Global Aircraft Tube and Duct Assemblies Market Size, Share, Growth Analysis By Aircraft Type (Commercial Aircraft [Narrow Body Aircraft, Wide Body Aircraft, Regional Jets], Fighter Jets, Military Aircraft), By Material (Aluminum, Steel, Nickel, Titanium, Composite, Inconel), By Duct Type (Rigid, Semi-Rigid, Flexible), By Application (Engine Bleeds, Thermal Anti-Ice, Pylon Ducting (HVAC) Enamel, Fuselages, Inlets/Exhausts, Environment Control Systems (ECS), Lavatories, Waste Systems), By Sales Channel (OEMs, Aftermarket), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 183022

- Number of Pages: 268

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

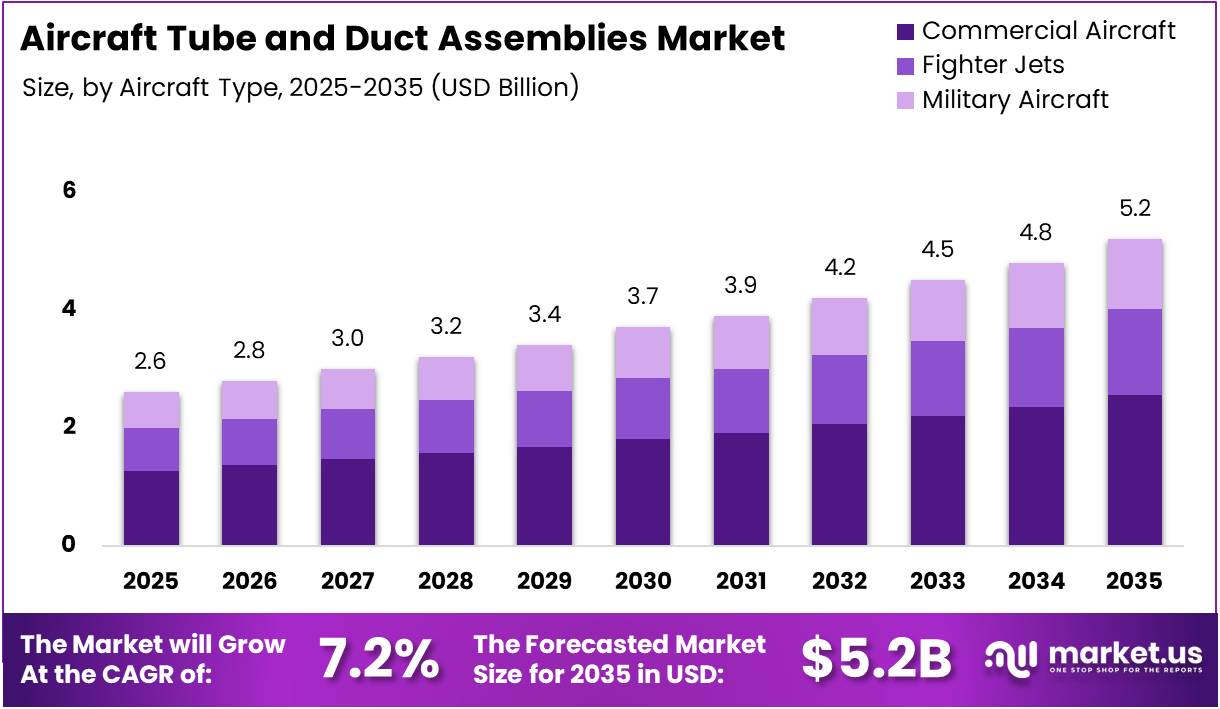

The Global Aircraft Tube and Duct Assemblies Market size is expected to be worth around USD 5.2 Billion by 2035 from USD 2.6 Billion in 2025, growing at a CAGR of 7.2% during the forecast period 2026 to 2035.

Aircraft tube and duct assemblies are critical fluid and air conveyance components used throughout the airframe. They transport hydraulic fluid, bleed air, fuel, and environmental control system air across key aircraft systems. These assemblies are manufactured using materials such as aluminum, titanium, steel, composites, and high-performance alloys like Inconel.

These components serve applications including engine bleed systems, thermal anti-ice, pylon ducting, fuselage routing, and environmental control systems. Moreover, they are essential for maintaining aircraft safety, efficiency, and structural integrity. Their use spans commercial aviation, military platforms, and emerging next-generation aircraft programs globally.

The market is supported by rising commercial aircraft production backlogs and sustained growth in global air passenger traffic. Additionally, expanding Aerospace MRO activities and fleet modernization programs are generating strong replacement demand for tube and duct components. Governments are also increasing defense aviation budgets, further driving demand for these assemblies.

Aviation regulatory bodies such as the FAA and EASA enforce strict certification standards for aircraft fluid systems. These regulations push manufacturers to adopt higher-grade materials and precision engineering processes. Consequently, compliance requirements are shaping product design and material selection strategies across the industry, while also raising the overall quality benchmark for assemblies.

According to the FAA, aircraft hydraulic tubing systems operate at pressures up to 3,000–5,000 psi (207–345 bar), establishing strict structural and material requirements for tube assemblies. According to NASA, engine bleed air duct systems must withstand temperatures of up to 600°C, requiring high-temperature resistant materials and advanced thermal insulation in aircraft ducting.

According to ASM International, titanium tubing provides approximately 40% weight reduction compared to steel while maintaining comparable strength. Additionally, according to Airbus, composite ducting systems deliver 20–30% weight savings over aluminum ducts. Furthermore, according to Boeing, pre-fabricated and pre-tested tube assemblies reduce installation errors by up to 70%.

According to NASA, additive manufacturing enables up to a 60% reduction in part count for complex aerospace duct assemblies. Moreover, according to EASA, additive manufacturing reduces production lead time by approximately 30–50% for aerospace ducting components compared to conventional fabrication, supporting faster delivery and reduced overall production costs.

Key Takeaways

- The global Aircraft Tube and Duct Assemblies Market was valued at USD 2.6 Billion in 2025 and is projected to reach USD 5.2 Billion by 2035.

- The market is expected to grow at a CAGR of 7.2% during the forecast period from 2026 to 2035.

- By Aircraft Type, Commercial Aircraft held the largest segment share of 48.9% in 2025.

- By Material, Aluminum dominated with a market share of 31.6% in 2025.

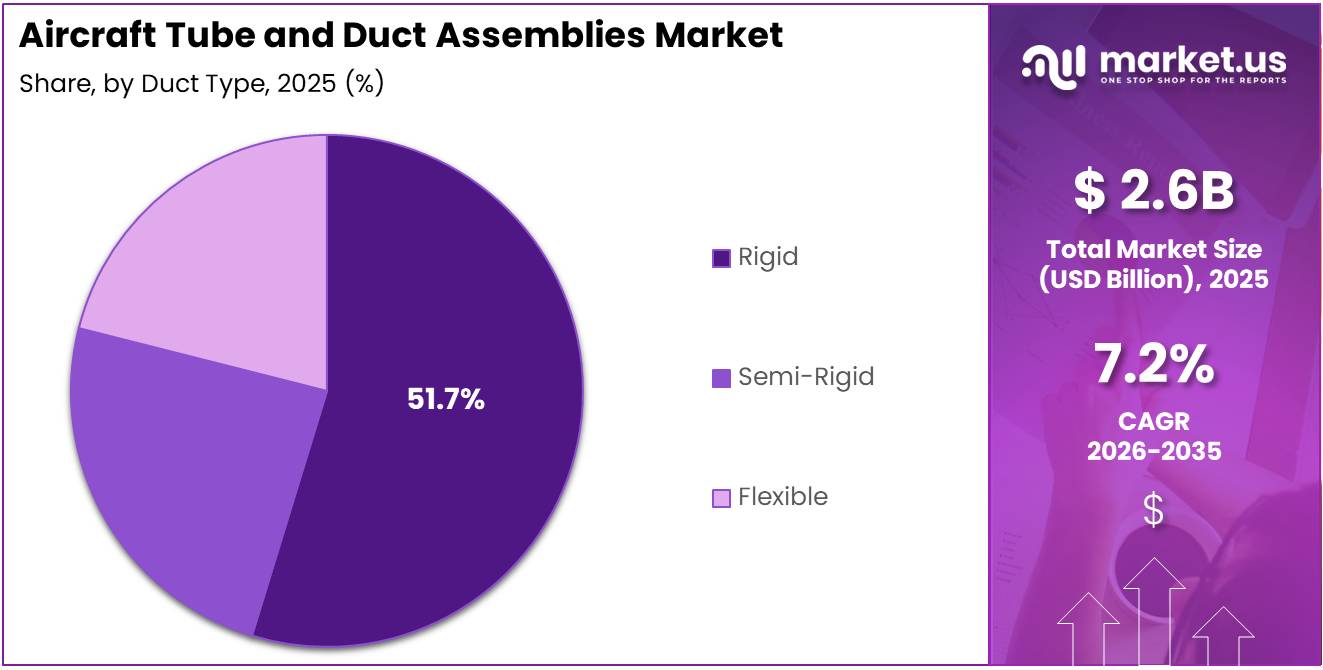

- By Duct Type, Rigid ducts held the highest share at 51.7% in 2025.

- By Application, Engine Bleeds was the leading segment with a share of 19.3% in 2025.

- By Sales Channel, OEMs accounted for the dominant share of 56.9% in 2025.

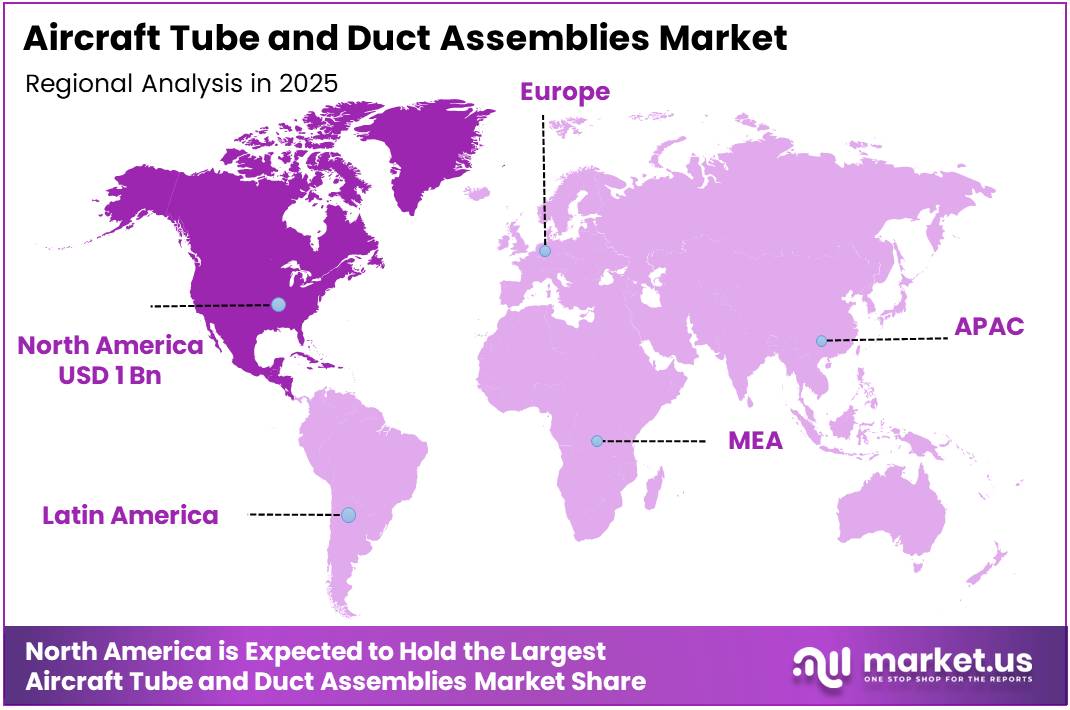

- North America was the leading region with a market share of 38.50%, valued at approximately USD 1 Billion in 2025.

Aircraft Type Analysis

Commercial Aircraft dominates with 48.9% due to high production volumes and growing global air travel demand.

In 2025, Commercial Aircraft held a dominant market position in the By Aircraft Type segment of Aircraft Tube and Duct Assemblies Market, with a 48.9% share. This category covers Narrow Body Aircraft, Wide Body Aircraft, and Regional Jets. All three require extensive tube and duct systems for bleed air, hydraulic, and ECS functions.

Fighter Jets represent a specialized and high-value sub-segment in this market. These platforms demand precision-engineered assemblies capable of withstanding extreme pressure, vibration, and thermal stress. Moreover, advanced fighter aircraft incorporate complex onboard systems requiring a greater number of precisely routed tube and duct assemblies, and increasing defense budgets further support this demand.

Military Aircraft represent another key contributor to overall market revenue. These platforms require durable, corrosion-resistant assemblies designed for long operational lifecycles and challenging environments. Additionally, rising geopolitical tensions and active global defense procurement programs are increasing military aircraft orders, thereby generating stable and growing demand for associated tube and duct systems.

Material Analysis

Aluminum dominates with 31.6% due to its lightweight properties, corrosion resistance, and cost-effectiveness in aircraft manufacturing.

In 2025, Aluminum held a dominant market position in the By Material segment of Aircraft Tube and Duct Assemblies Market, with a 31.6% share. Aluminum is widely used due to its lightweight nature, excellent corrosion resistance, and ease of fabrication. It remains the preferred material for commercial aircraft tube and duct systems globally.

Steel is used in high-pressure hydraulic tube assemblies requiring superior structural strength and durability. It performs reliably under extreme pressure conditions, making it a preferred material for hydraulic and fuel line tube systems. Moreover, steel assemblies are widely used in military aircraft platforms where robustness and resistance to mechanical stress are critical operational requirements.

Nickel alloys are preferred in high-temperature environments such as engine-adjacent duct systems where standard materials would fail under sustained thermal exposure. These alloys maintain mechanical integrity and resist oxidation at elevated temperatures. Consequently, nickel-based materials are widely specified in military and high-performance aerospace applications that demand enhanced durability and long-term reliability under extreme operating conditions.

Titanium offers approximately 40% weight reduction compared to steel while maintaining comparable strength, making it ideal for weight-sensitive airframe tube systems. It is widely adopted in modern aircraft programs where reducing structural weight directly improves fuel efficiency. Moreover, titanium’s excellent corrosion resistance extends assembly service life, lowering long-term maintenance costs for operators.

Composite materials are increasingly adopted in aircraft tube and duct assemblies due to their ability to achieve 20–30% weight savings compared to aluminum ducts. These materials improve overall aircraft efficiency by reducing structural load. Additionally, composites offer excellent resistance to corrosion and fatigue, making them a strong fit for modern commercial and next-generation aircraft designs.

Inconel, a high-performance nickel superalloy, is used in extreme heat zones such as engine bleed and exhaust duct assemblies. It maintains structural integrity at temperatures exceeding 600°C, where standard metals would degrade. Consequently, Inconel is the preferred material for engine-adjacent ducting applications that demand exceptional thermal stability and long-term performance under continuous high-heat operating conditions.

Duct Type Analysis

Rigid ducts dominate with 51.7% due to their ability to handle high-pressure and high-temperature aerospace applications.

In 2025, Rigid held a dominant market position in the By Duct Type segment of Aircraft Tube and Duct Assemblies Market, with a 51.7% share. Rigid ducts are preferred for their structural stability and ability to withstand high-pressure and high-temperature conditions. They are widely used in engine bleed, hydraulic, and primary airflow ducting systems.

Semi-Rigid ducts offer a balance between the structural firmness of rigid ducts and the flexibility of fully flexible variants. They are commonly used in aircraft sections where limited movement or vibration absorption is required. Consequently, semi-rigid assemblies are applied in routing paths that involve moderate bends and space constraints within the airframe.

Flexible ducts are used in areas requiring high movement tolerance, vibration dampening, or complex routing through tight spaces. They are especially valuable in ECS, lavatory, and waste system connections where rigid designs are impractical. Moreover, flexible assemblies simplify installation and maintenance, reducing turnaround time during aircraft servicing activities.

Application Analysis

Engine Bleeds dominates with 19.3% due to its critical role in powering aircraft pneumatic and environmental systems.

In 2025, Engine Bleeds held a dominant market position in the By Application segment of Aircraft Tube and Duct Assemblies Market, with a 19.3% share. Engine bleed systems extract compressed air from engine compressor stages to power cabin pressurization, anti-icing, and ECS functions. These systems require high-temperature and high-pressure rated duct assemblies.

Thermal Anti-Ice systems use bleed air ducts to prevent ice formation on wing leading edges and engine inlets. These assemblies must withstand high thermal loads and continuous airflow demands. Moreover, regulatory requirements mandate reliable anti-ice performance across all weather conditions, ensuring consistent procurement of certified thermal ducting components for commercial and military aircraft platforms.

Pylon Ducting connects engine systems to airframe routing, managing fuel, hydraulic, and electrical lines within a compact structural space. These assemblies must meet strict fire resistance and pressure ratings. Additionally, pylon duct systems require precise engineering to accommodate vibration, thermal expansion, and multi-system integration demands across various aircraft types.

Fuselages require extensive internal tube and duct routing to support hydraulic, ECS, and bleed air distribution throughout the airframe. These assemblies span long distances and must be lightweight yet structurally reliable. Consequently, fuselage ducting design demands careful material selection and routing optimization to minimize weight while maintaining full system performance.

Inlets/Exhausts require precisely routed duct assemblies to manage airflow and maintain aerodynamic and structural system efficiency. These components operate under significant pressure differentials and thermal stress. Therefore, materials such as titanium and Inconel are commonly used in inlet and exhaust duct applications to ensure long-term reliability and performance.

Environment Control Systems (ECS) rely on duct networks to regulate cabin air quality, temperature, and pressure throughout flight. ECS ducting must balance airflow efficiency with minimal weight and noise transmission. Moreover, increasing passenger comfort expectations and stricter cabin air quality standards are driving demand for advanced ECS duct assemblies in new aircraft programs.

Lavatories use specialized duct assemblies for water supply, waste management, and ventilation within aircraft cabin systems. These assemblies must resist corrosion, moisture, and biological contamination. Additionally, growing airline focus on cabin hygiene and regulatory compliance is increasing demand for high-quality, durable lavatory ducting solutions in both new builds and retrofit programs.

Waste Systems use flexible duct assemblies designed for reliable fluid and waste conveyance across complex airframe routing paths. These systems must meet strict containment and leak-prevention standards. Furthermore, as airlines expand cabin facilities and operate larger aircraft with more lavatories, demand for robust and certified waste system duct assemblies continues to grow.

Sales Channel Analysis

OEMs dominate with 56.9% due to their direct integration into new aircraft manufacturing programs and long-term supply contracts.

In 2025, OEMs held a dominant market position in the By Sales Channel segment of Aircraft Tube and Duct Assemblies Market, with a 56.9% share. Original Equipment Manufacturers procure tube and duct assemblies during the aircraft production phase, often under long-term supply agreements. This channel benefits directly from rising aircraft delivery rates and new program launches.

The Aftermarket segment serves airlines, MRO providers, and aircraft operators with replacement and repair-grade tube and duct assemblies. Demand in this segment is driven by aging aircraft fleets, increasing flight cycles, and mandatory maintenance schedules. However, growing global fleet sizes and extended aircraft lifecycles are steadily expanding aftermarket revenue opportunities.

Both channels are expected to grow over the forecast period. The OEM channel will continue to benefit from aircraft production ramp-ups, while the aftermarket channel is poised for acceleration as global fleets age. Together, these channels ensure a consistent and diversified demand base for aircraft tube and duct assembly manufacturers worldwide.

Key Market Segments

By Aircraft Type

- Commercial Aircraft

- Narrow Body Aircraft

- Wide Body Aircraft

- Regional Jets

- Fighter Jets

- Military Aircraft

By Material

- Aluminum

- Steel

- Nickel

- Titanium

- Composite

- Inconel

By Duct Type

- Rigid

- Semi-Rigid

- Flexible

By Application

- Engine Bleeds

- Thermal Anti-Ice

- Pylon Ducting (HVAC) Enamel

- Fuselages

- Inlets/Exhausts

- Environment Control Systems (ECS)

- Lavatories

- Waste Systems

By Sales Channel

- OEMs

- Aftermarket

Drivers

Increasing Commercial Aircraft Production and MRO Expansion Drive Market Growth

Rising commercial aircraft production backlogs at major aircraft manufacturers are generating strong and sustained demand for tube and duct assemblies. Airlines worldwide are expanding their fleets to meet growing air passenger traffic. Consequently, manufacturers are increasing assembly output, directly driving procurement volumes for precision-engineered tube and duct components across global supply chains.

The adoption of lightweight materials such as titanium, composites, and advanced aluminum alloys is significantly enhancing the performance and efficiency of tube and duct assemblies. These materials reduce overall aircraft weight and improve fuel economy. Moreover, material innovation is opening new design possibilities, further driving their use in modern aircraft systems.

Global MRO activities are expanding rapidly as airline fleets age and flight frequencies increase. This growth is generating consistent replacement demand for tube and duct components that degrade under heat, pressure, and vibration over time. Additionally, regulatory requirements for scheduled maintenance intervals ensure ongoing procurement of certified replacement assemblies from qualified component suppliers.

Restraints

Stringent Certification Requirements and Custom Design Complexity Limit Market Growth

Aviation certification and compliance requirements enforced by bodies such as the FAA and EASA impose strict standards on tube and duct assembly design, testing, and approval. These rigorous processes significantly extend product development timelines. Consequently, new entrants and smaller manufacturers face considerable challenges in bringing certified products to market within competitive timeframes.

Custom design and integration requirements for tube and duct assemblies add significant complexity to the manufacturing process. Each aircraft program often requires unique routing paths, connector types, and material specifications. This customization extends lead times and increases engineering costs, limiting the scalability of production and making it difficult to achieve economies of scale.

Together, these restraints create bottlenecks in the supply chain and increase the risk of delivery delays for aircraft programs. High qualification costs and lengthy approval cycles also discourage investment in new product development. Therefore, manufacturers must allocate significant resources to compliance management, which can divert attention and capital away from innovation and capacity expansion.

Growth Factors

Advanced Materials, UAM Platforms, and Smart Tubing Systems Accelerate Market Expansion

The integration of advanced composite and titanium alloys into tube and duct assemblies presents a significant growth opportunity for the market. These materials offer superior weight reduction, corrosion resistance, and thermal performance. Additionally, as aircraft manufacturers prioritize fuel efficiency and structural optimization, demand for assemblies made with these advanced materials is expected to rise steadily.

The emergence of Urban Air Mobility platforms and eVTOL aircraft is creating a new demand frontier for tube and duct assemblies. These next-generation aircraft require compact, lightweight, and highly durable ducting solutions. Moreover, increasing investment from aviation startups and established aerospace companies in UAM technology is expanding the total addressable market significantly.

Smart tubing systems embedded with sensors for real-time performance monitoring represent a transformative growth opportunity. These systems enable predictive maintenance by detecting pressure drops, temperature anomalies, and structural stress in duct assemblies. Consequently, adoption of sensor-integrated ducting reduces unplanned downtime and improves aircraft operational reliability, attracting strong interest from airlines and MRO providers.

Emerging Trends

Additive Manufacturing, Advanced Materials, and Digital Twins Reshape the Market Landscape

Additive manufacturing is emerging as a transformative production method for complex tube and duct geometries in aerospace applications. This technology enables manufacturers to produce intricate shapes with fewer components and reduced joint points. Furthermore, it shortens production lead times and improves design flexibility, making it increasingly attractive for both new aircraft programs and MRO applications.

Growing use of corrosion-resistant and high-temperature resistant materials is a key trend shaping product development in this market. Materials such as Inconel, titanium, and advanced composites are being adopted to meet the demanding thermal and chemical conditions of modern aircraft systems. Additionally, these materials extend assembly service life, lowering overall lifecycle costs for operators.

Digital twin technology is gaining traction in the design and performance optimization of aircraft tube and duct assemblies. By creating virtual replicas of physical assemblies, engineers can simulate operational conditions, detect design weaknesses, and optimize performance before production. Consequently, digital twin adoption is reducing prototyping costs and improving product quality across the aerospace supply chain.

Regional Analysis

North America Dominates the Aircraft Tube and Duct Assemblies Market with a Market Share of 38.50%, Valued at USD 1 Billion

North America holds the leading position in the global Aircraft Tube and Duct Assemblies Market, accounting for a 38.50% share valued at approximately USD 1 Billion. The region benefits from a well-established aerospace manufacturing base, high defense spending, and significant commercial aircraft production activity. Strong OEM procurement networks and advanced MRO infrastructure further reinforce North America’s market dominance.

Europe Aircraft Tube and Duct Assemblies Market Trends

Europe represents a significant market for aircraft tube and duct assemblies, driven by its strong commercial aviation sector and established aerospace manufacturing capabilities. The region supports leading aircraft production programs, generating steady demand for high-quality duct and tube components. Additionally, growing defense modernization efforts across European nations are supporting procurement of advanced ducting solutions.

Asia Pacific Aircraft Tube and Duct Assemblies Market Trends

Asia Pacific is the fastest-growing region in the aircraft tube and duct assemblies market, driven by rapidly expanding aviation sectors in China, India, and Southeast Asia. Increasing aircraft deliveries, growing airline fleets, and rising domestic air travel demand are fueling procurement of tube and duct assemblies. Moreover, the region is attracting new aerospace manufacturing investments from global players.

Middle East and Africa Aircraft Tube and Duct Assemblies Market Trends

The Middle East and Africa region presents steady growth opportunities for the aircraft tube and duct assemblies market. Expansion of airline fleets and growing aviation infrastructure investments are driving demand across the region. Additionally, defense procurement programs in Gulf nations are increasing demand for military aircraft components, including specialized tube and duct assemblies designed for harsh operating environments.

Latin America Aircraft Tube and Duct Assemblies Market Trends

Latin America represents an emerging market for aircraft tube and duct assemblies, supported by fleet expansion and MRO growth in Brazil and Mexico. The region’s aviation sector is gradually recovering and modernizing, driving both replacement and new supply demand. Furthermore, increasing regional air connectivity initiatives are expected to support long-term procurement of tube and duct components.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Eaton is a global leader in aerospace fluid conveyance and ducting systems, serving both commercial and defense aviation markets. The company provides a broad portfolio of hose assemblies, tube fittings, and duct systems engineered to meet stringent aerospace certification standards. Eaton continues to expand its capabilities through strategic acquisitions and targeted manufacturing facility investments, reinforcing its leadership across global aircraft programs.

Fiber Dynamics, Inc. specializes in the design and manufacture of flexible aircraft ducting and insulation systems for aerospace applications. The company serves both OEM and aftermarket customers with a focused product range covering thermal, acoustic, and environmental control system ducting. Fiber Dynamics is recognized for its engineering expertise and ability to deliver customized solutions that meet precise aircraft program requirements.

AmCraft Manufacturing is a U.S.-based manufacturer known for producing high-quality flexible ducting solutions for the aerospace and aviation industry. The company offers a broad range of lightweight, durable duct assemblies used in ECS, HVAC, and airflow management applications. AmCraft’s products are engineered to meet demanding performance standards and are deployed across both commercial and general aviation platforms globally.

Woolf Aircraft Products Inc. is a specialized manufacturer offering precision tube assemblies, fluid fittings, and related aerospace components. The company focuses on delivering high-reliability products for both OEM and MRO customers in the civil and military aviation sectors. Woolf Aircraft is noted for its quality-driven manufacturing approach and its ability to meet strict aerospace industry specifications and certification requirements.

Key Players

- Eaton

- Fiber Dynamics, Inc.

- AmCraft Manufacturing

- Woolf Aircraft Products Inc.

- PMF Industries, Inc.

- Flexaust, Inc.

- STEICO Industries Inc.

- RSA Engineered Products LLC

- Smiths Group plc

- Senior plc

- PFW Aerospace GmbH

Recent Developments

- January 2026 – TransDigm Group announced the acquisition of Jet Parts Engineering and Victor Sierra Aviation for approximately USD 2.2 billion, significantly strengthening its aerospace components portfolio. This strategic move is expected to enhance TransDigm’s supply capabilities for aircraft tube, duct, and related fluid system components across multiple aviation programs.

- December 2025 – Rangsons secured a long-term contract with Airbus for the supply of A320 aircraft components, marking a significant milestone in its aerospace manufacturing expansion. This partnership reinforces Rangsons’ position as a trusted supplier in the global commercial aviation supply chain.

- November 2025 – Eaton announced an expansion of its aerospace components manufacturing facility in the Town of Middlesex, backed by a USD 6.8 million investment. This capacity expansion is aimed at increasing production output to meet growing demand across commercial and defense aviation programs.

- June 2025 – Eaton signed an agreement to acquire Ultra PCS Limited, aiming to strengthen its presence in fast-growing aerospace markets. This acquisition is expected to broaden Eaton’s product range and enhance its competitive position in aircraft fluid and ducting system solutions globally.

Report Scope

Report Features Description Market Value (2025) USD 2.6 Billion Forecast Revenue (2035) USD 5.2 Billion CAGR (2026-2035) 7.2% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Aircraft Type (Commercial Aircraft, Narrow Body Aircraft, Wide Body Aircraft, Regional Jets, Fighter Jets, Military Aircraft), By Material (Aluminum, Steel, Nickel, Titanium, Composite, Inconel), By Duct Type (Rigid, Semi-Rigid, Flexible), By Application (Engine Bleeds, Thermal Anti-Ice, Pylon Ducting (HVAC) Enamel, Fuselages, Inlets/Exhausts, Environment Control Systems (ECS), Lavatories, Waste Systems), By Sales Channel (OEMs, Aftermarket) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Eaton, Fiber Dynamics, Inc., AmCraft Manufacturing, Woolf Aircraft Products Inc., PMF Industries, Inc., Flexaust, Inc., STEICO Industries Inc., RSA Engineered Products LLC, Smiths Group plc, Senior plc, PFW Aerospace GmbH Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Aircraft Tube and Duct Assemblies MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Aircraft Tube and Duct Assemblies MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Eaton

- Fiber Dynamics, Inc.

- AmCraft Manufacturing

- Woolf Aircraft Products Inc.

- PMF Industries, Inc.

- Flexaust, Inc.

- STEICO Industries Inc.

- RSA Engineered Products LLC

- Smiths Group plc

- Senior plc

- PFW Aerospace GmbH

Our Clients

- 183022

- March 2026