Quick Navigation

Report Overview

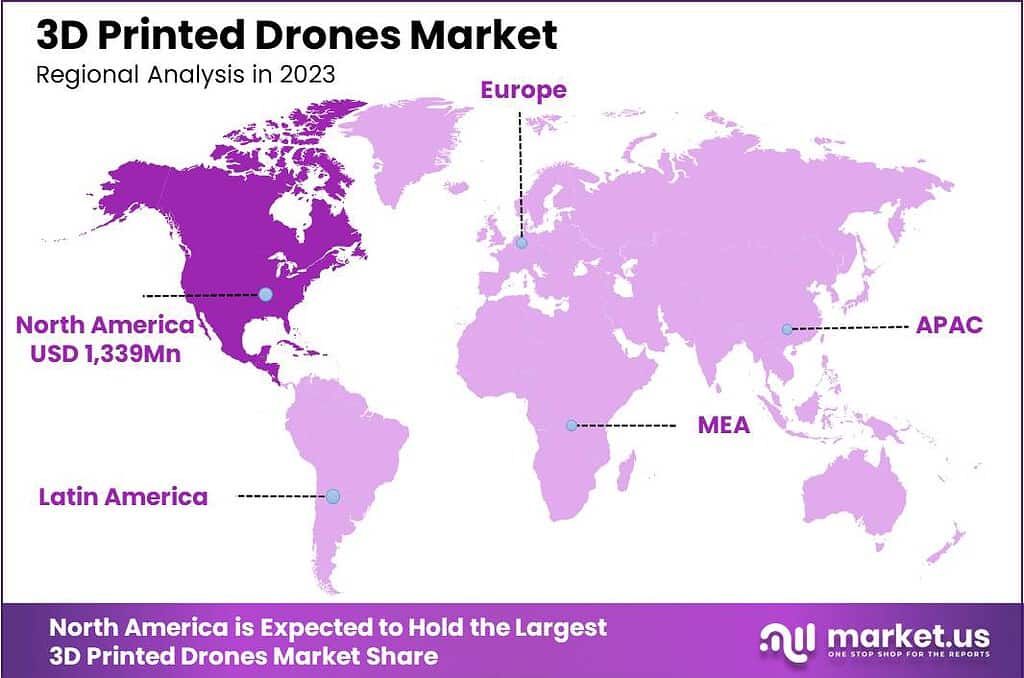

The Global 3D Printed Drones Market size is expected to be worth around USD 3,721 Million By 2033, from USD 581 Million in 2023, growing at a CAGR of 20.4% during the forecast period from 2024 to 2033. In 2023, North America held a dominant market position, capturing more than a 36.3% share, holding USD 1,339 Million revenue.

3D printed drones refer to unmanned aerial vehicles (UAVs) that incorporate components manufactured through 3D printing technology. This method, also known as additive manufacturing, involves creating physical objects by layering material based on digital models. 3D printing enables the production of complex, lightweight structures that are often difficult or expensive to build using traditional manufacturing techniques.

The market for 3D printed drones has been expanding as both the demand for drones and the accessibility of 3D printing technology grow. This sector spans various applications, including military, commercial, and recreational uses. Commercially, these drones are employed for tasks such as delivery services, aerial photography, and large-scale agriculture. On the recreational side, hobbyists often use 3D printed drones for racing and personal enjoyment.

The increasing versatility and declining costs of 3D printers have made them more accessible to manufacturers and hobbyists alike, further stimulating market growth. Key drivers for the 3D printed drones market include the advanced customization capabilities of 3D printing, which allow for rapid prototyping and design adjustments to meet specific operational requirements.

The cost efficiencies associated with 3D printing, reducing material waste and manufacturing expenses, also contribute significantly to its adoption. Additionally, the shorter supply chain for components facilitated by localized manufacturing processes is a crucial factor. Government and defense investments in drone technology further propel the market forward, reflecting a strategic emphasis on enhancing operational capabilities and readiness through advanced technologies.

Demand in the 3D printed drones market is largely driven by their increased utility in commercial applications such as surveying, mapping, and delivery services. The ability to customize drone components for specific tasks enhances their appeal to various industries. Moreover, as regulations surrounding drone operations continue to evolve, there is a growing need for adaptable and efficient UAV solutions, which 3D printing can provide.

The expanding scope of drone applications presents significant opportunities within the 3D printed drones market. For instance, as drone delivery services become more prevalent, there is a potential for a rise in demand for customized drones that can handle specific types of deliveries, such as medical supplies or food products. Furthermore, advancements in 3D printing materials, such as lighter and more durable composites, could open new avenues for drone applications in harsh or complex environments.

According to G2, the United States dominates the global 3D printing market, contributing $3.1 billion (22%) in market share. Europe is a powerhouse in the industry, with 52% of 3D printing businesses based there. The UK alone represents a significant chunk, with a market size of £468 million, making it Europe’s second-largest and fifth-largest globally.

Looking ahead, The Global 3D Printing Market size is expected to be worth around USD 135.4 Billion By 2033, from USD 19.8 Billion in 2023, growing at a CAGR of 21.2% during the forecast period from 2024 to 2033. Closer on the horizon, the UK market is set to expand to £685 million by 2026, driven by a CAGR of 10%.

Demand for 3D printing is on the rise, with 61% of users planning to increase investment, while only 36% are content with their current spending. On average, customers spend over £8,000 annually, and 23% of them invest nearly £80,000. However, cost remains a barrier, as highlighted by 55% of respondents who feel it limits more frequent use.

Germany plays a key role in metal additive manufacturing, producing 62% of PBF metal AM systems worldwide. The market for small industrial metal printers is expected to hit $1 billion by 2027, underscoring its growing appeal

Technological advancements in 3D printing have been crucial in propelling the 3D printed drones market forward. Improvements in 3D printing technologies have enabled the use of a wider range of materials, including high-performance thermoplastics and metals, which are ideal for drone components. Additionally, innovations in 3D printing techniques have led to faster production times and higher precision in manufactured parts, which are essential for the functionality and reliability of drones.

Key Takeaways

- The global 3D printed drones market is projected to grow significantly over the next decade. Valued at USD 581 million in 2023, it is expected to reach a remarkable USD 3,721 million by 2033, reflecting an impressive CAGR of 20.4% from 2024 to 2033.

- In 2023, North America emerged as the leading region, contributing to over 36.3% of the market share with revenues exceeding USD 1,339 million. This dominance is largely attributed to technological advancements and widespread adoption of 3D printing technologies in drone manufacturing.

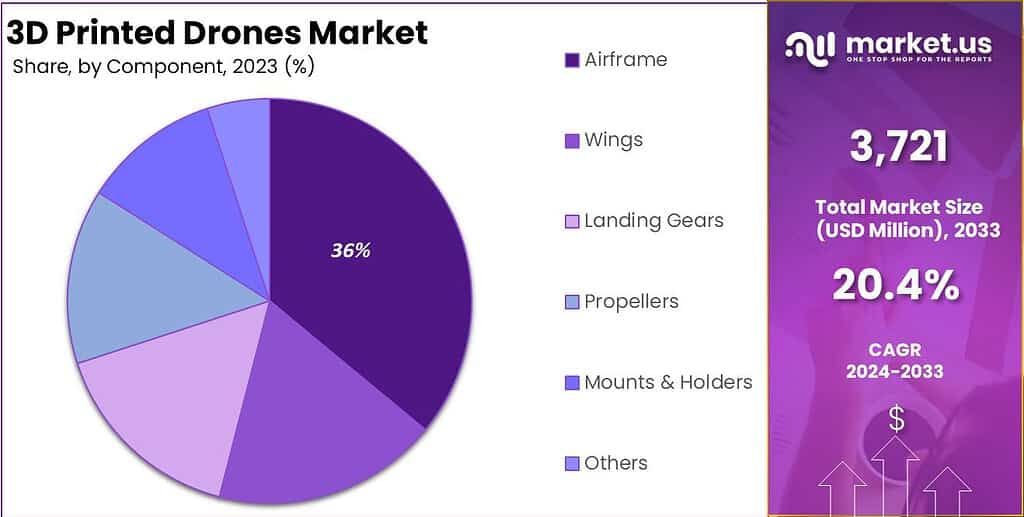

- The airframe segment played a crucial role in the market’s performance in 2023, holding more than 36.3% of the share. This segment continues to be a focal point for manufacturers, as 3D printing allows for lightweight, durable designs that enhance drone efficiency.

- Similarly, the Fused Deposition Modeling (FDM) technology stood out as the dominant technique, driven by its affordability and versatility across industries. FDM’s widespread application made it a preferred choice, strengthening its position in the 3D printed drones market.

- The multi-rotor drones segment captured significant attention in 2023, holding a dominant share due to its flexibility and operational efficiency. These drones have proven effective in various sectors, including military, commercial, and recreational applications, further boosting their demand.

- Lastly, the military segment led the market in 2023, fueled by substantial investments in advanced drone technologies for combat and surveillance.

AI’s Impact on 3D Printed Drones

The integration of artificial intelligence (AI) with 3D printing technology is revolutionizing the design and production of drones, enhancing their capabilities and efficiency. This collaboration enables drones to be designed and manufactured much faster, with a case in point being the U.S. Air Force’s ability to design and 3D print drones in under 48 hours, showcasing significant advancements in military technology and rapid deployment scenarios.

AI’s role extends beyond just speeding up production; it also improves the operational capabilities of drones. AI algorithms empower drones to autonomously perform complex tasks, adapt to dynamic environments, and make decisions in real-time. This technology is particularly useful in military applications where drones can perform reconnaissance missions without risking human lives, adapting to battlefield conditions autonomously.

Furthermore, the field of 3D printing itself is being transformed by AI, which is being used to optimize the printing process. This results in higher precision, efficiency, and material usage, which are critical in industrial applications. AI-driven 3D printing allows for the creation of more complex designs and structures that were previously challenging to achieve, thus broadening the scope of drone functionalities and applications.

Component Analysis

In 2023, the airframe segment of the 3D printed drones market held a dominant position, capturing more than a 36.3% share. This leading stance can be attributed to the critical role that airframes play in the structural integrity and overall functionality of drones.

Airframes, which include the main body of a drone, are essential for housing key components such as sensors, cameras, and batteries, and for providing the structural basis upon which other crucial elements like wings and propellers are mounted.

The predominance of the airframe component in the market is further supported by the advancements in 3D printing technologies that allow for the creation of complex, lightweight, and durable airframe designs. These advancements enhance the performance and efficiency of drones by optimizing aerodynamics and reducing weight, which is particularly beneficial in applications requiring long duration flights and high maneuverability.

Moreover, the ability to customize airframes through 3D printing caters to a diverse range of applications, from commercial and military to recreational uses, offering tailored solutions that meet specific operational requirements. This customization capability, coupled with reduced production times and costs, continues to drive the demand for 3D printed airframes, supporting their significant market share.

The sustained interest in developing and optimizing 3D printed airframes is indicative of their central importance to the drone’s operational capabilities and the broader push within the industry towards innovative manufacturing techniques that promise greater performance and cost efficiencies.

Technology Analysis

In 2023, the Fused Deposition Modeling (FDM) segment held a dominant market position in the 3D printed drones industry, capturing a substantial share due to its widespread adoption across various sectors. FDM’s popularity stems from its cost-effectiveness and accessibility, making it an attractive option for both newcomers and established entities in the field of 3D printing.

This technology is particularly favored for its ability to create durable, functional parts efficiently, which aligns well with the requirements for manufacturing drone components such as frames and housings. The robust growth of the FDM market is driven by continuous advancements in the technology, including improvements in printing speeds, resolution, and material compatibility.

These enhancements have expanded the potential applications of FDM in the drone market, from prototyping to the production of final drone components that require intricate details and high reliability. Moreover, the ability to use a variety of thermoplastic materials, such as ABS and PLA, allows manufacturers to tailor the properties of the drone components to specific operational needs, including lightweight or heat-resistant characteristics.

Additionally, the environmental and operational flexibility of FDM printers adds to their appeal. These printers are suitable for a variety of settings, from small-scale workshops to large manufacturing floors, and they offer ease of use and maintenance which is crucial for scaling production without requiring extensive technical know-how.

Type Analysis

In 2023, the multi-rotor segment held a dominant market position within the 3D printed drones market, capturing a significant share due to its versatility and operational efficiency across various industries, including military, commercial, and recreational applications.

The preference for multi-rotor drones stems from their ability to perform stable vertical take-offs and landings, maneuver in tight spaces, and hover in fixed positions, which are essential capabilities for applications ranging from aerial photography to surveillance and delivery services.

The adaptability of multi-rotor drones to incorporate various technological enhancements such as advanced sensors, cameras, and automated systems has further solidified their market dominance. These drones are particularly favored for tasks that require precise control and stationary hovering, attributes that are crucial for sectors such as real estate photography, environmental monitoring, and public safety operations.

The ability of multi-rotor drones to carry different payloads and perform under diverse operational demands also contributes to their widespread use. Technological advancements have played a pivotal role in the evolution of multi-rotor drones. Innovations in battery life, propulsion systems, and lightweight materials developed through 3D printing have enhanced the performance and reduced the costs of these drones, making them more accessible and efficient.

The ongoing development in 3D printing technologies enables more rapid prototyping and customization of drone components, further enhancing the capabilities and applications of multi-rotor drones in various sectors. The growth trajectory of the multi-rotor segment is supported by continuous improvements in 3D printing techniques that allow for the production of complex geometries and customized drone solutions, catering to the specific needs of different industries.

Application Analysis

In 2023, the military segment of the 3D printed drones market held a dominant position, primarily due to significant investments in enhancing combat and surveillance capabilities. The adoption of 3D printing technology within military applications has been driven by the need for customized drone solutions that can be rapidly prototyped and deployed, thus reducing production times and costs significantly.

The ability to quickly produce drones tailored for specific military operations gives armed forces a substantial advantage, enabling them to stay ahead of technological advancements and changing mission requirements. This rapid prototyping capability is crucial for adapting to evolving threats and for the continuous improvement of reconnaissance and operational strategies.

Moreover, the cost-effectiveness of 3D printing allows for the production of drones at a lower cost, which is particularly beneficial given the constraints of military budgets. This cost efficiency not only facilitates the production of a larger volume of drones but also allows for funds to be allocated to other critical areas of defense.

Overall, the integration of 3D printing into military drone manufacturing represents a significant technological shift, promising enhanced operational efficiency and a better alignment with modern warfare demands. The ongoing investments and innovations in this area underscore the growing importance and reliance on 3D printed drones within the defense sector.

Key Market Segments

By Component

- Airframe

- Wings

- Landing Gears

- Propellers

- Mounts & Holders

- Others

By Technology

- Fused Deposition Modeling (FDM)

- Stereolithography (SLA)

- Selective Laser Sintering (SLS)

- Others

By Type Analysis

- Fixed-wing

- Multi-rotor

- Single-rotor

- Hybrid

By Application Analysis

- Consumer

- Military

- Commercial

- Government & Law Enforcement

Driver

Enhanced Customization and Rapid Prototyping Capabilities of 3D Printing

One of the key drivers of the 3D printed drones market is the enhanced customization and rapid prototyping capabilities afforded by 3D printing technology. This technology allows for quick design changes and the creation of complex geometries that are not possible with traditional manufacturing methods.

The agility to adapt to specific requirements and the reduced time from design to production significantly benefit sectors like defense, where tailored solutions are often crucial for mission success. This adaptability is not only fostering innovation but is also enhancing the functionality of drones, making them more efficient for a wide range of applications including surveillance, delivery, and environmental monitoring.

Restraint

Stringent Industry Certifications and Limited Material Availability

Despite the growth, the 3D printed drones market faces significant restraints, including stringent industry certifications and the limited availability of suitable materials. Regulatory standards, which ensure the safety and reliability of drones, can pose challenges in terms of compliance, especially for new market entrants.

Additionally, the materials used in 3D printing, while evolving, still do not fully match the diversity and performance specifications required for more demanding applications. These factors can hinder the broader adoption of 3D printing technology in drone manufacturing, affecting the rate at which new and innovative drone solutions are introduced to the market.

Opportunity

Development of New 3D Printing Technologies

The ongoing development of new 3D printing technologies presents significant opportunities in the 3D printed drones market. Innovations such as multi-material printing and advanced manufacturing techniques like Continuous Liquid Interface Production (CLIP) are set to broaden the capabilities of 3D printed drones.

These advancements could lead to the production of drones that are not only lighter and stronger but also integrated with advanced electronics for enhanced functionalities. Such technological advancements are expected to open new applications in both commercial and military sectors, driving further growth in the market.

Challenge

Product Quality Compliance

A major challenge in the 3D printed drones market is ensuring product quality compliance with industry standards. As the use of drones expands into critical areas such as commercial airspaces and sensitive environmental monitoring, the demand for high reliability and performance standards increases.

Meeting these standards consistently with 3D printed components can be difficult due to variations in printing processes and material properties. Manufacturers must invest in advanced quality control systems and adhere to rigorous testing protocols to overcome these challenges, ensuring that their drones meet the necessary performance and safety criteria.

Growth Factors

The growth of the 3D printed drones market is significantly driven by the increased customization and flexibility that 3D printing technology offers. This technology allows manufacturers to swiftly adapt and modify drone designs based on evolving customer needs and operational requirements, facilitating innovation and technical enhancements.

The reduction in production costs and time due to the elimination of traditional manufacturing constraints is a notable growth factor. As drones become more integral to sectors like defense, agriculture, and public safety, the ability to produce them quickly and cost-effectively becomes increasingly valuable. Additionally, the push towards lightweight and complex drone structures, achievable through 3D printing, enhances performance and functionality, which further drives market expansion.

Emerging Trends

Emerging trends in the 3D printed drones market reflect the technological advancements and expanding application areas. There is a significant movement towards integrating multi-material 3D printing and continuous production technologies, such as Continuous Liquid Interface Production (CLIP). These innovations enable the production of more sophisticated drones that can include a mix of materials with varying properties, enhancing their utility and performance.

The trend of using drones equipped with advanced sensory and autonomous capabilities is also on the rise, propelled by the ongoing development in 3D printing techniques that support such functionalities. This evolution is aligning with the growing demand for drones in surveillance, delivery services, and environmental monitoring, which are set to redefine how businesses and governments operate.

Business Benefits

The adoption of 3D printing in drone manufacturing offers numerous business benefits, including significant reductions in inventory and logistics costs due to on-demand production capabilities. This shift enables companies to maintain leaner inventories and reduces the lead times for parts and products, enhancing supply chain efficiency.

Customization is another significant advantage, as companies can tailor drones to specific applications, which is especially beneficial in sectors like agriculture and infrastructure, where operational needs can vary greatly. Additionally, the ability to rapidly prototype and iterate designs allows businesses to innovate more effectively, keeping pace with technological advancements and market demands. These benefits collectively contribute to a competitive edge in a rapidly evolving market.

Regional Analysis

In 2023, North America maintained a commanding lead in the 3D printed drones market, capturing a significant 36.3% share with a revenue of approximately USD 1,339 million. This dominant position is largely attributed to the region’s robust adoption of advanced technologies, particularly within the defense and aerospace sectors.

North America’s market leadership is reinforced by the presence of major drone manufacturers and a strong ecosystem that supports innovation and the development of high-performance, complex drone designs enabled by 3D printing technologies.

The region’s commitment to research and development in 3D printing for drones is evident in the substantial investments from both public and private sectors. Innovations in this market are propelled by the need for drones that offer greater functionality and customization, which 3D printing technology facilitates more efficiently than traditional manufacturing methods. This has led to North America not just leading in terms of market share but also in technological advancements in the drone industry.

Furthermore, the strategic use of 3D printed drones in applications ranging from commercial aerial surveillance to complex military operations underscores the region’s progressive approach to adopting next-gen technologies. These drones are increasingly used for critical tasks such as infrastructure inspection, agricultural monitoring, and law enforcement, showcasing their growing importance across various sectors.

The regulatory environment in North America also plays a crucial role in shaping the market. The United States and Canada have developed specific regulations that facilitate drone testing and commercial use, which helps maintain North America’s leading position in the global market. This supportive regulatory framework, combined with ongoing technological advancements, positions North America to continue its dominance in the 3D printed drones market

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

The 3D-printed drones market is experiencing significant growth, driven by advancements in additive manufacturing and the increasing demand for customized, lightweight unmanned aerial vehicles (UAVs). Several key players are leading this innovative sector:

Boeing has been at the forefront of integrating 3D printing into its drone manufacturing processes. In 2023, the company unveiled a new line of unmanned aerial vehicles (UAVs) that incorporate 3D-printed components, enhancing performance and reducing production costs. This strategic move has solidified Boeing’s position as a leader in the aerospace industry.

AeroVironment has also made notable strides in the 3D-printed drones sector. The company has focused on developing lightweight, high-performance drones utilizing additive manufacturing techniques. In 2023, AeroVironment introduced a new drone model featuring a fully 3D-printed airframe, offering improved durability and reduced weight. This innovation has strengthened AeroVironment’s market presence and expanded its product portfolio.

Parrot Drone SAS, a French company, has been a pioneer in the commercial drone market. In 2023, Parrot launched a new series of drones with 3D-printed components, catering to various industries such as agriculture, surveillance, and mapping. This diversification has enabled Parrot to capture a broader market share and meet the evolving demands of its customers.

Top Key Players Covered

- The Boeing Company

- AeroVironment, Inc.

- BAE Systems plc

- Draganfly Innovations, Inc.

- Thales Group

- Parrot Drones SAS

- General Atomics

- Skydio, Inc.

- Airbus SE

- Flyability SA

- Dronamics Global Limited

- Kratos Defense & Security Solutions, Inc.

- Lockheed Martin Corporation

- Firestorm Labs, Inc.

- Northrop Grumman Systems Corporation

Recent Developments

- In April 2024, the U.S. Navy awarded Insitu, Inc., a Boeing subsidiary, an $84 million contract to deliver UAVs and sensor payloads. This initiative aims to bolster surveillance for the Navy, Marine Corps, and allied forces, showcasing a growing reliance on cutting-edge unmanned systems to enhance operational efficiency.

- In March 2024, Firestorm Labs, Inc. secured $12.5 million in seed funding, led by Lockheed Martin Ventures and other defense-focused investors. The funding highlights a significant push toward rapid technology delivery and ensuring interoperability across military operations, addressing the evolving demands of modern warfare.

- In February 2024, General Atomics demonstrated its Advanced Air-Launched Effects (A2LE) platform, a breakthrough made using additive manufacturing. Launched from the internal weapons bay of an MQ-20 Avenger, this achievement underscores the potential for agile and cost-effective solutions in next-generation combat systems.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 581 Mn |

| Forecast Revenue (2033) | USD 3,721 Mn |

| CAGR (2024-2033) | 20.4% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Fixed-wing, Multi-rotor, Single-rotor, Hybrid), By Component (Airframe, Wings, Landing Gears, Propellers, Mounts & Holders, Others), By Technology (Fused Deposition Modeling (FDM), Stereolithography (SLA), Selective Laser Sintering (SLS), Others), By Application (Consumer, Military, Commercial, Government & Law Enforcement) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | The Boeing Company, AeroVironment Inc., BAE Systems plc, Draganfly Innovations Inc., Thales Group, Parrot Drones SAS, General Atomics, Skydio Inc., Airbus SE, Flyability SA, Dronamics Global Limited, Kratos Defense & Security Solutions Inc., Lockheed Martin Corporation, Firestorm Labs Inc., Northrop Grumman Systems Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |