Quick Navigation

Report Overview

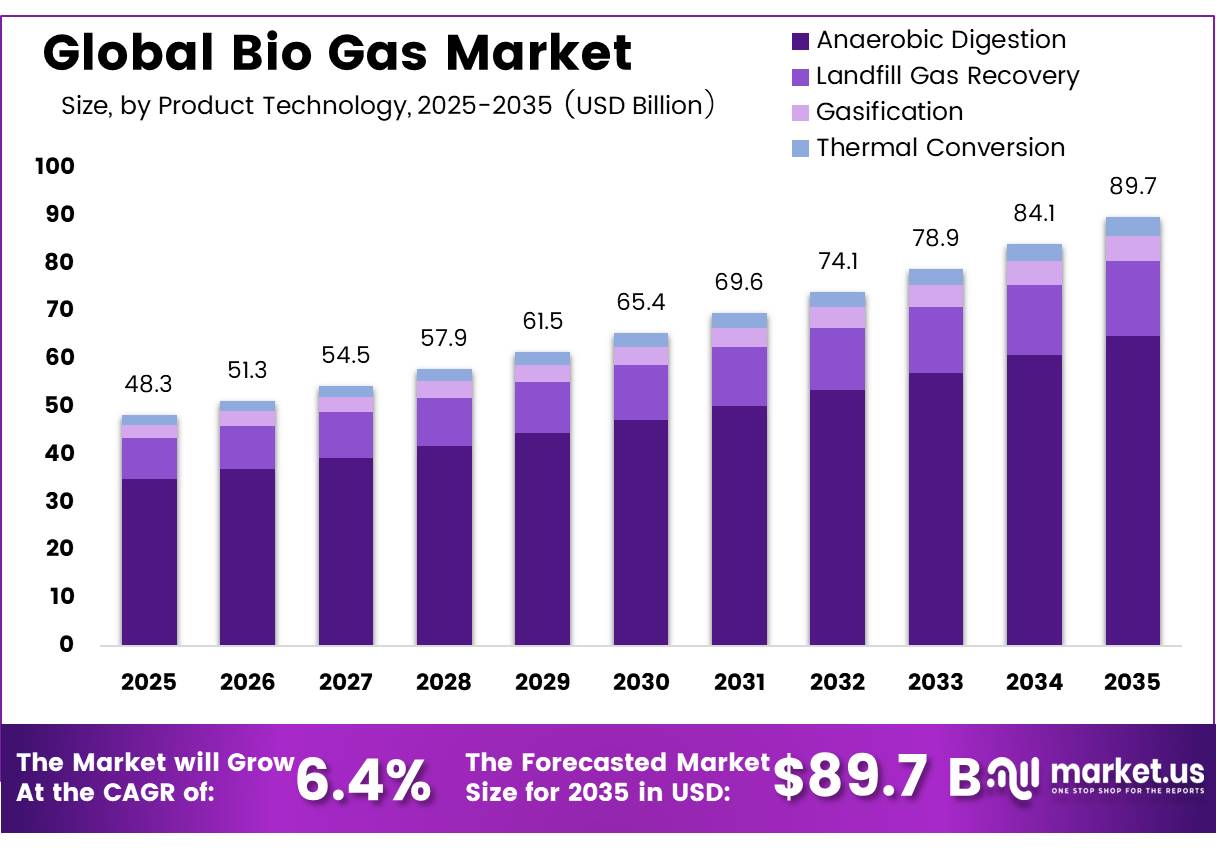

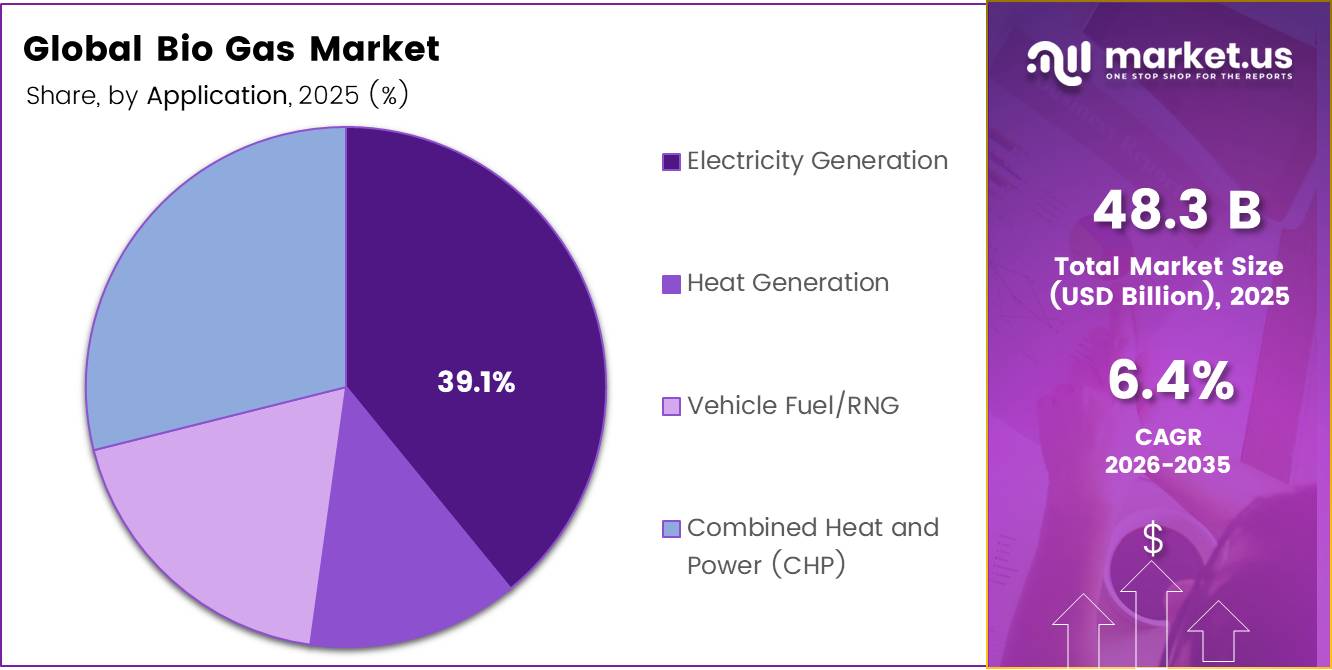

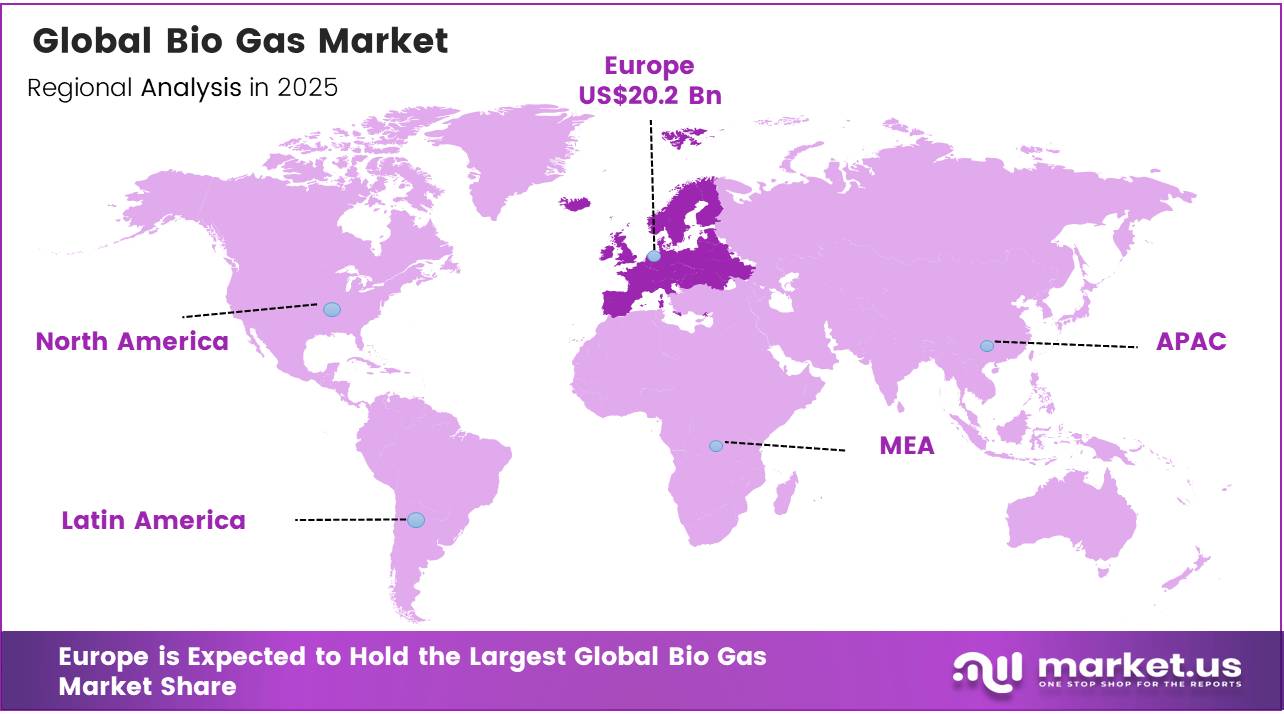

In 2025, the Global Biogas Market was valued at USD 48.3 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 6.4%, reaching about USD 89.7 billion by 2035. Europe held a dominant Market position, capturing more than a 41.7% share, holding USD 20.1 Billion revenue.

The global biogas market is an important part of the renewable energy value chain that uses organic waste for the production of sustainable energy sources used in transportation, industrial activities, and energy production.

- As per the European Biogas Association (June 2025), the annual production capacity of biomethane in Europe stood at 7 billion cubic meters by Q1 2025, marking a 9% growth from 2024, with 1,678 biomethane plants in operation in Europe, representing a net addition of 165 plants.

- As per the European Commission (2026), the EU spent €336.7 billion on energy imports in 2025, making it increasingly urgent for the development of domestic biogas facilities.

Key Takeaways

- The global biogas market was valued at USD 48.3 billion in 2025.

- The global bio gas market is projected to grow at a CAGR of 6.4% and is estimated to reach USD 89.7 billion by 2035.

- On the basis of source, the Agricultural dominated the market, constituting 48.7% of the total market share.

- Based on the production type, the Anaerobic Digestion dominated the biogas market, with a substantial market share of around 72.3%

- Based on the application, electricity generation led the market, comprising 39.1% of the total market.

- In 2025, the Europe was the most dominant region in the biogas market, accounting for 41.7% of the total global consumption.

In India, data from the Ministry of New and Renewable Energy (April 2026) showed that there were 132 CBG plants operating under the SATAT program with an aggregate production capacity of 920 tons per day, with Oil Marketing Companies purchasing 82,000 tons of CBG in the previous fiscal year. The U.S. Department of Energy (2025) announced investment of $23 million in supporting biomass and waste-to-energy technologies including biogas upgrading technologies for renewable diesel and jet fuel production.

Biogas Market Segment

Source Analysis

Agricultural represents dominant Segment in the Market.

Agricultural waste is the largest source of biogas feedstock, contributing 48.7% of the total. India alone has 150 million tonnes of agricultural waste each year, along with 190 million tonnes of animal and poultry waste, constituting the largest source of unexplored biomass potential for biogas production. The SATAT program of the government has already installed 132 CBG plants that produce 920 tonnes per day, mostly using agricultural waste.

Municipal solid waste (MSW) is currently the second-largest source, India generates nearly 62 million tonnes of municipal solid waste every year, creating strong potential for waste-to-energy projects. In October 2025, GAIL signed a concession agreement for a Bengaluru-based MSW-to-CBG plant, which will process 300 tonnes of segregated waste per day and produce 12.6 tonnes of CBG daily. In January 2025, the US DOE will invest $23 million for waste-to-fuel technologies.

Production Technology Analysis

Anaerobic digestion represents dominant Segment in the Market.

Anaerobic digestion dominates the biogas production by 72.3% of the biogas produced. The Ministry of New and Renewable Energy (Government of India) extends centralized financial assistance of ₹1.0 crore per 12,000 m³/day for biogas generation using AD technology from urban, agricultural, and industrial wastes. In 2025, the Sardar Swaran Singh National Institute of Bio-Energy under MNRE pioneered a groundbreaking catalyst technology that enhances methane production by up to 30%, increasing efficiency of AD systems.

The fastest-growing segment is gasification, The European Commission has endorsed a €2.59 million LIFE-W2B project (September 2025–August 2029), involving gasification and anaerobic digestion, to produce 1,000 tons of biomethane from waste annually. Central financial assistance of ₹2,500–15,000 per kW is extended for biomass gasification initiatives in India.

Application Analysis

Electrical generation are the most widely used application.

Electrical generation continues to be the leading biogas application it makes up 39.1% of total biogases produced for household use. This was confirmed by the International Energy Agency (Renewables 2025) and there was a 22% increase in capacity from 2022 to 2023. In Europe, electricity accounts for 15% of biomethane use, while Germany has around 9,600 biogas plants producing base-load renewable electricity.

Vehicle fuel is the fastest growing segment. The American Biogas Council (2025) estimated that in 2025 U.S. RNG production increased by 24% to 225.6 million MMBtu. 23% of total biomethane is consumed for transportation purposes in Europe. The three countries in which almost all the biomethane is used as vehicle fuel include Italy, Sweden, and Estonia. By the end of 2024, 40% of the U.S. biogas was converted into RNG compared to just 17% in 2019.

Key Market Segments

By Source

- Municipal

- Landfill

- Wastewater

- Industrial

- Food Scrap

- Wastewater

- Agricultural

- Poultry

- Swine Farm

- Dairy

- Agricultural Residue

By Production Technology

- Anaerobic Digestion

- Landfill Gas Recovery

- Gasification

- Thermal Conversion

By Application

- Electricity Generation

- Heat Generation

- Vehicle Fuel/RNG

- Combined Heat and Power (CHP)

Drivers

Biomethane upgrading and grid injection build-out

Pipeline-grade biomethane is the strongest biogas market growth driver in 2026 because it expands revenue opportunities beyond local power generation. Global biomethane output is around 10 bcme, representing only 0.2% of natural gas demand, but production is growing by nearly 20% annually.

In Europe, biomethane plants increased from 1,548 to 1,678 between the 2024 and 2025 reporting cycles, with 165 new facilities added and 56 starting operations in early 2025. Installed European capacity reached about 7 bcm per year, while nearly 86% of plants were connected to gas grids. This expansion supports contracted gas sales, transport-fuel supply, cross-border trading, and stronger project bankability.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Biomethane upgrading and grid injection build-out | +2.4% | EU core, North America core, APAC urban gas corridors | Medium term (2-4 years) |

| Renewable fuel mandates and credit-backed offtake | +2.1% | US core, EU core, India core, Latin America spill-over | Short term (≤ 2 years) |

| Methane abatement and landfill-organics compliance | +1.8% | North America, EU, India metros, developed APAC | Short term (≤ 2 years) |

| Agricultural digesters and manure monetization | +1.6% | US dairy belts, Western Europe, India, China | Medium term (2-4 years) |

| Digestate valorization and fertilizer substitution | +1.2% | EU core, India, North America, Latin America agri zones | Medium term (2-4 years) |

| Industrial decarbonization and dispatchable gas demand | +1.4% | EU industry clusters, US manufacturing belts, maritime corridors | Long term (≥ 4 years) |

Restraints

High CAPEX & Unfavorable Project Finance Economics

High upfront capital costs remain a major restraint on the global biogas market in 2026. Industrial plants typically require EUR 3,000–7,000 per kWe, equal to about USD 3–7 million for a 1 MWe facility and USD 12–25 million for plants above 5 MWe. Biomethane projects generally cost USD 2–20 million, while large installations can exceed USD 50 million.

Payback periods of 3–7 years, OPEX equal to 15–20% of annual revenue, and feedstock transport costs reaching 40% of revenue weaken project returns. In India, only around 160 of 1,150 registered SATAT plants were operational by mid-2025, highlighting financing and commercialization difficulties. These pressures are estimated to reduce the market’s forecast CAGR by approximately 1.7 percentage points in the short-to-medium term.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX & Unfavorable Project Finance Economics | -1.7% | Global; acute in India CBG (APAC), Eastern Europe, Sub-Saharan Africa | Short to Medium term (1–3 years) |

| Permitting Delays & Multi-Agency Regulatory Fragmentation | -1.5% | EU-27 core; India (multi-ministry); North America (state-level); Eastern Europe | Short term (≤ 2 years) |

| Feedstock Supply Chain Instability & RED III Sustainability Compliance | -1.2% | EU-27 (RED III mandate); India (agricultural logistics); North America; APAC corridors | Medium term (2–4 years) |

| Fossil Gas Price Competition undermining unsubsidized biomethane commercial viability | -1.0% | North America (Henry Hub ~$3.50/MMBtu, 2026E); EU (TTF ~$11.6/MMBtu); Global LNG corridors | Short to Medium term (1–3 years) |

| Digestate Management & Environmental Compliance Cost Burden | -0.7% | EU-27 (Nitrates Directive, BioAbfV 2025 update); UK; Emerging APAC compliance | Medium to Long term (3–5 years) |

| Skilled Workforce Deficit constraining operational scale-up and plant utilization rates | -0.6% | Global; critical in APAC (India, SEA), Sub-Saharan Africa, Eastern Europe | Long term (≥ 4 years) |

Opportunity

Industrial heat switch

Germany’s newly approved €5 billion industrial decarbonisation scheme in 2026 explicitly includes biomethane alongside electrification, hydrogen, heat recovery, and carbon capture, and covers sectors such as glass, ceramics, paper, pulp, cement, lime, and chemicals, with required emissions cuts of at least 50% within four years and 85% by the end of 15-year contracts.

For biogas producers, the opportunity is to move beyond commodity gas sales into indexed industrial decarbonization contracts bundled with guarantees of origin, carbon accounting, and reliability services; this can reduce customer acquisition cost per unit of contracted volume, lengthen offtake duration to 7-15 years, and create gross margin expansion of an estimated 300-600 basis points versus undifferentiated grid sales, particularly in Germany, northern Italy, France, Benelux, and the UK where industrial gas density and policy-backed decarbonization funding are strongest.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR | Geographic Relevance | Execution Window |

|---|---|---|---|

| Bio-CO2 monetization | +1.9% | EU core, Nordics, UK, N. America | Medium term (2-4 years) |

| Bio-LNG in shipping | +1.6% | EU ports, Nordics, India, Singapore corridors | Medium term (2-4 years) |

| Industrial heat switch | +1.4% | Germany, Italy, France, Benelux, UK | Short term (≤ 2 years) |

| India grid-injection CBG | +1.3% | India core, APAC spill-over | Short term (≤ 2 years) |

| Data-center CHP PPAs | +1.0% | N. America core, Nordics, Ireland, India | Medium term (2-4 years) |

| Brownfield M&A roll-up | +0.9% | Germany, Italy, France, CEE, UK | Medium term (2-4 years) |

Challenges

High capex and complex project finance

High capital intensity and complex financing structures are estimated to reduce the biogas market’s potential CAGR by around 1.7 percentage points. In the United States, fewer than 3,000 biogas projects operate despite more than 17,000 identified opportunities and potential capture capacity of about 781 billion cubic feet annually, leaving over 80% of technical potential undeveloped. In India, support includes INR 565 crore for biomass aggregation equipment, INR 1,450 crore for digestate development, and state-level subsidies of INR 0.75–5 crore per plant. However, projects still require blended financing, while due-diligence periods commonly reach 9–18 months and financial-close rates remain below 50% for early-stage pipelines.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| High capex and complex project finance | -1.7% | India core, North America core, EU investment hubs | Medium term (2-4 years) |

| Grid injection rules and interconnection bottlenecks | -1.5% | EU regulatory hubs, North America gas networks | Long term (≥ 4 years) |

| Feedstock aggregation logistics and seasonality | -1.3% | India core, APAC corridors, Latin America agri zones | Medium term (2-4 years) |

| Technology performance variability and upgrading reliability | -1.2% | EU plants, North America RNG sites, APAC emerging markets | Medium term (2-4 years) |

| Skilled workforce and O&M capability gaps | -1.0% | India, Southeast Asia, Latin America, emerging Africa | Long term (≥ 4 years) |

| Policy execution complexity and multi-scheme coordination | -0.9% | India core, EU policy clusters, APAC national programmes | Medium term (2-4 years) |

Geopolitical Impact Analysis

Geopolitical Realignment and Supply Chain Fragmentation Reshaping Bio Gas Manufacturing.

The Russia-Ukraine war has changed the biogas market. It is no longer about the environment. The Russia-Ukraine war has made biogas a necessary part of energy security. Russia invading Ukraine caused a problem with fuels. This made biomethane development very important. It was needed to replace gas that was imported.

Since 2020 more than 50 new biogas policies have been made around the world. The main reason for these policies is energy security because of the war. In Europe there is a plan called REPowerEU. This plan was made in May 2022. It wants to produce 35 billion meters of sustainable biomethane every year by 2030. This will help end the import of energy from Russia.

They are also looking at a way to increase the trade of -fossil gas. This includes gas from Ukraine. By 2025 Europe had the ability to produce 7 billion cubic meters of biomethane per year. Investors have put 28 billion euros into this sector. However this is still not enough to meet the target for 2030. Biomethane production in the European Union grew by 14% in 2024. Germany is the market for biogas in the world. It produced 329 petajoules of biogas.

The production of biomethane in the European Union is very important. It means that the European Union does not need to import 15 thousand barrels of oil and 2 billion cubic meters of gas every year. The Russia-Ukraine war and biogas are closely related. The Russia-Ukraine war has made biogas very important, for energy security. Biogas production is increasing because of the Russia-Ukraine war.

Regional Analysis

Europe Held the Largest Share of the Global Biogas Market.

Europe dominates the global biogas market, which has taken a commanding market share of 41.7% in 2025 due to well-established policies, commitments to renewable energy generation, and biogas infrastructure in place. In 2024, according to the International Energy Agency, biogas production in the EU increased by 3%, but biomethane production surged by 14% annually, while Germany alone contributed to 53% of total EU biogas production, further establishing Europe’s leadership in the market. Furthermore, in 2022, European Commission launched its REPowerEU initiative aimed to increase the country’s biomethane production up to 35 bcm annually by 2030, thus sustaining demand in the region.

Asia-Pacific is the fastest-growing region in terms of biogas consumption. The IEA reported that India was the fastest-growing bioenergy market in the period from 2023 to 2030, representing one-third of total global growth in bioenergy demand, driven by a requirement to add 5% of compressed biogas to transportation fuel, along with piped natural gas usage from FY 2025-2026 onwards. There were already 170 operational plants producing compressed biogas in India in 2022, while another 300 plants were being constructed in the region.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The primary competitive advantages in biogas plant operations and technology include technological differentiation, scalability efficiency, and integration of the entire feedstock chain. One of the top priorities for these entities is innovation and the development of such technologies as advanced anaerobic digestion, membrane biogas upgrading, and cryogenic separation technologies that increase the yields of pure methane and make biogas plants more efficient in producing renewable natural gas. Another strategic focus lies in the expansion of large centralized biogas plants because they produce more gas per ton of feedstock and provide better opportunities for grid injection or bio-LNG production in transport.

The vertical integration with agricultural cooperatives, municipal waste management agencies, and food processors allows securing the feedstock base and ensuring the efficiency of cost management when organic waste is volatile. The strategy of capacity expansion is highly relevant in Europe and North America because it allows aligning with concentrated demands due to the presence of mandates for renewable fuels and corporate carbon neutrality goals. Moreover, methane leak detection systems, process automation by means of IoT, ISCC certification, and the signing of long-term contracts with utility companies and transport fleets can help in increasing customer lock-in.

Major Players In The Industry

- Engie SA

- DMT International

- IES Biogas

- EnviTec Biogas AG

- Weltec Biopower GmbH

- AAT Abwasser- und Abfalltechnik GmbH

- BEKON GmbH

- Nijhuis Saur Industries

- Xebec Adsorption Inc.

- Bright Renewables BV

- Scandinavian Biogas Fuels International AB

- PlanET Biogas Group

- BTS Biogas SRL

- BioConstruct GmbH

- Other Key Players

Key Development

- In March 2025, EnviTec Biogas AG started operations at its largest biogas plant built in the US, which was a major milestone for the company’s growth strategy in North America and solidified its status as a world leader in biogas plant operations.

- March 2025 ENGIE SA commissioned its largest biomethane production facility in France as part of the French government’s “Plan Biogaz” program to double biomethane capacity in France by 2030. This has strengthened ENGIE SA’s position as the world leader in integrated biomethane production in Europe.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$48.3 Bn |

| Forecast Revenue (2035) | US$89.7 Bn |

| CAGR (2026-2035) | 6.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Source (Municipal (Landfill, Wastewater), Industrial (Food Scrap, Wastewater), Agricultural (Poultry, Swine Farm, Dairy, Agricultural Residue), By Production Technology (Anaerobic Digestion, Landfill Gas Recovery, Gasification, Thermal Conversion), By Application (Electricity Generation, Heat Generation, Vehicle Fuel/RNG, Combined Heat and Power (CHP)) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Engie SA, DMT International, IES Biogas, EnviTec Biogas AG, Weltec Biopower GmbH, AAT Abwasser- und Abfalltechnik GmbH, BEKON GmbH, Nijhuis Saur Industries, Xebec Adsorption Inc., Bright Renewables BV, Scandinavian Biogas Fuels International AB, PlanET Biogas Group, BTS Biogas SRL, BioConstruct GmbH, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |