Global Veterinary Biopsy Needles Market By Product (Aspiration Biopsy Needles, Core Biopsy Needles, Vacuum-Assisted Biopsy Needles, Bone Biopsy Needles, Tissue Biopsy Needles and Others), By Animal Type (Companion Animals, Livestock Animals and Others), By Application (Tumor Diagnosis, Infectious Disease Diagnosis, Inflammatory Disease Diagnosis, Diagnostic, Therapeutic and Research), By End-User (Veterinary Hospitals, Veterinary Clinics, Research Institutes and Others), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 181365

- Number of Pages: 304

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

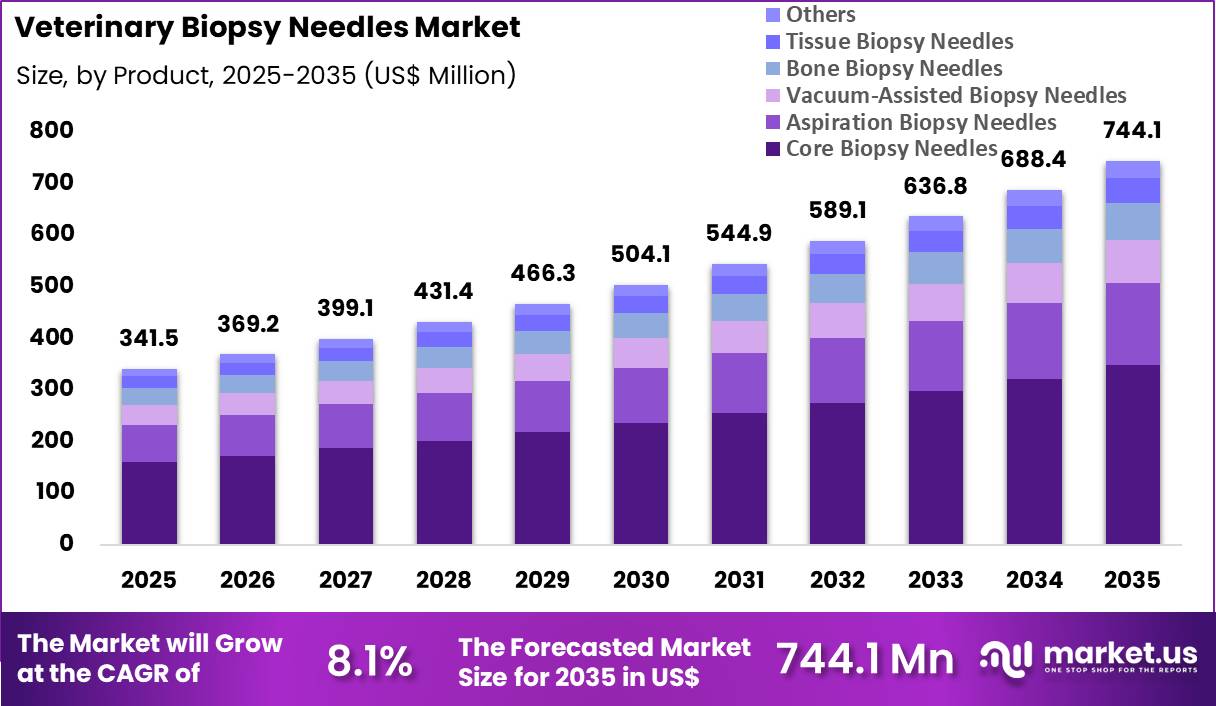

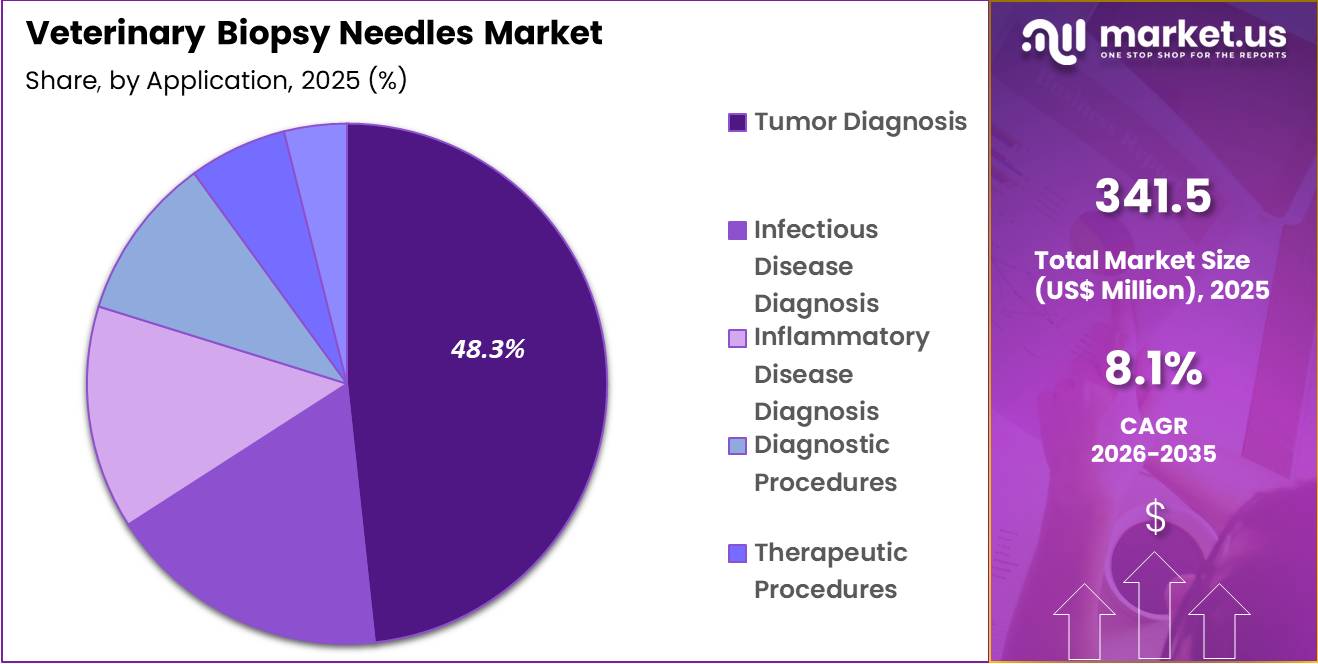

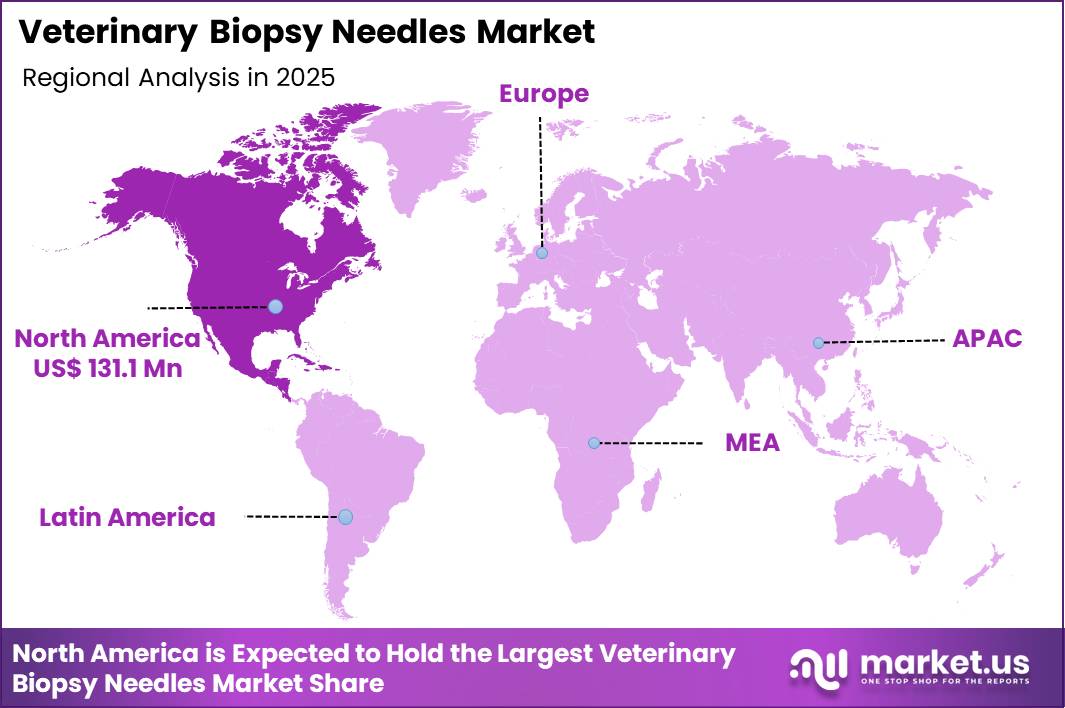

The Global Veterinary Biopsy Needles Market size is expected to be worth around US$ 744.1 Million by 2035 from US$ 341.5 Million in 2025, growing at a CAGR of 8.1% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 38.4% share with a revenue of US$ 131.1 Million.

Increasing demand for accurate, minimally invasive diagnostics in veterinary medicine accelerates the Veterinary Biopsy Needles market as veterinarians require specialized tools that deliver reliable tissue samples with reduced risk to animal patients.

Small animal practitioners increasingly perform ultrasound-guided fine-needle aspiration biopsies on lymph nodes and abdominal masses in dogs and cats, obtaining cytologic material to differentiate inflammatory, infectious, or neoplastic processes without open surgery.

These needles support core biopsy procedures in feline hepatic and splenic lesions, yielding histologic samples essential for confirming lymphoma, hepatocellular carcinoma, or inflammatory disease in companion animals. Equine veterinarians apply larger-gauge biopsy needles to obtain liver and muscle tissue in cases of suspected equine motor neuron disease or polysaccharide storage myopathy, providing definitive diagnosis to guide supportive care and prognosis discussions.

In exotic animal practice, veterinarians utilize fine-needle aspiration on reptilian and avian masses to identify granulomas, abscesses, or neoplasms, often avoiding exploratory surgery in patients with high anesthetic risk. Large animal clinicians employ biopsy needles for percutaneous liver sampling in cattle with suspected hepatic lipidosis or copper toxicity, enabling rapid identification of metabolic disorders and targeted nutritional interventions.

Manufacturers pursue opportunities to develop automatic, reusable biopsy systems that improve sample consistency and operator safety, expanding applications in high-volume small animal hospitals where frequent biopsies demand efficiency and reduced hand fatigue. Developers advance ergonomic, lightweight designs with adjustable penetration depths, broadening utility in diverse companion animal sizes from toy breeds to large dogs requiring precise organ sampling.

These innovations facilitate integration with ultrasound and endoscopic guidance, enhancing diagnostic yield in thoracic and abdominal procedures. Opportunities emerge in single-use, sterile needle kits with safety features that minimize needlestick risks for veterinary staff. Companies invest in high-quality cutting-edge needles that preserve tissue architecture for accurate histopathology in oncology and dermatologic cases.

In January 2026, Sterylab S.r.l. officially launched the Pet-Gun, an automatic, reusable biopsy system designed for veterinary use. According to the product launch details, the system features an ultra-lightweight firing mechanism and a 15mm/22mm penetration depth setting, allowing for precise sampling of internal organs in varying sizes of companion animals.

Recent trends emphasize automated mechanisms, ultrasound compatibility, and safety enhancements, positioning the market for growth in efficient, low-risk diagnostic sampling across companion, equine, and exotic animal practice.

Key Takeaways

- In 2025, the market generated a revenue of US$ 341.5 Million, with a CAGR of 8.1%, and is expected to reach US$ 744.1 Million by the year 2035.

- The product segment is divided into aspiration biopsy needles, core biopsy needles, vacuum-assisted biopsy needles, bone biopsy needles, tissue biopsy needles and others, with core biopsy needles taking the lead with a market share of 46.8%.

- Considering animal type, the market is divided into companion animals, livestock animals and others. Among these, companion animals held a significant share of 67.2%.

- Furthermore, concerning the application segment, the market is segregated into tumor diagnosis, infectious disease diagnosis, inflammatory disease diagnosis, diagnostic, therapeutic and research. The tumor diagnosis sector stands out as the dominant player, holding the largest revenue share of 48.3% in the market.

- The end-user segment is segregated into veterinary hospitals, veterinary clinics, research institutes and others, with the veterinary hospitals segment leading the market, holding a revenue share of 56.0%.

- North America led the market by securing a market share of 38.4%.

Product Analysis

Core biopsy needles accounted for 46.8% of growth within product and dominate the veterinary biopsy needles market due to their ability to obtain intact tissue samples that allow accurate histopathological evaluation. Veterinarians increasingly rely on core biopsy techniques because these devices collect larger tissue samples compared with aspiration needles.

Larger samples improve diagnostic reliability during tumor assessment and organ disease evaluation. Companion animal oncology continues to expand as pets live longer and receive more advanced veterinary care. The American Veterinary Medical Association reports that pet ownership continues to increase across households, which expands the population requiring veterinary diagnostic procedures.

Veterinarians frequently select core biopsy needles when diagnosing tumors, liver diseases, and kidney disorders. The segment is expected to strengthen as veterinary diagnostic practices increasingly adopt advanced pathology testing and precision diagnostic methods.

Animal Type Analysis

Companion animals accounted for 67.2% of growth within animal type and dominate the veterinary biopsy needles market due to the rapidly expanding global pet population and rising veterinary healthcare spending. Dogs and cats frequently undergo diagnostic procedures to identify tumors, infections, and inflammatory diseases.

Pet owners increasingly seek early diagnosis and advanced treatment options for their animals. According to the American Pet Products Association, pet industry spending in the United States exceeded $136 billion in recent years, reflecting strong demand for veterinary services and diagnostics.

Veterinarians perform biopsy procedures to guide treatment planning and confirm disease progression in companion animals. The segment is projected to expand as pets live longer and receive more complex medical care. Growing awareness of animal oncology and preventive veterinary care further supports diagnostic demand in this segment.

Application Analysis

Tumor diagnosis accounted for 48.3% of growth within application and dominate the veterinary biopsy needles market due to the increasing incidence of cancer among companion animals. Veterinary oncologists rely on biopsy procedures to identify tumor types, determine malignancy, and guide treatment decisions.

Accurate tissue sampling remains essential for pathological confirmation of cancer. Veterinary medical literature indicates that cancer represents one of the leading causes of death in older dogs and cats. This rising disease burden increases the need for diagnostic biopsy procedures.

Veterinary hospitals frequently perform biopsies during imaging-guided diagnostic workflows that evaluate suspicious masses or organ abnormalities. The segment is anticipated to grow as veterinary oncology services expand and diagnostic imaging technologies improve tumor detection. Increasing availability of specialized veterinary pathology laboratories further strengthens biopsy utilization for cancer diagnosis.

End-User Analysis

Veterinary hospitals accounted for 56.0% of growth within end users and dominate the veterinary biopsy needles market due to their advanced diagnostic infrastructure and specialized veterinary teams. Hospitals provide imaging technologies such as ultrasound and CT scanning that support accurate biopsy procedures.

These facilities also maintain surgical capabilities and pathology partnerships that enable comprehensive diagnostic workflows. Veterinary hospitals handle complex disease cases that require advanced testing and tissue analysis. The growing demand for specialized veterinary treatments encourages pet owners to seek care at hospital-based facilities.

Hospitals also treat large numbers of referral cases from smaller clinics. The segment is expected to strengthen as veterinary hospitals expand oncology, internal medicine, and diagnostic imaging services that rely heavily on biopsy-based testing.

Key Market Segments

By Product

- Aspiration Biopsy Needles

- Core Biopsy Needles

- Vacuum-Assisted Biopsy Needles

- Bone Biopsy Needles

- Tissue Biopsy Needles

- Others

By Animal Type

- Companion Animals

- Livestock Animals

- Others

By Application

- Tumor Diagnosis

- Infectious Disease Diagnosis

- Inflammatory Disease Diagnosis

- Diagnostic

- Therapeutic

- Research

By End-User

- Veterinary Hospitals

- Veterinary Clinics

- Research Institutes

- Others

Drivers

Rising companion animal diagnostic procedures are driving the market.

Veterinary practices have increased the frequency of biopsy sampling in companion animals due to growing awareness of neoplastic and inflammatory conditions. The procedure supports definitive histopathological diagnosis for masses detected during routine examinations or imaging. Demand for precise needle designs has intensified to minimize tissue trauma and improve sample yield.

Practitioners favor automated or semi-automated biopsy needles for consistent core acquisition in superficial and deep lesions. The driver correlates with elevated pet ownership and willingness to pursue advanced diagnostics. Facilities report higher utilization in oncology and dermatology cases requiring tissue confirmation.

Enhanced needle visibility under ultrasound guidance facilitates accurate targeting. The trend supports integration with in-house pathology workflows for rapid preliminary assessments. Sustained procedural volumes maintain steady procurement of specialized veterinary biopsy instruments. This factor underpins consistent market demand across companion animal segments.

Restraints

Limited reimbursement for veterinary biopsy procedures is restraining the market.

Pet insurance policies frequently exclude or provide partial coverage for diagnostic biopsies, placing financial burden on owners. The absence of standardized veterinary-specific reimbursement codes contributes to inconsistent payer support. Owners often defer or decline procedures due to out-of-pocket expenses exceeding several hundred dollars.

The restraint moderates procedure volumes in general practice settings. Facilities prioritize less costly diagnostic alternatives such as fine-needle aspiration when reimbursement remains uncertain. The factor influences purchasing decisions toward more economical needle options. Manufacturers encounter slower adoption of premium biopsy systems in cost-sensitive markets.

The dynamic limits scalability of advanced biopsy technologies in routine care. Providers face challenges justifying investment in specialized instrumentation without reliable financial recovery. This constraint persists in tempering broader market penetration.

Opportunities

Development of ultrasound-guided veterinary biopsy protocols is creating growth opportunities.

Standardized ultrasound-guided techniques enable precise needle placement in abdominal and thoracic lesions with reduced complications. These protocols expand indications for biopsy in organs previously challenging to access safely. Opportunities arise for training programs that certify practitioners in guided biopsy methods.

The framework supports adoption of coaxial needle systems for multiple sampling passes. Veterinary specialists gain capacity to perform minimally invasive diagnostics in outpatient settings. Enhanced procedural safety improves case acceptance among cautious owners.

The development facilitates collaboration between general practitioners and referral centers. Such protocols promote utilization of advanced imaging-compatible needles. The opportunity fosters differentiation through improved diagnostic yield and patient outcomes. This advancement positions participants for expansion in image-guided veterinary interventions.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions influence the veterinary biopsy needles market through clinic investment levels, livestock health spending, and companion animal diagnostics demand. Inflation increases costs for stainless steel, precision machining, sterilization, and packaging, which raises manufacturing expenses for device suppliers.

Higher interest rates limit capital spending by veterinary hospitals and diagnostic laboratories planning equipment upgrades. Geopolitical tensions disrupt global sourcing of medical-grade metals, needle components, and specialized coatings, creating supply uncertainty for manufacturers.

Current US tariffs on imported medical device parts and raw materials increase production costs and tighten margins for distributors serving veterinary clinics. These pressures can slow purchasing decisions among smaller veterinary practices and regional diagnostic centers.

At the same time, manufacturers strengthen domestic metal sourcing and expand regional production capabilities to improve supply reliability. Rising focus on early disease detection and advanced veterinary diagnostics continues to support steady and confident market growth.

Latest Trends

Introduction of specialized coaxial veterinary biopsy needle systems is driving the market.

A manufacturer launched an updated coaxial biopsy needle line in 2024 featuring enhanced echogenic markings for improved ultrasound visibility. The system incorporates a removable inner stylet and outer cannula designed specifically for veterinary soft tissue applications. Clearance and market introduction targeted improved core quality in small animal patients.

The development addresses clinician feedback on needle stability during multi-pass sampling. Practitioners benefit from reduced tissue drag and consistent specimen integrity. The 2024-2025 availability aligns with increasing demand for ultrasound-assisted procedures. Facilities report potential decreases in procedure time and repeat sampling needs.

The innovation supports compatibility with portable veterinary ultrasound units. Early clinical feedback highlights superior performance in hepatic and splenic biopsies. Overall, this advancement elevates technical capabilities in veterinary diagnostic sampling.

Regional Analysis

North America is leading the Veterinary Biopsy Needles Market

North America accounted for 38.4% of the veterinary biopsy needles market in 2025 as veterinary hospitals and specialty animal clinics expanded diagnostic services for early detection of cancer and chronic diseases in animals. Companion animal healthcare has grown significantly as pet owners increasingly pursue advanced diagnostics and specialized veterinary treatment.

According to the American Veterinary Medical Association, U.S. pet owners spent about USD 38.3 billion on veterinary care and products in 2023, reflecting rising investment in animal health services that support diagnostic procedures such as tissue biopsies. Veterinary oncologists and diagnostic specialists frequently use biopsy needles during ultrasound-guided and image-assisted procedures to confirm tumors, infections, and organ disorders.

Expansion of veterinary specialty hospitals and referral centers across the United States and Canada has strengthened access to advanced imaging and pathology services. Veterinary universities and research institutes are also increasing training programs focused on oncology and diagnostic pathology in animals.

Manufacturers are developing improved biopsy needle designs that enhance sampling precision while minimizing trauma to animal tissues. Growing awareness among pet owners about early disease diagnosis has encouraged veterinarians to recommend biopsy procedures more frequently. These factors collectively supported the steady growth of veterinary diagnostic sampling technologies across North America in 2025.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to witness notable expansion during the forecast period as veterinary healthcare services strengthen across emerging economies and demand for advanced diagnostics increases. Countries such as China, India, Japan, and Australia are experiencing rapid growth in pet ownership and veterinary infrastructure.

According to the Food and Agriculture Organization, the global livestock population includes billions of animals used in agriculture, with a substantial share located in Asian countries that require veterinary health monitoring and disease diagnosis. Veterinary clinics and animal hospitals across the region are expanding diagnostic capabilities to detect tumors, infectio

ns, and metabolic disorders in both companion animals and livestock. Governments are strengthening veterinary healthcare systems and animal disease surveillance programs to improve livestock productivity and food safety. Veterinary education institutions are expanding training in pathology, diagnostic imaging, and animal oncology.

Private veterinary hospital chains are introducing advanced imaging technologies that enable precise needle-guided tissue sampling. Regional medical device suppliers are developing affordable biopsy instruments tailored for veterinary applications. These developments are expected to drive continued growth of veterinary diagnostic sampling technologies across Asia Pacific in the coming years.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

Key participants in the Veterinary Biopsy Needles Market strengthen growth through continuous development of precision biopsy instruments, expansion of veterinary diagnostic services, and strategic collaborations with animal hospitals and specialty veterinary clinics. Companies focus on improving needle design, ergonomic handling, and imaging compatibility to support accurate tissue sampling in companion and livestock animals.

They also expand distribution networks and invest in veterinary education programs that help clinicians adopt advanced diagnostic procedures. Argon Medical Devices represents a notable participant in the Veterinary Biopsy Needles Market and operates as a U.S.-based medical device manufacturer that develops biopsy instruments, interventional radiology products, and minimally invasive procedural tools used across healthcare and veterinary settings.

The company emphasizes product reliability, clinical training, and innovation to support precise diagnostic interventions. Industry competitors continue to pursue new product introductions, expanded veterinary partnerships, and technological refinement to strengthen adoption of modern biopsy solutions across veterinary healthcare systems.

Top Key Players

- Medtronic plc

- Becton, Dickinson and Company (BD)

- Jorgensen Laboratories

- Argon Medical Devices, Inc.

- Olympus Corporation

- Jrgen Kruuse A/S

- Surgivet

- Vygon Vet

- B. Braun Melsungen AG

- Cook Group

- Merit Medical Systems

- KARL STORZ

Recent Developments

- In February 2025, Argon Medical Devices expanded its BioPince Ultra Full-Core biopsy instrument line to include 20G and 18G variants specifically validated for veterinary oncology. This development allows veterinarians to capture larger, high-quality tissue cores from small animal patients with significantly less procedural trauma than traditional fine-needle aspiration.

- In June 2025, Mermaid Medical Group entered into a strategic supply agreement with several US-based specialist veterinary networks to distribute its “coaxial” biopsy needle systems. These needles enable clinicians to perform multiple samplings through a single puncture, which has become a preferred method for diagnosing complex hepatic and renal conditions in feline and canine patients.

Report Scope

Report Features Description Market Value (2025) US$ 341.5 Million Forecast Revenue (2035) US$ 744.1 Million CAGR (2026-2035) 8.1% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product (Aspiration Biopsy Needles, Core Biopsy Needles, Vacuum-Assisted Biopsy Needles, Bone Biopsy Needles, Tissue Biopsy Needles and Others), By Animal Type (Companion Animals, Livestock Animals and Others), By Application (Tumor Diagnosis, Infectious Disease Diagnosis, Inflammatory Disease Diagnosis, Diagnostic, Therapeutic and Research), By End-User (Veterinary Hospitals, Veterinary Clinics, Research Institutes and Others) Regional Analysis North America – The US, Canada; Europe – Germany, France, The U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America Competitive Landscape Medtronic plc, Becton, Dickinson and Company (BD), Jorgensen Laboratories, Argon Medical Devices, Inc., Olympus Corporation, Jrgen Kruuse A/S, Surgivet, Vygon Vet, B. Braun Melsungen AG, Cook Group, Merit Medical Systems, KARL STORZ. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Veterinary Biopsy Needles MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Veterinary Biopsy Needles MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Medtronic plc

- Becton, Dickinson and Company (BD)

- Jorgensen Laboratories

- Argon Medical Devices, Inc.

- Olympus Corporation

- Jrgen Kruuse A/S

- Surgivet

- Vygon Vet

- B. Braun Melsungen AG

- Cook Group

- Merit Medical Systems

- KARL STORZ

Our Clients

- 181365

- March 2026