Quick Navigation

Report Overview

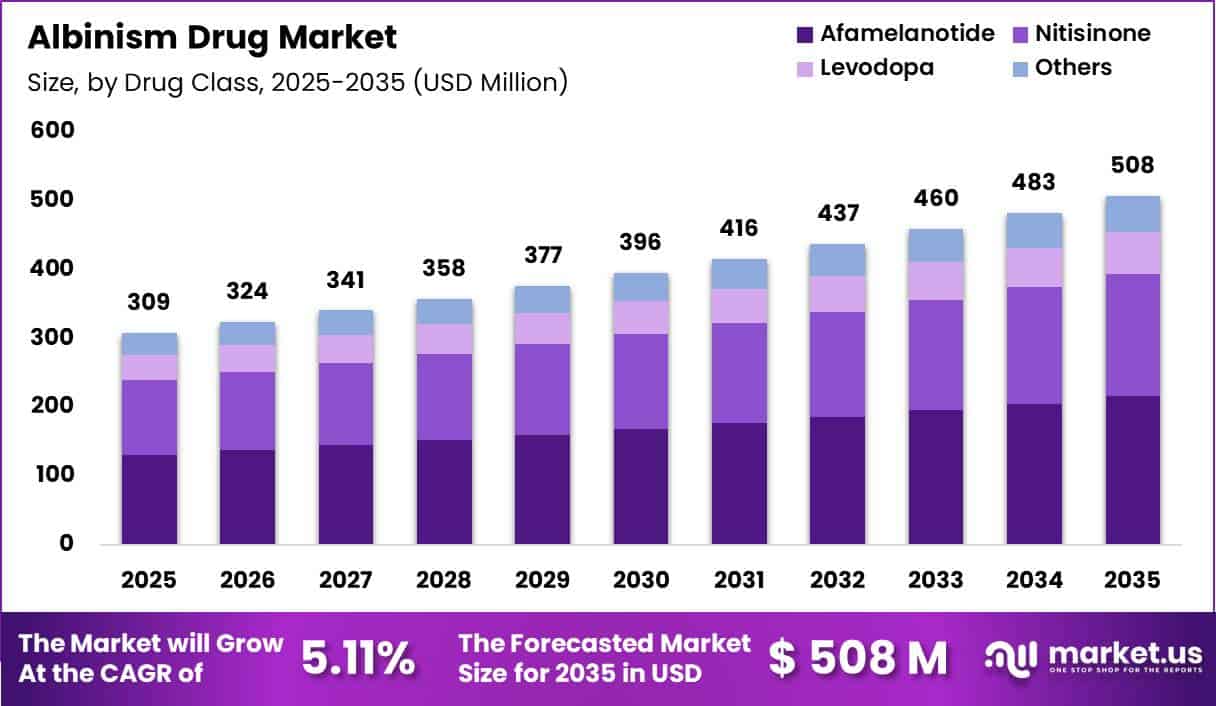

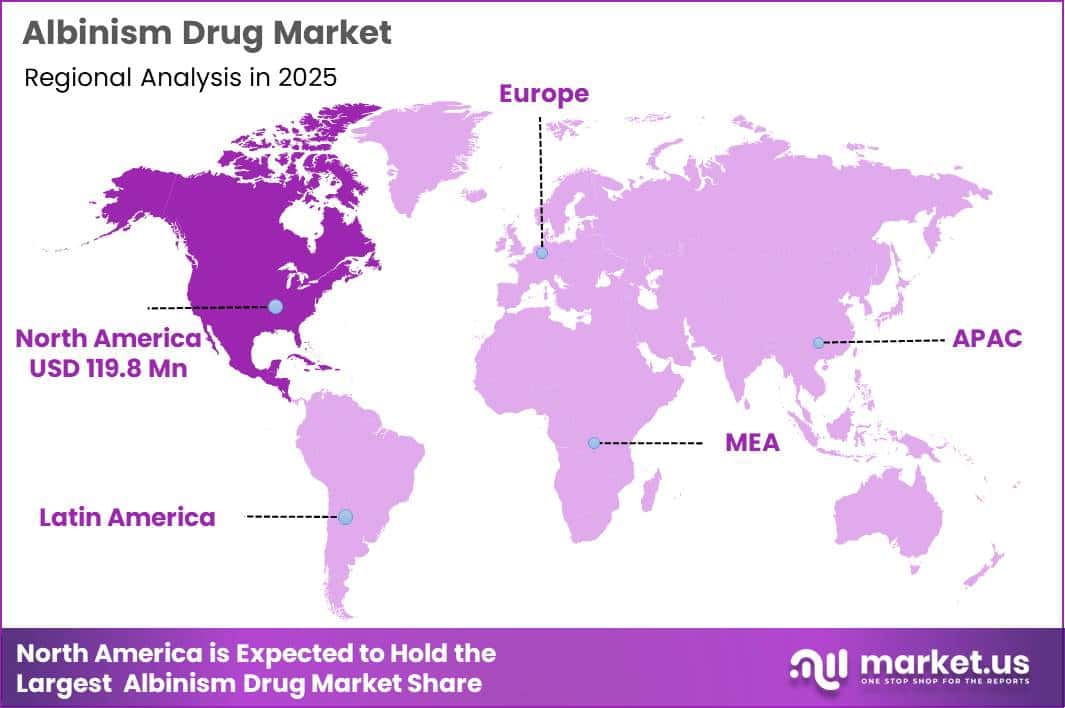

Global Albinism Drug Market size is expected to be worth around US$ 508 Million by 2035 from US$ 309 Million in 2025, growing at a CAGR of 5.11% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 38.60% share with a revenue of US$ 119.08 Million.

Albinism is a rare inherited condition in which the body produces little or no melanin, the pigment responsible for coloring the skin, hair, and eyes. This lack of melanin can lead to very light skin and hair, as well as characteristic eye changes.

The global prevalence of oculocutaneous albinism is estimated at roughly 1 in 17,000–20,000 people in Europe and the United States, while some African populations have reported rates as high as 1 in 1,000. Because melanin is essential for normal eye development, many individuals with albinism experience low vision, nystagmus, and marked sensitivity to light.

As a result, lifelong vision care, strict sun protection, and regular skin examinations are central to management, rather than relying on drug therapy alone. Experimental gene-based approaches aimed at correcting the underlying genetic defects remain at a very early research stage, mostly in animal models, and no gene therapy or definitive pharmacologic cure is currently available in routine clinical practice.

At present, there is no cure for albinism, so there is no single “albinism drug.” Treatment instead focuses on managing symptoms and complications, particularly visual impairment and skin cancer risk.

A small number of experimental drugs are under investigation. Researchers are studying agents such as nitisinone and L-dihydroxyphenylalanine (L-DOPA) to boost melanin production in certain genetic subtypes, including forms like OCA1B.

These compounds aim to enhance pigmentation in the skin, hair, and eyes and potentially improve visual function. However, clinical results to date have been modest, and these therapies have not yet become part of standard care.

For now, best practice remains a combination of supportive ophthalmologic care, UV-protective strategies, and careful dermatologic surveillance, while research continues to explore future gene-based and pharmacologic options.

Key Takeaways

- Market Size: Global Albinism Drug Market size is expected to be worth around US$ 508 Million by 2035 from US$ 309 Million in 2025.

- Market Share: The Market growing at a CAGR of 5.11% during the forecast period from 2026 to 2035.

- Drug Class Analysis: Afamelanotide represents the leading segment, accounting for approximately 42.5% of the global market share in 2025.

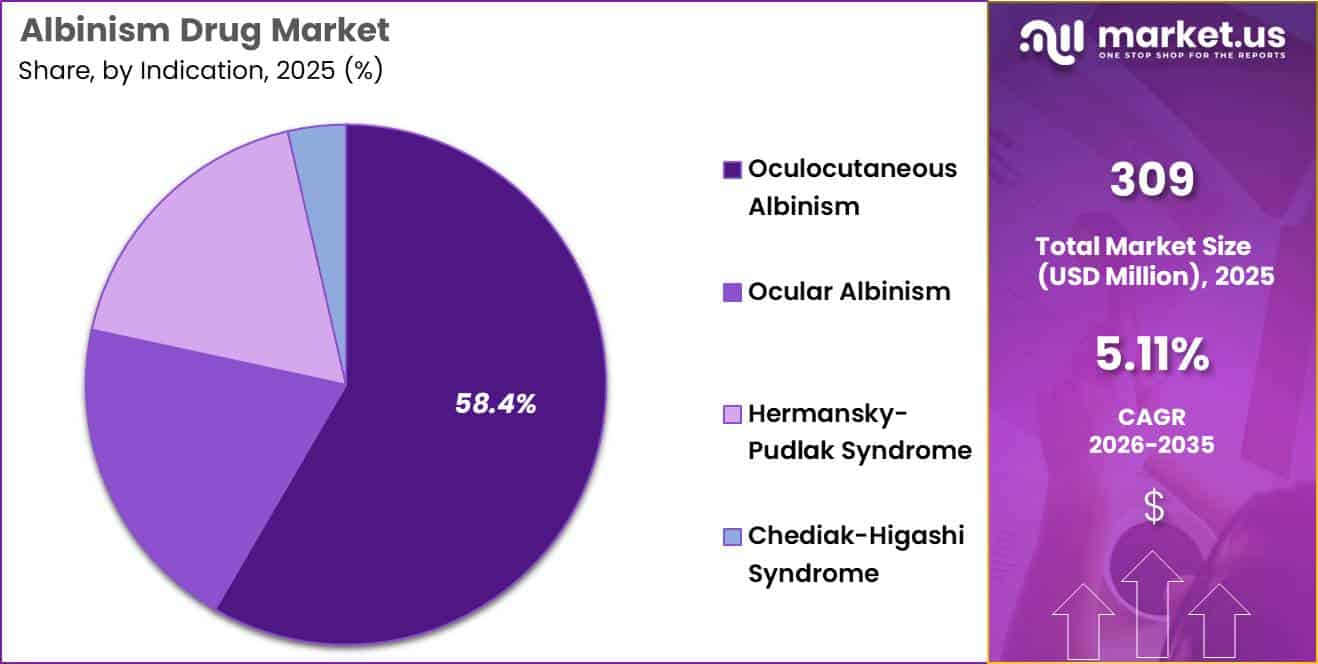

- Indication Analysis: Oculocutaneous Albinism (OCA) is projected to dominate the global market, accounting for approximately 58.4% of total market share.

- Route of Administration Analysis: Injectable formulations are projected to dominate the market, accounting for 44.6% of total share in 2025.

- Distribution Channel Analysis: Specialty pharmacies are projected to dominate the market, accounting for approximately 39.2% of the total share in 2025.

- Regional Analysis: In 2025, North America led the market, achieving over 38.60% share with a revenue of US$ 119.08 Million.

Drug Class Analysis

The drug class segmentation of the albinism drug market reflects a highly specialized and evolving therapeutic landscape, driven by targeted pharmacological interventions aimed at improving melanin production, visual function, and associated metabolic pathways. Prescription-based therapies continue to dominate the market, supported by increasing research in rare genetic disorders and the need for disease-modifying treatments

Among drug classes, Afamelanotide represents the leading segment, accounting for approximately 42.5% of the global market share in 2025. Its dominance is attributed to its mechanism as a melanocortin-1 receptor agonist, which stimulates eumelanin production and provides photoprotection benefits. The drug has gained regulatory acceptance in several regions, reinforcing its commercial adoption and clinical preference.

The Nitisinone segment is emerging as a promising therapeutic category, supported by clinical evidence indicating its ability to enhance pigmentation through tyrosine pathway modulation. Its repositioning from metabolic disorders to albinism treatment highlights ongoing innovation, although adoption remains limited due to early-stage clinical validation.

Levodopa is also utilized in niche applications, particularly for neurological and visual pathway support, though its market penetration is comparatively moderate. The “Others” category, including experimental gene therapies and adjunct treatments, is expected to witness gradual growth, driven by advancements in precision medicine and rare disease research.

Indication Analysis

The indication-based segmentation of the albinism drug market demonstrates a clear concentration toward high-prevalence genetic subtypes, with therapeutic demand largely driven by clinical severity, multisystem involvement, and unmet treatment needs.

The market is primarily categorized into Oculocutaneous Albinism (OCA), Ocular Albinism, Hermansky–Pudlak Syndrome (HPS), and Chediak–Higashi Syndrome (CHS), each reflecting distinct pathological and therapeutic profiles.

Oculocutaneous Albinism (OCA) is projected to dominate the global market, accounting for approximately 58.4% of total market share in 2025. Thisg skin, dominance is attributed to its higher prevalence and broader clinical manifestation, affectin hair, and ocular systems due to impaired melanin production. The significant patient pool and continuous research into pigmentation-enhancing therapies have reinforced its leading position.

The Ocular Albinism segment represents a moderate share, characterized by vision-related abnormalities without extensive skin involvement. Demand for therapeutic interventions in this segment is supported by increasing diagnosis rates and advancements in ophthalmic care.

Hermansky–Pudlak Syndrome (HPS) constitutes a niche but clinically significant segment, driven by its multisystem complications, including bleeding disorders and pulmonary conditions, which increase treatment complexity and cost.

Similarly, Chediak–Higashi Syndrome (CHS) accounts for a smaller share due to its rare incidence; however, its association with immune dysfunction and severe systemic manifestations necessitates specialized therapeutic approaches, supporting steady but limited market growth.

Route of Administration Analysis

The route of administration segment in the albinism drug market is structured across injectable, oral, topical, and implantable delivery systems, reflecting differences in therapeutic efficacy, disease severity, and patient compliance.

Injectable formulations are projected to dominate the market, accounting for 44.6% of total share in 2025, driven by their high bioavailability and rapid systemic absorption. Parenteral delivery enables drugs to bypass gastrointestinal barriers, ensuring precise dosing and faster onset of action, which is critical in advanced or experimental therapies.

Oral formulations represent a significant segment due to ease of administration, cost-effectiveness, and suitability for long-term management. These drugs are widely preferred for chronic symptom control despite limitations related to variable absorption and bioavailability.

Topical therapies hold a notable share, particularly for managing dermatological manifestations such as photosensitivity and skin protection, forming a core component of daily treatment regimens.

Implantable delivery systems are emerging as an advanced segment, offering sustained drug release and improved patient adherence. These systems are gaining traction in precision medicine and long-term therapeutic strategies, supported by broader advancements in drug delivery technologies.

Distribution Channel Analysis

The distribution channel landscape of the albinism drug market is structured across specialty pharmacies, hospital pharmacies, retail pharmacies, and other channels, each contributing distinctly to product accessibility and patient adherence.

Specialty pharmacies are projected to dominate the market, accounting for approximately 39.2% of the total share in 2025. This dominance is attributed to their advanced capabilities in handling complex therapies, patient counseling, and reimbursement support, which are critical for managing rare genetic conditions such as albinism.

Hospital pharmacies represent a significant segment, driven by the administration of prescription therapies during clinical consultations and inpatient care. Their role is particularly vital in early-stage diagnosis and treatment initiation, where medical supervision is required.

Retail pharmacies contribute to market expansion through widespread geographic presence and ease of access, particularly in urban and semi-urban regions. They facilitate the distribution of maintenance medications and supportive treatments, enhancing long-term therapy adherence.

The “others” segment, including online pharmacies and direct-to-patient distribution models, is witnessing gradual growth. Increasing digital adoption and home delivery services are expected to support this segment, improving convenience and expanding patient reach globally.

Key Market Segments

By Drug Class

- Nitisinone

- Afamelanotide

- Levodopa

- Others

By Indication

- Oculocutaneous Albinism

- Ocular Albinism

- Hermansky-Pudlak Syndrome

- Chediak-Higashi Syndrome

By Route of Administration

- Oral

- Injectable

- Topical

- Implantable

By Distribution Channel

- Hospital Pharmacies

- Specialty Pharmacies

- Retail Pharmacies

- Others

Driving Factors

The primary driver of the albinism drug market is the increasing prevalence of genetic disorders combined with dermatological and ophthalmic complications. Albinism affects approximately 1 in 17,000 to 1 in 20,000 individuals globally, with significantly higher prevalence in certain regions such as Sub-Saharan Africa (up to 1 in 5,000 people). This widespread occurrence creates a consistent demand for symptomatic treatments, including photoprotection therapies, vision correction drugs, and dermatological care.

Additionally, individuals with albinism face up to a 1,000-fold increased risk of skin cancer, primarily due to lack of melanin protection against ultraviolet radiation. This has led to increased demand for preventive pharmaceutical products such as high-SPF dermatological formulations and emerging melanin-stimulating therapies.

Government and global health bodies, including United Nations human rights programs, have intensified awareness initiatives, indirectly boosting diagnosis rates and treatment uptake. Improved screening and genetic counseling services have also contributed to earlier identification of cases. As diagnosis rates improve, the patient pool eligible for therapeutic interventions expands, thereby supporting sustained market growth.

Trending Factors

A notable trend in the albinism drug market is the shift toward targeted and supportive therapies rather than curative treatments, as no definitive cure currently exists. Clinical management is increasingly focused on multidisciplinary care, combining dermatology, ophthalmology, and genetic counseling.

Emerging research is exploring gene-based therapies and melanin biosynthesis modulation, although these remain in early development stages. Current treatment approaches emphasize preventive care, including broad-spectrum sunscreens, retinoids, and visual aids, reflecting a supportive care model. This trend is reinforced by healthcare guidelines that prioritize lifelong UV protection and regular ophthalmic monitoring.

Another observable trend is the integration of public health programs. For example, awareness campaigns linked to International Albinism Awareness Day have increased early diagnosis rates. Epidemiological studies indicate that only 13% of countries have reliable prevalence data, highlighting ongoing efforts to improve disease surveillance.

Digital health tools and tele-ophthalmology are also being adopted to address access gaps, particularly in developing regions. These trends collectively indicate a gradual transition toward holistic, patient-centric management models, which is expected to shape future drug development strategies.

Restraint Factors

The albinism drug market faces significant constraints, primarily due to the absence of curative therapies and limited commercial incentives. As a rare genetic disorder, albinism has a relatively small patient population, which restricts large-scale pharmaceutical investments.

Clinical complexity also acts as a barrier. Albinism is not a single disease but a group of genetic disorders with multiple subtypes, each involving different mutations affecting melanin production. This heterogeneity complicates drug development and reduces the feasibility of standardized treatment protocols.

Furthermore, limited epidemiological data remains a critical challenge. Only a small proportion of countries have comprehensive prevalence statistics, which affects market forecasting and investment decisions. In addition, healthcare access disparities—particularly in low-income regions where prevalence is higher—restrict treatment adoption.

Economic barriers also persist. Long-term management requires continuous use of sunscreens, visual aids, and medical consultations, which may not be affordable for all patients. The lack of reimbursement frameworks in several countries further limits drug accessibility. These combined factors significantly restrain the growth potential of the albinism therapeutics market.

Opportunity

Despite existing limitations, the market presents strong opportunities driven by advancements in genetic research and orphan drug development frameworks. Increasing recognition of albinism as a public health concern has encouraged governments and global organizations to promote inclusive healthcare policies.

The orphan drug designation in several regions provides incentives such as tax credits, market exclusivity, and accelerated approvals, which can attract pharmaceutical investment into rare diseases like albinism. Given that approximately 1 in 70 individuals globally carry a gene associated with oculocutaneous albinism, the latent carrier population suggests long-term diagnostic and therapeutic demand.

There is also growing opportunity in preventive dermatology and advanced photoprotection formulations, particularly in high UV exposure regions. Innovations in gene therapy and CRISPR-based interventions offer future potential for addressing underlying genetic defects.

Additionally, expanding healthcare infrastructure in emerging markets, combined with international funding initiatives, is expected to improve treatment accessibility. With increasing awareness and research funding, the albinism drug market is positioned for moderate but sustained growth, particularly in specialized therapeutic segments.

Regional Analysis

North America accounted for the largest share of the albinism drug market, supported by increasing exposure to environmental toxins that disrupt the histological structure of melanin, alongside a rising level of awareness regarding albinism across the region.

The region led the global market, capturing over 38.60% share and generating revenue of approximately US$ 119.08 million. Additionally, well-established healthcare infrastructure and higher diagnosis rates have contributed to sustained market dominance.

The Asia-Pacific region is projected to register significant growth over the forecast period. This expansion is driven by increasing government-led initiatives aimed at improving awareness, a rise in medical tourism, and a growing focus on research and development activities.

Furthermore, the presence of a large population base, substantial untapped market opportunities, and increasing demand for high-quality healthcare services are expected to accelerate market growth in the region.

At the country level, the report provides a detailed assessment of key market-influencing factors and regulatory changes that shape both current and future market dynamics. Analytical frameworks such as downstream and upstream value chain analysis, evaluation of technological trends, Porter’s Five Forces analysis, and relevant case studies are incorporated to generate accurate market forecasts for individual countries.

Moreover, the analysis considers the presence and accessibility of global brands, along with the competitive challenges posed by domestic and regional players. Factors such as domestic tariffs, trade routes, and supply chain dynamics are also evaluated to provide a comprehensive outlook on country-specific market performance.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

The competitive landscape of the albinism drug market is characterized through a comprehensive evaluation of key market participants. Detailed insights are provided on company profiles, including financial performance, revenue generation, and overall market potential.

The analysis also highlights investments in research and development, reflecting the strategic focus on innovation and pipeline expansion within the albinism treatment space. Additionally, information on new market initiatives, global footprint, and geographical expansion strategies is incorporated to assess competitive positioning.

Operational capabilities are examined through data on production sites, manufacturing facilities, and production capacities, offering an understanding of supply-side strengths. Furthermore, company-specific strengths and weaknesses are evaluated to identify competitive advantages and potential risks.

Product-related analysis includes product launches, portfolio breadth and depth, and application-level dominance. All data points presented are specifically aligned with each company’s activities and strategic focus within the albinism drug market, ensuring a targeted and relevant competitive assessment.

Market Key Players

- Clinuvel Pharmaceuticals Limited

- Orpharma

- Novartis AG

- Pfizer Inc.

- Merck & Co., Inc.

- Johnson & Johnson Services, Inc.

- AbbVie Inc.

- Takeda Pharmaceutical Company Limited

- Sanofi S.A.

- Bristol-Myers Squibb Company

- Eli Lilly and Company

- Amgen Inc.

- Gilead Sciences, Inc.

- Biogen Inc.

- Vertex Pharmaceuticals Incorporated

- Others

Recent Developments

- Clinuvel Pharmaceuticals Limited 2026: Clinuvel Pharmaceuticals Limited expanded its global clinical engagement through dermatology and photomedicine conferences, strengthening the positioning of its afamelanotide-based therapy and improving physician awareness in photosensitivity-related conditions.

- Novartis AG and Pfizer Inc.: advanced research initiatives focused on gene therapy and targeted treatments aimed at addressing melanin production pathways, reflecting a shift toward precision medicine.

- Bristol-Myers Squibb Company 2025: Bristol-Myers Squibb Company and Eli Lilly and Company strengthened their rare disease portfolios through increased R&D investments and expansion of specialty care divisions, indirectly supporting niche indications such as albinism.

- 2025–2026: Takeda Pharmaceutical Company Limited and AbbVie Inc. engaged in strategic research collaborations and clinical partnerships aimed at accelerating innovation in pigmentation disorders and orphan drug development.

- 2025–2026: Gilead Sciences, Inc. and Biogen Inc. expanded their advanced biologics and genetic research platforms, supporting long-term development of novel therapies applicable to rare genetic conditions including albinism.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 309 Million |

| Forecast Revenue (2035) | US$ 508 Million |

| CAGR (2026-2035) | 5.11% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Drug Class (Nitisinone, Afamelanotide, Levodopa, Others) By Indication (Oculocutaneous Albinism, Ocular Albinism, Hermansky-Pudlak Syndrome, Chediak-Higashi Syndrome) By Route of Administration (Oral, Injectable, Topical, Implantable) By Distribution Channel(Hospital Pharmacies, Specialty Pharmacies, Retail Pharmacies, Others) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Clinuvel Pharmaceuticals Limited, Orpharma, Novartis AG, Pfizer Inc., Merck & Co., Inc., Johnson & Johnson Services, Inc., AbbVie Inc., Takeda Pharmaceutical Company Limited, Sanofi S.A., Bristol-Myers Squibb Company, Eli Lilly and Company, Amgen Inc., Gilead Sciences, Inc., Biogen Inc., Vertex Pharmaceuticals Incorporated, Others. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |