Global Unified Endpoint Security Market Size, Share and Analysis By Component (Software, Services), By Deployment Mode (Cloud Based, On-Premises), By Enterprise Size (Small and Medium Enterprises, Large Enterprises), By End-User (BFSI, Healthcare, Retail, IT and Telecommunications, Government and Defense, Manufacturing, Others), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2025-2035

- Published date: March 2026

- Report ID: 180831

- Number of Pages: 331

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Key Takeaway

- Key Insight Summary

- By Component

- By Deployment Mode

- By Enterprise Size

- By End User

- By Region

- Growth Factors

- Emerging Trends

- Key Market Segments

- Key Regions and Countries

- Driver Analysis

- Restraint Analysis

- Opportunity Analysis

- Challenge Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

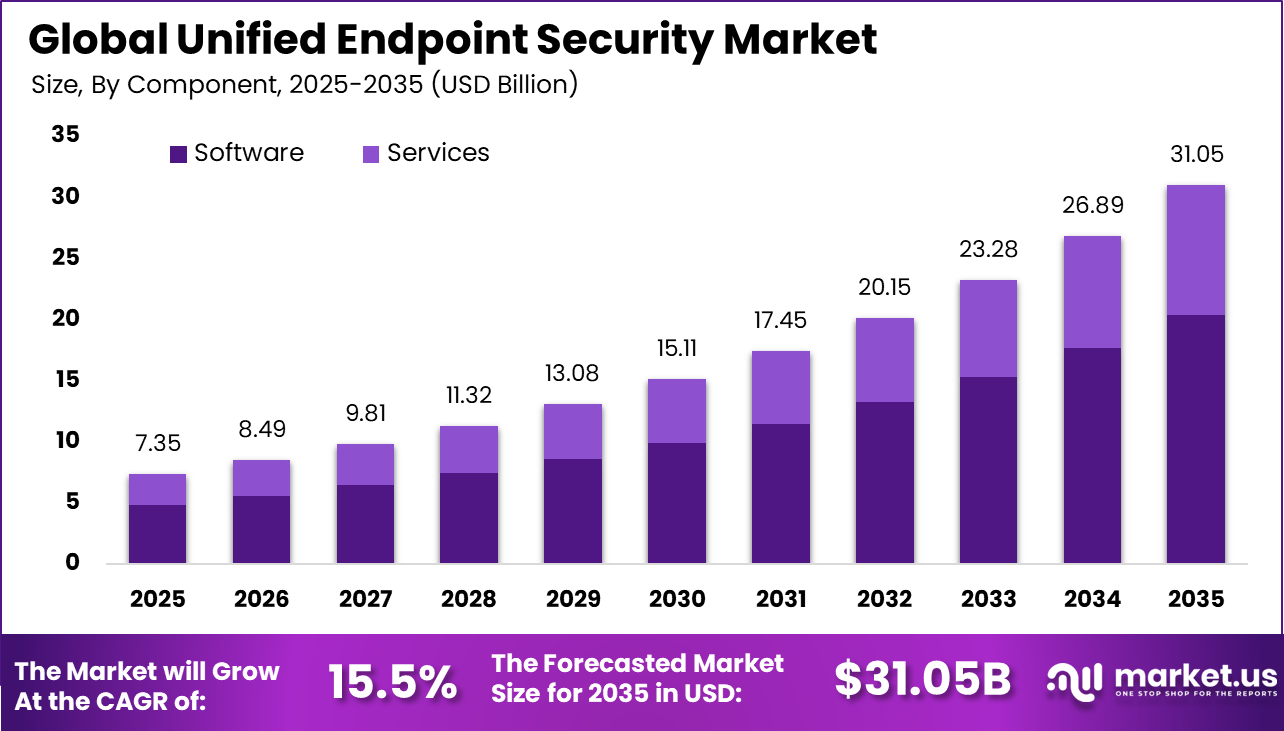

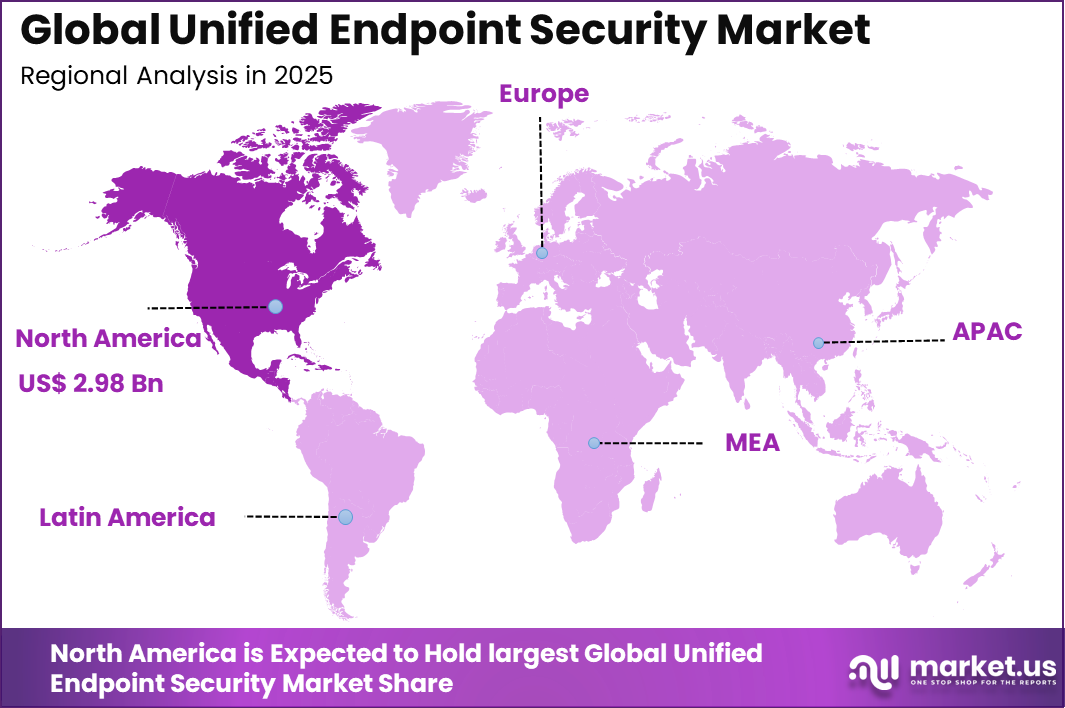

The Global Unified Endpoint Security Market size is expected to be worth around USD 31.05 billion by 2035, from USD 7.35 billion in 2025, growing at a CAGR of 15.5% during the forecast period from 2025 to 2035. North America held a dominant market position, capturing more than a 40.6% share, holding USD 2.98 billion in revenue.

The unified endpoint security market focuses on integrated platforms designed to protect devices such as laptops, desktops, servers, and mobile endpoints from cyber threats. These systems combine multiple security capabilities including endpoint protection, detection, response, and device management within a centralized platform. As organizations expand remote work environments and digital operations, endpoints have become a primary attack surface. Unified endpoint security platforms help organizations manage and secure these devices consistently.

The increasing use of remote work environments, cloud-based services, and connected devices has significantly expanded the attack surface for organizations. Traditional security solutions that operate independently often fail to provide complete protection. Unified endpoint security platforms address this challenge by delivering a comprehensive security architecture that monitors, detects, and responds to threats across all endpoint devices in real time.

One of the primary drivers of the unified endpoint security market is the rapid increase in cyberattacks targeting enterprise networks. Cybercriminals increasingly exploit vulnerabilities in endpoint devices to gain access to corporate systems. Unified endpoint security platforms help organizations detect and block these threats before they spread across networks.

Advancements in automation and analytics have strengthened endpoint protection capabilities. Modern platforms analyze device behavior in real time to detect suspicious activity. Automated response mechanisms isolate compromised devices and prevent threat spread. As cyber threats continue to evolve, unified endpoint security has become a critical layer within enterprise cybersecurity frameworks.

For instance, in January 2026, IBM expanded QRadar XDR with endpoint detection that nabbed 25% more U.S. contracts. Armonk’s AI-powered platform slashes investigation times, reinforcing North America’s cybersecurity edge for banks and healthcare facing sophisticated attacks daily.

Key Takeaway

- In 2025, the Software segment led the Unified Endpoint Security Market, accounting for 65.7% of total share.

- In 2025, On Premises deployment remained dominant, capturing 58.8% of the market.

- In 2025, Large Enterprises represented the primary customer segment with a 70.4% share.

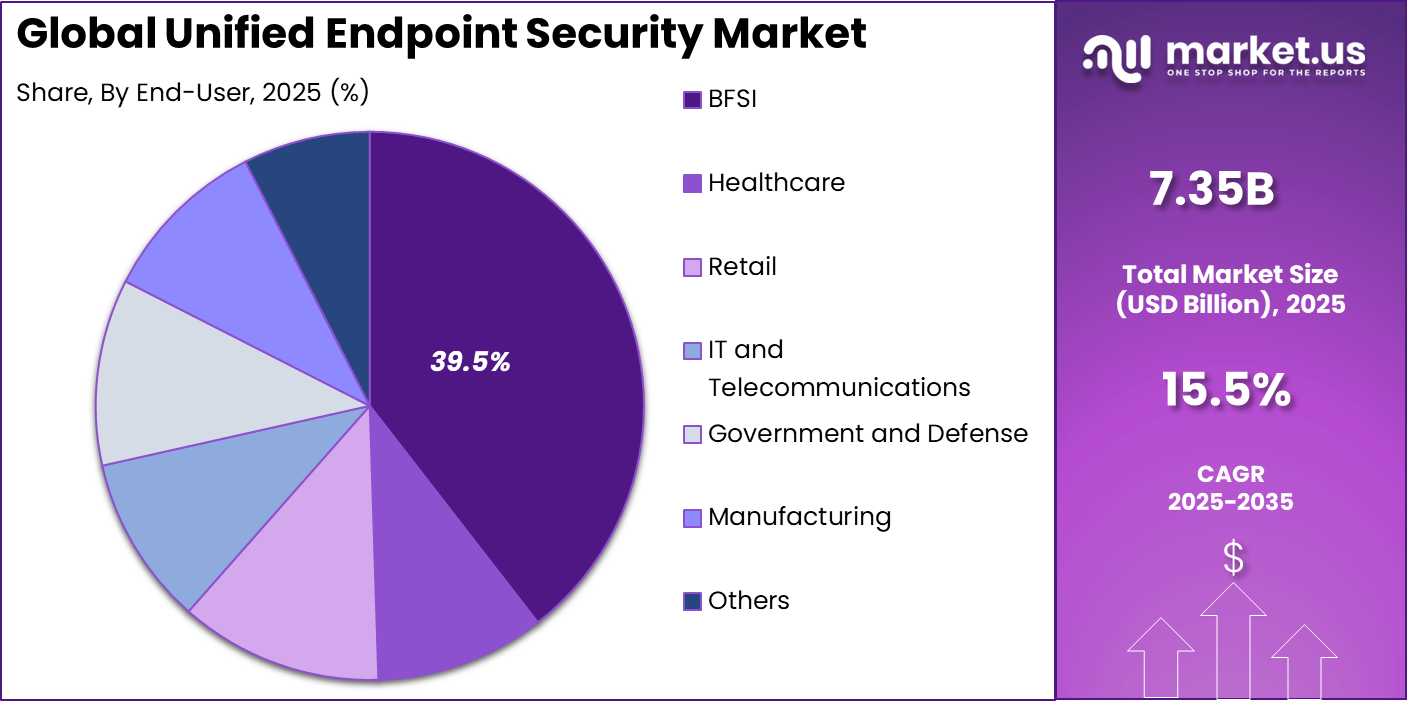

- In 2025, the BFSI sector held the largest end user share at 39.5%.

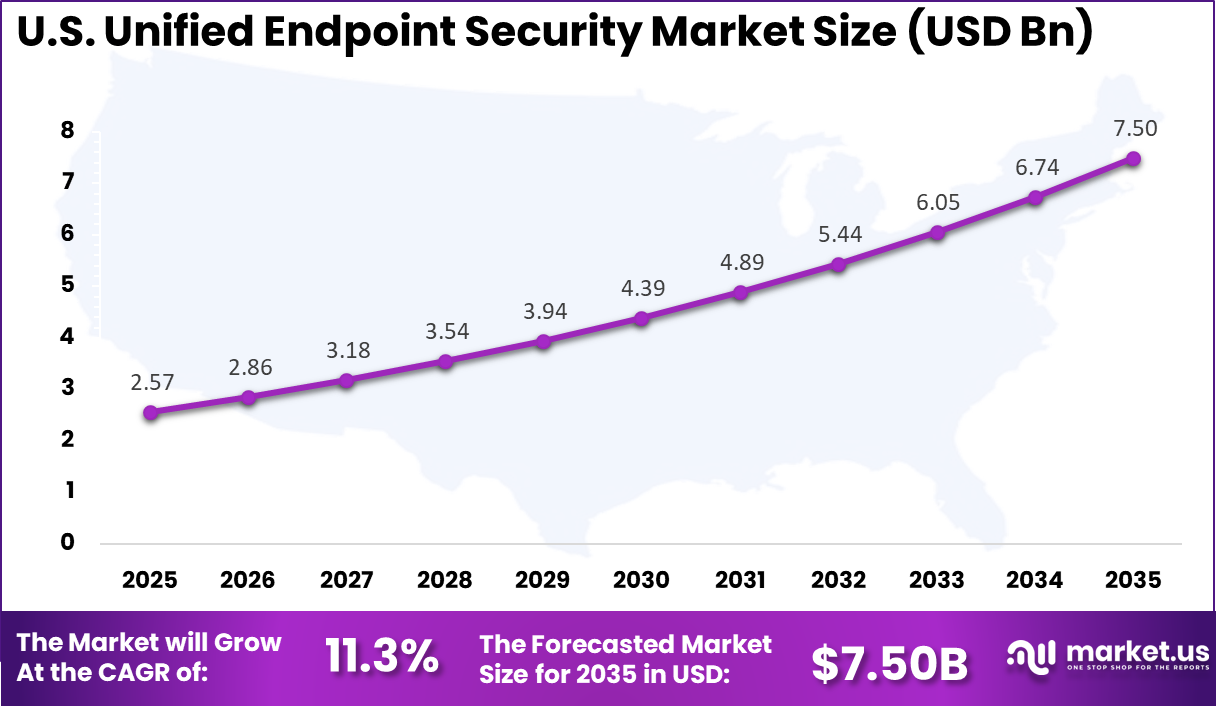

- In 2025, North America secured a 40.6% regional share, while the U.S. market reached USD 2.57 billion and recorded a growth rate of 11.3%.

Key Insight Summary

- Global connected devices are projected to reach 38.6 billion by 2025, increasing endpoint exposure across networks.

- Around 72% of cyber incidents involve endpoints as either the primary target or the initial attack entry point.

- Approximately 80% to 90% of successful ransomware attacks originate from unmanaged devices.

- The average cost of a data breach reached USD 4.88 million in 2024, highlighting the financial impact of endpoint vulnerabilities.

- Endpoint malware detections increased by 300% in the third quarter of 2024, reflecting heightened threat activity.

- About 72% of IT and security professionals report that siloed security data slows response efforts, with 63% confirming delays in critical incident handling.

- While 75% of IT employees report regular BYOD usage, only 52% of organizations formally permit it, increasing shadow IT exposure.

- Windows accounts for 40.26% of the Unified Endpoint Management market share in 2025, maintaining platform dominance.

- The IT and Telecommunications sector holds 25.10% of UEM adoption, while Healthcare represents the fastest growing vertical due to remote care expansion and compliance requirements.

By Component

Software accounts for 65.7% of the market, reflecting the central role of integrated security platforms in monitoring and protecting enterprise endpoints. These platforms provide capabilities such as threat detection, vulnerability scanning, device management, and automated response mechanisms. Security teams rely on software solutions to analyze endpoint activity and identify suspicious behavior before it leads to system compromise.

The growing sophistication of cyber threats has increased reliance on advanced security analytics and automated monitoring tools. Endpoint security software integrates with broader cybersecurity infrastructures to provide centralized visibility across devices and networks. As organizations expand digital operations, software based security platforms remain the foundation of unified endpoint protection strategies.

For Instance, in January 2026, Microsoft rolled out updates to Defender for Endpoint, sharpening AI-driven threat detection across devices. This boosts the software’s edge by automating responses to ransomware, helping teams spot issues faster without constant manual checks. It fits right into unified setups, keeping software dominant as attacks grow craftier.

By Deployment Mode

On premises deployment represents 58.8% of the market, indicating a strong preference for maintaining endpoint security infrastructure within internal networks. Many enterprises manage sensitive data and therefore require direct control over security systems and monitoring processes. Internal deployment allows organizations to enforce strict governance policies and customized security configurations.

Maintaining security systems on internal infrastructure also supports integration with existing enterprise networks and legacy IT environments. Organizations operating in regulated industries often prefer internal security monitoring to meet compliance requirements. As data protection remains a priority, on premises deployment continues to maintain strong adoption.

For instance, in March 2026, VMware announced tighter integration for on-site Workspace ONE, easing hybrid management. IT crews can now lock down local servers with fewer steps, ideal for firms wary of cloud shifts. It reinforces on-premises appeal by blending control with modern endpoint needs.

By Enterprise Size

Large enterprises account for 70.4% of market adoption due to the scale and complexity of their IT infrastructures. These organizations manage thousands of endpoints across multiple locations, increasing the risk of cyber threats and unauthorized access. Unified endpoint security platforms help centralize monitoring and maintain consistent security policies across devices.

Large organizations also maintain dedicated cybersecurity teams responsible for monitoring threats and responding to incidents. Automated endpoint security systems help these teams detect vulnerabilities and respond quickly to potential breaches. As enterprise digital ecosystems continue to expand, large companies remain the primary adopters of unified endpoint security solutions.

For Instance, in February 2026, Cisco refreshed its Secure Endpoint for big networks, adding global visibility features. Large teams managing thousands of devices now track threats across sites more easily, scaling protection without gaps. This keeps enterprises hooked on comprehensive coverage.

By End User

The BFSI sector represents 39.5% of the market due to the critical importance of protecting financial data and transactional systems. Financial institutions manage large volumes of sensitive information that must be secured against cyber threats. Endpoint security platforms help monitor devices used in banking operations and ensure secure access to financial systems.

Cybersecurity threats targeting financial institutions continue to increase as digital banking services expand. Unified endpoint security solutions enable financial organizations to maintain continuous monitoring and enforce strict access controls. As financial services become increasingly digital, the BFSI sector remains a key adopter of advanced endpoint security technologies.

For Instance, in January 2026, Fortinet upgraded its FortiEDR for financial networks, targeting phishing in banking apps. BFSI users gain from the quick isolation of compromised trader laptops, safeguarding transactions. It’s a smart fit for sectors where downtime costs millions.

By Region

North America holds 40.6% of the market share due to strong cybersecurity awareness and widespread adoption of enterprise security technologies. Organizations in the region invest heavily in endpoint protection solutions to secure digital infrastructure and comply with data protection regulations. The presence of advanced technology ecosystems further supports regional adoption.

For instance, in January 2026, Broadcom’s Symantec Endpoint Security achieved 98% malware detection rates in independent U.S. tests, expanding its North American footprint. This reinforces American leadership in unified security by delivering scalable protection for hybrid environments serving over 60,000 global enterprises from San Jose.

Within North America, the United States contributes USD 2.57 billion with a growth rate of 11.3%. The country’s large enterprise sector and expanding digital economy have strengthened demand for unified endpoint security platforms. Continued investment in cybersecurity infrastructure and threat intelligence capabilities is expected to support sustained market growth.

For instance, in January 2026, VMware, under Broadcom, launched AI-driven endpoint security updates to its unified management platform, serving 80% of Fortune 100 firms in North America. This innovation reinforces U.S. market leadership by enabling zero-trust security for hybrid workforces across cloud and on-premises environments.

Growth Factors

One of the major growth factors driving the Unified Endpoint Security Market is the rapid expansion of remote and hybrid work environments. Employees increasingly access corporate systems through personal laptops, smartphones, and remote networks. Unified endpoint security platforms help organizations maintain secure access by monitoring device activity and enforcing security policies regardless of user location.

Another growth factor is the increasing adoption of cloud computing and digital business operations. Organizations rely on multiple cloud applications and distributed IT infrastructure, which requires advanced endpoint protection to prevent unauthorized access and data breaches. Unified security platforms allow enterprises to manage security across cloud and on-premise environments from a single interface.

Emerging Trends

One emerging trend in the Unified Endpoint Security Market is the integration of artificial intelligence and behavioral analytics into security platforms. AI-driven systems analyze device activity patterns and identify anomalies that may indicate malicious behavior. This capability allows organizations to detect threats earlier and respond more effectively to cyber incidents.

Another trend is the convergence of endpoint security with unified endpoint management solutions. Modern platforms combine device management and cybersecurity functions to simplify IT operations and improve security visibility. This integration allows organizations to deploy updates, enforce policies, and detect threats from a unified platform.

Key Market Segments

By Component

- Software

- Services

By Deployment Mode

- Cloud Based

- On-Premises

By Enterprise Size

- Small and Medium Enterprises

- Large Enterprises

By End-User

- BFSI

- Healthcare

- Retail

- IT and Telecommunications

- Government and Defense

- Manufacturing

- Others

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver Analysis

Increasing Frequency of Cybersecurity Threats

A major driver of the Unified Endpoint Security Market is the rising number of cyberattacks targeting endpoint devices. Attackers frequently exploit vulnerabilities in user devices to gain unauthorized access to corporate networks. Unified endpoint security solutions provide advanced monitoring and threat detection capabilities that help organizations identify and mitigate these threats quickly.

Another driver is the growing complexity of enterprise IT environments. Organizations operate numerous devices across multiple locations and networks, making security management more challenging. Unified endpoint security platforms simplify security administration by consolidating monitoring, threat detection, and response capabilities into a single system.

Restraint Analysis

Implementation Complexity and Cost

One restraint affecting the Unified Endpoint Security Market is the complexity of implementing integrated security systems within large enterprise environments. Organizations may already use multiple security tools that require integration with new unified platforms. Managing this transition can require technical expertise and careful planning.

Another restraint involves the cost associated with deploying advanced security solutions. Implementing unified endpoint security platforms often requires investment in new infrastructure, training, and ongoing system maintenance. Smaller organizations may delay adoption due to budget limitations.

Opportunity Analysis

Expansion of IoT and Connected Devices

A significant opportunity in the Unified Endpoint Security Market lies in the expansion of IoT devices and connected technologies. Industrial systems, smart devices, and connected infrastructure generate new endpoints that must be secured against cyber threats. Unified endpoint security platforms can extend protection to these devices, helping organizations maintain secure operations.

Another opportunity involves the integration of endpoint security with broader security frameworks such as zero-trust architectures. Zero-trust security models require continuous verification of user and device identity. Unified endpoint security platforms provide the monitoring and control capabilities necessary to support these advanced security strategies.

Challenge Analysis

Managing Advanced and Evolving Threats

One of the major challenges in the Unified Endpoint Security Market is the rapid evolution of cyber threats. Attackers continually develop new techniques to bypass traditional security defenses. Security platforms must constantly update detection mechanisms and threat intelligence to remain effective against emerging attack methods.

Another challenge involves managing large volumes of security alerts generated by endpoint monitoring systems. Security teams may struggle to prioritize alerts and respond effectively without automated analysis tools. Organizations must implement advanced analytics and automation capabilities to manage these workloads efficiently.

Key Players Analysis

The Unified Endpoint Security Market is dominated by global technology companies that deliver integrated endpoint protection platforms combining threat detection, device management, and security analytics. Microsoft, VMware, IBM, and Cisco provide enterprise security ecosystems that protect endpoints across cloud, mobile, and on premise environments. Their solutions integrate artificial intelligence driven threat detection with centralized management tools.

Dedicated cybersecurity vendors contribute specialized endpoint detection and response technologies. CrowdStrike, Sophos, Trend Micro, Fortinet, and Check Point Software Technologies provide advanced endpoint security platforms with behavioral analytics and real time threat intelligence. Their products focus on detecting ransomware, advanced persistent threats, and fileless malware attacks. Continuous innovation in automated response capabilities has strengthened their competitive positioning.

Additional endpoint security providers further expand the market ecosystem. Broadcom through its Symantec security portfolio, along with Trellix, SentinelOne, Bitdefender, Tanium, Ivanti, BlackBerry, F-Secure, ESET, and Kaspersky offer endpoint protection, vulnerability management, and threat intelligence solutions. These vendors compete through AI driven malware detection, automated remediation tools, and cloud native security architectures.

Top Key Players in the Market

- Microsoft

- VMware

- IBM

- Cisco

- Broadcom (Symantec)

- CrowdStrike

- McAfee

- Trend Micro

- Sophos

- Check Point Software Technologies

- Ivanti

- BlackBerry

- Fortinet

- Trellix

- SentinelOne

- Bitdefender

- Tanium

- F-Secure

- ESET

- Kaspersky

- Others

Recent Developments

- In March 2026, Cisco refreshed Secure Endpoint with GenAI-powered sandboxing, detecting 98% of polymorphic malware on first pass. Their integration with Umbrella now offers unified protection across 10 million endpoints globally, reinforcing Silicon Valley’s dominance in network-integrated endpoint defense.

- In November 2025, Broadcom’s Symantec Endpoint Security Complete added cloud-native deception tech, trapping 75% more lateral movement attempts. This acquisition-fueled upgrade targets hybrid workforces, solidifying their North American stronghold in comprehensive, scalable endpoint protection suites.

Report Scope

Report Features Description Market Value (2025) USD 7.3 Bn Forecast Revenue (2035) USD 31.05 Bn CAGR (2025-2035) 15.5% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2025-2035 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends Segments Covered By Component (Software, Services), By Deployment Mode (Cloud-Based, On-Premises), By Enterprise Size (Small and Medium Enterprises, Large Enterprises), By End-User (BFSI, Healthcare, Retail, IT and Telecommunications, Government and Defense, Manufacturing, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Microsoft, VMware, IBM, Cisco, Broadcom (Symantec), CrowdStrike, McAfee, Trend Micro, Sophos, Check Point Software Technologies, Ivanti, BlackBerry, Fortinet, Trellix, SentinelOne, Bitdefender, Tanium, F-Secure, ESET, Kaspersky, Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Unified Endpoint Security MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Unified Endpoint Security MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Microsoft

- VMware

- IBM

- Cisco

- Broadcom (Symantec)

- CrowdStrike

- McAfee

- Trend Micro

- Sophos

- Check Point Software Technologies

- Ivanti

- BlackBerry

- Fortinet

- Trellix

- SentinelOne

- Bitdefender

- Tanium

- F-Secure

- ESET

- Kaspersky

- Others

Our Clients

- 180831

- March 2026