Quick Navigation

Report Overview

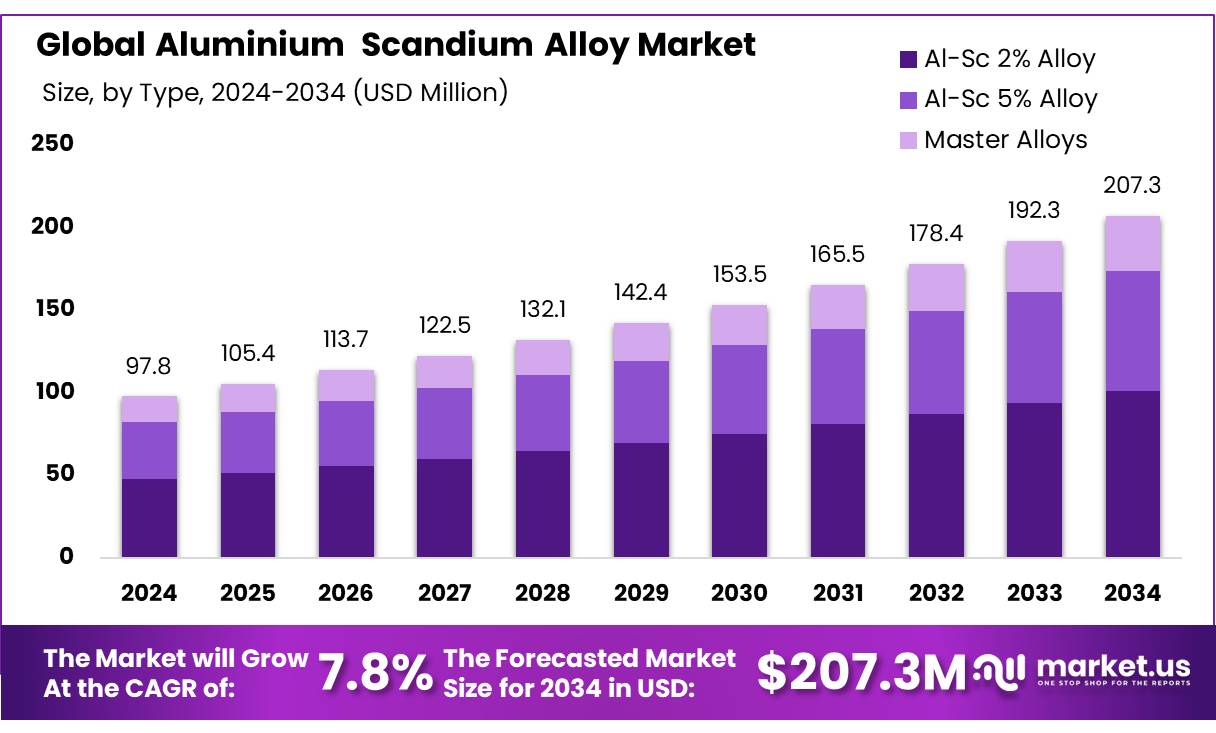

The Global Aluminium Scandium Alloy Market size is expected to be worth around USD 207.3 Mn by 2034, from USD 97.8 Mn in 2024, growing at a CAGR of 7.80% during the forecast period from 2025 to 2034.

Aluminum-scandium alloys are specialized materials composed of aluminum and small amounts of scandium. The incorporation of scandium significantly enhances the aluminum alloy’s mechanical properties, including its strength, weldability, and resistance to grain refinement, while maintaining its lightweight nature.

This combination of properties makes aluminum-scandium alloys particularly beneficial for high-performance applications. The alloys exhibit improved strength-to-weight ratios, enhanced corrosion resistance, and excellent performance in high-temperature environments. These characteristics make them ideal for industries such as aerospace, Transportation, Consumer Goods, and sports equipment manufacturing.

Aluminum-scandium alloy is widely applied across various industries due to its exceptional strength-to-weight ratio. In the aerospace industry, where weight reduction is crucial for fuel savings and enhanced performance. These alloys are used in aircraft structures such as fuselage components and wing panels, delivering strength and durability without adding unnecessary weight.

Additionally, in the sports industry, Sc-Al alloys are utilized to manufacture high-performance equipment, such as lightweight bicycle frames, which offer superior strength-to-weight ratios, helping competitive cyclists achieve faster speeds and improved performance. In the automotive industry, it’s utilized in engine blocks, chassis, and body panels to reduce vehicle weight, enhance performance, and meet environmental regulations. Furthermore, their corrosion-resistant properties are ideal for renewable energy infrastructure, including wind turbines and solar panel frames.

Key Takeaways

- The global aluminum scandium alloy market was valued at US$ 97.8 Million in 2024.

- The global aluminum scandium alloy market is projected to grow at a CAGR of 7.80% and is estimated to reach US$ 207.3 Million by 2034.

- Among types, Al-Sc 2% alloy accounted for the majority of the market share at 9%.

- By manufacturing process, casting accounted for the largest market share of 3%.

- By application, defense & aerospace accounted for the majority of the market share at 2%.

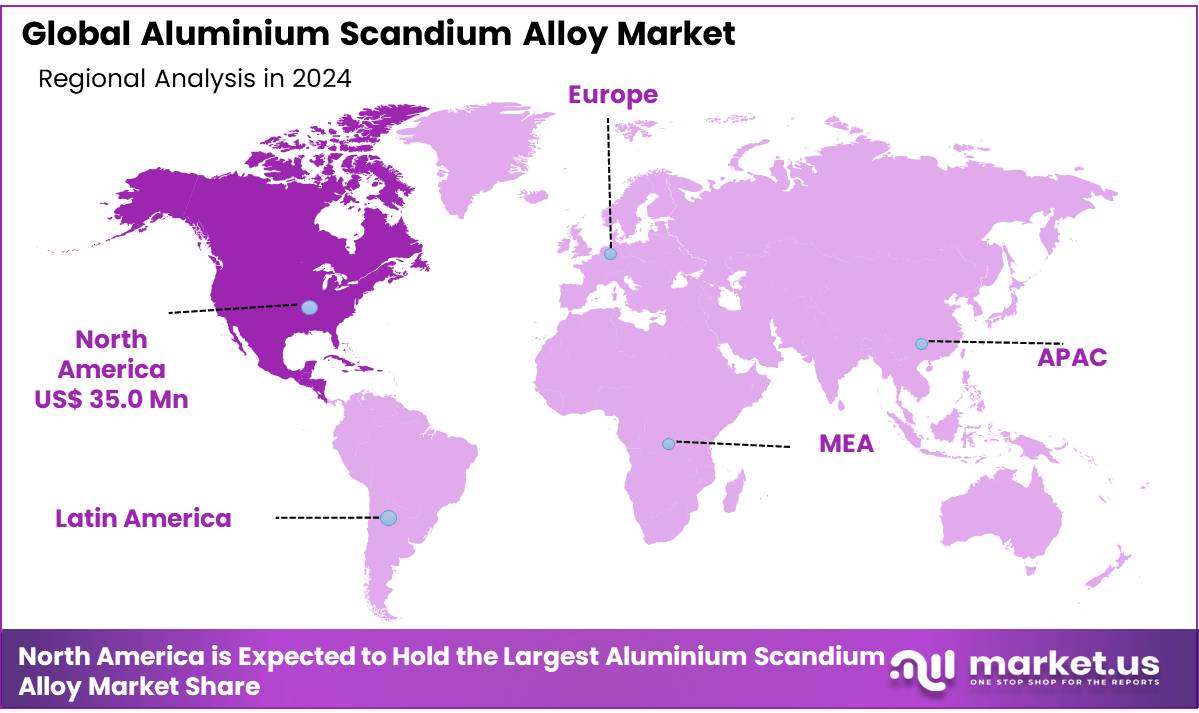

- North America is estimated as the largest market for aluminum scandium alloy with a share of 9 % of the market share.

Type Analysis

The aluminum scandium alloy market is segmented based on type into Al-Sc 2% Alloy, Al-Sc 5% Alloy and Master Alloys. In 2024, the type Al-Sc 2% alloy segment held a significant revenue share of 48.9%. Due to its widespread use in various industries, especially in aerospace and automotive applications. The Al-Sc 2% alloy offers a favorable balance of enhanced mechanical properties, such as increased strength and improved corrosion resistance, while maintaining cost-effectiveness compared to higher-concentration alloys. These advantages make it suitable for applications requiring lightweight, high-strength materials, without the high cost associated with higher scandium content alloys.

Furthermore, the Al-Sc 2% Alloy is often preferred in applications where the alloy’s properties meet the required specifications for performance. This has made the 2% alloy a preferred choice for industries focused on optimizing material costs while still achieving the desired performance. As industries like aerospace, automotive, and 3D printing continue to expand, the demand for Al-Sc 2% alloys is expected to grow, driving its significant market share in 2024.

Manufacturing Process Analysis

Based on the manufacturing process, the market is further divided into Casting, Powder Metallurgy, Additive Manufacturing, and Others. The predominance of the Casting, commanding a substantial 54.3 % market share in 2024. due to its ability to produce complex shapes with high precision and efficiency. Casting offers excellent material utilization, minimizing waste and optimizing cost-effectiveness. It is particularly advantageous for aluminum-scandium alloys, as these materials exhibit superior fluidity and castability, leading to smoother finishes and reduced post-processing requirements. Additionally, casting provides parts with excellent strength and durability, while advancements in automation further enhance the process, solidifying its dominance in the market.

Additionally, casting is a versatile and scalable process, capable of producing both small and large quantities of parts quickly and cost-effectively. For industries requiring lightweight yet strong components, such as the automotive and aerospace sectors, casting with aluminum-scandium alloys provides an optimal balance of strength, durability, and reduced weight. This makes casting a dominant choice in the manufacturing of high-performance components that meet stringent industry demands for fuel efficiency, durability, and environmental sustainability.

Application Analysis

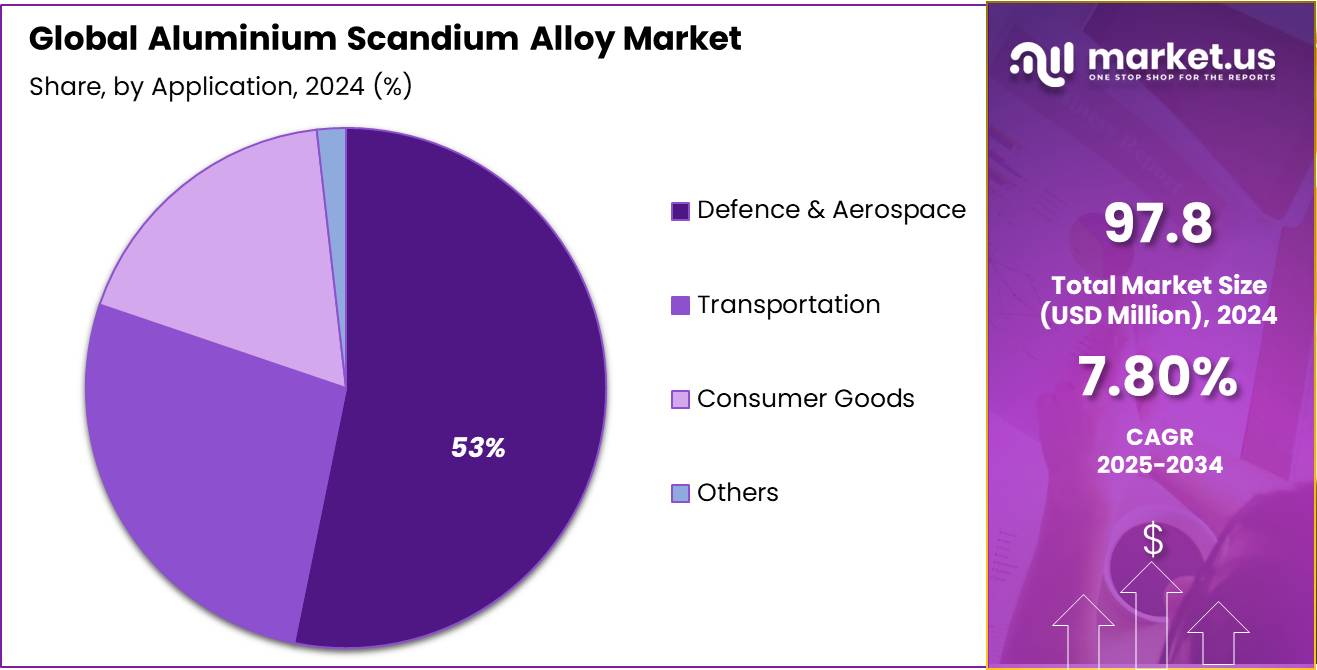

Based on application, the market is further divided into defense & aerospace, transportation, consumer goods and others. The predominance of the defense & aerospace, commanding a substantial 53.2 % market share in 2024. due to the critical need for lightweight, high-strength materials in this industry. Aluminum-scandium alloys offer superior strength-to-weight ratios, making them ideal for aircraft components such as fuselage structures, wings, and engine parts, where weight reduction directly translates to improved fuel efficiency and performance.

Additionally, the alloys’ durability and corrosion resistance make them highly suitable for the demanding conditions of aerospace applications. This sector’s continuous innovation and focus on advanced materials drive the high demand for aluminum-scandium alloys in defense and aerospace applications. Moreover, the increasing investment in defense and aerospace technologies, including the development of next-generation aircraft, satellites, and defense equipment, further boosts the market share of this sector. Additionally, the continuous evolution of technologies in these industries necessitates the use of sophisticated manufacturing methods, positioning defense & aerospace as a leading application in the market.

Key Market Segments

By Type

- Al-Sc 2% Alloy

- Al-Sc 5% Alloy

- Master Alloys

By Manufacturing Process

- Casting

- Powder Metallurgy

- Additive Manufacturing

- Others

By Application

- Defence & Aerospace

- Transportation

- Consumer Goods

- Others

Drivers

Rising demand of high- strength material

The demand for high-strength materials in industries such as aerospace, transportation, robotics, and automation is driving the growth of the aluminum-scandium alloy market. As sectors prioritize lightweight materials without compromising strength or durability, aluminum-scandium alloys have become the preferred choice due to their exceptional strength-to-weight ratio. In the aerospace industry, where weight reduction is essential for fuel efficiency and performance, these material’s ability to maintain strength while minimizing mass makes them important for aircraft components and spacecraft applications.

Furthermore, the growing demand for lighter, stronger materials in the transportation sector has significantly boosted the adoption of aluminum-scandium alloys in automotive and commercial vehicle manufacturing. These alloys offer an optimal balance of strength and reduced weight, which is crucial for enhancing vehicle performance and improving fuel efficiency. As the shift towards fuel-efficient and environmentally friendly vehicles intensifies, aluminum-scandium alloys are increasingly seen as a go-to solution for meeting these industry demands.

Additionally, the rise of robotics and automation is driving the growth of the aluminum-scandium alloy market. As technology evolves, the demand for long-lasting, durable robotic components rises, aluminum-scandium alloys provide superior tensile strength and enhanced fatigue resistance, making them ideal materials for advanced robotic systems and automated machinery. This trend is poised to accelerate as industries continue to seek cutting-edge materials for robotics and automation.

Restraints

Fluctuating Aluminum And Scandium Prices

Fluctuating aluminum prices pose a significant restraint to the growth of the global aluminum scandium alloy market. Aluminum and scandium, being the primary raw material used in the production of Al-Sc alloy, directly influence the cost of manufacturing and, ultimately, the pricing of alloy products. Any significant variation in the price of these materials can disrupt the supply chain, increase production costs, and affect the profitability of manufacturers.

This market volatility creates uncertainty for both producers and buyers of aluminum scandium alloy making it a key challenge for the industry. Furthermore, aluminum prices are highly sensitive to global market dynamics, including changes in supply and demand, energy costs, trade policies, and geopolitical tensions. For instance, fluctuations in energy costs, which are closely tied to aluminum production, can cause significant shifts in aluminum prices. Aluminum production is an energy-intensive process, and any increase in energy prices, such as rising fuel or electricity costs, can push up the cost of aluminum. This, in turn, increases the input costs for aluminum scandium alloy manufacturers, who may find it difficult to absorb these costs without passing them on to end-users, thus impacting global demand.

Opportunity

Advancements in additives manufacturing

The rapid advancements in additive manufacturing, particularly Selective Laser Melting (SLM) and Laser Powder Bed Fusion (LPBF) present significant growth opportunities for the global aluminum scandium alloy market. These innovative technologies provide the production of complex geometries and structures that were once impossible with traditional manufacturing methods, driving the demand for materials that can withstand the requirements of high-performance industries.

Aluminum scandium alloys, now more accessible due to advancements in extraction and processing, offer a unique combination of lightweight properties, high strength, and exceptional corrosion resistance. As industries such as aerospace, automotive, and medical increasingly seek materials that optimize performance and efficiency, aluminum scandium alloys are positioned to play a critical role in meeting these demands.

Moreover, as LPBF and similar additive manufacturing techniques continue to evolve, manufacturers can able to modify material properties by adjusting the composition of aluminum alloys, by incorporating scandium. This capability allows for the creation of parts with highly customized microstructures, enhancing performance and durability without adding weight.

In aerospace, where weight reduction is crucial for fuel efficiency and overall performance, these alloys are especially beneficial. As ongoing research improves additive manufacturing processes and material science, the demand for aluminum scandium alloys is expected to surge. Their ability to meet the stringent needs of industries requiring high-performance, lightweight, and durable parts ensures that aluminum scandium alloys will be pivotal in shaping the future of additive manufacturing, driving substantial growth in the global market.

Trend

AI and Automation in Alloy Production

The integration of artificial intelligence (AI) and automation in the production of aluminium-scandium alloys is driving significant advancements in material design and manufacturing. By leveraging AI algorithms and machine learning techniques, companies can optimize the composition of aluminum-scandium alloys to achieve specific properties like enhanced strength, corrosion resistance, and lightweight characteristics. This offers the manufacture of alloys in customized form for demanding applications in industries such as aerospace, automotive, and high-performance engineering. The ability to automate and predict alloy properties accelerates the development cycle, making it easier to bring innovative materials to market faster.

Moreover, AI and automation are streamlining the alloy design process by automating tasks like data analysis, composition optimization, and property prediction. This not only enhances material performance but also reduces production costs. By analyzing vast datasets, AI systems can identify cost-effective combinations of alloying elements and minimize the use of expensive or environmentally harmful materials. These advancements contribute to more sustainable production practices, as businesses can reduce waste and optimize resource usage while still achieving high-quality materials.

Additionally, AI-driven systems can improve predictive maintenance and quality control in the production of aluminium-scandium alloys. By embedding sensors in alloy components and analyzing real-time data, AI algorithms can predict potential failures or maintenance needs, helping businesses proactively address issues before they lead to downtime or costly repairs. This predictive capability ensures the reliability and longevity of aluminum-scandium alloy components, further enhancing their performance in critical applications. As AI continues to evolve, its role in the design, production, and maintenance of advanced alloys is expected to expand, driving both innovation and efficiency in the manufacturing sector.

Geopolitical Impact Analysis

Geopolitical tensions and trade disruptions impact the aluminum and scandium alloy market, driving price volatility and altering production costs.

Geopolitical factors play a significant role in shaping the global aluminum and scandium alloy market, particularly through raw material supply and trade restrictions. The aluminum supply chain is heavily concentrated in key regions such as China, Russia, and Canada, making the market vulnerable to disruptions caused by geopolitical tensions, trade wars, or sanctions.

These events can lead to price volatility and regional scarcity, impacting the availability of aluminum for alloy production. Scandium, being a rare earth element with limited production sources, is even more susceptible to supply chain disruptions. Geopolitical instability in major producing countries like Russia and China, or trade restrictions such as sanctions on Russian exports, can significantly affect scandium supply, driving up costs and altering global trade dynamics.

Additionally, trade wars, such as the ongoing U.S.-China dispute, further exacerbate market uncertainties by introducing tariffs on aluminum and other critical raw materials. These tariffs can increase the cost of aluminum-scandium alloys for manufacturers relying on imported raw materials, ultimately impacting production costs and pricing. Additionally, shifts in regional trade agreements—such as the U.S.-Mexico-Canada Agreement (USMCA) or European Union trade policies can either facilitate or complicate the flow of aluminum and scandium alloys across borders, further influencing market conditions.

Regional Analysis

In 2024, North America dominated the global aluminium-scandium alloy market, accounting for 35.9% of the total market share, driven by increasing demand from industries such as aerospace, defense, and automotive. The lightweight and high-strength properties of aluminum-scandium alloys make them ideal for applications requiring durability and performance, particularly in the aerospace sector, where they are used in aircraft components to reduce weight and improve fuel efficiency.

Additionally, the growing focus on sustainability and the demand for more energy-efficient transportation solutions are further boosting the use of these alloys in the automotive sector, particularly for electric vehicle production. Furthermore, government initiatives and investments in defense and aerospace industries are also contributing to market growth, many leading manufacturers in the North America region have established strategic partnerships and expanded their presence globally.

By collaborating with international firms and dominating their extensive distribution networks, these companies gain access to new markets and customers worldwide. Additionally, the U.S. and Canada are key players in the aerospace industry, with significant military and commercial aerospace manufacturing activities.

The demand for advanced materials like aluminum-scandium alloys, which offer superior performance compared to traditional aluminum, is expected to continue rising as defense and aviation companies seek to improve the efficiency and strength of their products. Moreover, with the increasing interest in electric vehicles and lightweight automotive solutions, the North American market for aluminum-scandium alloys is poised for further expansion in the coming years.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Key players dominate the aluminum-scandium alloy market through innovation and specialized solutions for

the aerospace, defense, and automotive industries.

Key players in the aluminum-scandium alloy market include AMG Aluminum, Rusal, Sumitomo Metal Mining Co., Ltd., China Hunan Oriental Scandium Co., Ltd., and Rio Tinto. These companies focus on developing advanced alloys to meet the growing demand in aerospace, defense, and automotive industries. AMG Aluminum invests heavily in cutting-edge alloys for aerospace applications. Rusal emphasizes high-performance alloys to enhance strength and durability.

Sumitomo Metal Mining offers solutions for the automotive and aerospace sectors. Hunan Oriental Scandium is expanding the market within China, while Rio Tinto specializes in creating alloys for high-performance use. These companies maintain their dominance by continually innovating and adapting to industry needs.

The following are some of the major players in the industry

- Rio Tinto

- Rusal

- AMG Aluminum

- KBM Affilips

- Stanford Advanced Materials

- Ashurst Technology Ltd.

- Aluminum Precision Products, Inc.

- Materion Corporation

- Scandium International Mining Corp.

- Clean TeQ Holdings Limited

- Glencore

- Sumitomo Metal Mining Co., Ltd.

- Metallica Minerals Limited

- Platina Resources Limited

- Australian Mines Limited

- Treibacher Industrie AG

- Heraeus Holding GmbH

- Hunan Oriental Scandium Co., Ltd.

- Intermix-met

- Advanced Metallurgical Group N.V.

- Others

Recent Development

- May 2023- NioCorp is partnering with Nanoscale Powders to explore the production of the first U.S.-based mine-to-master alloy, vertically integrated aluminum-scandium alloy production. This initiative aims to reduce reliance on China for scandium, with pilot-scale production of aluminum-scandium master alloy using purchased scandium feedstock planned before the Elk Creek project’s commercial operation.

- August 9, 2023- NioCorp Developments Ltd. secured $10 million in federal funding for U.S. aluminum-scandium (AlSc) master alloy production, supported by Senator Deb Fischer and Congressman Don Bacon, to strengthen domestic production for defense and aerospace applications. This development highlights the region’s robust research and development activities in advanced materials for critical industries.

- September 2024- Scandium Canada has filed a provisional patent with the U.S. Patent and Trademark Office for aluminum scandium (Al-Sc) alloy powders for additive manufacturing (AM), developed in collaboration with McMaster University. This innovation aims to enhance the production of lightweight, high-strength components for industries like aerospace, automotive, and maritime, marking a significant step in the company’s commitment to advancing scandium applications and reducing carbon emissions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 97.8 Mn |

| Forecast Revenue (2034) | US$ 207.3 Mn |

| CAGR (2025-2034) | 7.80 % |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Al-Sc 2% Alloy, Al-Sc 5% Alloy, Master Alloys), By Manufacturing Process (Casting, Powder Metallurgy, Additive Manufacturing, Others), By Application (Defence & Aerospace, Transportation, Consumer Goods, Others), |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC- China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America- Brazil, Mexico & Rest of Latin America; Middle East & Africa- GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Rio Tinto, Rusal, AMG Aluminum, KBM Affilips, Stanford Advanced Materials, Ashurst Technology Ltd., Aluminum Precision Products, Inc., Materion Corporation, Scandium International Mining Corp., Clean Te Q Holdings Limited, Glencore, Sumitomo Metal Mining Co., Ltd., Metallica Minerals Limited, Platina Resources Limited, Australian Mines Limited, Treibacher Industries AG, Heraeus Holding GmbH, Hunan Oriental Scandium Co., Ltd., Intermix met, Advanced Metallurgical Group N.V. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |