Quick Navigation

Report Overview

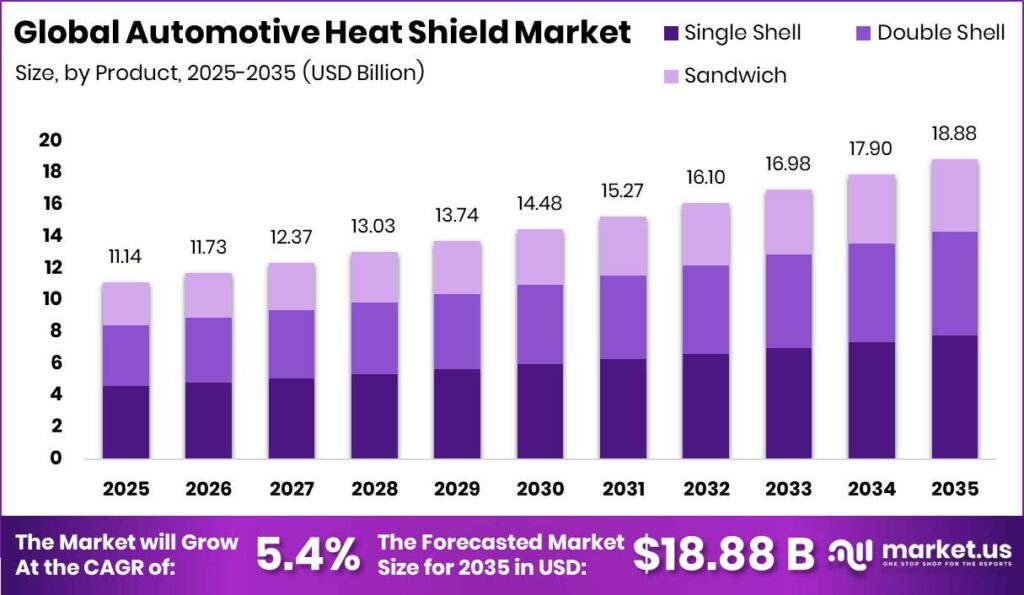

Global Automotive Heat Shield Market size is expected to be worth around USD 18.88 Billion by 2035 from USD 11.14 Billion in 2025, growing at a CAGR of 5.42% during the forecast period 2026 to 2035. This steady climb reflects rising shield content per vehicle as engines run hotter. Suppliers gain a decade-long window to reprice product lines and secure long OEM contracts.

Automotive heat shields protect vehicle parts and occupants from engine and exhaust heat. Manufacturers form them from metallic and non-metallic materials into single, double, and sandwich shell designs. The market spans product, material, application, vehicle type, and sales channel segments. This structure lets suppliers serve factory OEM lines and replacement aftermarket buyers through separate, targeted strategies across regions.

Key Takeaways

- Global Automotive Heat Shield Market will reach USD 18.88 Billion by 2035, up from USD 11.14 Billion in 2025.

- The market grows at a CAGR of 5.42% across the 2026 to 2035 forecast period.

- Single Shell leads the By Product segment with a 41.20% share.

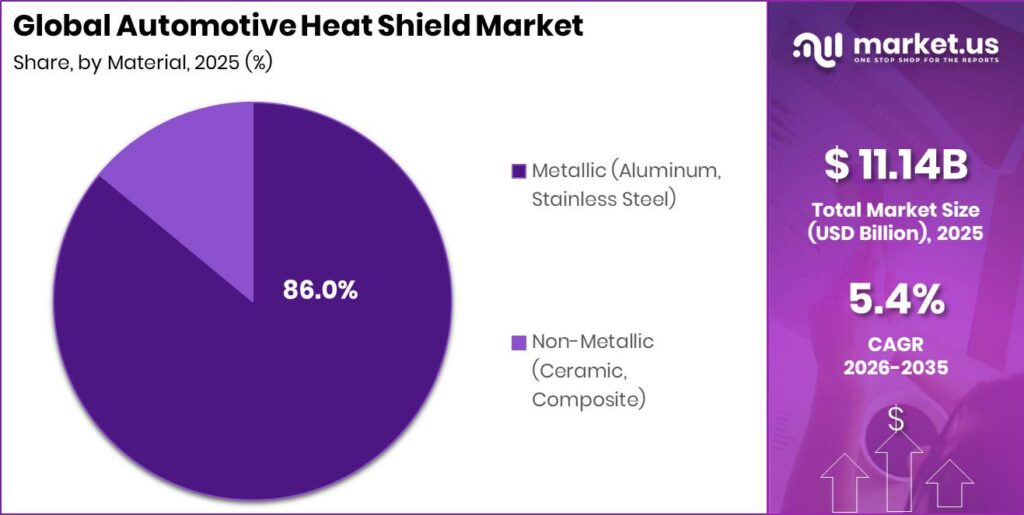

- Metallic materials dominate By Material with an 86.00% share.

- Engine Compartment leads By Application with a 39.10% share.

- Passenger Cars lead By Vehicle Type with a 31.20% share.

- OEM channels account for 78.10% of the By Sales Channel segment.

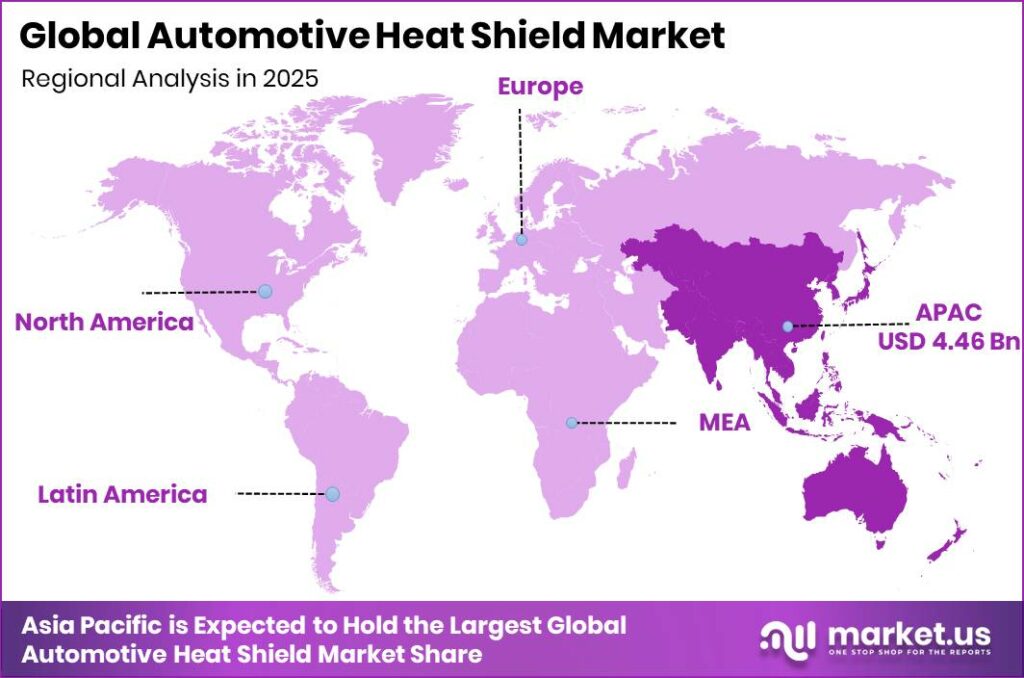

- Asia Pacific dominates with a 40.10% regional share, valued at USD 4.46 Billion.

Emissions rules now shape heat shield demand as strongly as vehicle volume. Data from the European Environment Agency shows average CO₂ emissions from new passenger cars fell to 96.7 g/km in 2025 from 106.7 g/km in 2024. Tighter limits push closer-coupled aftertreatment systems that run hotter. This means suppliers must design higher-temperature shields to stay compliant and defend OEM program share.

Safety performance also lifts thermal shielding requirements across new vehicles. The European New Car Assessment Programme found that 98% of vehicles tested in 2025 achieved four-star or five-star safety ratings. High safety expectations force automakers to protect cabins and fuel systems from heat exposure. This creates steady demand for certified shielding on nearly every new passenger platform reaching the market.

Product Analysis

Single Shell dominates with 41.20% due to low cost and simple production.

In 2025, Single Shell held a dominant market position in the By Product segment of Automotive Heat Shield Market, with a 41.20% share. This design uses one metal layer, keeping tooling and material costs low. Its simplicity suits high-volume, cost-sensitive vehicle programs. Suppliers scaling single-shell output can defend volume contracts while funding investment in higher-value double-shell and sandwich formats.

Double Shell shields use two layers with an air gap that improves thermal insulation. This construction suits hotter engine and exhaust zones needing stronger protection. Rising exhaust temperatures under new emissions rules favor this design. This means suppliers can upsell buyers from single-shell to double-shell products, lifting content value per vehicle over the forecast period.

Sandwich shields bond insulating material between metal layers for maximum heat and noise control. This format serves premium and high-performance applications with demanding thermal loads. Automakers value the combined thermal and acoustic benefit directly. As a result, suppliers can position sandwich shields as a premium tier that commands higher prices on advanced powertrain platforms.

Material Analysis

Metallic dominates with 86.00% due to proven durability and low cost.

In 2025, Metallic held a dominant market position in the By Material segment of Automotive Heat Shield Market, with an 86.00% share. Aluminum and stainless steel resist high heat while staying easy to stamp and form. Their proven performance anchors most exhaust and engine shielding. Suppliers should treat metallic shields as a stable cash base that funds development of advanced non-metallic formats.

Non-Metallic materials include ceramic and composite options built for extreme temperatures and lower weight. These suit demanding zones where metal alone struggles or adds too much mass. Electric vehicle battery shielding increasingly favors these advanced materials. This means suppliers investing in ceramic and composite capability can capture premium, high-margin demand as thermal loads rise across new platforms.

Application Analysis

Engine Compartment dominates with 39.10% due to concentrated heat and dense components.

In 2025, Engine Compartment held a dominant market position in the By Application segment of Automotive Heat Shield Market, with a 39.10% share. This zone packs hot components close to fuel lines and wiring. Dense layouts demand multiple shields per vehicle. Suppliers with engine-bay expertise can secure high-content programs and defend pricing as under-hood temperatures climb across new engine designs.

Exhaust System shields protect surrounding parts from the hottest gases in the vehicle. Closer-coupled aftertreatment systems raise temperatures in this zone sharply. New emissions rules add filters and catalysts near the engine. This creates rising shield content per vehicle, giving suppliers a direct path to higher exhaust-related revenue over the forecast period.

Turbocharger shields contain intense localized heat from forced-induction units. Growing turbocharged engine adoption expands demand for this application. These units require precise, high-temperature shielding to protect nearby components. As a result, suppliers with turbo-specific design capability can attach premium pricing to a widely fitted and growing engine technology.

Under Bonnet shields guard cabin and electrical parts from radiated engine heat, while Under Chassis shields protect the floor and underbody from exhaust routing heat, together holding the remaining share collectively. These zones expand as SUVs and pickups grow in size. This means suppliers gain incremental shielding area per vehicle as larger body styles spread across major markets.

Vehicle Type Analysis

Passenger Cars dominate with 31.20% due to high global production volumes.

In 2025, Passenger Cars held a dominant market position in the By Vehicle Type segment of Automotive Heat Shield Market, with a 31.20% share. Passenger cars drive the bulk of global vehicle output and shield fitment. Their scale anchors supplier revenue and factory utilization. Manufacturers that secure passenger-car OEM contracts gain the volume needed to fund advanced material development across their portfolios.

Light Commercial Vehicles serve delivery and trade fleets that run long hours under heavy thermal loads. This segment values durable, reliable shielding over premium features. Rising e-commerce logistics sustains steady LCV output. This means suppliers can pursue stable, volume-based shield contracts with fleet operators seeking dependable original and replacement supply.

Heavy Commercial Vehicles use large exhaust and aftertreatment systems that demand extensive shielding. These vehicles integrate SCR and DPF units that run at high temperatures. Their long service life sustains aftermarket replacement demand. As a result, suppliers can build durable revenue from both original fitment and a steady stream of HCV shield replacements.

Electric Vehicles need battery thermal barriers rather than exhaust shields, shifting the material mix. Global electric car sales exceeded 17 Million in 2024, an increase of more than 25% over 2023, according to the International Energy Agency. This rapid growth erodes exhaust shield demand while creating new battery shielding needs. This means suppliers must pivot toward EV thermal barrier products to protect long-term revenue.

Sales Channel Analysis

OEM dominates with 78.10% due to factory fitment on new vehicles.

In 2025, OEM held a dominant market position in the By Sales Channel segment of Automotive Heat Shield Market, with a 78.10% share. OEM channels supply shields directly to vehicle assembly lines under long-term contracts. This locks suppliers into stable, high-volume powertrain programs. Manufacturers winning OEM approval gain predictable revenue and early access to next-generation thermal specifications.

Aftermarket covers replacement shields sold after a vehicle leaves the factory, driven by heat damage and corrosion. This channel offers higher margins but faces counterfeit competition in some regions. An aging global vehicle parc sustains steady replacement demand. This means suppliers offering certified, durable replacement shields can defend margin against low-quality substitutes across mature markets.

Key Market Segments

By Product

- Single Shell

- Double Shell

- Sandwich

By Material

- Metallic (Aluminum, Stainless Steel)

- Non-Metallic (Ceramic, Composite)

By Application

- Engine Compartment

- Exhaust System

- Turbocharger

- Under Bonnet

- Under Chassis

By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles (LCV)

- Heavy Commercial Vehicles (HCV)

- Electric Vehicles (EV)

By Sales Channel

- OEM

- Aftermarket

Regional Analysis

Asia Pacific Dominates the Automotive Heat Shield Market with a Market Share of 40.10%, Valued at USD 4.46 Billion

Asia Pacific led the Automotive Heat Shield Market in 2025 with a 40.10% share worth USD 4.46 Billion. China, India, and Southeast Asia drive this lead through high vehicle production. Autoneum acquired Chinese supplier Chengdu FAW-Sihuan Automobile Interior Parts to strengthen its China production capabilities in May 2025. This means suppliers building capacity in Asia Pacific gain proximity to the world’s largest vehicle output base.

Asia Pacific also ranks as the fastest-growing region, powered by rising vehicle production across China, India, and Southeast Asia. Expanding middle-class demand lifts passenger-car sales each year. Local content rules encourage domestic shield manufacturing. As a result, investors building local capacity in India and ASEAN can capture new volume before competitors establish scale in these markets.

Europe and North America anchor demand for advanced, high-temperature shields under strict emissions and safety rules. Data from the European Environment Agency shows 10.8 Million new passenger cars were registered across the EU, Norway, and Iceland in 2025. This large base sustains steady shield fitment despite rising electrification. This means suppliers can match product tiers to each region’s distinct regulatory and buyer profile.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Market Dynamics

Market Opportunity Analysis - Advanced materials, electric vehicle applications, and Asia Pacific localization open the clearest entry points for new players

Non-Metallic materials sit far below the 86.00% held by Metallic in the By Material segment. Ceramic and composite shields serve extreme-temperature zones where metal adds too much weight. This gap widens as engines run hotter and EVs demand new barriers. This means new entrants investing in advanced material capability can build share before the segment matures and pricing tightens.

Electric Vehicles trail the 31.20% Passenger Cars hold in the By Vehicle Type segment, yet demand entirely new battery thermal protection. EV makers need barriers that ICE-focused suppliers rarely offer today. This mismatch leaves high-value content poorly served. By contrast, suppliers that specialize in EV battery shielding can capture premium demand ahead of slower legacy competitors.

Sandwich shields remain underexploited against the 41.20% Single Shell holds in the By Product segment. Their combined thermal and acoustic performance suits premium and high-heat platforms. Few suppliers scale this format at competitive cost today. As a result, early movers in sandwich shield production can target premium programs where buyers accept higher pricing for superior protection.

Asia Pacific leads with a 40.10% regional share worth USD 4.46 Billion, yet local organized manufacturing in India and ASEAN stays underbuilt. Local content rules reward domestic production. This creates a clear localization gap for early investors. Instead of exporting into these markets, players building regional capacity can secure volume before competitors establish scale.

Technology and Innovation Landscape - Higher operating temperatures drive next-generation shield material development

A 2025 SAE International technical paper states that conventional under-hood automotive heat shields are typically designed for average operating temperatures up to 225°C. This limit reflects the thermal ceiling of standard stamped metal designs. Rising engine complexity now tests that boundary. This means suppliers relying on legacy materials risk losing programs to rivals offering higher-temperature solutions.

The same 2025 SAE paper reports that newer internal combustion engine designs may raise average operating temperatures to approximately 300°C, requiring improved shield materials. This 75°C jump forces a shift toward advanced alloys and composites. Standard shields cannot safely handle the added load. As a result, manufacturers that develop thermo-oxidative resistant materials can win the next generation of hotter engine platforms.

Advanced composite and multi-layer construction offers a path to meet these higher thermal demands while cutting weight. Aerogel and ceramic fiber materials sustain extreme heat that metal alone cannot. This supports both hotter ICE engines and EV battery barriers. This means suppliers investing in multi-material lamination gain a technical edge across two growing application areas at once.

Drivers

Tighter emissions rules directly expand heat shield content per vehicle. EU Regulation 2024/1257, or Euro 7, enters force for new light-duty models from November 2026, alongside U.S. EPA standards for model year 2027. These rules push catalytic converters and filters closer to the engine, creating gas temperatures between 600°C and 950°C in zones once below 450°C. This forces automakers to add more shielding per platform.

A compliant Euro 7 platform typically adds 3–6 heat shield components per vehicle versus its Euro 6 predecessor. This raises total shield content value per vehicle by an estimated 18–28%. OEM sourcing now embeds suppliers into powertrain programs 24–36 months before production. As a result, manufacturers gain revenue visibility that justifies investment in hydroforming and high-temperature alloy capacity at scale.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening Emissions Standards Mandating Advanced Aftertreatment & Exhaust Thermal Management | +1.65% | European Union, India, United States, China | Short term (≤ 2 years) |

| Turbocharged & GDI Engine Proliferation Expanding Per-Vehicle Heat Shield Content | +1.25% | Global — led by Europe, China, North America | Short term (≤ 2 years) |

| Commercial Vehicle Fleet Growth & SCR/DPF Integration Requirements | +0.90% | India, China, Brazil, North America | Medium term (2–4 years) |

| Rising SUV & Pickup Truck Mix Increasing Underbody Shielding Surface Area | +0.70% | North America, China, Middle East, Australia | Short term (≤ 2 years) |

| Shift to Lightweight Multi-Layer & Double-Shell Shield Configurations | +0.55% | Global — concentrated at European & Japanese OEM programs | Medium term (2–4 years) |

| Expanding Aftermarket Replacement Cycle in Aging Global Vehicle Parc | +0.37% | North America, Europe, Middle East & Africa | Short term (≤ 2 years) |

Restraints

Battery electric vehicles carry no engine, exhaust, or catalytic converter, removing shields worth an estimated 60–70% of content value per conventional vehicle. China’s new-energy vehicle share of registrations topped 50% monthly from mid-2024, shrinking the addressable ICE shield pool. Europe’s battery EV share settled near 15–18% in 2025. This means suppliers face a structural decline in exhaust-related shield demand across major markets.

A mid-size ICE car carries exhaust shield content worth about USD 45–90 at OEM pricing, while the equivalent battery EV carries near-zero legacy content. Premium European ICE shield volumes fell an estimated 8–12% year-on-year in 2024 to 2025. This forces portfolio diversification into commercial and EV battery applications. As a result, suppliers need 12–24 months of qualification investment before new revenue arrives.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Battery EV Penetration Eliminating Exhaust-Adjacent Heat Shield Content | -1.20% | China, Europe, North America, South Korea | Medium term (2–4 years) |

| Aluminum & Stainless Steel Raw Material Price Volatility Compressing Margins | -0.75% | Global — most acute in import-dependent emerging markets | Short term (≤ 2 years) |

| Cross-Border Trade Tariffs Disrupting Integrated Supply Chains | -0.50% | United States, Canada, Mexico, European Union | Short term (≤ 2 years) |

| OEM Powertrain Sourcing Freeze During Platform Electrification Transition | -0.35% | Europe, North America | Medium term (2–4 years) |

| High Tooling & Dies Investment Limiting Agility of Smaller Tier-2 Suppliers | -0.27% | South Asia, Southeast Asia, Eastern Europe | Long term (≥ 4 years) |

Challenges

Multiple coexisting powertrains create a combinatorial explosion of unique shield geometries. Naturally aspirated, turbocharged, mild hybrid, and full hybrid designs each need a bespoke shield profile. A mid-sized Tier-1 supplier serving 8–12 OEM programs in 2026 may manage over 350–500 distinct part numbers, up from about 200–250 five years prior. This proliferation fragments production and raises complexity across stamping plants.

This fragmentation lifts tooling cost per unit by an estimated 18–25% and adds 45–90 minutes of changeover downtime per product-family transition. Modular tooling that absorbs 15–20% geometry variation offers a path forward. Building it requires USD 8–20 Million in tooling research and 3–5 years to deploy. This creates a clear revenue stream for suppliers that master flexible, high-mix manufacturing before rivals.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Multi-Geometry SKU Proliferation Complexity | -0.65% | Global — concentrated at Tier-1 & Tier-2 stamping plants | Long term (≥ 4 years) |

| High-Temperature Forming & Fabrication Skill Gap | -0.55% | South Asia, Southeast Asia, Eastern Europe | Long term (≥ 4 years) |

| Hybrid Powertrain Thermal Cycle Durability Validation | -0.45% | Global — concentrated in OEM hybrid platform programs | Medium term (2–4 years) |

| Counterfeit & Sub-Standard Aftermarket Shield Proliferation | -0.35% | South Asia, Southeast Asia, Sub-Saharan Africa, Latin America | Long term (≥ 4 years) |

| Weight Reduction vs. Thermal Performance Trade-Off | -0.30% | Global — most acute in European & Japanese OEM programs | Medium term (2–4 years) |

Opportunities

EV battery thermal barriers form structurally untapped white space for shield makers. Battery thermal runaway events generate cell temperatures above 700–1,000°C within milliseconds. Standards like UN ECE Regulation No. 100 and China’s GB/T 38661-2020 demand barriers that hold integrity for at least 5 minutes post-event. This means standard stamped metal shields cannot meet the need without major reformulation.

New materials like aerogel composites and mica laminates command USD 80–180 per battery module shield versus USD 12–35 for exhaust shields. This delivers gross margins of 28–40% against the 12–18% typical of conventional shields. Fewer than 20–25% of established makers had qualified EV barrier products by 2025. As a result, early movers can capture a high-margin, underserved market with lasting advantage.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| EV Battery Pack Thermal Barrier & Fire Suppression Shield Integration | +1.55% | China, Europe, North America, South Korea | Medium term (2–4 years) |

| Aerogel & Advanced Composite Multi-Layer Shield Premiumization | +0.90% | Europe, North America, Japan | Long term (≥ 4 years) |

| Heavy-Duty Off-Highway & Industrial Engine Shield Crossover | +0.70% | North America, Australia, Middle East, India | Long term (≥ 4 years) |

| India & ASEAN Local Manufacturing Capacity Buildout | +0.55% | India, Vietnam, Indonesia, Thailand | Short term (≤ 2 years) |

| Exhaust Heat Recovery System Shield Integration Upsell | +0.40% | Europe, Japan, North America | Long term (≥ 4 years) |

Key Company Insights

ElringKlinger AG positions itself as a thermal management leader pivoting toward electrification. The company showcased next-generation shielding, sealing, and lightweight battery components for electric vehicles at IAA Mobility 2025 in September 2025. This aligns its portfolio with a shifting market where more than 20% of new cars sold worldwide in 2024 were electric, according to the International Energy Agency. This creates an advantage as demand moves from exhaust shields toward EV battery thermal barriers.

Autoneum Holding AG anchors its strategy in acoustic and thermal management with a strong push into EV safety products. The company launched E-Fiber mica-free flame shields to improve battery safety and thermal shielding in March 2025. This early move into EV-specific barriers positions Autoneum ahead of slower rivals. However, its concentration in interior and acoustic products leaves competitive risk if metallic shield demand recovers unexpectedly.

Key Players

- Tenneco Inc.

- Dana Incorporated

- ElringKlinger AG

- Autoneum Holding AG

- Alkegen

- Morgan Advanced Materials

- Lydall Inc.

- Carcoustics International GmbH

- FAURECIA SE

- Benteler International AG

- Zircotec Ltd.

- Federal-Mogul (Tenneco)

Recent Developments

- May 2025 – ElringKlinger announced continued ramp-up of high-volume series production for its electromobility business, including cell contacting systems used in advanced EV battery applications.

- March 2025 – Autoneum launched its new E-Fiber flame shields, introducing a mica-free flame protection solution for electric vehicles to improve battery safety and thermal shielding.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 11.14 Billion |

| Forecast Revenue (2035) | USD 18.88 Billion |

| CAGR (2026-2035) | 5.42% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Single Shell, Double Shell, Sandwich), By Material (Metallic (Aluminum, Stainless Steel), Non-Metallic (Ceramic, Composite)), By Application (Engine Compartment, Exhaust System, Turbocharger, Under Bonnet, Under Chassis), By Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCV), Heavy Commercial Vehicles (HCV), Electric Vehicles (EV)), By Sales Channel (OEM, Aftermarket) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Tenneco Inc., Dana Incorporated, ElringKlinger AG, Autoneum Holding AG, Alkegen, Morgan Advanced Materials, Lydall Inc., Carcoustics International GmbH, FAURECIA SE, Benteler International AG, Zircotec Ltd., Federal-Mogul (Tenneco) |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |