Quick Navigation

Report Overview

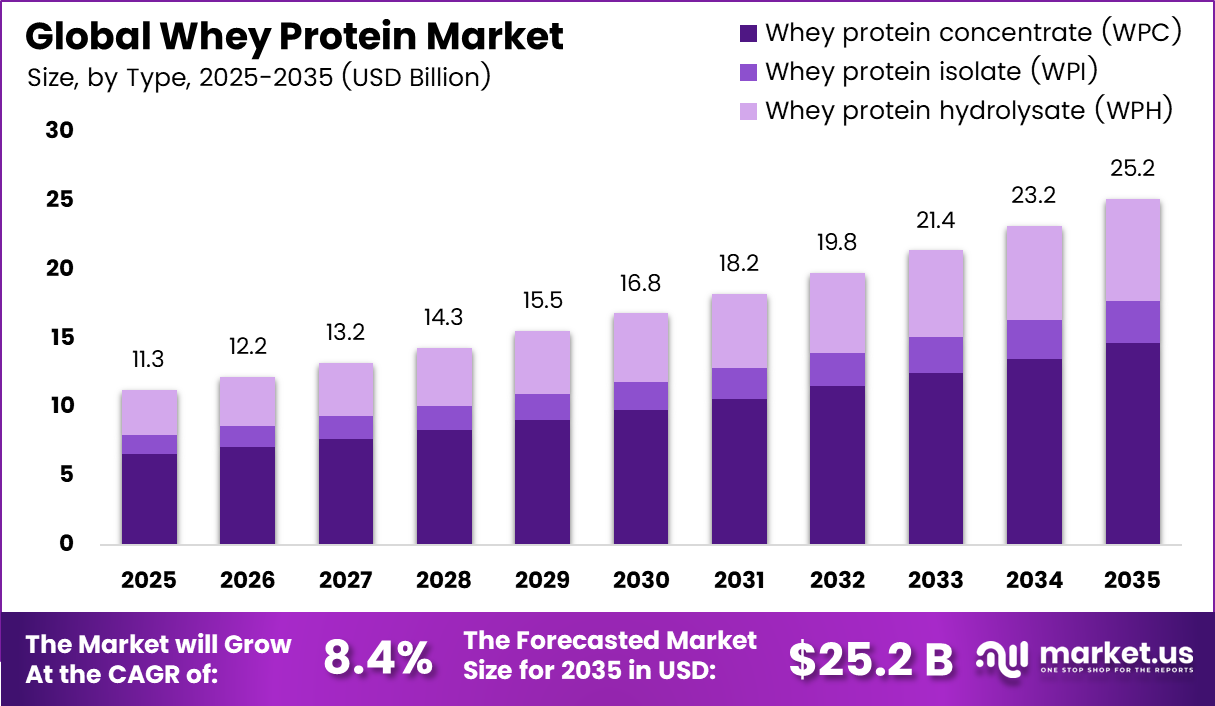

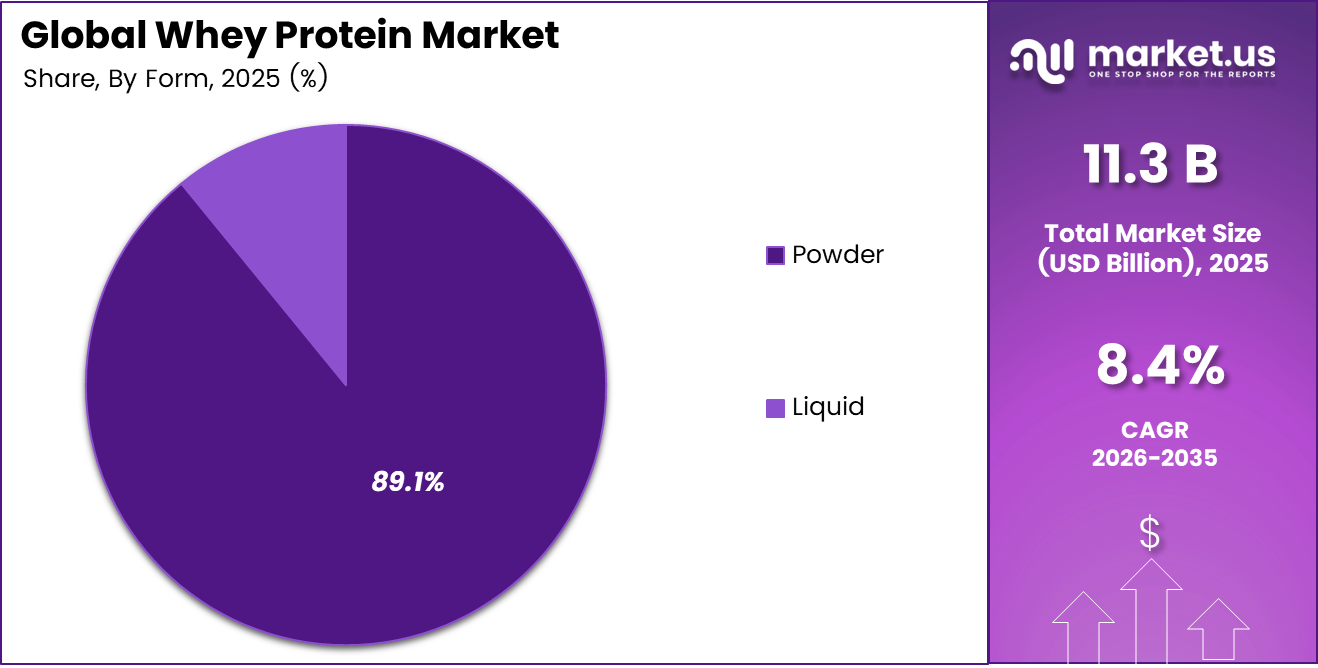

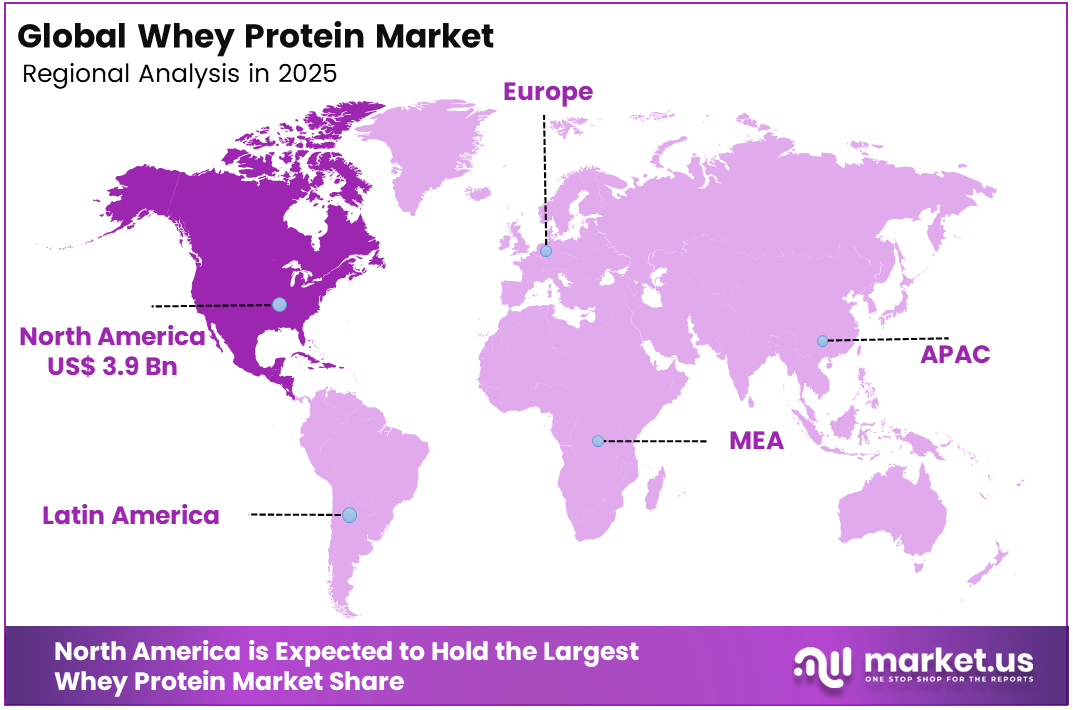

The Global Whey Protein Market size is expected to be worth around USD 11.3 billion by 2025, growing at a CAGR of 8.4% during the forecast period from 2026 to 2035, reaching USD 25.2 billion by 2035. North America held a dominant market position, capturing more than a 34.8% share, holding USD 3.93 billion in revenue.

Optimum Nutrition revealed in February 2026 that its popular Gold Standard 100% Whey protein supplement, which is the most highly sought after in the market globally, crossed the mark of having sold more than one billion cumulative units, with over 70% of total sales in 2025 made from North America and the Asia Pacific collectively.

Whey protein is of high biological value and is a complete source of protein that is produced as a by-product of cheese and casein processing, and it is used in many applications ranging from sports nutrition to clinical nutrition and pet foods. Whey protein can be classified as three main products: whey protein concentrate (WPC), whey protein isolate (WPI), and whey protein hydrolysate (WPH). It contains all the essential amino acids and is highly bioavailable; therefore, it is considered the gold standard of protein ingredients against which all other protein sources are compared.

Factors boosting the global whey protein market include the increasing trend toward a global fitness culture, the demand for whey proteins from institutional customers in the segments of clinical and infant nutrition, and the burgeoning Asian-Pacific sports nutrition market that is seeing premiumization of protein sales grow at double-digit growth rates. E-commerce and subscription nutrition services are further adding to the demographic base of buyers.

Key Takeaways

- The global whey protein market size is forecast to have a market valuation of US$ 11.3 billion in 2025.

- The global whey protein market size is anticipated to achieve a market valuation of US$ 25.2 billion by 2035.

- It will register a CAGR of 8.4% through the forecast period from 2026 to 2035.

- The type segment is dominated by Whey Protein Concentrate (WPC), which occupies 58.3% of the market share because of its cost-effectiveness and increased use in formulations.

- Powder form takes precedence over other forms because of its 89.1% share due to its long shelf life and easy usage in dietary supplements.

- Sports and performance nutrition account for the largest application segment, occupying 32.5% market share because of increased awareness about fitness.

- Food Grade commands a large 70.4% share in the grade segment because of widespread usage in food and beverages.

- North America has the largest regional market share, accounting for 34.8% of the market, due to increased usage of health supplements.

Type Analysis

Whey Protein Concentrate (WPC) Dominates Market through Cost-Efficiency and Broad Application Versatility

Market for Whey Protein Concentrate (WPC) enjoys a dominant position in the product types market with a revenue share worth 58.3% in 2025, owing to the cost-effective nature of the production process, with protein levels between 29% and 89%, coupled with ready availability as a co-product from the global cheese production industry of more than 22.5 million metric tons per annum in 2024.

For instance, according to the USDA Dairy Export Council’s annual trade data released in early 2025, WPC exports from the United States were estimated to have reached 320,000 metric tons during 2024, registering an increase of 9.2% year-on-year, with Asia Pacific food producers and sports nutrition brands representing the fastest-growing buyer segments.

Whey Protein Isolate (WPI) takes 12.2% share as the solution for lactose-intolerant customers and clinical nutrition, with protein purity above 90%. Whey Protein Hydrolysate (WPH) makes up 29.5% of the segment and is experiencing rapid growth supported by hypoallergenic infant formulas and elite sports nutrition use cases.

Form Analysis

Powder Form Dominates Market through Superior Shelf Life and Supply Chain Compatibility

Powder Form takes precedence by commanding 89.1% market revenue contribution in 2025, due to its attributes such as room-temperature storage, 18-24 months shelf-life, and easy adaptability to the sports nutrition/functional food manufacturing process on a large scale across the globe. The dominance of Powder Form is further supported by its feasibility for online selling and cross-border retail sales without the requirement for cold chain logistics support.

For instance, Optimum Nutrition, Dymatize, and MyProtein collectively dominated global whey protein powder sales in 2025, with North America and Europe representing the largest per-capita consuming regions for whey powder-based supplements, supported by the United States alone generating over US$ 1.8 billion in annual whey protein export revenue according to the US Dairy Export Council’s Annual Trade Report 2025.

The whey protein liquid form accounts for 10.9% market share, driven by growing consumption of ready-to-drink (RTD) protein shakes, with the RTD category poised for a CAGR of 11.2% up to 2030. Nevertheless, cold chain requirements, shorter shelf life, and higher logistics costs restrict the penetration ability of the liquid form versus the powder form up to 2035.

Application Analysis

Sports and Performance Nutrition Dominates Market through Global Fitness Culture and Premium Brand Expansion

The Sports and Performance Nutrition application segment dominates with a revenue share of 32.5% in 2025, owing to more than 210,000 gymnasiums and fitness centers and 1.1 billion people actively engaged, driving structural recurring demand for whey protein for muscle building, energy endurance, and recovery purposes. Premium WPI and WPH segments hold retail prices of US$ 35–80/kg in B2C e-commerce channels, driving high-margin revenues for branded sports nutrition companies that greatly outstrip their ingredient market volume share.

For instance, according to the Optimum Nutrition Press Release dated February 2026, the Gold Standard 100% Whey product accounted for more than 4.2 million SKU sales on Amazon platforms across the US and EU regions each month in 2025, with approximately 62% of purchasers belonging to the recreational fitness age bracket of 25–40 years.

The other application markets account for a combined 67.5% share. Dietary supplements form the second-largest application on account of hypoallergenicity. Food & Beverages fortification is the fastest growing sub-application, while animal feed is a consistent source of commodity-grade WPC consumption.

Grade Analysis

Food Grade Dominates Market through High-Volume Consumption across Consumer Applications

Whey Protein for Food Grade is estimated to account for 70.4% in 2025 as the product finds applications in several consumer-oriented end-user markets such as sports nutrition, functional foods, baking, confectionery products, baby milk formulas, and even animal feed. The whey protein for the food-grade category enjoys FDA GRAS approval as well as EU Novel Foods certification and Codex standards for its use in different countries around the world.

For instance, according to the US Dairy Export Council’s Annual Trade Report published in February 2025, food-grade WPC-80 remained the single largest traded whey protein category globally in 2024, reflecting its unmatched institutional procurement dominance across food manufacturers, sports nutrition brands, and infant formula buyers worldwide.

Pharmaceutical & Clinical Grade is the fastest-growing segment, owing to its use in enteral nutrition, oncological recovery, and geriatric therapy applications that require protein purity greater than 95%. Feed Grade WPC-34 is used in aquaculture and high-end pet food markets.

Key Market Segments

By Type

- Whey Protein Concentrate (WPC)

- Whey Protein Isolate (WPI)

- Whey Protein Hydrolysate (WPH)

By Form

- Powder

- Liquid

By Application

- Sports and Performance Nutrition

- Dietary/Nutritional Supplements

- Infant Formula and Baby Foods

- Food & Beverages

- Animal Feed & Pet Food

By Grade

- Food Grade

- Pharmaceutical / Clinical Grade

- Feed Grade

Opportunity Analysis

Medical‑grade & clinical nutrition whey

Positioning whey as a clinically validated, medical-grade protein for sarcopenia, oncology, metabolic syndrome, and post-operative recovery creates a major opportunity beyond sports nutrition and functional foods. Hospital and medical nutrition currently represent only a low-single-digit share of global whey volumes, indicating a potential market of USD 3–5 billion by 2035 if penetration reaches 10–15% of eligible patients across North America, Europe, China, and Japan.

Suppliers can support adoption through clinical trials, regulatory compliance, and product development partnerships with hospitals and healthcare providers. Clinical whey products could command prices 30–50% above standard sports powders and raise gross margins from 20–25% to 35–40%. Specialized shakes, tube-feeding products, and sachets could deliver further scale benefits, potentially adding around 1.5 percentage points to global market CAGR through 2035.

Opportunity Impact Summary Table

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Medical-grade & clinical nutrition whey | +1.5% | North America, EU, East Asia | Medium term (2–4 years) |

| Precision nutrition & D2C subscription ecosystems | +1.2% | North America core, EU, urban APAC | Short term (≤ 2 years) |

| Affordable whey fortification for mass FMCG | +1.0% | APAC emerging, LATAM, Middle East | Medium term (2–4 years) |

| Sustainable, low-carbon, and traceable whey platforms | +0.8% | EU, UK, North America | Long term (≥ 4 years) |

| Fermented, hybrid animal-plant protein formats | +0.7% | EU, North America, Japan, South Korea | Long term (≥ 4 years) |

| B2B functional ingredients for specialized categories | +0.9% | Global, with APAC and EU hotspot | Short–medium term (≤ 4 years) |

Challenges Analysis

Constrained whey processing capacity

Underinvestment in membrane filtration, spray-drying, and instantization capacity has created a major whey processing bottleneck. U.S. inventories have reportedly fallen by around 50% since 2023, while WPC and WPI prices have increased by 100–130% over the past 18–24 months. Critical plants are operating at 85–90% utilization, creating 10–15% throughput losses and extending normal delivery times by 5–10 days.

This shortage is estimated to reduce market CAGR by around 1.3 percentage points by delaying product launches and limiting supply. Some manufacturers may reduce protein content by 5–10 grams per serving or blend whey with plant proteins. Addressing the issue will require USD 25–60 million in processing investment per site, long-term supply agreements, and improved membrane and drying technologies that could increase throughput by 5–7% over the next 2–4 years.

Challenges Impact Summary Table

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Constrained whey processing capacity | -1.3% | US & EU dairy hubs | Medium term (2-4 years) |

| High-cost import dependence | -1.1% | India & EM sports nutrition | Long term (≥ 4 years) |

| Dairy labor and farm pressure | -0.8% | North America & EU farms | Medium term (2-4 years) |

| Volatile protein input pricing | -1.0% | Global branded manufacturers | Short term (≤ 2 years) |

| Logistics & cold-chain gaps | -0.7% | APAC & MEA corridors | Medium term (2-4 years) |

| Regulatory & sustainability compliance | -0.6% | EU, UK, select APAC | Long term (≥ 4 years) |

Driver Analysis

Cheese-output expansion lifting whey feedstock availability

Whey protein supply is closely linked to cheese production because higher cheese output creates more liquid whey for conversion into dry whey, WPC, and WPI. U.S. cheese production reached 13.38 billion pounds during January–November 2025, rising 2.5% year over year. November output increased 5.9% to 1.218 billion pounds, while Italian cheese production grew 6.8%, expanding sweet-whey availability for processors.

Higher feedstock volumes improve plant utilization and spread filtration and drying costs across more production. However, processors are increasingly prioritizing premium ingredients: cumulative dry whey output declined 3.2%, WPC production fell only 0.4%, and isolate output increased 15.6% in November 2025. This shift toward higher-value whey fractions improves revenue per pound of whey solids and supports market growth across North America and APAC export channels.

Driver Impact Summary Table

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cheese-output expansion lifting whey feedstock availability | +1.6% | North America core, EU core, Oceania export base, APAC import markets | Short term (≤ 2 years) |

| Sports nutrition and high-protein food mainstreaming | +2.1% | North America core, EU, China, India, Southeast Asia, Middle East urban channels | Medium term (2-4 years) |

| Higher-value mix shift toward isolates, RTD, and medical nutrition | +1.8% | North America core, EU premium markets, Japan, South Korea, GCC | Medium term (2-4 years) |

| Regulatory tightening is improving quality assurance and formalization | +1.2% | India, North America, the EU, and cross-border e-commerce corridors | Short term (≤ 2 years) |

| Whey valorization and sustainability economics in dairy processing | +1.0% | EU, North America, Oceania, Latin America spill-over | Medium term (2-4 years) |

| Precision-fermentation competition expanding category innovation | +0.7% | U.S. innovation hubs, EU pending corridors, Asia strategic launch markets | Long term (≥ 4 years) |

Restraint Analysis

Whey input inflation

Raw material and ingredient inflation remains the leading restraint because whey protein costs are closely tied to elevated dairy prices. USDA data show Central U.S. dry whey prices increased from USD 0.4101/lb in January 2024 to USD 0.7162/lb in January 2025 and remained at USD 0.6480/lb in April 2026. In mid-June 2026, weekly edible dry whey prices were still between USD 0.6100 and USD 0.6800/lb, keeping WPC and WPI production costs high before filtration, energy, freight, and packaging expenses.

U.S. whey protein inventories have reportedly fallen by around 50% since 2023, while WPC and WPI prices have increased by more than 50% since early 2026, with WPI reaching nearly USD 11/lb. This pressure could reduce EBITDA margins by an estimated 250–450 basis points for mid-sized sports nutrition brands and lead to retail price increases of 8–15% or smaller pack sizes. As a result, when input inflation is estimated to create a 1.9 percentage-point drag on the 2026 baseline CAGR, particularly in North America and import-dependent Asian markets.

Restraint Impact Summary Table

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Whey input inflation | -1.9% | North America core, EU, import-dependent APAC | Short term (≤ 2 years) |

| Tight protein inventories | -1.6% | U.S., Canada, India, SEA | Short term (≤ 2 years) |

| Demand pull from the formula | -1.2% | U.S., EU, China-linked Asia | Medium term (2-4 years) |

| Labeling compliance drag | -0.9% | North America core, EU retail channels | Medium term (2-4 years) |

| Trade route distortion | -1.1% | EU-China lanes, APAC corridors | Medium term (2-4 years) |

| Alt-protein substitution | -0.8% | U.S., Western Europe, urban APAC | Long term (≥ 4 years) |

Geopolitical Impact Analysis

Trade Policy, Dairy Tariffs, and Sovereign Food Security Reshaping Global Whey Protein Supply Chains

The global supply chain of whey protein is experiencing structural changes arising from three major factors simultaneously occurring: US-China trade disputes, EU sustainability policies, and emerging markets’ state investment initiatives toward food sovereignty. The retaliatory tariffs imposed by China of up to 25% on dairy exports from the US, which have only been partially mitigated by 2024, are prompting American whey manufacturers to expand their export capacity to Southeast Asian countries, Mexico, and the Middle East, to maintain production levels at their cheese-whey manufacturing plants.

European sustainability measures are estimated to raise the cost of compliance for Whey Protein Concentrate (WPC) producers in Europe by 8–14%, thereby providing price competitiveness advantages for Fonterra and US producers. The PLI Scheme of India, with US$ 2.8 billion committed to food processing from 2024 to 2025, aims at making India the future regional hub for processing and exporting whey proteins.

On the other hand, Vision 2030 of Saudi Arabia and the National Food Security Strategy of the UAE have created institutional government demand for clinically approved and infant formula-grade whey proteins, offering multi-year revenue visibility to foreign manufacturers such as Arla Foods, Fonterra, and Lactalis Ingredients.

For instance, according to the Fonterra Co-operative Group Annual Report published in September 2024, Fonterra reported that its Middle East and Africa regional whey protein sales grew 19% year-on-year, with UAE and Saudi Arabian infant formula manufacturers and clinical nutrition procurement agencies representing the fastest-growing buyer segments, directly reflecting the commercial impact of Gulf sovereign food security investment programs on premium whey protein demand.

Regional Analysis

North America Leads Global Whey Protein Market through Integrated Dairy Infrastructure and Strong Nutrition Demand

North America commands the top spot in the worldwide whey protein market with a 34.8% revenue share, valued at about US$ 3.93 Billion in 2025, owing to the presence of the United States which has the world’s biggest cheese and whey protein integrated manufacturing system are producing an output of 6.8 million metric tons of cheese in 2024 while yielding the highest amount of whey co-products worldwide for protein extraction.

North America’s leadership position in this market is further bolstered by the presence of the largest number of integrated whey processors in the world, such as Glanbia, Hilmar, and Leprino Foods, along with the US’s fitness industry, military nutrition requirements, and Canada’s high-end infant formula market, all of which have created a demand portfolio that is structured and recession-proof.

For instance, according to the US Dairy Export Council’s Annual Trade Report published in February 2026, US high-protein whey exports reached a record 77,811 metric tons in 2025, a 6% year-on-year increase, with Japan, the European Union, Southeast Asia, and India representing the fastest-growing destination markets, reflecting North America’s strengthening position as the leading global supplier of premium whey protein ingredients.

The Asia Pacific region registers the highest CAGR of 11.4%, thanks to the growth of the health foods industry in China, the protein nutrition trend in India, and growing infant formula sales in Southeast Asia. The Europe region has 24.8% market share based on the regulation requiring the mandatory use of whey proteins in infant formula and high fitness supplements sales in Germany and the UK.

Key Regions and Countries Covered in this Report

- North America

- U.S.

- Canada

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of Middle East & Africa

The whey protein market at an international level can be characterized by moderate to high competitive intensity, involving competition from major dairy co-operatives, ingredient processors, and branded nutritional food companies along value chains.

The competitive advantage for participants within this space is founded on integrated procurement of raw whey through the ability to own or partner with major cheese producers, the ability to produce premium quality WPC-80 and WPI, and distribution capabilities in North America, Europe, and Asia-Pacific markets.

The ongoing market development towards premium nutrition and functionality has increased the competitiveness of branded consumer nutrition food companies like Nestle, Danone, Abbott, and Herbalife among ingredient suppliers.

Pharmaceutical-grade investment in manufacturing capabilities, sustainable sourcing certification, and artificial intelligence-enabled precision nutrition platforms partnerships has made the difference for key providers compared to commodity-based competitors, thus creating opportunities for premium pricing and stable long-term supply agreements with multinational food and nutrition brands into 2035.

Market Key Players

- Glanbia plc

- Fonterra Co-operative Group Ltd.

- Arla Foods / Arla Foods Ingredients

- Hilmar Cheese Company, Inc.

- Saputo Inc.

- Lactalis Ingredients (Lactalis Group)

- FrieslandCampina Ingredients

- Carbery Group

- Alpavit (DMK Group)

- Wheyco GmbH

- Milk Specialties Global

- Leprino Foods Company

- Olam Group (Olam International)

- Agropur Inc. (incl. Davisco Foods International)

- Maple Island Inc.

- Nestlé S.A.

- Danone S.A. (incl. Nutricia)

- Abbott Laboratories (nutrition segment)

- Herbalife Nutrition Ltd.

- GNC Holdings, LLC

- Others

Key Development

- In March 2026, Glanbia plc launched its next-generation WPI-95 Clear Protein ingredient in the US market and secured a US$ 320 million supply agreement with a major consumer sports nutrition brand through 2029, reinforcing its position as the leading premium whey protein ingredient supplier to the North American sports nutrition industry.

- In February 2026, Fonterra Co-operative Group Ltd. commissioned a new high-volume WPC-80 spray drying facility in Waikato, New Zealand, adding 45,000 metric tons of annual production capacity to meet rising Asia Pacific food manufacturer and sports nutrition brand demand for premium-grade whey protein concentrate ingredients.

- In January 2026, Arla Foods Ingredients secured EU Novel Food approval for its Lacprodan HYDRO.365 hydrolyzed WPH peptides product across 12 European countries, enabling commercial launch into clinical nutrition, geriatric supplementation, and hypoallergenic infant formula channels across the European market.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 11.3 Billion |

| Forecast Revenue (2035) | USD 25.2 Billion |

| CAGR (2026-2035) | 8.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Whey Protein Concentrate (WPC), Whey Protein Isolate (WPI), Whey Protein Hydrolysate (WPH)), By Form (Powder, Liquid), By Application (Sports and Performance Nutrition, Dietary/Nutritional Supplements, Infant Formula and Baby Foods, Food & Beverages, Animal Feed & Pet Food), By Grade (Food Grade, Pharmaceutical/Clinical Grade, Feed Grade) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC – China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America – Brazil, Mexico & Rest of Latin America; Middle East & Africa – GCC, South Africa & Rest of MEA |

| Competitive Landscape | Glanbia plc, Fonterra Co-operative Group Ltd., Arla Foods, Arla Foods Ingredients, Hilmar Cheese Company, Inc., Saputo Inc., Lactalis Ingredients, Lactalis Group, FrieslandCampina Ingredients, Carbery Group, Alpavit, DMK Group, Wheyco GmbH, Milk Specialties Global, Leprino Foods Company, Olam Group, Olam International, Agropur Inc., Davisco Foods International, Maple Island Inc., Nestlé S.A., Danone S.A., Nutricia, Abbott Laboratories, Herbalife Nutrition Ltd., GNC Holdings, LLC. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |