Quick Navigation

Report Overview

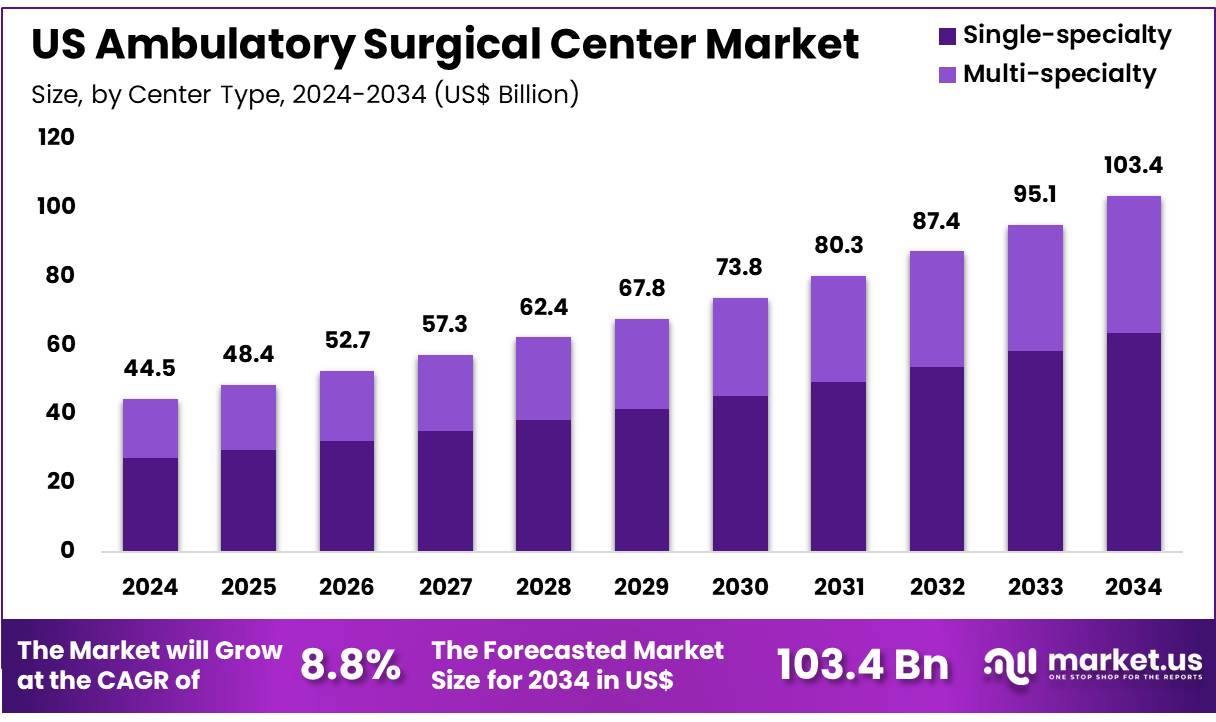

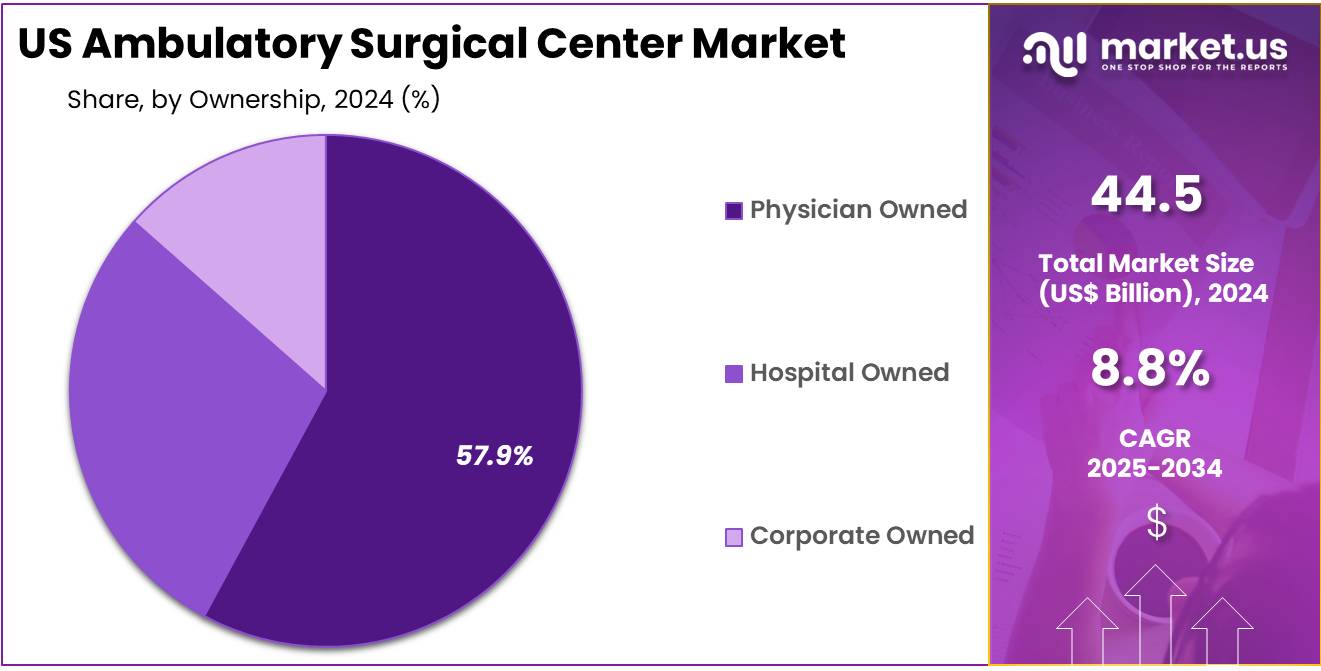

The US Ambulatory Surgical Center Market size is expected to be worth around US$ 103.4 Billion by 2034 from US$ 44.5 Billion in 2024, growing at a CAGR of 8.8% during the forecast period 2025 to 2034.

Rising demand for outpatient procedures and cost-effective healthcare solutions is driving the growth of the US ambulatory surgical center (ASC) market. ASCs provide a wide range of medical services, including orthopedic, ophthalmic, gastrointestinal, and plastic surgeries, offering patients a more convenient and affordable alternative to traditional hospital-based care. The increasing focus on minimally invasive procedures, coupled with advancements in surgical technology, contributes to the rising preference for outpatient surgeries.

As patients seek quicker recovery times and lower healthcare costs, ASCs offer attractive solutions that improve overall healthcare efficiency. In April 2023, Koninklijke Philips N.V. partnered with Northwell Health to launch a seven-year collaboration focused on standardizing patient monitoring systems, enhancing patient outcomes, and fostering data innovation. This collaboration reflects the growing emphasis on improving operational efficiencies and patient care within healthcare settings, including ASCs.

Additionally, the increasing adoption of advanced medical equipment and digital health technologies in ASCs is enhancing surgical precision, improving patient safety, and optimizing post-surgery recovery. The shift towards value-based care models, along with favorable reimbursement policies for outpatient procedures, presents significant opportunities for the expansion of ASCs.

As healthcare providers and patients alike continue to recognize the benefits of outpatient surgeries, the ASC market will likely experience continued growth driven by technological innovation, improved operational models, and rising demand for cost-effective healthcare solutions.

Key Takeaways

- In 2024, the market for US ambulatory surgical center generated a revenue of US$ 44.5 billion, with a CAGR of 8.8%, and is expected to reach US$ 103.4 billion by the year 2033.

- The center type segment is divided into single-specialty and multi-specialty, with single-specialty taking the lead in 2024 with a market share of 61.4%.

- Considering ownership, the market is divided into physician owned, hospital owned, and corporate owned. Among these, physician owned held a significant share of 57.9%.

- Furthermore, concerning the speciality segment, the market is segregated into orthopedics, pain management/spinal injections, gastroenterology, ophthalmology, and others. The orthopedics sector stands out as the dominant player, holding the largest revenue share of 45.2% in the US ambulatory surgical center market.

Center Type Analysis

The single-specialty segment led in 2024, claiming a market share of 61.4% owing to the increasing preference for specialized, cost-effective care in outpatient settings. Patients are increasingly seeking dedicated centers that focus on specific procedures, such as orthopedic surgeries or eye care, as these centers provide expertise and high-quality outcomes.

The rise in demand for minimally invasive surgeries, which often require specialized expertise, is anticipated to drive growth in single-specialty centers. Furthermore, as healthcare providers continue to focus on improving operational efficiencies and reducing costs, single-specialty centers are projected to thrive by offering focused, streamlined services.

The growing trend of patients opting for outpatient procedures rather than hospital-based surgeries is likely to contribute to the expansion of this segment, particularly as patients prioritize convenience and quicker recovery times.

Ownership Analysis

The physician owned held a significant share of 57.9% as more physicians seek to gain greater control over their practices and revenue streams. Physician-owned centers offer benefits such as flexibility in scheduling, personalized patient care, and a more direct decision-making process, which is expected to attract more healthcare professionals.

Additionally, physician ownership allows for a more efficient management structure, reducing overhead costs and enhancing profitability. The rise in demand for outpatient surgeries, particularly in specialties like orthopedics and ophthalmology, is likely to further boost this segment. As physicians seek to maintain control over their clinical and financial operations, the physician-owned segment is projected to experience sustained growth, supported by a favorable regulatory environment and patient satisfaction with high-quality, personalized care.

Specialty Analysis

The orthopedics segment had a tremendous growth rate, with a revenue share of 45.2% owing to the increasing demand for outpatient orthopedic procedures, such as joint replacements, arthroscopies, and spine surgeries. The rise in musculoskeletal disorders, particularly among aging populations, is expected to drive more patients to seek outpatient surgical options, which provide quicker recovery times and lower costs compared to hospital settings.

Additionally, advancements in minimally invasive techniques and technology are anticipated to make orthopedic surgeries more efficient and less invasive, encouraging more patients to opt for ambulatory settings. As healthcare providers continue to focus on providing cost-effective and high-quality care, the orthopedic specialty segment is likely to experience significant growth, driven by both the aging population and the increasing preference for outpatient surgical options.

Key Market Segments

Center Type

- Single-specialty

- Multi-specialty

Ownership

- Physician Owned

- Hospital Owned

- Corporate Owned

Speciality

- Orthopedics

- Pain Management/Spinal Injections

- Gastroenterology

- Ophthalmology

- Others

Drivers

The shift of surgical procedures from inpatient to outpatient settings is driving the market

The shift of surgical procedures from inpatient to outpatient settings is driving the US ambulatory surgical center (ASC) market. Payers, particularly Medicare, and patients recognize the cost-effectiveness and convenience of performing eligible surgical procedures in an ASC compared to a traditional hospital setting. Technological advancements in surgical techniques and anesthesia allow for a wider range of procedures to be safely performed in an outpatient environment, with patients returning home the same day.

This ongoing migration of surgical volume from hospitals to ASCs directly increases the demand for ASC facilities and services. The Centers for Medicare & Medicaid Services (CMS) periodically updates the list of procedures approved for Medicare reimbursement in ASCs, directly enabling this shift; CMS added 37 surgical procedures to the ASC Covered Procedures List for Calendar Year 2024.

Restraints

Reimbursement policies and regulatory hurdles are restraining the market

Reimbursement policies and regulatory hurdles are restraining the US ambulatory surgical center market. While the shift to outpatient settings is a driver, the reimbursement rates offered by government payers like Medicare and private insurers for procedures performed in ASCs can be lower than those in hospital outpatient departments for similar services.

This disparity can impact the profitability of ASCs and their ability to invest in new technology or expand services. Additionally, navigating complex state and federal regulations pertaining to licensing, certification, and operation of ASCs presents an ongoing administrative burden. According to a summary of the proposed rule for Calendar Year 2025, CMS estimated total ASC Medicare payments for 2025 would be approximately US$7.4 billion, reflecting the significant but regulated revenue stream for these facilities.

Opportunities

The expansion of payable procedures in the ASC setting is creating growth opportunities

The expansion of payable procedures in the US ambulatory surgical center setting is creating growth opportunities. CMS regularly reviews procedures and considers adding them to the list of those eligible for Medicare reimbursement in ASCs. Each addition to this list opens up new service lines and revenue potential for ASCs, allowing them to perform a broader scope of surgical interventions.

This ongoing process of adding procedures, particularly complex ones like total joint replacements in recent years, significantly expands the market potential for ASCs and drives investment in specialized equipment and physician recruitment. CMS finalized the addition of 37 surgical procedures to the ASC Covered Procedures List for Calendar Year 2024, demonstrating continued expansion of payable services in this setting.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors influence the US ambulatory surgical center market. Economic conditions directly impact patient volumes as individuals may postpone elective surgical procedures due to financial concerns, including deductibles and copayments, even in the lower-cost ASC setting. Inflation increases operating expenses for ASCs, including costs for surgical supplies, pharmaceuticals, labor, and utilities, pressuring profit margins.

Geopolitical events can disrupt global supply chains for medical devices and surgical instruments, leading to potential shortages or increased costs for essential items used in procedures. However, a focus on healthcare cost containment, often amplified during economic pressures, can further drive the shift towards more affordable ASC settings, providing a contrasting positive effect on volume.

Current US tariff policies impact the US ambulatory surgical center market. Tariffs on imported surgical instruments, medical devices, and other supplies used in ASCs directly increase the cost of these essential inputs for ASC operators. This rise in supply costs impacts the profitability of procedures and can influence the overall cost of care in ASCs, potentially affecting their price advantage compared to hospitals.

Reports indicate that the US imports a significant value of medical devices and supplies, making ASCs susceptible to tariff-related price increases on these items. Conversely, these tariffs might encourage domestic manufacturing of surgical supplies and equipment, potentially leading to greater supply chain stability and potentially mitigating long-term cost increases, fostering a more resilient domestic industry supporting ASCs.

Latest Trends

Increased acquisition of ambulatory surgical centers by hospitals and health systems is creating lucrative prospects

Increased acquisition of ambulatory surgical centers by hospitals and health systems is creating growth opportunities in the US ambulatory surgical center market. Hospitals and larger health systems are increasingly acquiring or entering into partnerships with ASCs to integrate outpatient surgical services into their networks. This strategy allows them to capture a portion of the growing volume of procedures shifting to the outpatient setting, expand their geographic reach, and offer patients a lower-cost alternative for eligible surgeries while maintaining a connection to the patient within their system.

Reports on hospital and health system merger and acquisition activity, such as those highlighted by the American Hospital Association, indicate ongoing consolidation trends within the healthcare landscape that include the acquisition of outpatient facilities like ASCs.

Key Players Analysis

Key players in the US ambulatory surgical center (ASC) market pursue growth through strategic mergers and acquisitions, expanding their networks to increase patient volume and service offerings. They focus on forming joint ventures with hospitals and physician groups to enhance operational efficiency and access to specialized care.

Investments in advanced technologies, such as robotic-assisted surgeries and electronic health records, improve procedural outcomes and streamline workflows. Companies also emphasize geographic expansion into underserved regions, addressing the rising demand for outpatient surgical services. Additionally, they adapt to regulatory changes, such as the relaxation of Certificate of Need (CON) laws, to facilitate the development of new facilities and services.

SCA Health, a subsidiary of Optum, operates over 300 ASCs across 35 states, performing more than 1 million outpatient surgeries annually. The company partners with health plans, physician groups, and health systems to acquire, develop, and optimize surgical facilities. SCA Health’s affiliated physicians provide a range of surgical services, and the company has been part of Optum since 2017.

Recent Developments

- In January 2024, GE HealthCare acquired MIM Software, known for its expertise in medical imaging analysis and AI-driven solutions. These technologies are widely used in fields like radiation molecular radiotherapy, oncology, urology, and diagnostic imaging across healthcare environments, including imaging centers, specialty clinics, hospitals, and research institutions.

- In December 2023, GE HealthCare introduced the Vscan Air SL, a wireless portable ultrasound imaging system designed for quick cardiac and vascular evaluations at the point of care. This addition to the Vscan product line integrates XDclear and SignalMax technologies to provide high-quality imaging with enhanced sensitivity, penetration, and resolution, aimed at improving diagnostic accuracy and speeding up treatment decisions.

Top Key Players

- UnitedHealth Group

- Tenet Healthcare Corporation

- TeamHealth

- Surgery Partners

- SurgCenter

- Quorum Health

- GE HealthCare

- Edward-Elmhurst Health

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 44.5 billion |

| Forecast Revenue (2034) | US$ 103.4 billion |

| CAGR (2025-2034) | 8.8% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Center Type (Single-specialty and Multi-specialty), By Ownership (Physician Owned, Hospital Owned, and Corporate Owned), By Speciality (Orthopedics, Pain Management/Spinal Injections, Gastroenterology, Ophthalmology, and Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | UnitedHealth Group, Tenet Healthcare Corporation, TeamHealth, Surgery Partners, SurgCenter, Quorum Health, GE HealthCare, Edward-Elmhurst Health. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |