Global Wrapping Machine Market Size, Share, And Industry Analysis Report By Machine Type (Stretch, Shrink, Others), By Mode of Operation (Automatic, Semi-automatic), By Application (Food, Beverages, Chemicals, Personal Care, Pharmaceuticals, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 182548

- Number of Pages: 292

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

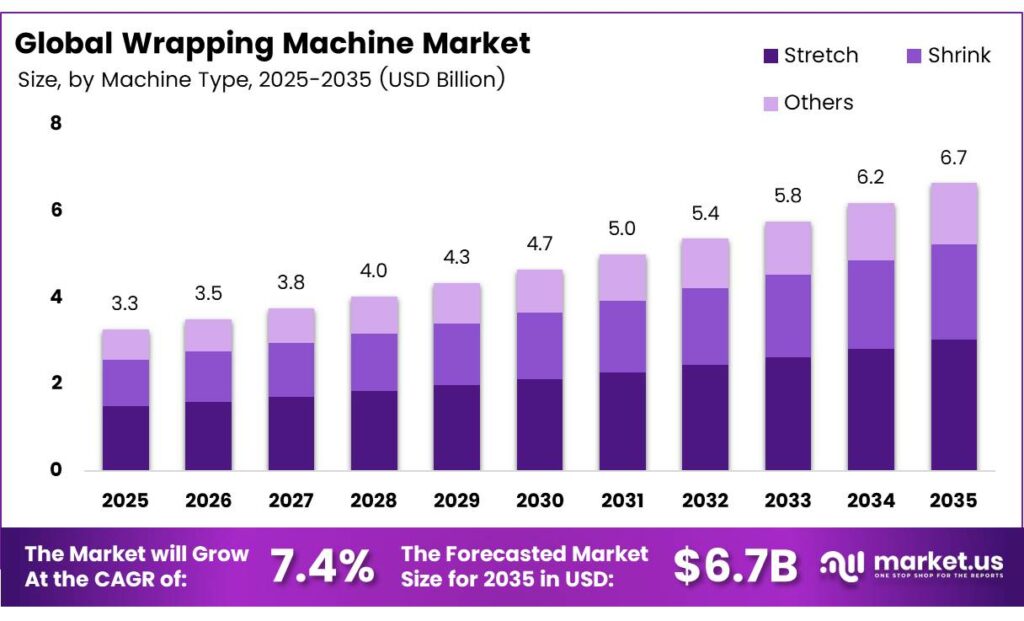

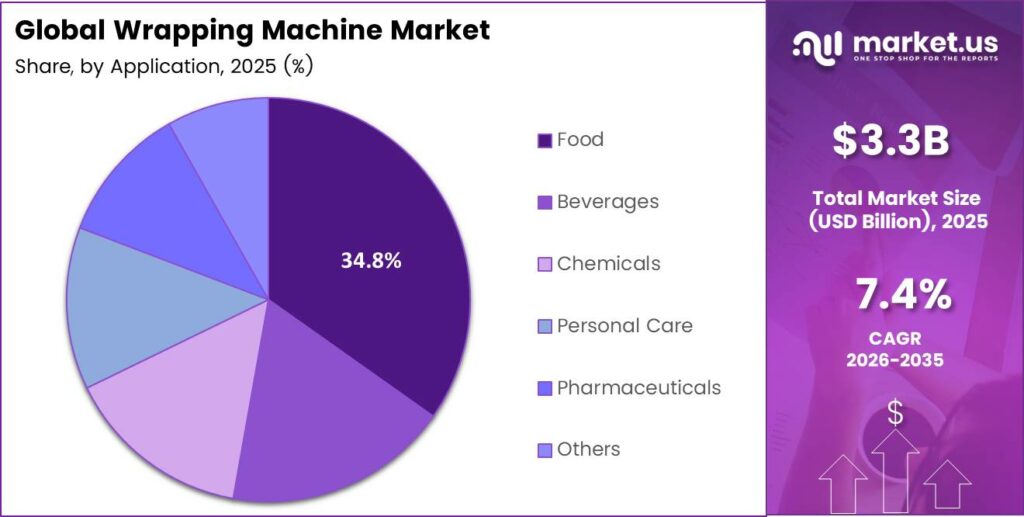

The Global Wrapping Machine Market size is expected to be worth around USD 6.7 billion by 2035 from USD 3.3 billion in 2025, growing at a CAGR of 7.4% during the forecast period 2026 to 2035.

The wrapping machine market covers industrial equipment designed to wrap, seal, and protect products for storage and transport. These machines serve sectors such as food and beverage, pharmaceuticals, chemicals, and personal care. Manufacturers use wrapping systems to ensure product integrity, reduce damage, and meet safety standards throughout the supply chain.

Modern wrapping machines include stretch wrappers, shrink tunnel systems, and hybrid automated lines. Each type addresses specific load stabilization and packaging requirements. Moreover, the shift toward automation has pushed manufacturers to adopt smarter systems capable of handling variable load sizes without manual intervention.

Global trade in packing or wrapping machinery reached $9.75 billion in 2024, increasing from $9.69 billion in 2023. This stable growth in trade volume reflects sustained industrial equipment demand across manufacturing economies worldwide.

European Union exports of packing or wrapping machinery reached $4,669,247,930 in 2024, making the EU the largest exporting region globally. This dominance highlights Europe’s deep manufacturing expertise in precision packaging equipment and its strong distribution networks into emerging markets.

Supply chain disruption events over the past several years have accelerated demand for reliable pallet-stabilization equipment. E-commerce fulfillment centers now handle millions of shipments weekly, creating a constant need for high-speed, automated wrapping systems. Additionally, labor shortages in warehouse operations have made fully automated wrapping solutions a strategic necessity rather than an optional upgrade.

Key Takeaways

- The Global Wrapping Machine Market is valued at USD 3.3 billion in 2025 and is projected to reach USD 6.7 billion by 2035, growing at a CAGR of 7.4%.

- Stretch wrapping machines dominate with a 43.6% market share in 2025.

- Semi-automatic machines hold the largest share at 54.2%.

- The Food segment leads with a 34.8% share.

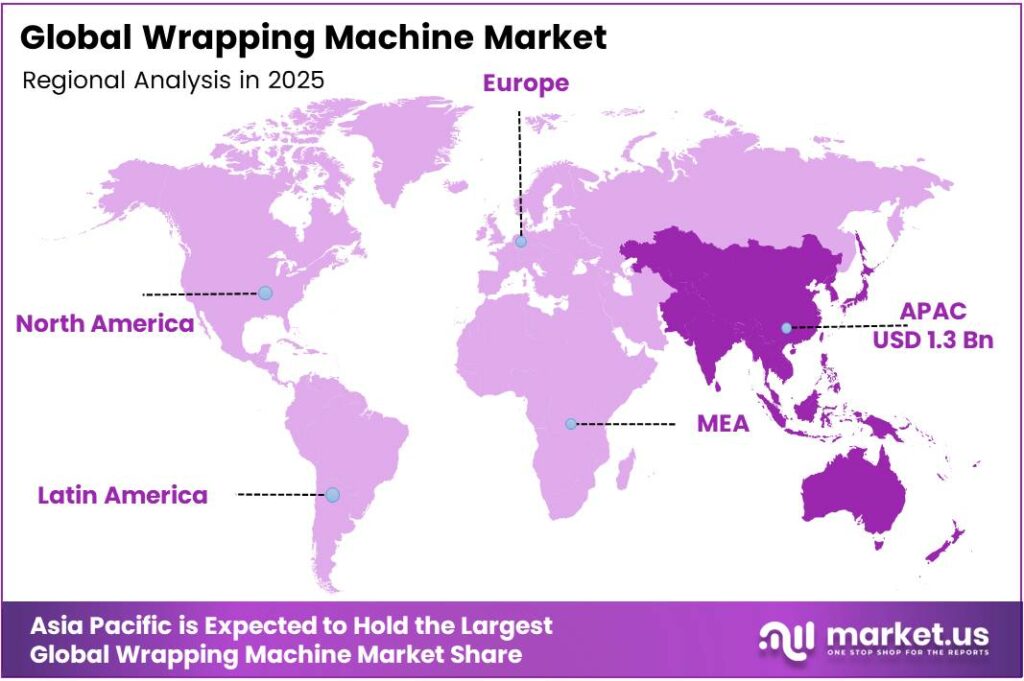

- Asia Pacific is the dominant region, holding a 39.5% share valued at approximately USD 1.3 billion in 2025.

By Machine Type Analysis

Stretch wrapping machines dominate with 43.6% due to their versatility in pallet stabilization across industries.

In 2025, Stretch wrapping machines held a dominant market position in the By Machine Type segment of the Wrapping Machine Market, with a 43.6% share. Stretch systems lead because they deliver reliable load containment at low film cost. Industries ranging from food distribution to chemical manufacturing depend on stretch wrappers to secure pallets during high-volume shipments.

Shrink wrapping machines serve sectors requiring tamper-evident, form-fitting packaging. Beverage and pharmaceutical companies favor shrink systems because they provide a tight, protective seal around individual products and multipacks. Additionally, shrink technology integrates well with high-speed automated lines used in consumer goods manufacturing.

By Mode of Operation Analysis

Semi-automatic machines dominate with 54.2% due to their cost-efficiency and operational flexibility for mid-sized facilities.

In 2025, Semi-automatic machines held a dominant market position in the By Mode of Operation segment of the Wrapping Machine Market, with a 54.2% share. Semi-automatic systems appeal strongly to small and medium enterprises that require reliable output without the capital investment of fully automated lines. These machines offer operators manual control at critical points while automating repetitive wrapping cycles.

Automatic wrapping machines represent the fastest-growing sub-segment as warehouses scale operations. Large distribution centers and multinational manufacturers adopt fully automated systems to address labor shortages and increase throughput. Moreover, robotic turntable and rotary arm systems now handle thousands of pallets per shift without human involvement, driving growing adoption.

By Application Analysis

The food segment dominates with 34.8% due to strict hygiene standards and high-volume packaging requirements in food production.

In 2025, the Food segment held a dominant market position in the By Application segment of the Wrapping Machine Market, with a 34.8% share. Food manufacturers require wrapping systems that meet hygiene certifications, withstand wash-down environments, and operate at high speeds. Consequently, wrapping equipment built for food applications commands premium pricing and sustained replacement cycles.

The Beverages segment drives demand for high-speed shrink and stretch equipment across bottling and canning operations. Beverage producers package millions of units daily, requiring consistent load integrity during pallet transport. Therefore, automated wrapping lines tailored for beverage multipacks represent a significant and growing application category.

The Chemicals segment relies on wrapping machines to contain hazardous materials and heavy industrial loads safely. Drum and sack wrapping systems designed for chemical applications require corrosion-resistant components. Additionally, regulatory compliance for chemical packaging pushes buyers toward certified, purpose-built wrapping machinery.

Key Market Segments

By Machine Type

- Stretch

- Shrink

- Others

By Mode of Operation

- Automatic

- Semi-automatic

By Application

- Food

- Beverages

- Chemicals

- Personal Care

- Pharmaceuticals

- Others

Emerging Trends

Hybrid Automation and Energy-Efficient Mechanisms Reshape Wrapping Operations

Manufacturers increasingly adopt hybrid automation solutions that combine stretch and shrink wrapping capabilities in a single system. This consolidation reduces floor space requirements and lowers operational complexity. Moreover, pneumatic and energy-efficient drive mechanisms are replacing older hydraulic systems, cutting electricity consumption and minimizing film waste across high-volume packaging facilities worldwide.

Smart Customization and Worker Safety Features Drive Equipment Design

Wrapping equipment designers now prioritize ergonomic safety features that reduce operator injury risk on busy packaging floors. Customizable wrapping programs for variable load sizes allow facilities to handle diverse product ranges without retooling. Additionally, sensor-driven load profiling and real-time adjustments enable manufacturers to adapt wrapping parameters instantly, improving consistency and reducing product damage during shipment.

Drivers

E-Commerce Expansion and Supply Chain Demands Accelerate Wrapping Equipment Adoption

Global e-commerce growth places intense pressure on fulfillment centers to stabilize and protect high volumes of palletized shipments. Distribution networks require reliable pallet wrapping systems capable of handling thousands of loads per shift. China exported wrapping machinery valued at $804,601,230 in 2024, with a total shipment volume of 7,228,960 units, reflecting surging global production capacity to meet this demand.

Labor Shortages and Sustainability Mandates Push Facilities Toward Automated Solutions

Acute warehouse labor shortages across North America and Europe compel facilities to replace manual wrapping stations with fully automated systems. Simultaneously, corporate sustainability commitments drive demand for film-optimization technologies that reduce plastic consumption per pallet. Therefore, wrapping machine suppliers that offer both automation capability and sustainability-certified film management gain a clear competitive advantage in current procurement cycles.

Restraints

High Capital Costs and Long Payback Periods Deter Small Enterprise Investment

Elevated upfront equipment costs and extended return-on-investment periods remain significant barriers for small and medium enterprises considering automation upgrades. Many SMEs operate thin margins that make large capital expenditures difficult to justify against incremental productivity gains. Consequently, budget-constrained buyers often defer automated wrapping investments, favoring manual or semi-automatic alternatives that carry lower purchase prices.

Legacy Infrastructure Compatibility Challenges Slow Modern System Deployment

Technical compatibility issues between modern wrapping machinery and existing legacy packaging lines create substantial deployment friction for manufacturers. Older conveyor systems, control architectures, and plant layouts do not always accommodate new automated wrappers without significant retrofitting. Additionally, integration costs and production downtime during installation further reduce the attractiveness of upgrading packaging lines for cost-sensitive operations.

Growth Factors

Paper-Based Wrapping Alternatives and Mobile Robotic Systems Unlock New Market Segments

Rising adoption of paper-based pallet wrapping alternatives offers manufacturers a viable path to reducing plastic use without sacrificing load performance. Simultaneously, mobile and robotic wrapping systems enable decentralized facilities to wrap loads wherever they are staged, eliminating fixed-station limitations. Germany exported $1,863,691,400 worth of packing or wrapping machinery in 2024, reflecting robust industrial manufacturing capacity supporting these advanced product lines.

Smart Sensor Integration and Regulatory Compliance Drive Next-Generation Equipment Development

Smart sensor integration for real-time load stability monitoring transforms wrapping machines into connected data assets within Industry 4.0 supply chains. Predictive analytics built on sensor data allows operators to anticipate film breaks and load failures before they occur. Moreover, machinery developers are investing heavily in compliant designs that satisfy new U.S. and EU sustainable packaging mandates taking effect in 2026, creating strong forward-looking demand.

Regional Analysis

Asia Pacific Dominates the Wrapping Machine Market with a Market Share of 39.5%, Valued at USD 1.3 Billion

Asia Pacific leads the global wrapping machine market, holding a 39.5% share valued at approximately USD 1.3 billion in 2025. Rapid industrialization, expanding e-commerce infrastructure, and growing food and beverage manufacturing activity across China, India, and Southeast Asia sustain this dominance. Additionally, government-backed industrial automation programs in the region accelerate wrapping equipment procurement among large and mid-sized manufacturers.

North America maintains a strong position in the wrapping machine market, driven by large-scale warehouse automation investments and advanced food processing operations. The United States leads regional demand, with distribution centers upgrading to robotic wrapping systems to address persistent labor shortages. Moreover, sustainability regulations pushing plastic reduction in packaging are accelerating the adoption of advanced film-management wrapping equipment across the region.

The Middle East and Africa market for wrapping machines expands steadily as food processing, petrochemical, and logistics sectors invest in modern packaging infrastructure. Gulf Cooperation Council countries drive regional demand through large-scale port and warehouse development projects. However, limited local manufacturing capacity means the region depends heavily on European and Asian equipment imports to supply its growing packaging needs.

Latin America represents a growing opportunity for wrapping machine suppliers as food and beverage export industries in Brazil and Mexico scale up packaging operations. Infrastructure investments and trade agreements are encouraging manufacturers to modernize their packaging lines.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Robopac is a global leader in stretch and shrink wrapping systems, offering a comprehensive portfolio of semi-automatic and fully automatic machines. The company focuses on integrating IoT connectivity and film-optimization technologies into its equipment. Robopac serves high-volume industries, including food, beverage, and logistics, and continues to expand its presence across North America, Europe, and the Asia Pacific through targeted distribution partnerships.

Orion Packaging Systems LLC specializes in rotary arm and turntable stretch wrappers designed for heavy-duty pallet stabilization in demanding warehouse environments. The company builds its products around operational durability and ease of maintenance, making it a preferred supplier for distribution centers managing continuous high-throughput operations. Orion consistently advances its automation portfolio to address growing demand for labor-reducing packaging solutions across North American markets.

Lantech holds a recognized position in the wrapping machine industry as a pioneer of stretch wrapping technology since the early development of pallet unitizing systems. The company’s product range includes turntables, rotary arms, and horizontal stretch wrappers serving manufacturing and logistics clients globally. Lantech focuses on sustainability by engineering machines that reduce film usage per pallet while maintaining load integrity across diverse shipping conditions.

Phoenix Wrappers delivers customized wrapping solutions for industries requiring specialized packaging configurations, including cold storage and hazardous material handling environments. The company emphasizes flexible machine design that accommodates varied load sizes, film types, and wrapping programs. Phoenix Wrappers supports clients through lifecycle service programs and technical customization, positioning itself as a solution-focused partner for mid-market and industrial packaging operations worldwide.

Top Key Players in the Market

- Robopac

- Orion Packaging Systems LLC

- Lantech

- Phoenix Wrappers

- Durapak

- Matco International

- ProMach Inc.

- Coesia S.p.A

- I.M.A. Industria Macchine Automatiche S.p.A.

- Syntegon Technology GmbH

Recent Developments

- In February 2026, Orion launched the American-made Flex Legion Turntable Pallet Wrapper. This new model strengthens the company’s domestic manufacturing capabilities and expands its automation portfolio for pallet wrapping solutions. Parent company ProMach acquired DJS Systems, a leading automation supplier for the disposable food packaging market.

- In March 2026, Lantech introduced the fully automated Parcel Pack system (comprising the TE Parcel Tray Erector and LA Parcel Lid Applicator). It produces up to 1,000 perfectly rectangular corrugated cardboard letterbox-format trays per hour for e-commerce and fulfillment. Key benefits include cost savings on shipping, built-in cushioning without extra padding, compact design for better truck loading/lower CO₂ emissions, and easy integration.

Report Scope

Report Features Description Market Value (2025) USD 3.3 Billion Forecast Revenue (2035) USD 6.7 Billion CAGR (2026-2035) 7.4% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Machine Type (Stretch, Shrink, Others), By Mode of Operation (Automatic, Semi-automatic), By Application (Food, Beverages, Chemicals, Personal Care, Pharmaceuticals, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Robopac, Orion Packaging Systems LLC, Lantech, Phoenix Wrappers, Durapak, Matco International, ProMach Inc., Coesia S.p.A, I.M.A. Industria Macchine Automatiche S.p.A., Syntegon Technology GmbH Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Robopac

- Orion Packaging Systems LLC

- Lantech

- Phoenix Wrappers

- Durapak

- Matco International

- ProMach Inc.

- Coesia S.p.A

- I.M.A. Industria Macchine Automatiche S.p.A.

- Syntegon Technology GmbH

Our Clients

- 182548

- March 2026