Global Water-borne Adhesives Market Size, Share, And Industry Analysis Report By Resin Type (Acrylics, Polyvinyl Acetate (PVA) Emulsion, Ethylene Vinyl Acetate (EVA) Emulsion), By Substrate (Paper and Paperboard, Plastics and Films, Wood and Composites, Metals, Glass and Ceramics), By Application (Flexible Packaging, Tapes and Labels, Paper Converting and Graphic Arts, Laminating and Filmic Structures, Flooring and Carpeting), By End-user (Paper, Board, and Packaging, Building and Construction, Transportation, Healthcare, Electrical and Electronics), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2025-2034

- Published date: February 2026

- Report ID: 177959

- Number of Pages: 203

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

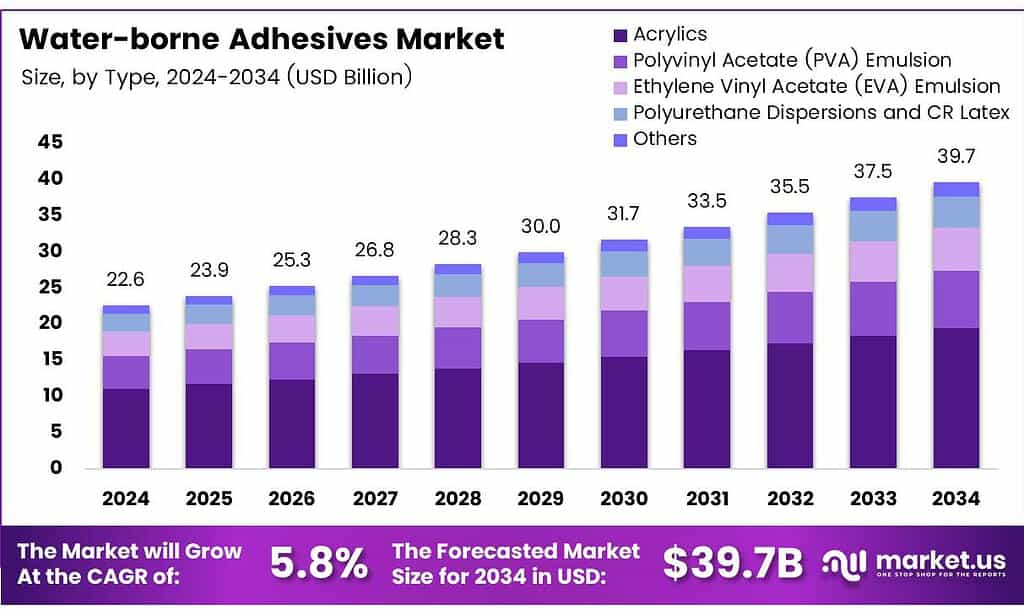

The Global Water-borne Adhesives Market size is expected to be worth around USD 39.7 billion by 2034 from USD 22.6 billion in 2024, growing at a CAGR of 5.8% during the forecast period 2025 to 2034.

Water-borne adhesives represent environmentally friendly bonding solutions that use water as the primary solvent carrier. These adhesive formulations deliver strong bonding performance while significantly reducing volatile organic compound emissions. Moreover, they serve diverse industrial applications requiring sustainable manufacturing practices.

The market encompasses acrylic-based systems, polyvinyl acetate emulsions, and polyurethane dispersions across multiple substrates. Industries increasingly adopt these solutions to meet stringent environmental regulations and consumer sustainability demands. Therefore, water-based bonding technologies replace traditional solvent-based alternatives in packaging, construction, and automotive sectors.

- Investment in Middleton, Massachusetts, reached $27 million in 2025, demonstrating industry commitment to production enhancement. This expansion supports increasing North American demand for sustainable adhesive solutions in durable goods manufacturing.

- China’s exports of adhesive products totaled $874,809.73 thousand and 245,552,000 kilograms in 2024. This substantial export volume reflectsthe Asia Pacific’s dominant manufacturing position and global supply chain significance.

Global demand accelerates, driven by flexible packaging expansion and green building initiatives worldwide. Manufacturers develop fast-drying formulations with enhanced adhesion properties for demanding applications. Consequently, innovation focuses on bio-based polymers and formaldehyde-free compositions that maintain industrial performance standards.

Arkema obtained mass balance ISCC PLUS certification for its waterborne acrylic resins facility in St. Charles, Louisiana. This sustainability certification enables bio-attributed resin production, reducing environmental impact across downstream adhesive applications and strengthening market positioning.

Key Takeaways

- The Global Water-borne Adhesives Market is projected to grow from USD 22.6 billion in 2024 to USD 39.7 billion by 2034 at a CAGR of 5.8%.

- The Acrylics segment leads By Resin Type with 37.5% market share.

- Paper and Paperboard substrate holds 41.7% dominance in substrate segmentation.

- Flexible Packaging application commands 31.9% market share.

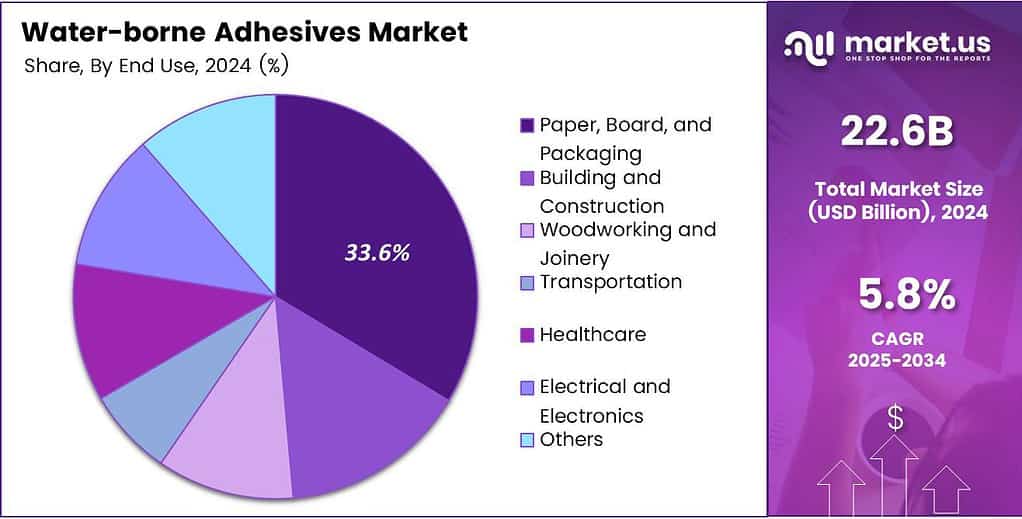

- The Paper, Board, and Packaging end-user segment accounts for 33.6%the of the total market.

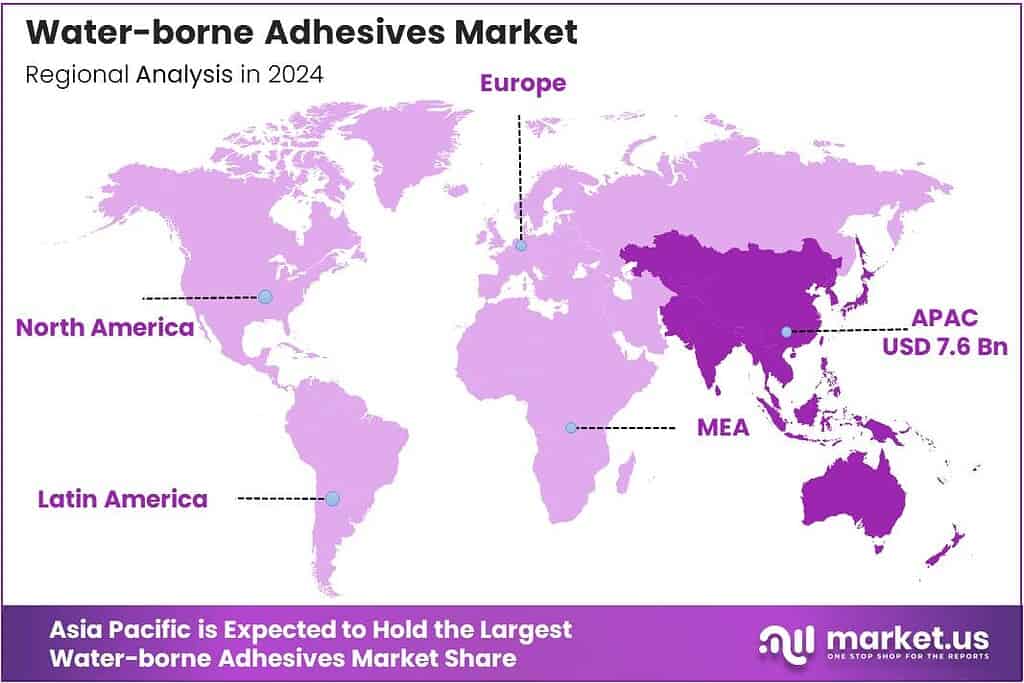

- Asia Pacific dominates the market with 43.1% market share, valued at USD 7.6 billion.

By Resin Type Analysis

Acrylics dominate with 37.5% due to superior adhesion properties and versatile application compatibility.

In 2025, Acrylics held a dominant market position in the By Resin Type segment of the Water-borne Adhesives Market, with a 37.5% share. Acrylic-based formulations deliver exceptional bonding strength across diverse substrates, including paper, plastics, and metals. These resins offer excellent water resistance and UV stability, making them ideal for outdoor applications.

Polyvinyl Acetate (PVA) Emulsion represents cost-effective bonding solutions widely adopted in woodworking and paper converting industries. PVA formulations provide strong initial tack and good adhesion to porous substrates. However, these emulsions demonstrate limited water resistance compared to acrylic alternatives. Therefore, applications focus on interior bonding requirements without moisture exposure concerns.

Ethylene Vinyl Acetate (EVA) Emulsion offers flexible bonding characteristics suitable for packaging and bookbinding applications. EVA-based adhesives maintain adhesion across temperature variations and substrate movement. Additionally, these formulations provide excellent compatibility with various coating processes. Consequently, manufacturers utilize EVA emulsions for specialty applications requiring elastic bond lines.

Polyurethane Dispersions and CR (Chloroprene Rubber) Latex deliver high-performance bonding for demanding industrial applications. Polyurethane dispersions provide superior chemical resistance and durability in the automotive and construction sectors. CR latex formulations offer excellent heat resistance and dynamic strength for specialized applications. Nevertheless, higher costs limit widespread adoption compared to commodity resin types.

By Substrate Analysis

Paper and paperboard dominate with 41.7% due to extensive packaging and converting applications globally.

In 2025, Paper and Paperboard held a dominant market position in the By Substrate segment of the Water-borne Adhesives Market, with a 41.7% share. This substrate category drives significant adhesive consumption across corrugated packaging, folding cartons, and labeling applications. Water-based formulations provide excellent fiber penetration and bonding strength for paper materials.

Plastics and Films represent growing substrate categories driven by flexible packaging expansion in the food and consumer goods sectors. Adhesive formulations for plastic substrates require specialized surface chemistry to achieve adequate wetting and adhesion. Manufacturers develop corona-treated film bonding solutions with enhanced interfacial strength. Therefore, innovation focuses on multi-layer lamination structures requiring optical clarity and barrier properties.

Wood and Composites consume substantial adhesive volumes for furniture manufacturing, cabinetry, and construction applications worldwide. Water-borne wood adhesives replace formaldehyde-containing alternatives to meet indoor air quality standards. These formulations provide durable bonds resistant to moisture and mechanical stress.

Metals, Glass and Ceramics, and other substrates require specialized bonding solutions for industrial assembly applications. Metal bonding adhesives deliver corrosion resistance and structural integrity in automotive and appliance manufacturing. Glass adhesives provide transparent bonds for architectural and decorative applications.

By Application Analysis

Flexible Packaging dominates with 31.9% due to rapid growth in food, beverage, and consumer goods packaging.

In 2025, Flexible Packaging held a dominant market position in the By Application segment of the Water-borne Adhesives Market, with a 31.9% share. This application drives adhesive demand for stand-up pouches, sachets, and multilayer film laminates globally. Water-based laminating adhesives meet food contact regulations while delivering excellent barrier properties.

Tapes and Labels represent significant application categories requiring pressure-sensitive and permanent bonding solutions across industries. Water-borne adhesives enable label production with excellent printability and adhesion to diverse container surfaces. These formulations support removable, repositionable, and permanent label constructions for product identification.

Paper Converting and Graphic Arts applications consume water-based adhesives for envelope manufacturing, bookbinding, and decorative laminating operations. These processes require fast-setting formulations with minimal moisture impact on paper substrates. Adhesive systems provide clean application and excellent lay-flat properties for converted paper products.

Laminating and Filmic Structures, Flooring and Carpeting, Bookbinding and Publishing, Non-woven and Hygiene Products, and other applications utilize specialized water-borne adhesives for specific performance requirements. Flooring adhesives provide permanent installation with moisture resistance. Non-woven applications require flexible bonds for diaper and hygiene product manufacturing.

By End-user Analysis

Paper, Board, and Packaging dominate with 33.6% due to extensive adhesive consumption across converting operations.

In 2025, Paper, Board, and Packaging held a dominant market position in the By End-user segment of the Water-borne Adhesives Market, with a 33.6% share. This sector encompasses corrugated box manufacturing, folding carton production, and flexible packaging converting operations worldwide. Water-based adhesives enable high-speed production lines while meeting food safety and environmental compliance requirements.

Building and Construction end-users adopt water-borne adhesives for flooring installation, wall covering, and interior finishing applications globally. These formulations provide low-VOC solutions meeting green building certification standards like LEED and BREEAM. Construction adhesives deliver durable bonds resistant to humidity and temperature variations in building environments.

Woodworking and Joinery industries utilize water-based adhesives for furniture assembly, cabinet manufacturing, and millwork production operations. These applications require strong wood-to-wood bonds with minimal formaldehyde emissions for indoor air quality. Fast-setting formulations improve production throughput while maintaining assembly strength requirements.

Transportation, Healthcare, Electrical and Electronics, and other end-users represent specialized market segments with specific adhesive performance requirements. Automotive applications utilize structural bonding for lightweighting initiatives and interior assembly. Healthcare products require biocompatible adhesives for medical device manufacturing. Electronics assembly demands precision dispensing with controlled curing characteristics.

Key Market Segments

By Resin Type

- Acrylics

- Polyvinyl Acetate (PVA) Emulsion

- Ethylene Vinyl Acetate (EVA) Emulsion

- Polyurethane Dispersions and CR (Chloroprene Rubber) Latex

- Others

By Substrate

- Paper and Paperboard

- Plastics and Films

- Wood and Composites

- Metals

- Glass and Ceramics

- Others

By Application

- Flexible Packaging

- Tapes and Labels

- Paper Converting and Graphic Arts

- Laminating and Filmic Structures

- Flooring and Carpeting

- Bookbinding and Publishing

- Non-woven and Hygiene Products

- Others

By End-user

- Paper, Board, and Packaging

- Building and Construction

- Woodworking and Joinery

- Transportation

- Healthcare

- Electrical and Electronics

- Others

Drivers

Increasing Adoption of Low-VOC and Environmentally Compliant Bonding Solutions Drives Market Growth

Industries worldwide transition to water-borne adhesives to meet stringent environmental regulations limiting volatile organic compound emissions. Manufacturers replace solvent-based formulations with aqueous systems that reduce workplace exposure risks and improve air quality. Consequently, regulatory compliance drives adoption across packaging, construction, and automotive sectors seeking sustainable manufacturing practices.

- Germany’s exports of adhesive products reached $610,305.36 thousand and 36,215,200 kilograms in 2024. This substantial export volume demonstrates European leadership in environmentally compliant adhesive production and global market supply.

Consumer brands increasingly demand eco-friendly packaging solutions that align with corporate sustainability commitments and stakeholder expectations. Water-based adhesives enable recyclable packaging structures without contaminating waste streams or compromising product protection. Therefore, brand owners specify aqueous bonding technologies to enhance environmental credentials and meet consumer preferences for sustainable products.

Restraints

Limited Performance Efficiency in High-Temperature and High-Moisture Environments Restricts Market Expansion

Water-borne adhesives demonstrate reduced bonding strength under elevated temperature conditions compared to solvent-based alternatives in industrial applications. Thermal stability limitations restrict adoption for automotive under-hood components and high-temperature assembly operations. Moreover, aqueous formulations require extended drying times that reduce production efficiency across manufacturing processes.

Moisture sensitivity creates application challenges for outdoor construction and marine environments requiring permanent water resistance. Water-based systems may experience bond degradation when exposed to sustained humidity or direct water contact. Therefore, manufacturers hesitate to adopt aqueous adhesives for critical structural bonding applications without performance validation.

Raw material price volatility significantly impacts production cost structures and profit margins throughout the adhesive supply chain. Acrylic monomers, vinyl acetate, and specialty additives experience price fluctuations linked to petroleum feedstock costs. Consequently, adhesive producers face margin pressure when unable to pass increased costs to price-sensitive end-users.

Growth Factors

Technological Advancements and Sustainable Application Expansion Accelerate Market Development

Woodworking and furniture manufacturing industries increasingly adopt water-borne adhesives to eliminate formaldehyde emissions and improve workplace safety. These applications benefit from fast-setting formulations that maintain production throughput while meeting environmental compliance requirements. Moreover, sustainable wood bonding solutions enable certification under green building and indoor air quality standards.

- European Union exports of adhesive products totaled $609,911.30 thousand and 43,676,500 kilograms in 2024. This robust export performance reflects European innovation leadership and market position in sustainable adhesive technologies. Additionally, EU manufacturers benefit from regional environmental regulations driving domestic and international demand.

Electric vehicle manufacturing creates emerging opportunities for specialized water-borne adhesives in battery assembly and component bonding applications. Automotive lightweighting initiatives require structural adhesives that reduce vehicle weight while maintaining safety performance. Therefore, adhesive manufacturers develop high-strength aqueous formulations specifically engineered for electric vehicle production requirements.

Emerging Trends

Bio-based Formulations and Strategic Industry Partnerships Reshape Market Landscape

Manufacturers develop bio-based and renewable polymer-based water-borne adhesive formulations using plant-derived raw materials and sustainable chemistry. These innovations reduce petroleum dependence while maintaining industrial performance characteristics across diverse applications. Moreover, bio-attributed resins enable carbon footprint reduction throughout product life cycles and supply chains.

- The United States exports of adhesive products reached $382,069.37 thousand and 33,089,300 kilograms in 2024. This export volume demonstrates North American competitiveness in specialty adhesive technologies and global market participation. Additionally, US manufacturers focus on high-performance formulations for demanding industrial applications.

Strategic collaborations between adhesive manufacturers and packaging companies accelerate application-specific product development and market penetration. Joint development programs optimize bonding solutions for emerging packaging formats and substrate combinations. Therefore, partnerships enable faster commercialization of innovative adhesive technologies that address evolving customer requirements across industries.

Regional Analysis

Asia Pacific Dominates the Water-borne Adhesives Market with a Market Share of 43.1%, Valued at USD 7.6 Billion

Asia Pacific commands market leadership driven by extensive manufacturing activity across the packaging, construction, and electronics industries. The region benefits from rapid industrialization, urbanization, and growing middle-class consumer spending patterns. China, India, and Southeast Asian countries drive adhesive consumption through expanding production capacity and infrastructure development.

North America demonstrates strong market growth supported by stringent environmental regulations and sustainability initiatives across industries. The region leads in bio-based adhesive development and green building practices requiring low-VOC bonding solutions. Moreover, e-commerce expansion and flexible packaging growth drive adhesive consumption in packaging converting operations throughout the United States and Canada.

Europe maintains a significant market presence through innovation leadership and environmental compliance enforcement, driving water-based adhesive adoption. The region implements strict VOC emission limits and chemical safety regulations, promoting aqueous bonding technologies. Therefore, European manufacturers focus on high-performance formulations for automotive, construction, and specialty industrial applications across developed economies.

Latin America exhibits moderate growth driven by construction activity expansion and packaging industry development in Brazil and Mexico. The region gradually adopts environmental standards encouraging water-based adhesive usage across manufacturing sectors. However, price sensitivity and economic volatility influence adoption rates compared to more developed markets.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

3M maintains global leadership in adhesive technologies through extensive research and development capabilities across diverse industrial applications. The company leverages proprietary polymer chemistry and application expertise to serve packaging, automotive, and construction markets worldwide. Moreover, 3M’s broad product portfolio includes pressure-sensitive adhesives, structural bonding solutions, and specialty formulations.

Arkema focuses on sustainable adhesive solutions through acrylic resin manufacturing and bio-based polymer development initiatives globally. The company operates integrated production facilities supplying water-borne dispersions for coating and adhesive applications across industries. Arkema’s sustainability certifications and renewable chemistry expertise differentiate its market position in environmentally compliant bonding technologies.

Ashland delivers specialty chemical solutions, including water-borne adhesive formulations for packaging, construction, and industrial assembly applications. The company provides technical support and customized product development services to meet customer-specific performance requirements. Ashland’s focus on sustainable chemistry and regulatory compliance supports adoption across environmentally conscious market segments.

Avery Dennison Corporation specializes in pressure-sensitive adhesive technologies serving labeling, graphics, and packaging markets worldwide. The company integrates materials science expertise with converting capabilities to deliver comprehensive adhesive solutions. Avery Dennison’s sustainability initiatives and innovation programs address evolving market requirements for recyclable and renewable materials.

Top Key Players in the Market

- 3M

- Arkema

- Ashland

- Avery Dennison Corporation

- Benson Polymers Pvt Ltd.

- DIC CORPORATION

- Dow

- Dymax

- Evonik Industries AG

- H.B. Fuller Company

Recent Developments

- In 2025, Arkema will focus on sustainability certifications for its waterborne resins, which are key components in waterborne adhesives and coatings. Arkema obtained mass balance ISCC PLUS certification for its waterborne acrylic resins manufacturing facility in St. Charles, Louisiana. This enables the production of bio-attributed resins with reduced environmental impact.

- In 2025, Avery Dennison Corporation will unveil an industry-first RFID label compatible with PET recycling streams. Opening its first India-based RFID production facility. The company’s recent announcements focus on RFID label technologies and sustainability in labeling.

Report Scope

Report Features Description Market Value (2024) USD 22.6 Billion Forecast Revenue (2034) USD 39.7 Billion CAGR (2025-2034) 5.8% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Resin Type (Acrylics, Polyvinyl Acetate (PVA) Emulsion, Ethylene Vinyl Acetate (EVA) Emulsion, Polyurethane Dispersions and CR (Chloroprene Rubber) Latex, Others), By Substrate (Paper and Paperboard, Plastics and Films, Wood and Composites, Metals, Glass and Ceramics, Others), By Application (Flexible Packaging, Tapes and Labels, Paper Converting and Graphic Arts, Laminating and Filmic Structures, Flooring and Carpeting, Bookbinding and Publishing, Non-woven and Hygiene Products, Others), By End-user (Paper, Board, and Packaging, Building and Construction, Woodworking and Joinery, Transportation, Healthcare, Electrical and Electronics, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape 3M, Arkema, Ashland, Avery Dennison Corporation, Benson Polymers Pvt Ltd., DIC CORPORATION, Dow, Dymax, Evonik Industries AG, H.B. Fuller Company Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Water-borne Adhesives MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample

Water-borne Adhesives MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- 3M

- Arkema

- Ashland

- Avery Dennison Corporation

- Benson Polymers Pvt Ltd.

- DIC CORPORATION

- Dow

- Dymax

- Evonik Industries AG

- H.B. Fuller Company

Our Clients

- 177959

- February 2026