Quick Navigation

- Report Overview

- Key Takeaways

- Analyst’s Viewpoint

- Growing Impact of AI

- US Vehicle Insurance Market

- Coverage Analysis

- Application Analysis

- Distribution Channel Analysis

- Vehicle Type Analysis

- Key Market Segments

- Driver

- Restraint

- Opportunity

- Challenge

- Growth Factors

- Emerging Trends

- Business Benefits

- Key Regions and Countries

- Key Player Analysis

- Recent Developments

- Report Scope

Report Overview

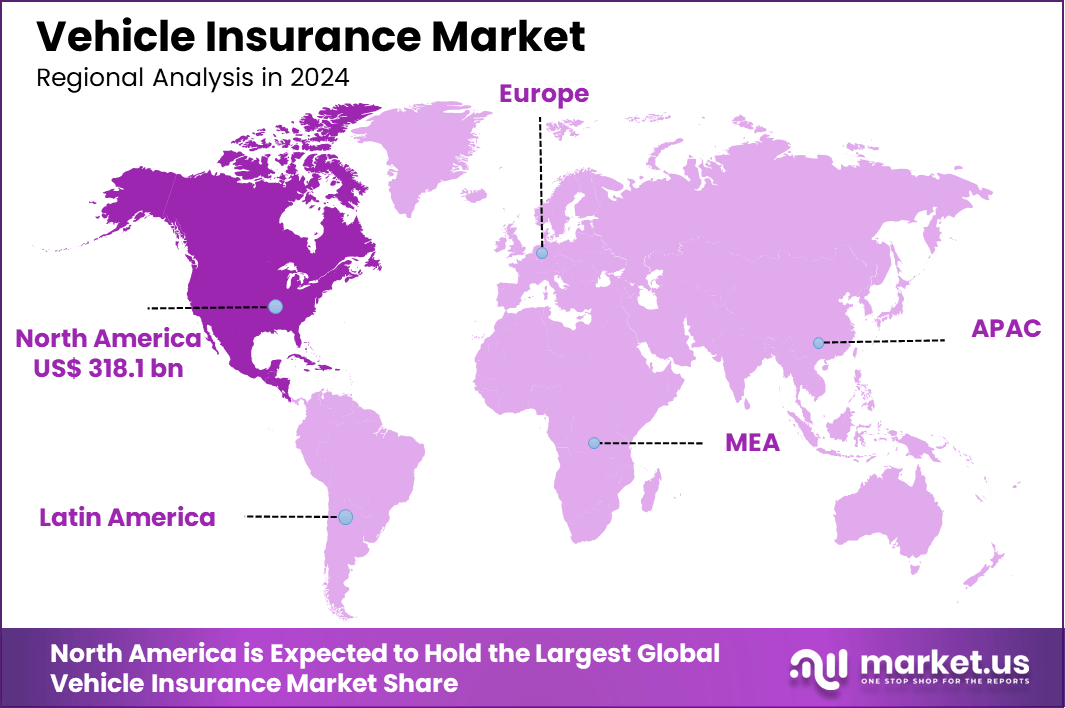

The Global Vehicle Insurance Market size is expected to be worth around USD 1,949.9 Billion By 2034, from USD 911.6 billion in 2024, growing at a CAGR of 7.9% during the forecast period from 2025 to 2034. In 2024, North America held a dominant market position, capturing more than a 34.9% share, holding USD 318.14 Billion revenue.

Vehicle insurance, also known as auto insurance, is a financial protection mechanism for vehicle owners. It covers losses due to accidents, theft, and other liabilities as stipulated in the insurance policy. The policy typically includes coverage for damage to the vehicle itself (comprehensive and collision coverages) and liability insurance for bodily injuries or property damage caused by the insured.

The vehicle insurance market’s growth is primarily fueled by the increasing adoption of personal and commercial vehicles globally. The expansion of the middle class, along with rising disposable incomes in emerging markets, contributes significantly to this trend. Additionally, the surge in economic activities across both developed and developing nations enhances the demand for commercial vehicles, further driving the need for vehicle insurance.

Technological advancements are reshaping the vehicle insurance market. Innovations such as telematics, big data analytics, and artificial intelligence are being leveraged to offer usage-based and personalized insurance models. These technologies help in assessing risks more accurately and processing claims more efficiently, thereby benefiting both insurers and policyholders.

The adoption of these technologies in the vehicle insurance sector is primarily due to their ability to reduce operational costs, enhance customer service, and offer competitive pricing. For example, AI-driven tools enable better risk assessment and quicker claims processing, which are crucial for maintaining competitiveness in the market.

According to the latest analysis by Forbes, the national average cost of full coverage car insurance in the United States stood at $2,150 annually as of early 2024. This reflects a significant upward trend, as auto insurance costs increased by 63.8% over the ten-year period from 2014 to 2023. A clear disparity exists among providers – USAA offers the most affordable full coverage at $1,412 per year, while Mercury ranks highest at $3,233, creating a notable annual difference of $1,821.

Minimum coverage also shows wide cost variation. Rates range from $241 per year (with Erie and Mercury) to $892 (with Safe Auto), amounting to a $651 difference. The Honda CR-V and Subaru Outback emerged as the most economical models to insure among top-selling vehicles, each at $1,723 per year. In contrast, the Tesla Model Y Long Range topped the list of costliest at $3,128, indicating a gap of $1,405.

When assessed by vehicle type, minivans had the lowest average premium at $2,041, while coupes, especially two-door sports cars, averaged a substantially higher $3,894 annually. Notably, vehicles such as the Toyota Tundra Double Cab LWB, Jeep Wrangler 2dr 4WD, and Subaru Crosstrek 4WD reported the lowest collision losses, whereas high-end models like the McLaren 720S convertible and BMW M8 recorded the highest loss ratios.

The growing awareness of the benefits of vehicle insurance and the continuous evolution of consumer preferences are generating robust demand. Investment opportunities are particularly pronounced in the integration of digital technologies, which can streamline operations and improve customer engagement.

One significant market trend is the shift towards digital insurance platforms, which offer comprehensive services online. These platforms simplify the process of comparing policies, purchasing insurance, and filing claims, thereby enhancing customer convenience.

Key Takeaways

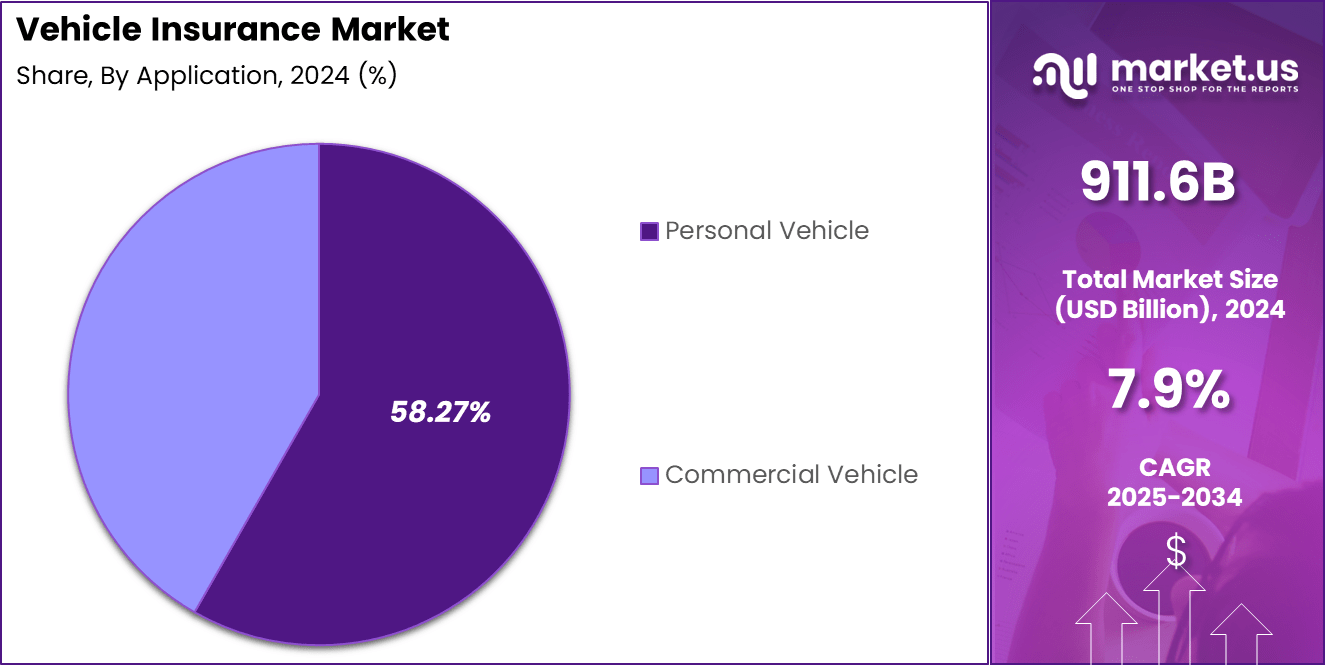

- The global vehicle insurance market is poised for substantial growth, with the market size projected to reach approximately USD 1,949.9 billion by 2034, up from USD 911.6 billion in 2024. This growth reflects a CAGR of 7.9% during the forecast period from 2025 to 2034.

- In 2024, North America emerged as the leading regional market, capturing over 34.9% of the global share, which translates to a market value of USD 318.14 billion. This dominance is largely attributed to high vehicle density, strong regulatory frameworks, and well-established insurance infrastructure.

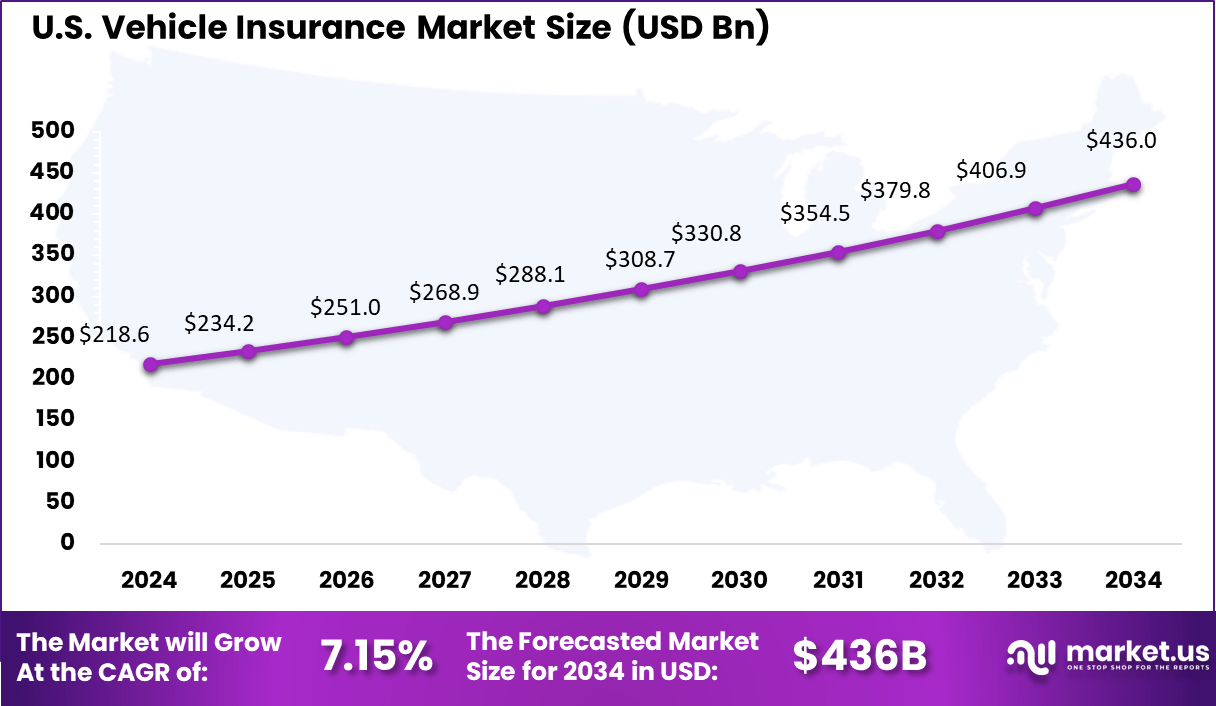

- The United States, in particular, represents a major contributor within this region. The U.S. vehicle insurance market is currently valued at USD 218.6 billion in 2024 and is expected to grow steadily to reach USD 436 billion by 2034. This projected growth represents a CAGR of 7.15% from 2025 to 2034.

- In terms of insurance types, the Third-Party Liability segment held a commanding position in 2024, accounting for over 70.1% of the total market share.

- By vehicle type, the Personal Vehicle segment led the market with a share exceeding 58.27% in 2024. Rising personal vehicle ownership, particularly in urban areas, along with the growing need for financial safety against accidents and theft, has sustained this segment’s prominence.

- Analyzing distribution channels, Insurance Agents and Brokers remained the most preferred mode in 2024, capturing a substantial share of the market.

- Additionally, the New Vehicles segment captured a significant market share in 2024. This is largely attributed to insurance requirements imposed by financing institutions and a growing preference among consumers to insure newly purchased vehicles immediately to avoid unforeseen repair and replacement costs.

Analyst’s Viewpoint

Regulatory changes, economic fluctuations, and technological innovations are among the top factors impacting the vehicle insurance market. Regulatory environments in various countries mandate basic insurance coverage, influencing market dynamics significantly.

For businesses, offering vehicle insurance can lead to diversified revenue streams, improved customer retention, and increased market penetration. The ability to bundle services and offer customized solutions also provides competitive advantages.

Innovations such as online insurance comparison tools, AI-driven risk assessment, and telematics for monitoring driving behaviors are revolutionizing the industry. These advancements facilitate more accurate pricing models and help in targeting specific customer segments.

The vehicle insurance market is highly regulated, with laws varying by region. These regulations ensure that insurance policies provide necessary protection to consumers and maintain fairness in the industry. Compliance with these regulations is crucial for insurance providers to operate successfully in different markets.

Growing Impact of AI

- Personalized Pricing Models: AI facilitates the analysis of large data sets involving driving behaviors, accident history, and vehicle usage patterns. This allows insurers to offer personalized insurance premiums, tailored to the specific risk profile of each customer. By accurately assessing risk, AI helps in pricing insurance products more fairly and competitively.

- Enhanced Claims Processing: AI significantly improves the efficiency of claims processing in vehicle insurance. Through automation and data analytics, AI can quickly assess damage, estimate repair costs, and verify claims with minimal human intervention. This not only speeds up the claims process but also reduces the potential for fraud and errors, leading to higher customer satisfaction.

- Risk Assessment and Management: AI-driven tools analyze data from various sources, including telematics devices installed in vehicles, to monitor driving patterns and detect risky behaviors. Insurers use this information to assess the likelihood of accidents and adjust policy terms accordingly. This proactive approach in risk management helps in mitigating potential losses before they occur.

- Customer Engagement and Retention: AI enhances customer engagement by providing more interactive and responsive insurance services. For example, chatbots and virtual assistants, powered by AI, offer 24/7 customer support, handle policy inquiries, and assist in policy management. This continuous engagement helps in building stronger relationships and improving customer retention rates.

- Market Expansion and New Product Development: AI enables insurers to explore new markets and develop innovative products that meet evolving customer needs. For instance, the introduction of usage-based insurance (UBI) models, like pay-as-you-drive, which relies on AI and telematics to track vehicle usage and adjust premiums accordingly.

US Vehicle Insurance Market

The US Vehicle Insurance Market is valued at approximately USD 218.6 Billion in 2024 and is predicted to increase from USD 234.2 Billion in 2025 to approximately USD 436 Billion by 2034, projected at a CAGR of 7.15% from 2025 to 2034.

In 2024, North America held a dominant market position in the vehicle insurance industry, capturing more than a 34.9% share with revenues amounting to USD 318.9 billion. This prominent standing can be attributed to several key factors that uniquely position North America at the forefront of the global vehicle insurance market.

Firstly, the high vehicle ownership rates in North American countries, particularly in the United States and Canada, drive the demand for vehicle insurance. The culture of vehicle dependency for commuting and the suburban lifestyle prevalent in this region necessitates extensive vehicle use, thereby increasing the need for insurance products.

The widespread acceptance and enforcement of vehicle insurance regulations also play a critical role. In the United States, for instance, auto insurance is mandatory in almost all states, with stringent penalties for non-compliance, ensuring that a majority of vehicle owners seek coverage.

Additionally, North America boasts a robust financial services sector with a mature insurance industry. This maturity is complemented by the presence of some of the world’s largest and most influential insurance companies, which not only serve local markets but also operate globally.

These firms are often at the cutting edge of integrating advanced technologies such as telematics, big data analytics, and artificial intelligence to enhance risk assessment, customer service, and claims processing. This technological adoption has made policies more customer-friendly and efficient, contributing to higher market penetration and customer retention rates.

Coverage Analysis

In 2024, the Third Party Liability segment held a dominant market position in the vehicle insurance industry, capturing more than a 70.1% share. This substantial market share can be attributed to several pivotal factors that underscore the segment’s central role in the vehicle insurance landscape.

Primarily, the widespread adoption of Third Party Liability insurance is driven by regulatory mandates across numerous regions, requiring vehicle owners to possess at least minimum liability coverage. This ensures that any damages inflicted by the insured vehicle on third parties, whether to property or persons, are covered, thereby mitigating financial risks for vehicle owners and protecting affected third parties.

Moreover, the preference for Third Party Liability insurance is reinforced by its relative affordability compared to more comprehensive coverage options. By focusing solely on liability, it provides essential protections without the additional premiums associated with covering damages to the insured’s own vehicle, making it a financially attractive option for many vehicle owners.

Additionally, the market’s growth is bolstered by the increasing volume of vehicles and the corresponding rise in traffic densities, which naturally heightens the risk of accidents involving third parties. The legal implications and potential financial liabilities from such incidents further accentuate the importance of this coverage. It serves as a fundamental safeguard, ensuring that individuals are not financially overwhelmed by costs potentially incurred from accidents.

Application Analysis

In 2024, the Personal Vehicle segment of the vehicle insurance market held a dominant market position, capturing more than a 58.27% share. This leading position can be attributed to several factors that underscore the robust demand and integral role of personal vehicle insurance in the market.

The primary driver for this segment’s dominance is the substantial increase in personal vehicle ownership, fueled by rising disposable incomes and a growing preference for private transportation. This trend is particularly prominent in regions with expanding middle-class populations, where personal vehicles are often seen as a necessity rather than a luxury.

Technological advancements in vehicle manufacturing, which include enhanced safety features and connected systems, have also played a significant role. While these innovations elevate the price and perceived value of personal vehicles, they simultaneously increase the complexity and cost of repairs.

Furthermore, the market for personal vehicle insurance is supported by aggressive marketing and customer acquisition strategies by major insurers, who often offer tailored insurance products that cater to diverse consumer needs. This customization can include everything from basic liability coverage to full comprehensive plans that cover a wide array of risks, thereby attracting a broader customer base.

Distribution Channel Analysis

In 2024, the Insurance Agents/Brokers segment held a dominant market position in the vehicle insurance industry, capturing a substantial share due to several pivotal factors that underscore its central role.

Primarily, this segment’s strength lies in the personalized service that agents and brokers offer, which remains highly valued by many customers, especially those who prefer a more tailored approach to selecting their insurance coverage. Agents and brokers excel in providing customized services that help clients navigate the complex landscape of vehicle insurance options to find the best fit for their specific needs.

Moreover, the expertise of insurance agents and brokers in risk assessment and their deep understanding of the insurance market play critical roles. They utilize this expertise to advise clients on the most appropriate levels of coverage and to help mitigate potential financial risks associated with owning and operating vehicles.

The segment’s growth is also supported by technological advancements that have transformed how insurance products are marketed and sold. Many agents and brokers now leverage online platforms to extend their reach and improve the efficiency of their operations.

This digital shift not only enhances their ability to serve a broader client base but also aligns with the growing consumer preference for digital interactions, which can streamline the purchasing process of vehicle insurance.

Vehicle Type Analysis

In 2024, the New Vehicles segment held a dominant market position in the vehicle insurance industry, capturing a significant market share. This dominance is largely driven by several key factors that cater to the preferences and needs of new vehicle owners.

Firstly, the attraction of new vehicles includes advanced safety features and technology which not only appeal to consumers but also to insurers. Newer vehicles often come equipped with the latest safety features and connectivity technologies, which can reduce the likelihood of accidents and thefts.

Insurance companies typically offer more favorable premiums for these vehicles because their advanced safety features pose a lower risk, which in turn, attracts a lower claim frequency. Additionally, the growth in new vehicle sales, supported by economic recovery and increasing disposable incomes, has contributed significantly to the expansion of this insurance segment.

As more consumers opt for new vehicles, the demand for corresponding insurance products naturally increases. The push towards newer, environmentally friendly vehicles like electric cars also supports growth in this segment, as these vehicles require specific insurance products that cover unique risks associated with advanced technologies.

Moreover, the insurance industry has seen a parallel growth in digital platforms that make it easier for consumers to access insurance products. These platforms not only simplify the process of comparing and purchasing insurance but also tailor products that are specific to the needs of new vehicle owners, enhancing customer satisfaction and driving further market growth.

Key Market Segments

By Coverage

- Third Party Liability

- Comprehensive

By Application

- Personal Vehicle

- Commercial Vehicle

By Distribution Channel

- Insurance Agents/Brokers

- Direct Response

- Banks

- Others

By Vehicle Type

- New Vehicles

- Used Vehicles

Driver

Digital Transformation and Regulatory Requirements

The vehicle insurance market is significantly driven by the integration of digital technologies and regulatory demands for minimum liability coverage. As insurers leverage data analytics and AI tools, they can offer more tailored products that align with consumer expectations and regulatory standards.

This technological shift not only streamlines the insurance process but also enhances customer engagement and satisfaction by providing more personalized services and efficient claim handling. Additionally, governments frequently enforce laws that require vehicle owners to maintain minimum liability coverage, ensuring that all parties are protected in the event of an accident.

Restraint

Fraud and Rising Costs

One of the primary restraints in the vehicle insurance market is the prevalence of insurance fraud, including false claims and exaggerated damages. These fraudulent activities lead to higher operational costs for insurers, as they must invest in sophisticated fraud detection technologies and processes to mitigate these risks.

Furthermore, the rising costs associated with vehicle repairs, driven by inflation and the increasing complexity of vehicle systems, also pose significant challenges. As cars become more advanced, the need for specialized repairs using original manufacturer parts increases, thereby elevating the overall cost of insurance claims.

Opportunity

Electric Vehicles and Advanced Safety Features

The surge in electric vehicle (EV) sales and the adoption of advanced safety features present substantial opportunities within the vehicle insurance market. EVs and vehicles equipped with advanced driver-assistance systems (ADAS) such as automatic braking and lane-keeping assist are seen as less risky, potentially attracting lower insurance premiums.

This shift not only opens new revenue streams for insurers but also encourages the development of innovative insurance products tailored to modern vehicles’ specific needs. Moreover, the environmental benefits and technological allure of EVs continue to capture consumer interest, promising growth in this segment of the market.

Challenge

Changing Consumer Behaviors and Economic Conditions

The vehicle insurance market faces challenges from evolving consumer behaviors and economic conditions. The recent stabilization in vehicle miles traveled post-pandemic has shifted driving patterns, affecting claim frequencies and severities.

Additionally, economic uncertainties and fluctuations in vehicle sales impact insurance shopping trends, with consumers increasingly seeking cost-effective options and personalized policies. Insurers must navigate these changes carefully, balancing rate adequacy with competitive offerings to retain customer loyalty and manage profitability in a market characterized by rapid technological advancements and shifting consumer expectations.

Growth Factors

The vehicle insurance market is experiencing significant growth, driven by several key factors. Increasing vehicle ownership worldwide, supported by rising personal income levels and economic growth, directly boosts the demand for vehicle insurance.

Furthermore, regulatory mandates requiring vehicle insurance across numerous countries solidify the market’s expansion. Technological advancements, particularly in telematics and AI, enhance risk assessment and claims management, making insurance offerings more appealing and efficient for consumers.

Emerging Trends

Emerging trends in the vehicle insurance sector focus heavily on the integration of technology. Digital insurance platforms that simplify policy management and claims processes are becoming standard. These platforms often feature digital wallets that centralize customer policies, enhancing convenience and retention.

Additionally, the adoption of electric vehicles (EVs) and autonomous vehicles is prompting insurers to develop new models that address the unique risks associated with these technologies. The push towards usage-based insurance models, where premiums are determined by actual vehicle usage and driving behavior, is also gaining traction.

Business Benefits

For businesses, offering vehicle insurance can lead to several strategic advantages. Insurance providers can diversify their product offerings and tap into new customer segments, especially as the automotive market evolves with increased sales of EVs and connected cars.

The ability to gather and analyze vast amounts of data from connected vehicles allows insurers to offer more personalized pricing and services, which can improve customer satisfaction and loyalty. Furthermore, businesses that adapt quickly to regulatory changes and technological advancements are likely to achieve a competitive edge, securing a stronger position in the market.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

The vehicle insurance market is shaped by several key players that significantly influence trends and market dynamics. These entities are typically large insurance companies that offer a range of policies covering everything from basic liability to comprehensive coverage.

Key players often engage in competitive strategies such as pricing adjustments, customer service enhancements, and the introduction of innovative features that cater to evolving consumer needs and technological advancements. The presence of these major players is crucial in maintaining a balanced competitive environment that benefits consumers.

In analyzing the vehicle insurance market, it is important to consider the contributions of each key player. These companies not only compete with one another but also play a pivotal role in setting industry standards and influencing regulatory developments.

Their strategies can include mergers and acquisitions, partnerships with automobile manufacturers, and investments in telematics and artificial intelligence to improve claim processing and risk assessment. Understanding the actions and market share of these key players helps stakeholders make informed decisions and anticipate future trends in the vehicle insurance industry.

Top Key Players in the Market

- Allstate Insurance Company

- China Pacific Insurance Co.

- Allianz

- People’s Insurance Company Of China

- State Farm Mutual

- Tokio Marine Group

- Automobile Insurance

- Geico

- Ping An Insurance (GROUP) Company Of China, Ltd.

- Admiral Group Plc

- Berkshire Hathaway Inc.

Recent Developments

- In January 2025, Allstate agreed to sell its Group Health business to Nationwide for $1.25 billion in cash. This move reflects Allstate’s focus on streamlining operations and concentrating on core insurance products.

- In December 2024, Allianz Australia acquired the general insurance business of the Royal Automobile Association of South Australia (RAA) for $642 million. This deal includes a 20-year exclusive distribution agreement for RAA’s home and motor insurance products.

- In December 2024, Bajaj Allianz General Insurance expanded its motor insurance offerings with the launch of two innovative products – Eco Assure – Repair Protection and Named Driver Cover. These solutions have been designed to provide customized protection tailored to individual driving behaviors and usage, reflecting a growing trend toward personalized insurance in India’s motor segment.

- Similarly, in August 2024, ICICI Lombard introduced the industry’s first-of-its-kind add-on, Smart Saver Plus, targeting long-standing customer concerns around repair delays and service quality. These product innovations show a clear industry shift toward fast, reliable, and customer-focused digital insurance, driven by rising consumer expectations and the need for competitive advantage.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 911.6 Bn |

| Forecast Revenue (2034) | USD 1,949.9 Bn |

| CAGR (2025-2034) | 7.9% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Coverage (Third Party Liability, Comprehensive), By Application (Personal Vehicle, Commercial Vehicle), By Distribution Channel (Insurance Agents/Brokers, Direct Response, Banks, Others), By Vehicle Type (New Vehicles, Used Vehicles) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Allstate Insurance Company, China Pacific Insurance Co., Allianz, People’s Insurance Company Of China, State Farm Mutual, Tokio Marine Group, Automobile Insurance, Geico, Ping An Insurance (GROUP) Company Of China, Ltd., Admiral Group Plc, Berkshire Hathaway Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |