Quick Navigation

Report Overview

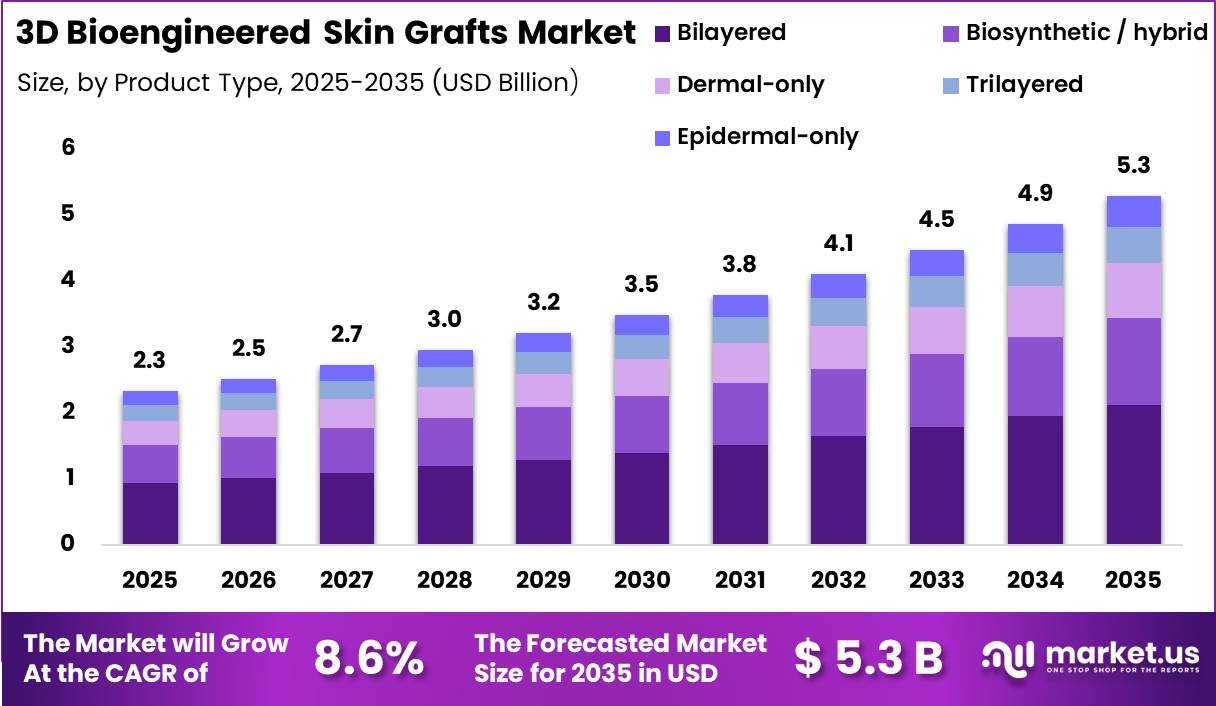

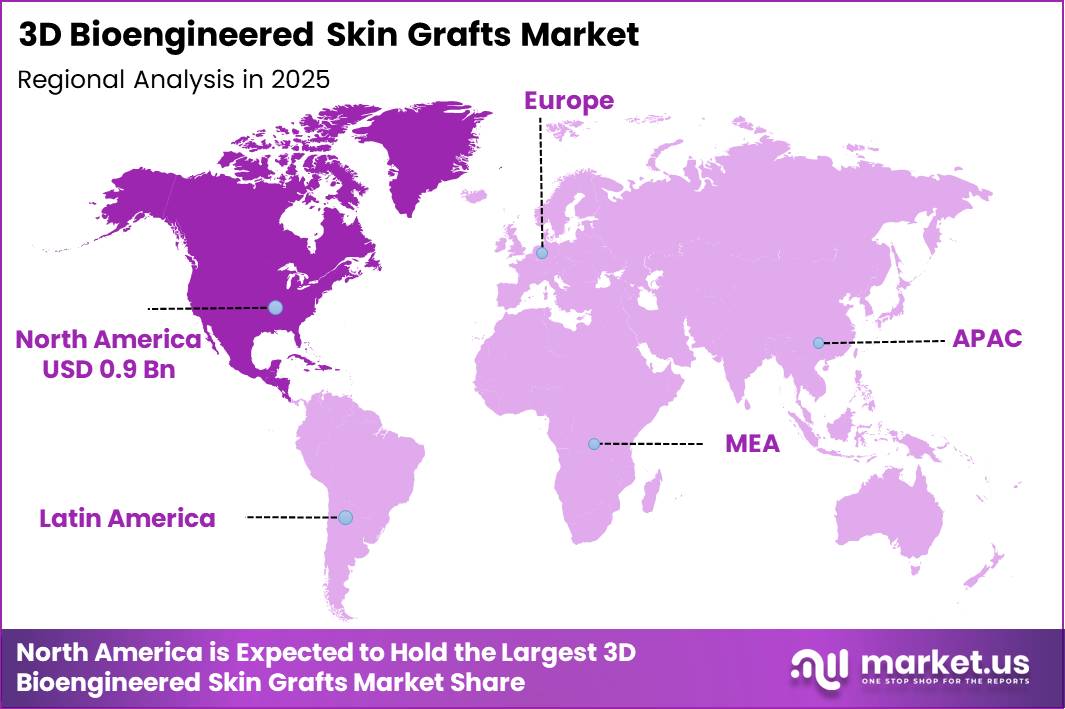

Global 3D Bioengineered Skin Grafts Market size is expected to be worth around US$ 5.3 Billion by 2035 from US$ 2.3 Billion in 2025, growing at a CAGR of 8.6% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 40.4% share with a revenue of US$ 0.94 Billion.

The 3D Bioengineered Skin Grafts market is defined as a class of tissue-engineered biological constructs designed to replicate native skin architecture combining living cells, biomaterial scaffolds, and extracellular matrix components for the treatment of chronic wounds, acute burn injuries, and reconstructive surgical defects.

- According to the NIH National Library of Medicine in 2025 stated that non-healing wounds affect approximately 1% of the global population, with prevalence expected to rise alongside an ageing global demographic.

Bioengineered allogeneic cellularized construct (BACC) received FDA approval for treatment of burn wounds, with Phase III clinical trial data confirming efficacy for deep partial thickness acute burns confirming regulatory validation of advanced bioengineered skin architectures in the U.S. market

Burn injuries impose a significant and persistent clinical burden an estimated 180,000 deaths are caused by burns every year, with the vast majority occurring in low and middle-income countries. The primary restraint is the high manufacturing cost of cell-based constructs and the complexity of maintaining cellular viability across cold-chain distribution networks, limiting accessibility in cost-constrained healthcare systems.

Future outlook is anchored in AI-driven wound assessment platforms, automated bioprinting systems, and personalised graft design capabilities that are progressively reducing production timelines and improving clinical matching precision.

Key Takeaways

- Market Size: Global 3D Bioengineered Skin Grafts Market size is expected to be worth around US$ 5.3 Billion by 2035 from US$ 2.3 Billion in 2025.

- Market Share: The market is growing at a CAGR of 8.6% during the forecast period from 2026 to 2035.

- Product Type Analysis: Bilayered grafts are identified as the dominant product type, accounting for 40.1% of the market in 2025, driven by their dual-layer replication of both dermal and epidermal skin architecture.

- Application Analysis: Chronic wounds are confirmed as the dominant application at 55.2%, anchored by the rising global prevalence of diabetic foot ulcers and venous leg ulcers.

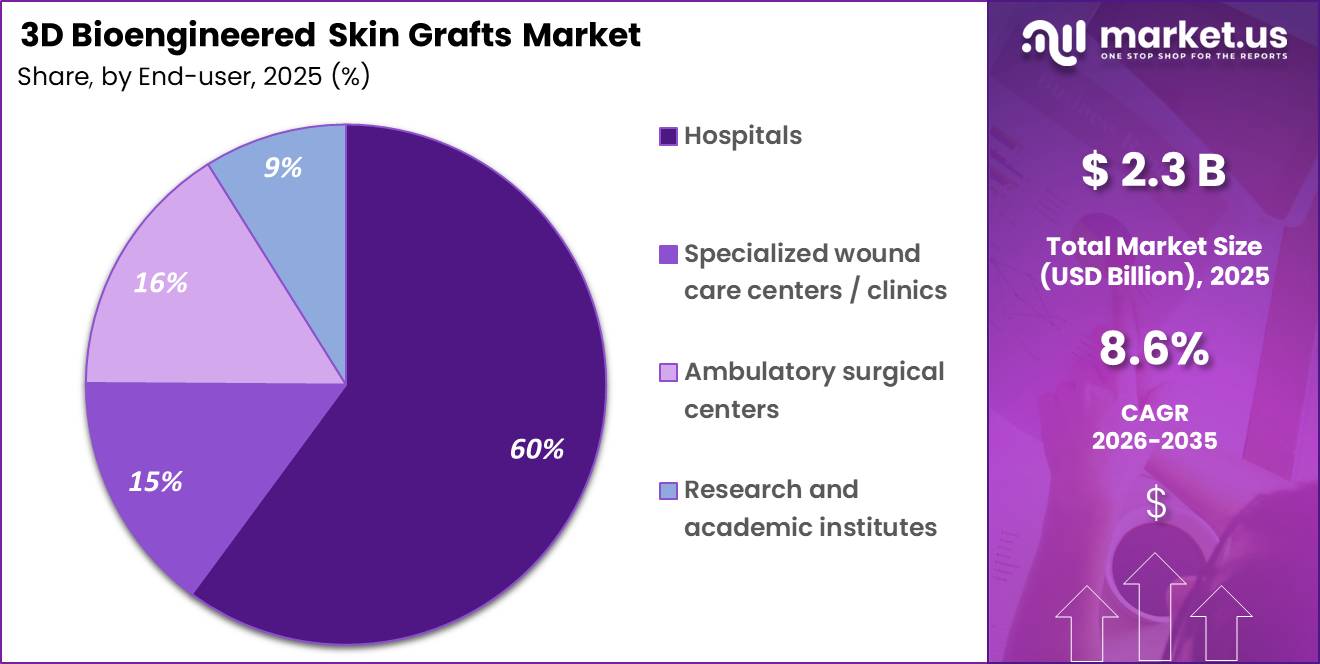

- End User Analysis: Hospitals lead end-user adoption at 60.1%, reflecting the procedural complexity and regulatory requirements associated with advanced skin graft implantation.

- Regional Analysis: North America holds the largest regional share at 40.4%, supported by established FDA regulatory pathways, high healthcare expenditure, and a concentration of leading market participants.

Product Type

Bilayered Product represents dominant Segment in the Market.

Bilayered products represent the dominant segment in the 3D bioengineered skin grafts market, accounting for 40.1% share in 2025. Their leadership is driven by superior structural replication of both dermal and epidermal layers, enabling improved wound closure, reduced contraction, and enhanced cosmetic outcomes. These grafts are widely used in chronic wound care, burns, and reconstructive procedures due to strong clinical acceptance, reimbursement support, and established commercial availability across advanced wound care systems.

Biosynthetic and hybrid grafts are the fastest-growing product type, supported by increasing demand for off-the-shelf and scalable wound solutions. These constructs combine synthetic scaffolds with biological materials such as collagen and growth factors, enabling reduced dependency on cold-chain logistics. Their rapid adoption is driven by acute wound care requirements, including trauma and burns, where immediate availability is critical. Technological advancements and manufacturing scalability are further accelerating their market penetration.

Application Analysis

3D Bioengineered Skin Grafts Are the Most Widely Used in Chronic Wounds.

Chronic wound applications held a leading 55.2% share of the 3D bioengineered skin grafts market in 2025. This dominance is primarily driven by the rising prevalence of diabetic foot ulcers, venous leg ulcers, and pressure injuries linked to diabetes and an ageing global population. Clinical guidelines, reimbursement support, and increasing adoption of advanced wound care biologics further reinforce demand across long-term care and hospital-based wound management settings

Acute wound applications are the fastest-growing segment, driven by increasing demand in burn care, trauma injuries, and surgical wound management. Expanding burn treatment infrastructure and improved emergency care systems are supporting adoption of advanced graft technologies. The growth is further influenced by the introduction of cell-based therapies and rapid-deployment skin substitutes designed for immediate clinical use. Rising investment in trauma systems and emergency healthcare delivery continues to strengthen this segment.

End User Analysis

3D Bioengineered Skin Grafts Are Mostly Utilized in the Hospitals Sector.

Hospitals dominated the 3D bioengineered skin grafts market in 2025 with a 60.1% share, driven by the complexity of procedures requiring sterile surgical environments and specialized clinical expertise. Burn units, plastic surgery departments, and diabetic limb salvage programs remain the primary demand centers within hospitals. Strong infrastructure for post-operative monitoring and reimbursement support further strengthens hospital-based adoption of advanced skin graft technologies.

Ambulatory surgical centers are the fastest-growing end-user segment, driven by a shift toward cost-efficient outpatient care. Reimbursement reforms and evolving payer policies are encouraging procedures to move away from traditional physician office settings. ASCs offer reduced treatment costs, faster patient turnover, and efficient procedural workflows, making them increasingly suitable for wound care applications. This structural shift is expected to continue as healthcare systems prioritize outpatient-based treatment delivery.

Key Market Segments

By Product Type

- Bilayered

- Biosynthetic / hybrid

- Dermal‑only

- Trilayered

- Epidermal‑only

By Application

- Chronic wounds

- Acute wounds (burns, trauma)

- Reconstructive & plastic surgery

By End-user

- Hospitals

- Specialized wound care centers / clinics

- Ambulatory surgical centers

- Research and academic institutes

Driver

Diabetic Foot Ulcer Burden Driving Advanced Graft Demand

Diabetes is a major structural driver of chronic wound growth, expanding the pool of patients requiring advanced wound care beyond what standard healing pathways can manage. The World Health Organization estimates that around 830 million people were living with diabetes in 2022, while the International Diabetes Federation projects this could rise to roughly 853 million by 2050.

Diabetic foot ulcers alone affect an estimated ~18.6 million people annually, creating a large and persistent treatment cohort.Clinically, diabetic foot ulcers typically enter advanced care pathways after failure of standard wound management, meaning worsening diabetes prevalence, infection risk, and limb-salvage interventions directly expand demand for higher-value solutions such as bioengineered skin substitutes and grafts.

For advanced graft developers, this shifts positioning away from episodic use cases (e.g., burns) toward recurring chronic wound indications. Diabetic foot ulcers in particular support repeat applications, measurable healing outcomes, and outpatient use, strengthening reimbursement cases and enabling more durable revenue streams for 3D bioengineered graft platforms.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Diabetic foot ulcer load expanding advanced graft demand | +2.4% | North America core, EU, APAC urban corridors, GCC | Medium term (2-4 years) |

| Burn injury burden sustaining acute reconstruction need | +1.8% | South Asia, Southeast Asia, Africa, Middle East, North America trauma centers | Medium term (2-4 years) |

| CMS/FDA evidence filter favoring clinically differentiated grafts | +1.6% | U.S. core, spill-over to EU reimbursement strategy | Short term (≤ 2 years) |

| 3D bioprinting customization improving fit, healing economics | +2.1% | U.S., EU, Japan, South Korea, China innovation hubs | Medium term (2-4 years) |

| Regenerative medicine pathways accelerating translational programs | +1.3% | U.S. core, selective EU and APAC biotech clusters | Long term (≥ 4 years) |

| Shift toward outpatient wound care and episode-based efficiency | +1.4% | U.S., Canada, Western Europe, advanced APAC systems | Short term (≤ 2 years) |

Challenge

Chronic Wound Care Talent Gap as a Structural Constraint

The chronic wound care talent gap is a key bottleneck limiting adoption of advanced 3D bioengineered skin grafts. Effective use of these therapies requires multidisciplinary expertise wound care nurses, endocrinologists, vascular and plastic surgeons, and rehabilitation specialists—capable of managing complex comorbidities such as diabetes and peripheral arterial disease.

Although global diabetes prevalence exceeds 500 million people, with a significant share developing diabetic foot ulcers, specialist wound care capacity remains concentrated in tertiary centers in high-income countries. In many low- and middle-income regions, dedicated wound clinics are scarce, and clinicians often manage 50–100 complex cases each, leading to delayed referrals, inconsistent graft use, and higher complication and failure rates due to inadequate follow-up, infection control, and off-loading.

Even in OECD systems, workforce shortages and uneven home-care coverage limit effective deployment of advanced therapies. This mismatch between rising clinical need and constrained specialist capacity is estimated to reduce achievable market CAGR by around 0.7 % points.Mitigation is gradually emerging through tele-wound platforms, standardized care pathways, and regional centers of excellence, but broad competency expansion is likely to take 4–8 years, keeping this as a persistent medium- to long-term constraint.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Complex GMP scale-up | -1.3% | North America, EU, APAC hubs | Medium term (2-4 years) |

| High biofabrication cost stack | -1.1% | High-income health systems | Long term (≥ 4 years) |

| Fragmented regulatory pathways | -0.9% | U.S., EU, Japan | Medium term (2-4 years) |

| Slow clinical evidence accumulation | -0.8% | Global tertiary centers | Long term (≥ 4 years) |

| Chronic wound care talent gap | -0.7% | LMICs, aging OECD | Long term (≥ 4 years) |

| Biologic input and logistics risk | -0.6% | Global supply corridors | Short term (≤ 2 years) |

Restraints

Fragmented FDA/EMA Pathways and Limited Evidence as a Commercial Constraint

Bioengineered and 3D-printed skin substitutes face fragmented regulatory classification across regions, including U.S. Food and Drug Administration and European Medicines Agency pathways. Depending on design and manufacturing, these products may be regulated as HCT/Ps, Class III medical devices, biologics, or combination products, each requiring different levels of clinical evidence and post-market surveillance.

In practice, this leads to a limited base of fully approved products, with many newer constructs operating under investigational or restricted-use frameworks. Clinical evidence is often constrained to small, single-arm studies (typically <100 patients) with short follow-up windows of 12–24 weeks, which limits the strength of reimbursement and adoption claims.

As regulatory expectations shift toward randomized controlled trials, standardized wound-healing endpoints, and long-term safety monitoring, pivotal studies can cost USD 20–40 million and take 24–36 months to enroll due to strict inclusion criteria for diabetic foot and venous leg ulcer populations.

These constraints delay commercialization by 2–4 years, increase development costs, and raise capital intensity, putting pressure on early-stage regenerative medicine firms. The result is slower scaling of manufacturing capacity and reduced near-term profitability, as companies absorb higher regulatory and clinical costs before achieving broad reimbursement acceptance.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented FDA / EMA pathways & limited clinical evidence | -2.0% | US core, EU | Medium term (2–4 years) |

| High bioprinting platform & bioink cost inflation | -1.5% | US, EU, APAC tier-1 | Long term (≥ 4 years) |

| GMP manufacturing complexity & low throughput | -1.3% | US, EU, Japan, South Korea | Medium term (2–4 years) |

| CMS / payer reimbursement uncertainty for skin substitutes | -1.2% | US core | Short–Medium (≤ 4 years) |

| Scarcity of skilled tissue engineering workforce | -0.8% | US, EU, select APAC | Long term (≥ 4 years) |

| Ethical, liability, and procurement constraints for human-derived materials | -0.7% | US, EU, Middle East | Medium–Long (≥ 3 years) |

Opportunity

Chronic Wound Bundled Value Based Programs

Bundled, outcomes based payment models for chronic wounds represent a key opportunity to expand adoption of 3D bioengineered skin substitutes 3D BSG beyond today’s fragmented fee for service wound care system. Chronic wounds, particularly diabetic foot, venous, and pressure ulcers, affect roughly 7 to 10 million patients across major OECD markets, but current spending is spread across dressings, debridement, and surgical care with limited integrated contracting.

If 3D BSG becomes the anchor of bundled care pathways, payers could link reimbursement to outcomes such as faster healing (20 to 30 % reduction in time), shorter hospital stays (2 to 3 days less per case), and lower amputation rates (10 to 15 % reduction). In this model, premium pricing of 25 to 35 % per episode can still be cost saving for payers, potentially unlocking an additional USD 2 to 4 billion in addressable value by 2030.

The growth impact comes from shifting even 10 to 15% of chronic wound episodes into structured, value based bundles centered on 3D BSG, rather than relying on incidence expansion. This transition could add roughly 2.0 % points to CAGR, but remains an emerging opportunity since most health systems have not yet fully integrated skin substitute based bundled reimbursement models.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Chronic wound bundled value-based programs | +2.0% | North America, Western Europe | Medium term (2–4 years) |

| LMIC burn & trauma access platforms | +2.3% | Africa, South-East Asia, Latin America | Long term (≥ 4 years) |

| Immunomodulated allogeneic graft platforms | +1.8% | North America core, EU, APAC developed | Medium term (2–4 years) |

| Pharma co-developed bioprinted skin for trials | +1.5% | Global Tier-1 pharma hubs | Short term (≤ 2 years) |

| Aesthetic and scar-revision premium segment | +1.2% | North America, EU, affluent APAC | Medium term (2–4 years) |

| Digital twin & robotics-enabled graft workflows | +1.0% | Leading tertiary centers globally | Long term (≥ 4 years) |

Geopolitical Impact Analysis

Trade Tariffs and Supply Chain Disruption Are Creating Cost Headwinds Across the Global 3D Bioengineered Skin Grafts Market.

The escalating U.S. and China trade conflict and broader global tariff environment are introducing measurable cost pressure across the bioengineered skin graft supply chain. Key raw material inputs including bovine collagen, synthetic polymer scaffolds, bioreactor components, and sterile packaging materials are sourced across international supply chains that are directly exposed to tariff escalation.

Smith+Nephew confirmed in its November 2025 SEC 6-K filing that tariff headwinds of US$ 60 million are anticipated in 2026 compounding the US$ 15–20 million net tariff impact incurred in 2025. This dual pressure from tariffs and the CMS physician office reimbursement reset is forcing manufacturers to actively restructure cost bases and accelerate operational efficiency programmes. Smaller market participants without the scale to absorb these combined headwinds are facing margin compression that may accelerate sector consolidation through 2026 and beyond.

Regional Analysis

North America Held the Largest Share of the Global 3D Bioengineered Skin Grafts Market

North America is the leading regional market for 3D bioengineered skin grafts in 2025, accounting for approximately 40.4% of global revenue at US$ 0.94 billion. This dominance is supported by a strong regulatory ecosystem led by the FDA, a well-established reimbursement framework for advanced wound care biologics, and high clinical adoption across hospitals and wound care centers. The region also has a large chronic wound patient base, driven primarily by a significant diabetic population, making it the most mature and revenue-intensive market globally.

According to CDC estimates, around 38.4 million Americans are living with diabetes, representing 11.6% of the U.S. population, which sustains strong demand for bioengineered skin grafts in chronic wound management. Major industry players such as Organogenesis Holdings, AVITA Medical, Integra LifeSciences, Vericel Corporation, and MiMedx Group are headquartered in the United States, reinforcing regional leadership through concentrated R&D, manufacturing, and commercialization capabilities.

Europe remains the second-largest market, supported by structured reimbursement systems under EU MDR and strong demand from ageing populations in countries such as Germany, France, and the United Kingdom. Asia Pacific is emerging as the fastest-growing regional market, driven by rapid expansion in diabetes prevalence, improving healthcare infrastructure, and increasing adoption of advanced wound care solutions.

China and India are expected to contribute the largest incremental growth through 2035, supported by rising clinical awareness and broader access to bioengineered skin graft technologies across expanding hospital networks.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The Global 3D Bioengineered Skin Grafts market operates under a moderately consolidated competitive structure at the product and commercial tier, with characteristics of oligopolistic behaviour among the leading U.S.-based manufacturers and a fragmented landscape among smaller regional and emerging market participants.

Organogenesis Holdings, AVITA Medical, Integra LifeSciences, Vericel Corporation, and MiMedx Group collectively dominate the North American market as the world’s largest and most reimbursement-developed market for advanced skin grafts.

At the technology and product innovation layer, competition is considerably more fragmented. Kerecis (Coloplast), AROA Biosurgery, Tissue Regenix Group, LifeNet Health, and Genoskin occupy specialised positions, each differentiated by proprietary biomaterial platforms, specific clinical indication focus, or geographic market concentration.

The overall market rewards regulatory approval depth, reimbursement access, clinical evidence breadth, and commercial infrastructure scale, competitive advantages concentrated among the five to six largest participants globally and that present meaningful structural barriers to new entrant commercialisation.

Major Key Players

- Genoskin

- Smith & Nephew plc

- Genzyme Biosurgery

- Vericel Corporation

- AROA Biosurgery Limited

- Integra LifeSciences Corporation

- COOK Biotech Incorporated

- Mölnlycke Health Care AB

- Avita Medical

- MiMedx Group, Inc.

- Organogenesis Holdings Inc.

- Tissue Regenix Group plc

- Kerecis (Coloplast)

- LifeNet Health, Inc.

- Stryker Corporation

- Others

Key Development

- In May 2026, AVITA Medical announced its Q1 2026 financial results conference call, scheduled for May 14, 2026, confirming continued commercial execution of the RECELL System and its biosynthetic graft portfolio across U.S. burn and trauma centres, with the company maintaining its strategic focus on RECELL as the standard of care for burns of 5% TBSA or greater.

- In March 2026, Organogenesis reported full year 2025 net product revenue of US$ 563.0 million an increase of US$ 81.0 million versus 2024 with Advanced Wound Care revenue of US$ 531.2 million growing 17% year-over-year, and Q4 2025 net income of US$ 43.7 million versus US$ 7.7 million in Q4 2024, confirming a record financial performance driven by Advanced Wound Care market adoption.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 2.3 Billion |

| Forecast Revenue (2035) | US$ 5.3 Billion |

| CAGR (2026-2035) | 8.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Bilayered, Biosynthetic/Hybrid, Dermal-only, Trilayered, and Epidermal-only), By Application (Chronic Wounds, Acute Wounds (Burns, Trauma), and Reconstructive & Plastic Surgery), By End-user (Hospitals, Specialized Wound Care Centers/Clinics, Ambulatory Surgical Centers, and Research and Academic Institutes) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Genoskin, Smith & Nephew plc, Genzyme Biosurgery, Vericel Corporation, AROA Biosurgery Limited, Integra LifeSciences Corporation, COOK Biotech Incorporated, Mölnlycke Health Care AB, Avita Medical, MiMedx Group Inc., Organogenesis Holdings Inc., Tissue Regenix Group plc, Kerecis (Coloplast), LifeNet Health Inc., Stryker Corporation, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |