Quick Navigation

- Report Overview

- Key Takeaways

- U.S. Aerospace Semiconductor Market

- Component Analysis

- Application Analysis

- End-Use Industry Analysis

- Key Market Segments

- Driver

- Restraint

- Opportunity

- Challenge

- Emerging Trends

- Business Benefits

- Key Regions and Countries

- Key Player Analysis

- Top Opportunities Awaiting for Players

- Recent Developments

- Report Scope

Report Overview

The Global Aerospace Semiconductor Market size is expected to be worth around USD 15 Billion By 2034, from USD 7.1 Billion in 2024, growing at a CAGR of 8.00% during the forecast period from 2025 to 2034. In 2024, North America held over 38% of the aerospace semiconductor market, with revenues around $2.6 billion. The U.S. market was valued at $2.5 billion and is expected to grow at a CAGR of 6.2%.

The aerospace semiconductor market is primarily driven by the increasing demand for advanced aerospace technologies, such as satellite systems, autonomous aircraft, and high-performance communication networks. The growing need for lightweight, energy-efficient components in space and aviation applications is a critical factor boosting the market’s expansion.

The growth of the aerospace semiconductor market is driven by several key factors such as the increasing complexity and capability of modern aircraft and spacecraft require more advanced semiconductor solutions. There is a growing emphasis on enhancing the safety and efficiency of aerospace operations, which drives demand for sophisticated electronics that semiconductors enable.

Additionally, the expansion of satellite networks for global communication and observation is further propelling the market. Ongoing technological advancements in semiconductor manufacturing, which improve performance and reduce costs, also contribute significantly to the expansion of this market.

Emerging trends in the aerospace semiconductor market include the integration of IoT technologies, improving connectivity and functionality for smarter, more connected fleets. This enhances aviation safety and efficiency. Additionally, there’s a focus on miniaturization and weight reduction, driving the production of smaller, lighter, and more powerful chip solutions.

Technological innovations in the aerospace sector focus on improving semiconductor capability and reliability. Materials like silicon carbide (SiC) and gallium nitride (GaN) are used for their ability to handle extreme temperatures and voltages. Additionally, advancements in 3D packaging allow for more components in smaller spaces, vital for aerospace applications.

The aerospace semiconductor market is expanding due to the adoption of electric and hybrid propulsion systems in aircraft, which require advanced semiconductors for efficient power management. Additionally, the growth of aerospace industries in regions like Asia-Pacific presents significant opportunities for semiconductor manufacturers.

Key Takeaways

- The Global Aerospace Semiconductor Market size is projected to reach approximately USD 15 billion by 2034, growing from USD 7.1 billion in 2024, at a CAGR of 8.00% during the forecast period from 2025 to 2034.

- In 2024, Integrated Circuits (ICs) held a dominant position in the aerospace semiconductor market, capturing more than a 35% share.

- The Avionics Systems & Flight Control segment captured more than a 30% share of the aerospace semiconductor market in 2024.

- In 2024, the Commercial Aviation segment held a dominant market position, capturing more than a 52% share of the aerospace semiconductor market.

- In 2024, North America dominated the aerospace semiconductor market, capturing more than a 38% share, with revenues amounting to approximately $2.6 billion.

- The U.S. aerospace semiconductor market was valued at $2.5 billion in 2024 and is projected to grow at a CAGR of 6.2%.

U.S. Aerospace Semiconductor Market

In 2024, the U.S. aerospace semiconductor market was valued at $2.5 billion. It is projected to grow at a compound annual growth rate (CAGR) of 6.2%. The growth in the aerospace semiconductor market is driven by advancements in semiconductor technology, rising demand for efficient and reliable aerospace components, and increased investment in R&D.

Semiconductors are crucial in navigation, communication, and propulsion systems, with the demand for high-quality solutions surging as aircraft and spacecraft require more sophisticated electronics for safety and efficiency.

The shift toward electric and autonomous aircraft is increasing demand for specialized semiconductors that can perform in harsh environments. Additionally, government and defense spending in the U.S. on aerospace technologies, including military and space exploration projects, is boosting the market. These factors contribute to a strong growth trajectory for the U.S. aerospace semiconductor market.

In 2024, North America held a dominant market position in the aerospace semiconductor market, capturing more than a 38% share, with revenues amounting to approximately $2.6 billion. This prominent standing is primarily driven by the presence of major aerospace manufacturers and intense technological advancements in the region.

The region’s innovation ecosystem, supported by a robust infrastructure of research institutions and collaborative initiatives between universities, aerospace companies, and semiconductor manufacturers, fuels the development of cutting-edge semiconductor technologies. These advancements are critical for enhancing the performance and safety of aerospace systems.

North America’s strict aerospace safety and quality regulations drive semiconductor manufacturers to produce highly reliable and high-performance products for critical applications. This regulatory environment pushes technological innovation and ensures ongoing investment in R&D, supporting the long-term growth of this market.

The U.S. and Canada’s focus on national security and space exploration accelerates the adoption of next-generation aerospace technologies. Efforts to modernize military aircraft and expand space missions drive the demand for advanced semiconductors, positioning North America as a leader in the global aerospace semiconductor market with strong growth prospects.

Component Analysis

In 2024, the Integrated Circuits (ICs) segment held a dominant position in the aerospace semiconductor market, capturing more than a 35% share. This segment comprises microprocessors, microcontrollers, digital signal processors (DSPs), and application-specific integrated circuits (ASICs).

The strong performance of ICs can be attributed to their critical role in enhancing the computational capabilities and efficiency of aerospace systems. As modern aerospace applications become more data-intensive and complex, the demand for powerful ICs that can process large amounts of data reliably and quickly continues to grow.

Microprocessors and microcontrollers are particularly significant within the IC segment, as they serve as the central units for managing the functions and operations of aerospace hardware. Their ability to execute a series of programmed instructions makes them indispensable for flight control systems, navigation, and other onboard automated systems.

Digital Signal Processors (DSPs) also contribute notably to the IC segment’s leadership. DSPs are essential for processing real-time signals such as audio, video, and sensor data, which are crucial for communication and monitoring systems in aerospace. Their ability to handle high-speed signal processing tasks with efficiency ensures their continued adoption in both commercial and military aerospace applications.

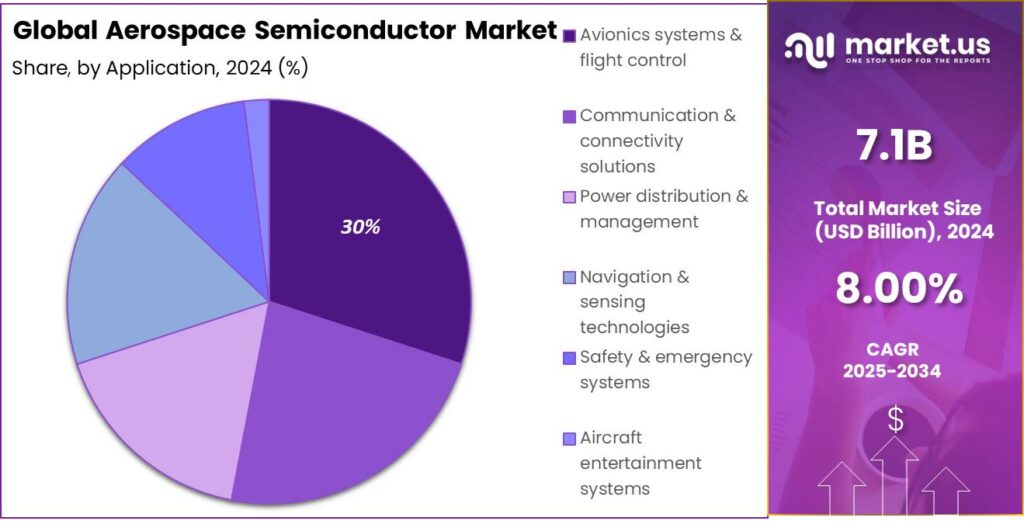

Application Analysis

In 2024, the Avionics Systems & Flight Control segment held a dominant market position, capturing more than a 30% share of the aerospace semiconductor market. This segment’s leadership is primarily attributed to the critical role that avionics play in modern aircraft, encompassing everything from navigation to aircraft stability systems.

The Communication & Connectivity Solutions segment has seen significant growth due to the rising need for seamless global connectivity. As airlines aim to improve passenger experience and operational efficiency, the demand for advanced communication semiconductors has surged.

Power distribution and management is a key segment in the aerospace semiconductor market. With aircraft electrification, there is a rising need for reliable semiconductors to efficiently manage power. These semiconductors optimize electric and hybrid systems, reduce energy consumption, and enhance safety through improved power control.

The Navigation & Sensing Technologies segment is crucial to aerospace, ensuring precision and reliability. Advanced semiconductors support GPS systems, weather radar, and other sensors essential for safe aircraft operations. As sensor technology improves, the demand for high-performance semiconductors to process real-time data drives market growth.

End-Use Industry Analysis

In 2024, the Commercial Aviation segment held a dominant market position in the aerospace semiconductor market, capturing more than a 52% share. This leading position is largely attributed to the global expansion of commercial airline fleets and the increasing incorporation of digital and electronic technologies in aircraft.

The push for more fuel-efficient and eco-friendly aircraft has driven innovations in semiconductor applications like power management, flight control, and communication systems. As airlines aim to reduce costs and improve safety and passenger experience, the demand for advanced electronics relying on sophisticated semiconductors continues to grow.

Additionally, the modernization of air traffic management systems to accommodate increasing air traffic and ensure safety operations has propelled the need for upgraded semiconductor components. These systems rely heavily on advanced electronics for navigation, surveillance, and communication, further cementing the critical role of semiconductors in commercial aviation.

The recovery of the commercial aviation sector, along with the growth in tourism and business travel, drives significant investment in new aircraft technologies. This resurgence fuels the expansion of the semiconductor market, as airlines invest in next-generation aircraft with advanced semiconductor technology to enhance efficiency, safety, and passenger comfort.

Key Market Segments

By Component

- Integrated Circuits (ICs)

- Microprocessors

- Microcontrollers

- Digital Signal Processors (DSPs)

- Application-Specific Integrated Circuits (ASICs)

- Discrete Components

- Transistors

- Diodes

- Sensors

- Pressure Sensors

- Temperature Sensors

- Motion Sensors

- Optoelectronics

- LEDs

- Infrared Devices

- Memory Devices

- DRAM

- Flash Memory

By Application

- Avionics systems & flight control

- Communication & connectivity solutions

- Power distribution & management

- Navigation & sensing technologies

- Safety & emergency systems

- Aircraft entertainment systems

By End-Use Industry

- Commercial Aviation

- Military Aviation

- Space Exploration

- Unmanned Aerial Vehicles (UAVs)

Driver

Increasing Demand for Air Travel

The aerospace semiconductor market is experiencing significant growth, primarily driven by the rising demand for air travel worldwide. As more people choose to fly, airlines are expanding their fleets, leading to a surge in aircraft production.

Emerging economies, particularly in the Asia-Pacific region, are witnessing a rapid increase in middle-class populations with disposable incomes. This demographic shift results in higher air travel demand, prompting airlines to acquire more aircraft.

Technological advancements in aerospace, such as the development of more fuel-efficient engines and enhanced navigation systems, also contribute to this demand. Modern aircraft are equipped with complex electronic systems that rely on high-performance semiconductors to function effectively.

Restraint

Supply Chain Disruptions

Despite the positive growth trajectory, the aerospace semiconductor market faces challenges due to supply chain disruptions. Global events, such as the COVID-19 pandemic, have exposed vulnerabilities in the supply chain, leading to component shortages and production delays. These disruptions have significantly impacted the timely delivery of semiconductor components essential for aerospace applications.

Additionally, geopolitical tensions have prompted companies to reassess their supply dependencies. For instance, reliance on suppliers from specific countries has become a concern, leading to efforts to diversify supply sources.

Diversifying suppliers helps mitigate risks from geopolitical conflicts and trade disputes that can disrupt supply chains. However, building new supplier relationships and qualifying alternative sources presents short-term challenges due to the time and resources required.

Opportunity

Technological Advancements in Semiconductor Materials

The aerospace semiconductor market stands to benefit from ongoing technological advancements in semiconductor materials. Innovations in materials science are leading to the development of semiconductors that offer superior performance, durability, and efficiency, which are crucial for aerospace applications.

One notable advancement is the increasing use of gallium nitride (GaN) semiconductors. GaN offers higher electron mobility than traditional silicon, enabling devices to operate at higher voltages and frequencies with greater efficiency.

Another promising development is the exploration of radiation-hardened semiconductor chips designed to withstand extreme environmental conditions encountered in aerospace settings. These chips are engineered to resist damage from ionizing radiation, ensuring reliable operation in high-altitude and space environments.

Challenge

Regulatory and Certification Complexities

The aerospace semiconductor industry must navigate a complex landscape of regulatory standards and certification processes. Ensuring that semiconductor components meet stringent safety, performance, and reliability criteria is essential for their integration into aerospace systems. The process of achieving certification can be time-consuming and resource-intensive.

Developing new semiconductor technologies for aerospace applications involves extensive testing and validation to comply with industry-specific regulations. These processes ensure components endure harsh aerospace conditions like extreme temperatures, radiation, and stress. The stringent standards mean even small design changes require thorough reevaluation, potentially delaying product development and deployment.

Emerging Trends

The aerospace semiconductor landscape in 2025 is being shaped by several key trends that leverage advanced technologies to meet the growing demands of the industry. One notable trend is the adoption of 3D stacking in memory technologies, such as DRAM and NAND flash, which is crucial for AI-driven applications requiring increased computational power and storage capabilities.

Additionally, the integration of AI on-device for vision tasks is gaining momentum. This technology allows AI and imaging processing to be run on the same chip, enhancing performance while reducing power consumption and costs

Another significant advancement is in the materials used for power components. Innovations with silicon carbide (SiC) and gallium nitride (GaN) are transforming power solutions in aerospace, offering higher efficiency and compact designs critical for sustainable operations.

Business Benefits

The incorporation of advanced semiconductors in the aerospace sector brings numerous business benefits, addressing both operational needs and strategic goals. Enhanced computational capabilities enable better data handling and real-time processing vital for autonomous systems and UAVs, which are increasingly used in both military and commercial aerospace applications.

The shift to on-device AI processing reduces latency and dependency on cloud services, which is vital for aerospace operations’ critical response times. Economically, increased local semiconductor production, as seen in the U.S., strengthens supply chains and enhances the security of essential aerospace components.

Advanced semiconductors drive innovation and global competitiveness by boosting aerospace system performance and efficiency. This enhances customer satisfaction and creates new opportunities, especially in advanced air mobility and commercial space exploration, which depend on high-performance semiconductor technologies.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

- Texas Instruments (TI) is a major player in the aerospace semiconductor market, known for its broad range of analog and mixed-signal chips. TI’s semiconductors are designed for mission-critical applications such as communication, sensing, and control systems used in aircraft and spacecraft. The company’s focus on reliability, low power consumption, and robust performance in extreme conditions makes its products essential for the aerospace industry.

- Analog Devices is another key player that specializes in high-performance analog, mixed-signal, and digital signal processing (DSP) semiconductors. Their products are widely used in aerospace applications that require precision and accuracy, such as radar systems, navigation, and flight control systems.

- Microchip Technology has established itself as a significant player in aerospace semiconductors, offering a wide range of solutions that meet the stringent demands of the industry. Their products are commonly used in satellite systems, avionics, and military applications. Microchip’s strengths lie in providing highly reliable and secure semiconductors, which are crucial for mission-critical operations.

Top Key Players in the Market

- Texas Instruments

- Analog Devices

- Microchip Technology

- STMicroelectronics

- Infineon Technologies

- ON Semiconductor

- Teledyne Technologies

- Renesas Electronics

- Xilinx

- Skyworks Solutions

- Qorvo

- Lattice Semiconductor

- Semtech Corporation

- Marvell Technology

- Rambus

- Nordic Semiconductor

- Silicon Laboratories

- Vishay Intertechnology

- Diodes Incorporated

- ROHM Semiconductor

- NXP Semiconductors

- Other Key Players

Top Opportunities Awaiting for Players

- Expansion of Advanced Air Mobility (AAM) Solutions: Mobility, which includes electric vertical takeoff and landing (eVTOL) aircraft and urban air mobility solutions. These innovations require specialized semiconductors for navigation, communication, and control systems. Companies that develop and supply these components stand to benefit from the growing demand in this emerging market.

- Integration of Artificial Intelligence (AI) in Aerospace Systems: Artificial intelligence is transforming aerospace operations, from predictive maintenance to autonomous flight systems. Semiconductors capable of handling complex AI computations are essential for these applications. The increasing adoption of AI in aerospace presents a substantial opportunity for semiconductor manufacturers to supply the necessary hardware.

- Expansion of IoT and Sensor Technologies: The military and aerospace sectors are extensively adopting IoT and sensor technologies for enhanced monitoring and operation efficiencies. This adoption is spurring the need for semiconductors that can facilitate real-time communication and data processing capabilities.

- Advancements in Satellite Technology: The proliferation of small satellites and constellations for communication, Earth observation, and navigation is creating a demand for compact, high-performance semiconductors. Companies that develop chips tailored for space applications, such as radiation-hardened components, are well-positioned to capitalize on this trend.

- Growth in Global Defense Spending: Many countries are ramping up their defense budgets, which includes modernizing military capabilities with new technologies. This expansion is a significant driver for the aerospace semiconductor market as advanced electronics become integral to new military equipment, including radar and communication systems.

Recent Developments

- In February 2025, IIT Madras and ISRO have successfully developed India’s first indigenous aerospace-grade semiconductor chip. By designing, developing, and fabricating the chip in-house, this achievement significantly reduces the risk of deploying systems vulnerable to backdoors or hardware Trojans, ensuring greater security and reliability for aerospace technologies.

- In early 2024, Marvell announced a new line of high-performance networking chips designed for aerospace applications, focusing on enhanced data processing capabilities for satellite communications.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 7.1 Bn |

| Forecast Revenue (2034) | USD 15 Bn |

| CAGR (2025-2034) | 8.00% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Integrated Circuits (ICs) (Microprocessors, Microcontrollers, Digital Signal Processors (DSPs), Application-Specific Integrated Circuits (ASICs)), Discrete Components (Transistors, Diodes), Sensors (Pressure Sensors, Temperature Sensors, Motion Sensors), Optoelectronics (LEDs, Infrared Devices), Memory Devices (DRAM, Flash Memory), By Application (Avionics systems & flight control, Communication & connectivity solutions, Power distribution & management, Navigation & sensing technologies, Safety & emergency systems, Aircraft entertainment systems), By End-Use Industry (Commercial Aviation, Military Aviation, Space Exploration, Unmanned Aerial Vehicles (UAVs)) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Texas Instruments, Analog Devices, Microchip Technology, STMicroelectronics, Infineon Technologies, ON Semiconductor, Teledyne Technologies, Renesas Electronics, Xilinx, Skyworks Solutions, Qorvo, Lattice Semiconductor, Semtech Corporation, Marvell Technology, Rambus, Nordic Semiconductor, Silicon Laboratories, Vishay Intertechnology, Diodes Incorporated, ROHM Semiconductor, NXP Semiconductors, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |