Global 3D Printing Dental Devices Market By Technology (Stereolithography (SLA), Digital Light Processing (DLP), Fused Deposition Modeling (FDM), Selective Laser Sintering (SLS), Polyjet Printing and Others), By Material Type (Resins, Metal, Ceramics and Photopolymer), By Application (Clear Aligner Models, Prosthodontics, Orthodontics, Implantology, Surgical Guides, Dental Models, Crowns and Bridges and Others), By End User (Dental Laboratories, Dental Clinics, Hospitals and Academic and Research Institutes), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 180918

- Number of Pages: 336

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

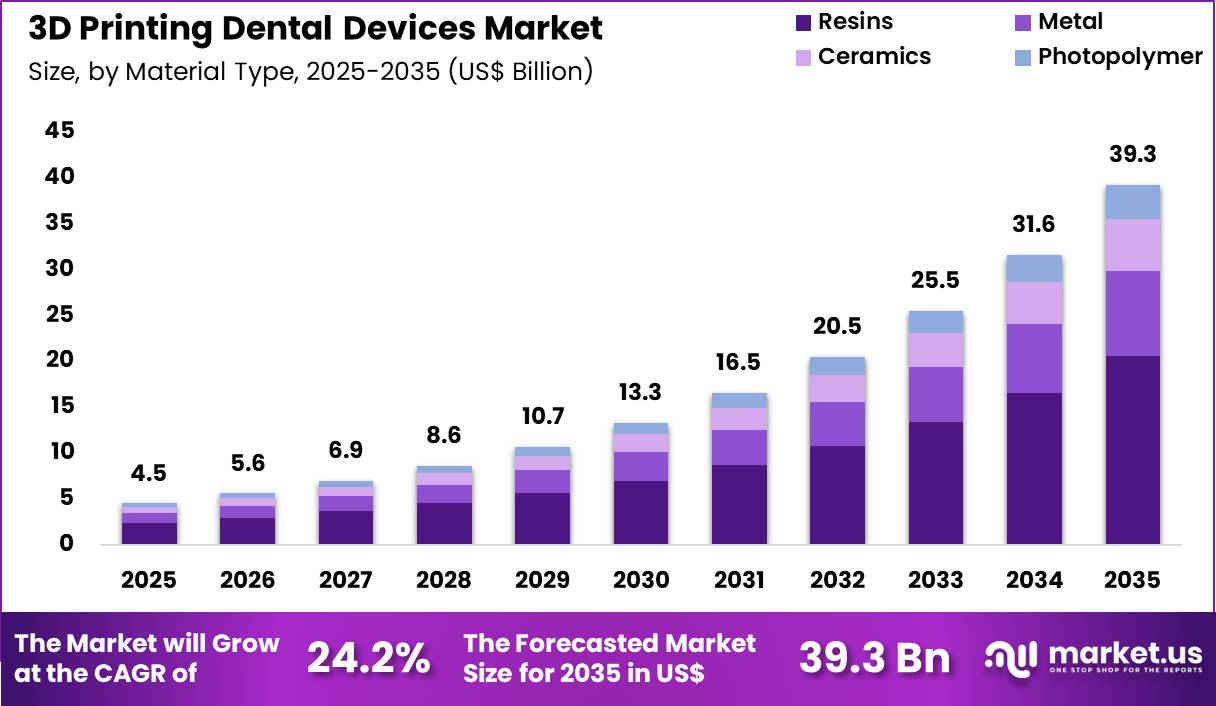

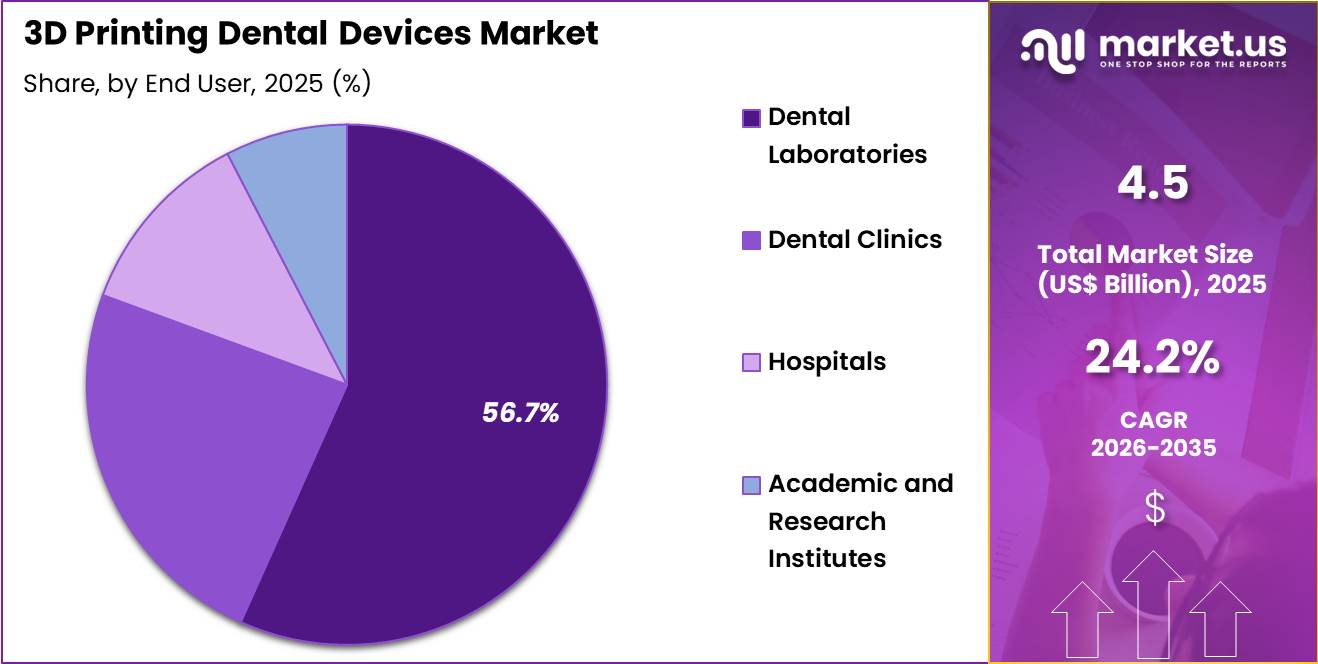

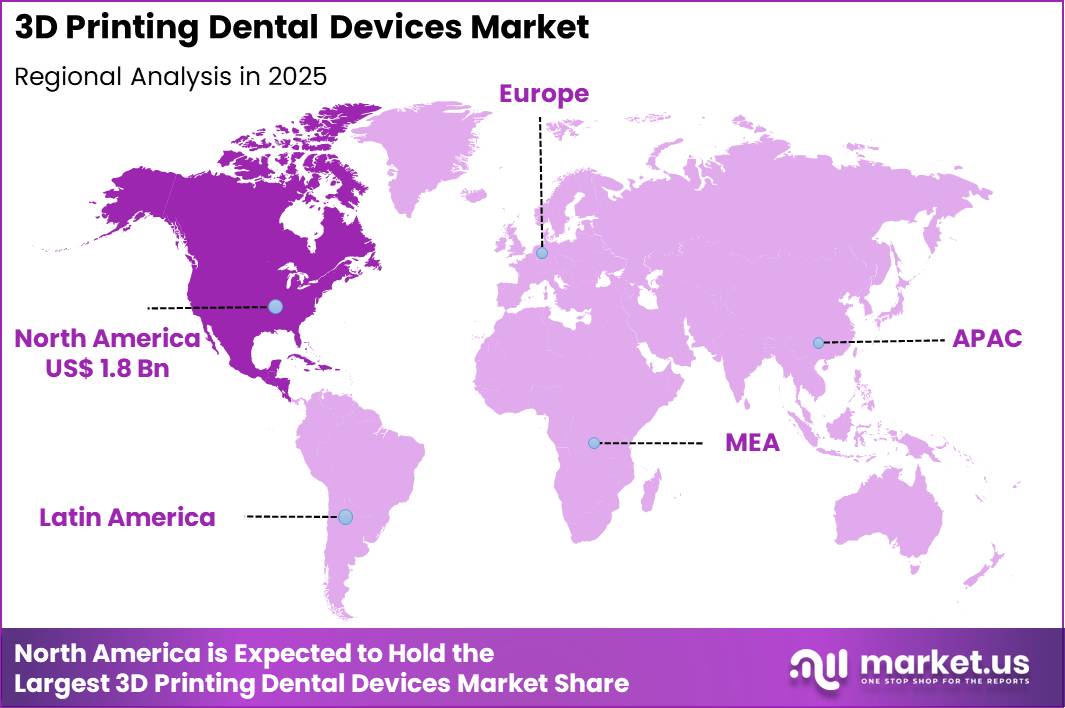

The Global 3D Printing Dental Devices Market size is expected to be worth around US$ 39.3 Billion by 2035 from US$ 4.5 Billion in 2025, growing at a CAGR of 24.2% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 39.5% share with a revenue of US$ 1.8 Billion.

Increasing adoption of digital dentistry and patient-specific solutions propels the 3D printing dental devices market as dental professionals seek technologies that deliver superior precision, customization, and efficiency in restorative and prosthetic workflows. Dental laboratories increasingly utilize 3D-printed crowns, bridges, and inlays to produce monolithic restorations from biocompatible resins, achieving high marginal fit and esthetic outcomes with reduced chairside adjustments.

These systems support orthodontic applications by fabricating clear aligners and retainers directly from digital scans, enabling rapid production of sequential appliances tailored to individual tooth movement plans. Oral surgeons apply 3D-printed surgical guides for implant placement, ensuring accurate positioning and angulation based on CBCT data to minimize complications and improve osseointegration success.

Prosthodontists employ 3D printing for removable partial dentures and complete dentures, creating lightweight frameworks and denture bases with optimized fit and reduced processing time compared to traditional methods. In pediatric and maxillofacial reconstruction, clinicians produce patient-specific obturators and craniofacial prostheses to restore function and appearance following trauma or congenital defects.

Manufacturers pursue opportunities to develop advanced biocompatible resins and multi-material printing capabilities, expanding applications in full-arch implant-supported prosthetics and hybrid restorations that combine printed frameworks with milled zirconia. Developers advance chairside 3D printing systems that enable same-day restorations, broadening utility in high-volume general practices and cosmetic dentistry.

These innovations facilitate integration with intraoral scanners and CAD software for seamless digital workflows. Opportunities emerge in sustainable, recyclable printing materials that maintain clinical performance while addressing environmental concerns. Companies invest in automated post-processing solutions to streamline finishing and polishing, reducing labor time.

In February 2025, Formlabs formed a strategic commercial relationship with Henry Schein to accelerate the use of digital dental production technologies. Through this arrangement, Henry Schein distributes Formlabs’ dental 3D printers across North America, helping dental laboratories adopt faster digital workflows for restorative and prosthetic applications.

In March 2025, Stratasys expanded its European footprint in dental additive manufacturing through partnerships with Nueva Galimplant in Spain and Gold Quadrat and Metaux Precieux in Germany. These collaborations broaden access to Stratasys’ dental printing technologies, including its full-color digital denture systems, enabling laboratories to improve production efficiency and reduce manual fabrication time.

Recent trends emphasize patient-specific design, chairside production, and hybrid manufacturing, positioning the market for growth in precision, speed, and cost-effective dental care delivery.

Key Takeaways

- In 2025, the market generated a revenue of US$ 4.5 Billion, with a CAGR of 24.2%, and is expected to reach US$ 39.3 Billion by the year 2035.

- The technology segment is divided into stereolithography (SLA), digital light processing (DLP), fused deposition modeling (FDM), selective laser sintering (SLS), polyjet printing and others, with stereolithography (sla)taking the lead with a market share of 58.4%.

- Considering material type, the market is divided into resins, metal, ceramics and photopolymer. Among these, resins held a significant share of 52.4%.

- Furthermore, concerning the application segment, the market is segregated into clear aligner models, prosthodontics, orthodontics, implantology, surgical guides, dental models, crowns and bridges and others. The clear aligner models sector stands out as the dominant player, holding the largest revenue share of 42.2% in the market.

- The end user segment is segregated into dental laboratories, dental clinics, hospitals and academic and research institutes, with the dental laboratories segment leading the market, holding a revenue share of 56.7%.

- North America led the market by securing a market share of 39.5%.

Technology Analysis

Stereolithography accounted for 58.4% of growth within technology and dominate the 3D printing dental devices market due to its high precision and ability to produce detailed dental structures. SLA printers generate extremely fine layers that replicate complex dental anatomy required for orthodontic appliances and prosthetic components.

Dental professionals increasingly adopt SLA systems to manufacture aligner molds, surgical guides, and dental models with high accuracy. The American Dental Association reports that orthodontic treatments continue to expand globally as more adults seek cosmetic dental correction, which drives demand for digitally produced appliances.

SLA technology is expected to remain dominant because it supports rapid production cycles and consistent quality in dental laboratories. Continuous improvements in photopolymer resins and printer resolution further strengthen adoption. Growing integration of digital dentistry workflows and intraoral scanning systems is projected to accelerate SLA technology usage in dental manufacturing.

Material Type Analysis

Resins accounted for 52.4% of growth within material type and dominate the market because they offer excellent printability, dimensional stability, and biocompatibility for dental applications. Dental laboratories rely heavily on photopolymer resins to produce orthodontic models, aligner molds, and surgical guides with precise surface quality.

Manufacturers continue to develop specialized dental resins designed for high mechanical strength and long-term oral compatibility. The demand for cosmetic dentistry procedures continues to grow as patients seek improved aesthetics and personalized dental solutions.

Resin materials allow technicians to fabricate highly customized dental devices that match patient-specific anatomy. The segment is anticipated to expand as dental clinics adopt chairside 3D printing technologies that rely heavily on resin-based materials. Continuous innovation in light-cured dental resins further improves strength, accuracy, and durability of printed devices.

Application Analysis

Clear aligner models accounted for 42.2% of growth within application and dominate the 3D printing dental devices market due to the rapid global expansion of orthodontic treatments using transparent aligners. Orthodontists increasingly replace traditional metal braces with clear aligner systems that provide improved aesthetics and patient comfort.

Aligners require a series of custom molds that guide gradual tooth movement, and 3D printing allows dental laboratories to manufacture these molds efficiently. The American Association of Orthodontists reports that orthodontic treatment demand among adults continues to increase significantly, which fuels the production of aligner systems.

The segment is expected to strengthen as digital orthodontics integrates intraoral scanning, treatment simulation software, and additive manufacturing technologies. Dental providers increasingly adopt digital workflows that support faster treatment planning and aligner production. Rising awareness of cosmetic dental treatments further contributes to the expansion of this application segment.

End-User Analysis

Dental laboratories accounted for 56.7% of growth within end users and dominate the 3D printing dental devices market due to their central role in manufacturing customized dental restorations and orthodontic components. Laboratories possess specialized equipment and technical expertise required for digital dental manufacturing workflows.

Technicians routinely use 3D printers to produce crowns, bridges, aligner molds, and surgical guides with high precision. Dental laboratories collaborate closely with dentists and orthodontists to translate digital patient scans into physical dental devices.

The adoption of digital dentistry continues to transform laboratory operations as additive manufacturing reduces production time and improves customization capabilities. Segment growth is expected to accelerate as laboratories invest in advanced printers, materials, and design software. Increasing demand for personalized dental treatments further strengthens the role of dental laboratories in the 3D printed dental devices ecosystem.

Key Market Segments

By Technology

- Stereolithography (SLA)

- Digital Light Processing (DLP)

- Fused Deposition Modeling (FDM)

- Selective Laser Sintering (SLS)

- Polyjet Printing

- Others

By Material Type

- Resins

- Metal

- Ceramics

- Photopolymer

By Application

- Clear Aligner Models

- Prosthodontics

- Orthodontics

- Implantology

- Surgical Guides

- Dental Models

- Crowns and Bridges

- Others

By End User

- Dental Laboratories

- Dental Clinics

- Hospitals

- Academic and Research Institutes

Drivers

Rising FDA clearances for 3D printed dental devices is driving the market.

The 3D printing dental devices market gains significant momentum from regulatory advancements that validate innovative solutions for clinical use. The U.S. Food and Drug Administration issued three notable clearances for dental technologies in 2025, facilitating broader integration into restorative and orthodontic practices.

These approvals encompass systems for enhanced imaging, aligner production, and prosthetic fabrication using additive manufacturing. Dental professionals increasingly adopt these cleared devices to achieve precise, patient-specific outcomes in procedures. The clearances underscore the maturing safety and efficacy profiles of 3D printed components.

Manufacturers respond by accelerating commercialization pipelines aligned with FDA standards. Educational programs for clinicians emphasize the benefits of cleared technologies in workflow optimization. Patients experience improved fit and comfort from customized restorations enabled by these innovations.

The regulatory endorsements stimulate investment in domestic production capabilities. This driver establishes a foundation for sustained market evolution through trusted, compliant offerings.

Restraints

Declining total revenue at Stratasys is restraining the market.

Stratasys Ltd., a prominent provider of 3D printing solutions including dental applications, reported total revenue of $627.6 million in fiscal year 2023. This figure decreased to $572.5 million in fiscal year 2024, representing an 8.8 percent contraction. Fiscal year 2025 revenue further declined to $551.1 million, a 3.7 percent drop from the previous year.

The successive reductions reflect broader challenges in hardware adoption amid economic pressures on dental labs. Suppliers encounter moderated demand for printers and materials tailored to dental workflows. Facilities postpone upgrades to 3D systems due to constrained capital budgets.

The revenue trajectory influences pricing adjustments for entry-level dental configurations. Innovation cycles slow as resources shift toward cost containment measures. Practitioners remain cautious in expanding 3D printing capabilities without clearer recovery signals. This restraint curtails the sector’s near-term expansion potential during the 2023-2025 period.

Opportunities

US$60 million funding round at Carbon is creating growth opportunities.

Carbon, a key innovator in digital light synthesis for dental aligners and models, secured $60 million in private equity funding on November 12, 2025. This infusion targets acceleration of advanced manufacturing platforms, with dental representing a core growth area. Opportunities emerge for scaled production of biocompatible resins optimized for intraoral applications.

The capital enables refinement of high-throughput printing for orthodontic labs handling volume orders. Developers can explore hybrid materials combining flexibility and durability for prosthetic uses. The funding supports expansion into underserved markets for clear aligner therapies.

Collaborative ventures with dental chains facilitate pilot programs for on-site fabrication. Enhanced throughput promises reduced lead times and inventory costs for providers. Such financial backing fosters integration of AI-driven design software with printing hardware. This opportunity strengthens the ecosystem for efficient, scalable 3D dental solutions.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions influence the 3D printing dental devices market through dental clinic investments, laboratory expansion plans, and patient spending on restorative treatments. Inflation raises costs for dental resins, metal powders, printing hardware, and post-processing equipment, which increases operational expenses for dental labs.

Higher interest rates reduce access to financing for small clinics and laboratories that plan to upgrade digital manufacturing systems. Geopolitical tensions disrupt the global supply of photopolymers, precision printer parts, and specialized dental materials, which creates procurement uncertainty.

Current US tariffs on imported 3D printing components and dental materials increase acquisition costs for equipment distributors and service providers. These pressures can delay technology upgrades and limit adoption among smaller dental practices.

At the same time, manufacturers invest in domestic material production and regional service networks to stabilize supply chains. Growing demand for customized dental restorations and digital dentistry workflows continues to support steady and confident market growth.

Latest Trends

FDA clearance for 3D Systems multi-material denture solution is driving the market.

3D Systems obtained U.S. Food and Drug Administration 510(k) clearance on October 9, 2025, for its multi-material denture solution enabling digital workflow completion. This approval covers the full commercial release of a system producing monolithic, multi-color dentures via additive manufacturing. The technology integrates gingiva and tooth components in a single print, streamlining laboratory processes.

Dentists benefit from enhanced esthetics and fit accuracy in removable prosthetics. The clearance validates the biocompatibility and mechanical performance of printed denture bases. Practices achieve cost efficiencies through reduced manual finishing steps.

The 2025 milestone aligns with demands for chairside customization in edentulous patients. Suppliers anticipate increased adoption in comprehensive digital dentistry suites. This development propels innovation in multi-material extrusion for restorative applications. Overall, the approval catalyzes a shift toward fully integrated 3D printed denture fabrication.

Regional Analysis

North America is leading the 3D Printing Dental Devices Market

North America accounted for 39.5% of the 3D printing dental devices market in 2025 as dental laboratories and clinics increasingly adopted digital manufacturing technologies for prosthetics, orthodontics, and surgical planning. The region’s strong dental care infrastructure and rapid integration of digital dentistry platforms have accelerated the transition from traditional casting techniques to additive manufacturing workflows.

According to the American Dental Association, about 202000 dentists were actively practicing in the United States in 2023, creating a large professional base that continues to adopt advanced dental technologies to improve treatment precision and efficiency. Dental laboratories across the United States and Canada are incorporating high resolution printers to produce crowns, bridges, aligner models, and surgical guides with improved turnaround times.

Orthodontic clinics are also expanding the use of digital scanning and printed aligner models to support customized treatment planning. Dental implant procedures and cosmetic dentistry demand have increased among adult patients seeking restorative and aesthetic treatments. Equipment manufacturers are introducing improved biocompatible resins and high speed printing platforms that enhance accuracy and clinical reliability.

Dental schools and research institutions across the region are integrating digital dentistry and additive manufacturing training into academic programs. These developments collectively strengthened the adoption of digital dental manufacturing technologies across North America in 2025.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to witness strong expansion during the forecast period as dental care infrastructure improves and digital dentistry adoption accelerates across emerging healthcare markets. Countries such as China, India, Japan, and South Korea are expanding dental clinics, laboratories, and academic institutions that support advanced oral healthcare technologies.

The World Health Organization reported in 2022 that oral diseases affect around 3.5 billion people globally, with a significant share of cases occurring across Asian populations, highlighting a large need for restorative and orthodontic treatments. Dental laboratories in the region are increasingly adopting digital scanning, computer aided design, and additive manufacturing technologies to produce customized dental components.

Growing awareness of aesthetic dentistry and orthodontic treatments among younger populations is also increasing demand for advanced dental solutions. Governments and private investors are strengthening dental education programs and clinical training infrastructure to support modern treatment techniques.

Regional manufacturers are introducing cost efficient printing materials and equipment designed for local dental laboratories. International dental technology companies are expanding partnerships with clinics and dental labs across Asia to accelerate digital dentistry adoption. These developments are expected to drive continued growth of digital dental manufacturing technologies across Asia Pacific in the coming years.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

Key participants in the 3D Printing Dental Devices market drive expansion through continuous innovation in digital dentistry workflows, advanced printing materials, and integrated design software that allows dentists to produce customized restorations with high precision.

Companies actively launch new printers, resins, and cloud-based design platforms to help dental clinics fabricate crowns, aligners, surgical guides, and prosthetics faster and more efficiently. Strategic collaborations, acquisitions, and product introductions also help manufacturers strengthen global market reach and enhance their competitive position.

3D Systems represents a notable player in the 3D Printing Dental Devices market and operates as a U.S.-based additive manufacturing company that develops advanced 3D printers, dental materials, and digital workflows for laboratories and dental clinics.

The firm supplies technologies used to create dentures, orthodontic models, and implant guides with high accuracy and reduced production time. Industry competitors such as Stratasys, Formlabs, and SprintRay continue to expand their portfolios and invest in research to accelerate adoption of digital dentistry technologies worldwide.

Top Key Players

- Stratasys, Ltd.

- 3D Systems Corporation

- EnvisionTEC US LLC (Desktop Health)

- Formlabs, Inc.

- Align Technology, Inc.

- SprintRay, Inc.

- Desktop Metal, Inc.

- Carbon, Inc.

- Shining 3D

- Roland DG Corporation

- Planmeca Oy

- DWS S.r.L.

- BEGO GmbH & Co. KG

- Prodways Group SA

- Asiga Pty. Ltd.

Recent Developments

- In October 2025, LuxCreo entered into a strategic collaboration with Angelalign Technology following a new investment agreement aimed at advancing materials used in the 3D printing of clear orthodontic aligners. The partnership is intended to support the development of stronger and more precise printing materials that can improve aligner durability and manufacturing efficiency in orthodontic production.

- In September 2025, SprintRay completed the acquisition of the dental-focused assets of EnvisionTEC/ETEC, formerly associated with Desktop Health. The deal transferred a range of intellectual property, product technologies, and related dental printing materials to SprintRay, strengthening the company’s capabilities in dental additive manufacturing and expanding its solutions for clinics and laboratories.

- In July 2025, 3D Systems introduced the NextDent Jetted Denture platform to the US dental market. The system enables production of fully integrated dentures through a single additive manufacturing process that combines multiple materials, allowing laboratories to produce prosthetics more efficiently while maintaining durability and aesthetic quality.

Report Scope

Report Features Description Market Value (2025) US$ 4.5 Billion Forecast Revenue (2035) US$ 39.3 Billion CAGR (2026-2035) 24.2% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Technology (Stereolithography (SLA), Digital Light Processing (DLP), Fused Deposition Modeling (FDM), Selective Laser Sintering (SLS), Polyjet Printing and Others), By Material Type (Resins, Metal, Ceramics and Photopolymer), By Application (Clear Aligner Models, Prosthodontics, Orthodontics, Implantology, Surgical Guides, Dental Models, Crowns and Bridges and Others), By End User (Dental Laboratories, Dental Clinics, Hospitals and Academic and Research Institutes) Regional Analysis North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America Competitive Landscape Stratasys, 3D Systems, EnvisionTEC, Formlabs, Align Technology, SprintRay, Desktop Metal, Carbon, Shining 3D, Roland DG, Planmeca, DWS, BEGO, Prodways, Asiga Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  3D Printing Dental Devices MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

3D Printing Dental Devices MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Stratasys, Ltd.

- 3D Systems Corporation

- EnvisionTEC US LLC (Desktop Health)

- Formlabs, Inc.

- Align Technology, Inc.

- SprintRay, Inc.

- Desktop Metal, Inc.

- Carbon, Inc.

- Shining 3D

- Roland DG Corporation

- Planmeca Oy

- DWS S.r.L.

- BEGO GmbH & Co. KG

- Prodways Group SA

- Asiga Pty. Ltd.

Our Clients

- 180918

- March 2026