automatically adjusting settings based on real-time data, reducing energy waste, and contributing to the overall sustainability of the structure.

In addition, the integration of smart glazing systems with ACPs offers advanced control over natural lighting and heat gain, optimizing both comfort and energy usage. As urban spaces evolve, these technologies enhance the user experience by creating dynamic, adaptable building envelopes that respond to both environmental and occupant needs.

With the growing trend toward smart cities and the increasing adoption of IoT (Internet of Things) devices, the integration of smart technologies in ACPs is expected to gain further traction. This convergence not only enhances the functionality of ACPs but also positions them as a crucial element in the next generation of sustainable and intelligent architecture, driving market demand and innovation in the building sector.

Geopolitical Impact Analysis

Geopolitical Tensions Significantly Impacted the Growth of the Aluminum Composite Panel (ACP) Market

Western European countries, such as Germany, were significantly dependent on Russian aluminum imports to meet their domestic needs. As a result, they are now experiencing supply shortages and elevated prices. Already struggling with an energy crisis and economic recession, the disruption in aluminum supply has intensified the strain on Europe’s industries.

In 2021, Russia produced approximately 3.76 million tons of aluminum, accounting for a substantial share of the global supply. The European Union, heavily reliant on imports to meet its aluminum demand, has been negatively impacted by geopolitical and logistical challenges, leading to a decline in both Russian aluminum production and European manufacturing output. One of the most immediate and profound effects of the Russia-Ukraine war has been the disruption of global supply chains.

Russia is a major global supplier of aluminum, a key raw material in the production of ACPs. As sanctions were imposed on Russia by Western countries, the supply of aluminum was severely constrained. This had a ripple effect throughout the aluminum industry, raising prices and creating shortages. Companies manufacturing ACPs faced increased costs for aluminum, which in turn pushed up the price of ACP products.

In early 2022, when the war began, the immediate impact was felt in the European markets, which are significant consumers of ACP for infrastructure and construction projects. Many European ACP manufacturers found themselves scrambling for alternative aluminum suppliers, resulting in delays in production and increased costs.

Additionally, sanctions on Russian industries disrupted the availability of aluminum and other metals, forcing manufacturers to explore alternative suppliers from regions such as China, India, and Australia. However, this shift increased transportation costs and led to a significant rise in lead times for raw materials.

Regional Analysis

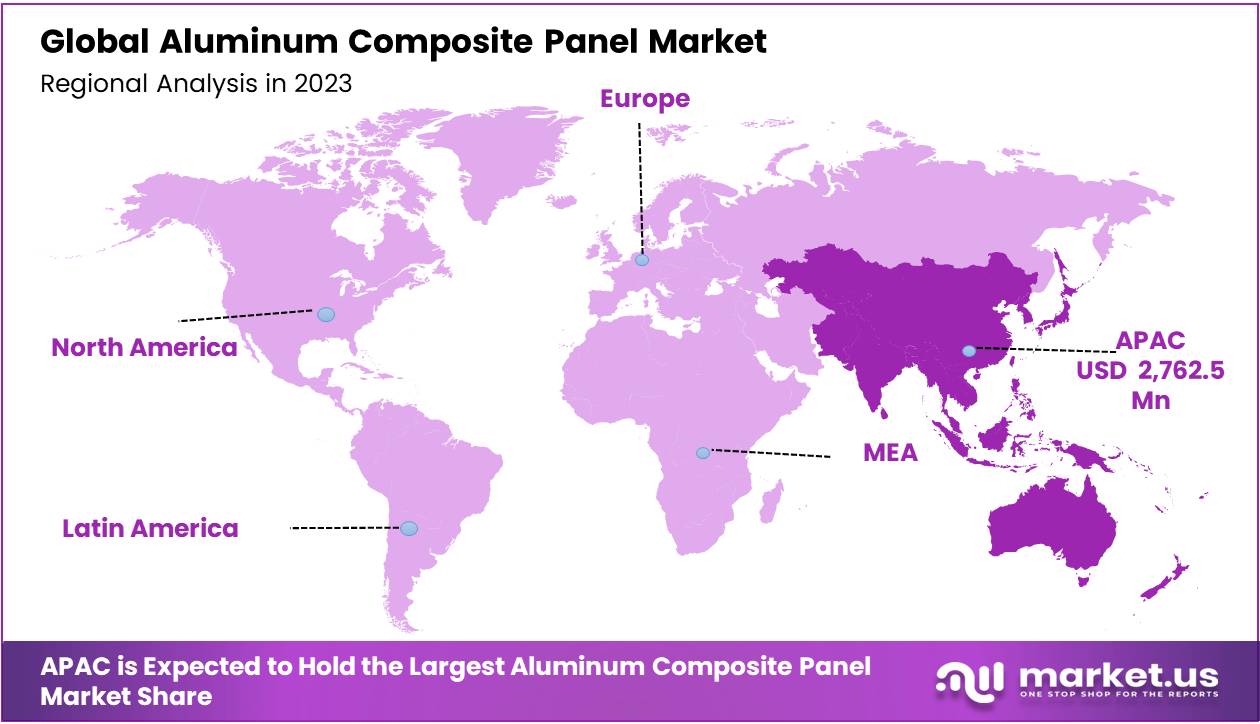

Asia-Pacific Dominated The Market Among Other Regions Owing to Their Strong Focus on Strategic Energy Policies

In 2023, Asia-Pacific held the largest market share of Aluminum Composite Panel (ACP) with 38.4%. The integration of smart technology with Aluminum Composite Panels (ACPs) is emerging as a significant trend, driven by the increasing demand for smart buildings and intelligent architectural solutions. As the construction industry moves toward more advanced and connected environments, ACPs are being incorporated into smart façades that enhance building performance, energy efficiency, and user experience.

One key example of this integration is the development of solar panels embedded into ACPs or the inclusion of electrochromic coatings, which enable the panels to change color or opacity in response to environmental conditions, such as sunlight. This feature not only contributes to aesthetic appeal but also optimizes solar energy absorption, improving the building’s energy efficiency.

Moreover, ACPs are now being integrated with smart sensors that monitor and respond to factors like temperature, humidity, air quality, and light levels, which can adjust building systems such as heating, ventilation, and air conditioning (HVAC). This integration enables buildings to become more energy-efficient by automatically adjusting settings based on real-time data, reducing energy waste, and contributing to the overall sustainability of the structure.

In addition, the integration of smart glazing systems with ACPs offers advanced control over natural lighting and heat gain, optimizing both comfort and energy usage. As urban spaces evolve, these technologies enhance the user experience by creating dynamic, adaptable building envelopes that respond to both environmental and occupant needs.

With the growing trend toward smart cities and the increasing adoption of IoT (Internet of Things) devices, the integration of smart technologies in ACPs is expected to gain further traction. This convergence not only enhances the functionality of ACPs but also positions them as a crucial element in the next generation of sustainable and intelligent architecture, driving market demand and innovation in the building sector.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Market Players In The Aluminum Composite Panel (ACP) Industry Are Evolving Through Various Strategies To Maintain Their Dominance.

Leading ACP manufacturers are heavily investing in product innovation to cater to the diverse needs of their clients and to keep up with evolving architectural trends. This includes the development of fire-retardant ACPs, eco-friendly materials, lightweight panels, and smart ACPs integrated with solar technologies or electrochromic coatings.

These innovations not only differentiate product offerings but also align with the growing demand for sustainable, energy-efficient, and technologically advanced materials. By diversifying their product portfolios, market players can serve a wider range of applications, from residential and commercial buildings to high-end infrastructure projects.

In a competitive market, companies are placing significant emphasis on brand differentiation and marketing strategies. By focusing on strong brand identities, companies highlight their commitment to quality, innovation, and sustainability.

Trade shows, industry events, and digital marketing platforms (e.g., websites, and social media) are leveraged to increase brand visibility and engage with potential customers. Educating consumers about the advantages of ACPs, particularly in terms of fire safety, energy efficiency, and aesthetics, is central to these marketing efforts.

Market Key Players

- Arconic Architectural Products

- Mitsubishi Chemical Group Corporation

- Alstone

- Fairfield Metal

- Shanghai Yaret Industrial Group Co., Ltd.

- 3A Composites

- Alubond USA

- Alumax Industrial Co., Ltd.

- Jyi Shyang Industrial Co., Ltd

- Shanghai Huayuan New Composite Materials

- Alstrong Enterprises India (Pvt) Ltd

- Qatar National Aluminum Panel Company

- Eurobond

- Sykon GmbH

- Aludecor

- Other Key Players

Recent Development

- In July 2024, 3A Composite announced their new surface coating under creative façade design for alucobond panels these new developments from 3a composites ACP Panels are available in 3 Brand New Colors Signal White (111), Moss Green (317) and Grey Brown (337), which offer design freedom for architecture in construction projects. These surface coatings are impressive for their aesthetics and durability.

- In September 2023, The Mitsubishi Chemical Group signed an agreement with the Japanese Windsurfing Association to jointly promote recycling activities for carbon fiber and other metal composites used in windsurfing equipment. In addition, MCG group and JWA Focus on development applications for recycled products and promote the knowledge gained through these activities to society.

Report Scope

| Report Features | Description |

| Market Value (2023) | US$ 7,188.4 Mn |

| Market Volume (KT) | XX |

| Forecast Revenue (2033) | US$ 13,230.9 Mn |

| CAGR (2024-2032) | 6.4% |

| Base Year for Estimation | 2023 |

| Historic Period | 2020-2023 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Structure Type (Pure Acrylic, and Modified Acrylic), By End-Use (Commercial Spaces, Hotels & Restaurants, Healthcare & Medical Facilities, Residential, Public Buildings, and Others |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Arconic Architectural Products, Mitsubishi Chemical Group Corporation, Alstone , Fairfield Metal, Shanghai Yaret Industrial Group Co., Ltd., 3A Composites, Alubond USA, Alumax Industrial Co., Ltd. yi Shyang Industrial Co., Ltd, Shanghai Huayuan New Composite Materials, Alstrong Enterprises India (Pvt) Ltd, Qatar National Aluminum Panel Company, Eurobond, Sykon GmbH, and Aludecor |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate User License (Unlimited User and Printable PDF) |

Market")