Global Torque Vectoring Market Size, Share, Growth Analysis By Electric Vehicle Type (BEV, HEV), By Clutch Actuation Type (Hydraulic, Electronic), By Propulsion (All-Wheel Drive/Four-Wheeled Drive (AWD/FWD), Front-Wheel Drive (FWD), Rear-Wheel Drive (RWD)), By Technology (Active Torque Vectoring System (ATVS), Passive Torque Vectoring System (PTVS)), By Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCV)), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 178569

- Number of Pages: 210

- Format:

-

keyboard_arrow_up

Quick Navigation

- Market Overview

- Key Takeaways

- Electric Vehicle Type Analysis

- Clutch Actuation Type Analysis

- Propulsion Analysis

- Technology Analysis

- Vehicle Type Analysis

- Key Market Segments

- Drivers

- Restraints

- Growth Factors

- Emerging Trends

- Regional Analysis

- Key Regions and Countries

- Key Company Insights

- Recent Developments

- Report Scope

Market Overview

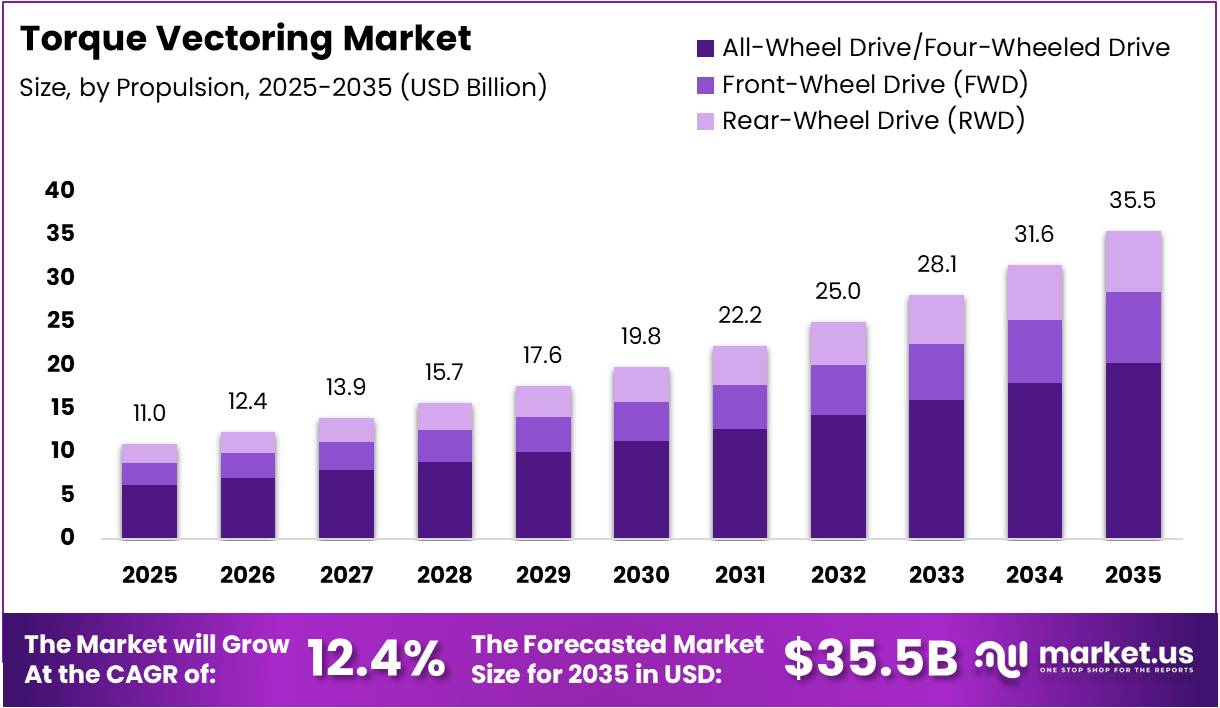

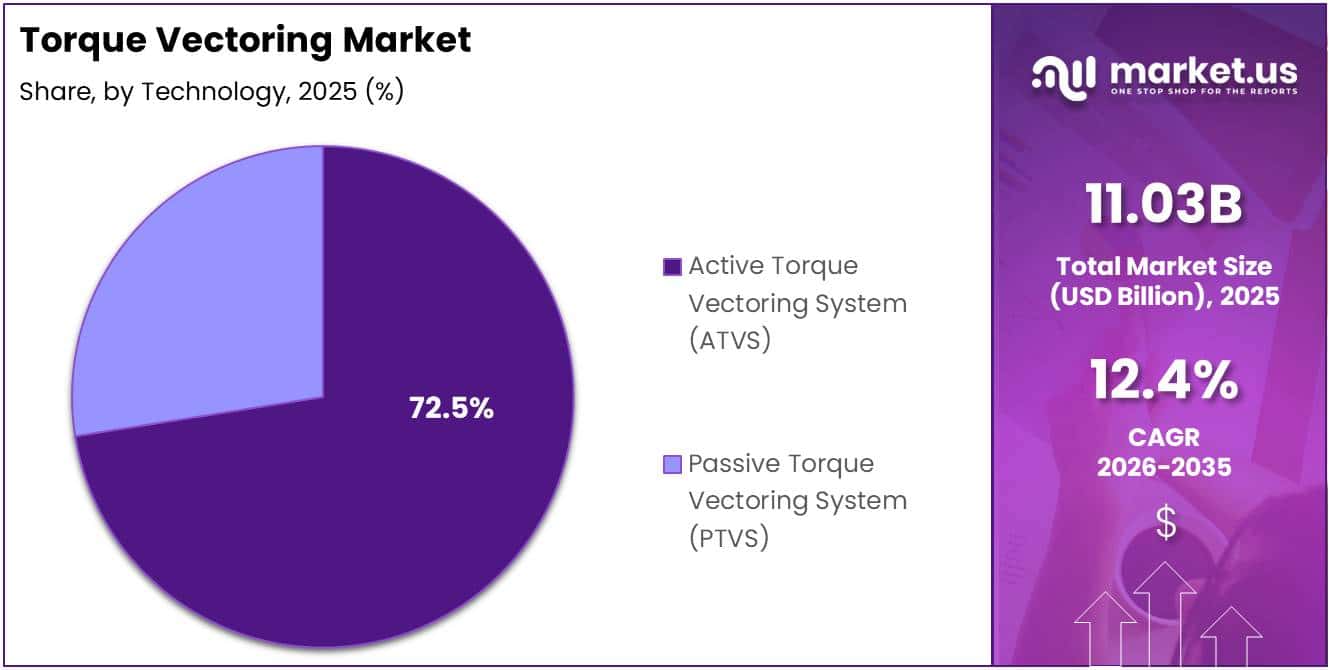

The Global Torque Vectoring Market size is expected to be worth around USD 35.5 Billion by 2035 from USD 11.03 Billion in 2025, growing at a CAGR of 12.4% during the forecast period 2026 to 2035.

The torque vectoring market refers to systems that distribute engine or motor torque independently to individual wheels, improving vehicle stability, handling, and traction. These systems are increasingly embedded in modern passenger cars, electric vehicles, and high-performance automobiles to deliver superior driving dynamics.

Torque vectoring technology works by actively managing wheel torque during acceleration, braking, and cornering. This gives drivers improved control, particularly in challenging road conditions. Moreover, it plays a key role in reducing understeer and oversteer, making it a critical safety feature for modern vehicles.

The growing adoption of electric and hybrid vehicles is a primary growth catalyst for this market. Automakers are integrating torque vectoring into battery electric vehicle platforms to optimize energy efficiency and performance. Consequently, demand from EV-focused OEMs is accelerating faster than any other segment in the automotive drivetrain space.

Government regulations around vehicle safety and emissions are also pushing automakers to adopt advanced drivetrain technologies. Regulatory frameworks in North America, Europe, and Asia are encouraging investment in vehicle dynamics systems. Additionally, safety mandates are driving demand for active stability control technologies, including torque vectoring, as standard equipment.

Research institutions and automotive engineers have validated significant performance gains from torque vectoring. According to a study published in Springer, a torque vectoring control strategy led to energy savings of more than 8% during steady-state cornering. Furthermore, according to IJRASET, enabling torque vectoring reduced yaw rate deviation during constant radius cornering from approximately 12–15% down to 3–5%, indicating significantly better trajectory tracking and stability.

Additional performance data supports the market’s technical value proposition. According to ScienceDirect, a hierarchical torque vectoring control strategy for four-in-wheel-motor electric vehicles achieved an 11.27% reduction in energy consumption compared with conventional control without compromising handling performance. These findings reinforce strong long-term demand across performance and utility vehicle segments.

Key Takeaways

- The global Torque Vectoring Market was valued at USD 11.03 Billion in 2025 and is projected to reach USD 35.5 Billion by 2035.

- The market is growing at a CAGR of 12.4% during the forecast period 2026 to 2035.

- By Electric Vehicle Type, BEV segment held a dominant market share of 68.9% in 2025.

- By Clutch Actuation Type, Hydraulic segment led with a 56.2% market share in 2025.

- By Propulsion, All-Wheel Drive/Four-Wheeled Drive (AWD/FWD) segment dominated with a 57.1% share in 2025.

- By Technology, Active Torque Vectoring System (ATVS) held the largest share at 72.5% in 2025.

- By Vehicle Type, Passenger Cars led with a 61.3% market share in 2025.

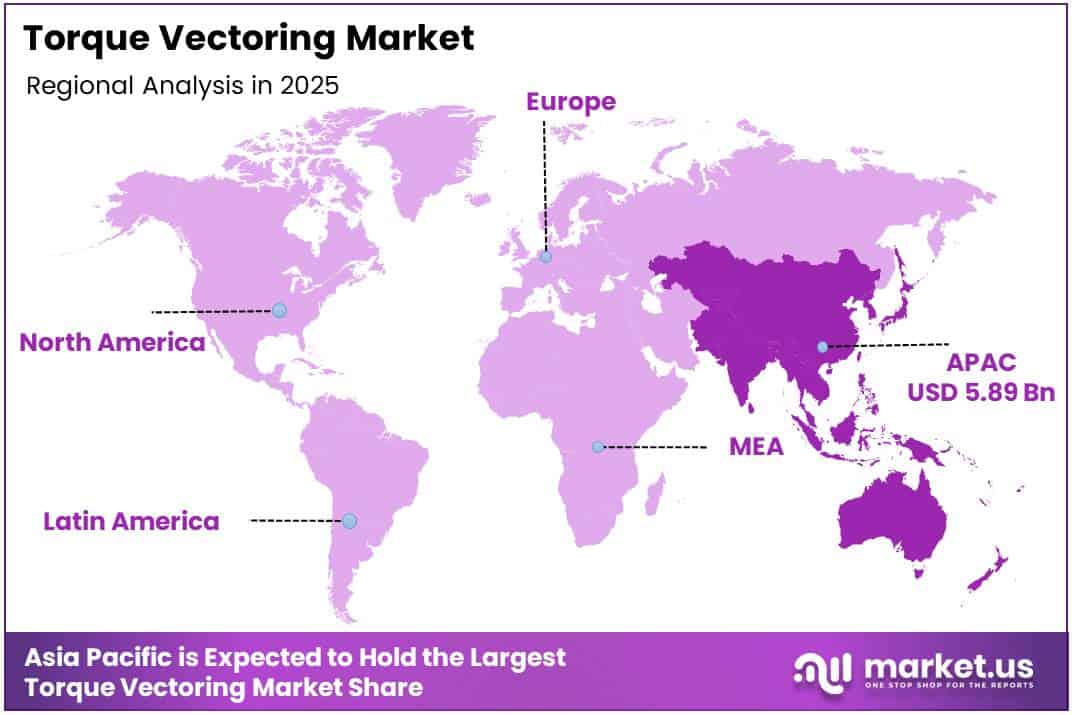

- Asia Pacific dominated the regional market with a 53.40% share, valued at USD 5.89 Billion in 2025.

Electric Vehicle Type Analysis

BEV dominates with 68.9% due to high torque vectoring integration in fully electric drivetrains.

In 2025, BEV held a dominant market position in the By Electric Vehicle Type segment of the Torque Vectoring Market, with a 68.9% share. BEVs benefit greatly from torque vectoring because electric motors allow precise, instant torque control at each wheel. This makes torque distribution more efficient and responsive compared to combustion-based alternatives.

The HEV segment, while smaller, continues to grow steadily as hybrid platforms adopt more sophisticated drivetrain management systems. Automakers are integrating torque vectoring into HEV architectures to enhance fuel efficiency and vehicle dynamics. Additionally, the expanding hybrid vehicle lineup across key markets supports consistent demand growth for this sub-segment.

Clutch Actuation Type Analysis

Hydraulic dominates with 56.2% due to proven reliability and widespread OEM adoption.

In 2025, Hydraulic held a dominant market position in the By Clutch Actuation Type segment of the Torque Vectoring Market, with a 56.2% share. Hydraulic systems are preferred for their durability, high torque capacity, and established performance credentials. Moreover, their compatibility with a wide range of vehicle types ensures continued OEM preference.

The Electronic actuation segment is gaining momentum as automakers shift toward software-defined vehicle platforms. Electronic systems offer faster response times and easier integration with advanced driver assistance systems. Consequently, this segment is expected to grow faster over the forecast period as EV adoption accelerates globally.

Propulsion Analysis

All-Wheel Drive/Four-Wheeled Drive (AWD/FWD) dominates with 57.1% due to superior traction and stability across vehicle classes.

In 2025, All-Wheel Drive/Four-Wheeled Drive (AWD/FWD) held a dominant market position in the By Propulsion segment of the Torque Vectoring Market, with a 57.1% share. AWD systems benefit most from torque vectoring as torque can be distributed across all four wheels independently. This enables greater control during cornering, acceleration, and adverse weather conditions.

The Front-Wheel Drive (FWD) segment holds a notable portion of the market, primarily in compact and economy vehicles. Torque vectoring in FWD configurations helps manage understeer, which is a common handling limitation. Therefore, automakers are increasingly offering torque vectoring as an upgrade in FWD-based models.

The Rear-Wheel Drive (RWD) segment is popular in performance and luxury vehicles, where precise rear-wheel torque control delivers dynamic handling characteristics. RWD torque vectoring is commonly found in sports cars and premium sedans. Additionally, the growing demand for high-performance EVs with rear-biased layouts supports this segment’s development.

Technology Analysis

Active Torque Vectoring System (ATVS) dominates with 72.5% due to real-time adaptive torque control and superior performance outcomes.

In 2025, Active Torque Vectoring System (ATVS) held a dominant market position in the By Technology segment of the Torque Vectoring Market, with a 72.5% share. ATVS dynamically adjusts torque distribution based on real-time vehicle data, offering responsive and precise handling. This makes it the preferred technology for both performance and safety-focused applications.

The Passive Torque Vectoring System (PTVS) segment serves cost-sensitive applications where simpler mechanical torque distribution is sufficient. Passive systems do not require electronic intervention and are commonly found in entry-level performance vehicles. However, their share is gradually declining as the industry shifts toward more intelligent and adaptive active systems.

Vehicle Type Analysis

Passenger Cars dominate with 61.3% due to mass-market adoption and high-volume production.

In 2025, Passenger Cars held a dominant market position in the By Vehicle Type segment of the Torque Vectoring Market, with a 61.3% share. The widespread adoption of torque vectoring in sedans, SUVs, and hatchbacks reflects growing consumer expectations for improved driving dynamics. Moreover, OEM integration into mainstream passenger vehicles continues to increase globally.

The Light Commercial Vehicles (LCV) segment is expanding as fleet operators and commercial vehicle manufacturers seek better traction control and load stability. Torque vectoring in LCVs improves operational efficiency across varied terrain and road conditions. Consequently, commercial fleets in logistics and last-mile delivery are gradually adopting these systems to enhance safety and performance.

Key Market Segments

By Electric Vehicle Type

- BEV

- HEV

By Clutch Actuation Type

- Hydraulic

- Electronic

By Propulsion

- All-Wheel Drive/Four-Wheeled Drive (AWD/FWD)

- Front-Wheel Drive (FWD)

- Rear-Wheel Drive (RWD)

By Technology

- Active Torque Vectoring System (ATVS)

- Passive Torque Vectoring System (PTVS)

By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles (LCV)

Drivers

Rising Demand for Vehicle Safety, Performance, and Electrification Drives Torque Vectoring Market Growth

The growing adoption of advanced vehicle stability and safety systems is a key driver for the torque vectoring market. Automakers are integrating active torque management into mainstream vehicles to meet safety standards. Moreover, consumer demand for improved cornering, traction, and handling has made torque vectoring a priority for vehicle engineering teams globally.

Increasing demand for high-performance and sports vehicles is fueling adoption of sophisticated torque vectoring solutions. Drivers seeking enhanced driving dynamics are pushing OEMs to offer active torque distribution as a standard or optional feature. Consequently, luxury and performance-oriented brands are investing heavily in next-generation torque management technologies.

The growing integration of electric and hybrid powertrains in automobiles is further expanding the market. Electric drivetrains are inherently well-suited for torque vectoring due to instant and precise motor control. Therefore, the rapid global expansion of EV production is directly contributing to increased torque vectoring system deployment across multiple vehicle platforms.

Restraints

System Complexity and Low Consumer Awareness Restrain Torque Vectoring Market Adoption

High complexity in system calibration and vehicle integration is a significant restraint for the torque vectoring market. These systems require precise tuning to work harmoniously with other vehicle control modules such as ABS and stability control. Moreover, integration challenges increase development timelines and add to overall vehicle manufacturing costs for OEMs.

The technical demands of torque vectoring systems also increase the burden on automotive engineers during the design phase. Ensuring compatibility across different drivetrain configurations and vehicle platforms requires extensive testing and validation. Consequently, smaller manufacturers and regional OEMs often face barriers to adoption due to limited technical resources and expertise.

Limited awareness among consumers about the performance benefits of torque vectoring further slows market growth. Many vehicle buyers are unfamiliar with how torque vectoring improves handling, safety, and efficiency. Therefore, the lack of consumer education reduces perceived value, which in turn affects purchasing decisions and the broader commercialization of these systems.

Growth Factors

EV Expansion, Autonomous Integration, and OEM Collaboration Accelerate Torque Vectoring Market Growth

The expansion in electric vehicle and hybrid vehicle segments presents a strong growth opportunity for the torque vectoring market. As EV adoption increases globally, automakers require advanced torque management solutions to maximize efficiency and performance. Moreover, purpose-built EV platforms are specifically designed to accommodate active torque vectoring from the ground up.

Integration with autonomous and connected vehicle technologies is another key growth factor. Torque vectoring systems play a vital role in vehicle dynamics management for self-driving applications. Consequently, as autonomous vehicle development accelerates, demand for intelligent torque distribution systems that respond to real-time sensor inputs is expected to increase significantly.

Collaborations between OEMs and Tier-1 suppliers for research and development innovation are driving meaningful advancements in torque vectoring technology. Joint ventures and strategic partnerships are enabling faster product development cycles and cost optimization. Therefore, these collaborations are helping bring more affordable and scalable torque vectoring solutions to a wider range of vehicle segments.

Emerging Trends

AI Integration, Software-Defined Dynamics, and Energy Efficiency Shape the Future of Torque Vectoring

The use of artificial intelligence and machine learning for real-time torque distribution is transforming how torque vectoring systems operate. AI-powered algorithms can analyze road conditions, driver behavior, and vehicle dynamics simultaneously. Moreover, this enables predictive torque adjustments that improve handling precision beyond what traditional rule-based control systems can achieve.

The emergence of software-defined vehicle dynamics systems is another major trend reshaping the torque vectoring market. These platforms allow torque vectoring behavior to be updated and customized through over-the-air software changes. Consequently, automakers can continuously improve system performance post-sale, adding significant value to both the vehicle and the customer experience.

Increased focus on energy-efficient vehicle performance is driving demand for torque vectoring systems that minimize drivetrain energy losses. Optimized torque distribution reduces unnecessary wheel slip and improves overall powertrain efficiency. Therefore, energy-conscious automakers and fleet operators are viewing torque vectoring not just as a performance tool but as a critical efficiency enabler.

Regional Analysis

Asia Pacific Dominates the Torque Vectoring Market with a Market Share of 53.40%, Valued at USD 5.89 Billion

Asia Pacific leads the global torque vectoring market, holding a dominant share of 53.40% and valued at USD 5.89 Billion in 2025. The region’s dominance is driven by large-scale automotive manufacturing in China, Japan, and South Korea, combined with rapid EV adoption. Moreover, strong government support for electric mobility and vehicle safety standards continues to accelerate market growth across the region.

North America Torque Vectoring Market Trends

North America represents a significant market for torque vectoring, supported by strong consumer demand for performance vehicles and advanced driver assistance systems. The United States leads regional adoption, with major automakers integrating torque vectoring into both electric and conventional vehicle platforms. Additionally, increasing regulatory focus on vehicle safety is encouraging broader deployment of active drivetrain technologies.

Europe Torque Vectoring Market Trends

Europe holds a strong position in the torque vectoring market, driven by the region’s well-established automotive engineering heritage and strict vehicle safety regulations. Germany, France, and the UK are key contributors, with premium automakers actively investing in torque vectoring for performance and electric vehicle lineups. Furthermore, the EU’s emissions reduction targets are accelerating EV integration, indirectly boosting torque vectoring adoption.

Middle East and Africa Torque Vectoring Market Trends

The Middle East and Africa market for torque vectoring is at an early growth stage but shows increasing potential. Rising vehicle sales in GCC countries and growing interest in high-performance SUVs are creating demand for advanced drivetrain technologies. However, limited local manufacturing capability means the region currently depends on imports, which may moderate near-term growth.

Latin America Torque Vectoring Market Trends

Latin America presents a developing opportunity for the torque vectoring market, with Brazil and Mexico leading automotive activity in the region. Growing vehicle sales and increasing awareness of safety technologies are gradually building demand. Consequently, as EV infrastructure develops and OEMs expand their presence in the region, torque vectoring adoption is expected to rise steadily.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

BorgWarner Inc. is a global leader in clean and efficient technology solutions for combustion, hybrid, and electric vehicles. The company has made significant investments in electric drivetrain components, including torque vectoring systems tailored for BEV platforms. Its strategic focus on electrification positions it as a core supplier to major OEMs seeking advanced torque management solutions.

GKN Automotive Ltd. is widely recognized for its expertise in driveline technologies, including advanced torque vectoring systems for AWD and electric vehicle platforms. The company supplies systems to a broad range of global automakers and continues to invest in next-generation eDrive solutions. Its strong OEM partnerships and engineering capabilities make it a key force in the global market.

JTEKT Corporation brings deep engineering expertise in drivetrain and steering systems, with a growing portfolio in torque vectoring technologies. The company focuses on developing compact, high-efficiency solutions suitable for both passenger cars and light commercial vehicles. Moreover, JTEKT’s integration of electronic control systems into its product lineup supports its competitive positioning in the evolving market.

American Axle & Manufacturing specializes in driveline and drivetrain components with a strong presence in the torque vectoring segment. The company serves global OEMs with scalable torque management solutions for both conventional and electric powertrains. Its ongoing investment in R&D and manufacturing innovation enables it to deliver cost-competitive systems aligned with emerging automotive trends.

Key Players

- BorgWarner Inc.

- GKN Automotive Ltd.

- JTEKT Corporation

- American Axle & Manufacturing

- Magna International Inc.

- Schaeffler Group

- Dana Incorporated

- Eaton Corporation

- Continental AG

- DENSO Corporation

- Valeo SA

- Hyundai Mobis

- Aisin Corporation

- Bosch Mobility Solutions

- Hitachi Astemo

- Other Key Players

Recent Developments

- January 2025 – American Axle & Manufacturing announced a combination with Dowlais in a deal valued at $1.44 Billion in cash and stock. This strategic merger is expected to strengthen the combined entity’s capabilities in driveline technologies, including torque vectoring systems for next-generation vehicle platforms.

- October 2024 – Schaeffler AG completed a merger with Vitesco Technologies Group AG, creating a stronger combined portfolio across electrification and drivetrain components. The integration is expected to enhance Schaeffler’s torque vectoring product offerings and expand its reach among global EV-focused OEM customers.

- May 2024 – BorgWarner launched its electric Torque Vectoring and Disconnect (eTVD) system specifically designed for battery electric vehicles (BEVs). This system delivers precise wheel-level torque control and improves handling dynamics, representing a key advancement in BorgWarner’s growing EV drivetrain technology portfolio.

Report Scope

Report Features Description Market Value (2025) USD 11.03 Billion Forecast Revenue (2035) USD 35.5 Billion CAGR (2026-2035) 12.4% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Electric Vehicle Type (BEV, HEV), By Clutch Actuation Type (Hydraulic, Electronic), By Propulsion (All-Wheel Drive/Four-Wheeled Drive (AWD/FWD), Front-Wheel Drive (FWD), Rear-Wheel Drive (RWD)), By Technology (Active Torque Vectoring System (ATVS), Passive Torque Vectoring System (PTVS)), By Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCV)) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape BorgWarner Inc., GKN Automotive Ltd., JTEKT Corporation, American Axle & Manufacturing, Magna International Inc., Schaeffler Group, Dana Incorporated, Eaton Corporation, Continental AG, DENSO Corporation, Valeo SA, Hyundai Mobis, Aisin Corporation, Bosch Mobility Solutions, Hitachi Astemo, Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- BorgWarner Inc.

- GKN Automotive Ltd.

- JTEKT Corporation

- American Axle & Manufacturing

- Magna International Inc.

- Schaeffler Group

- Dana Incorporated

- Eaton Corporation

- Continental AG

- DENSO Corporation

- Valeo SA

- Hyundai Mobis

- Aisin Corporation

- Bosch Mobility Solutions

- Hitachi Astemo

- Other Key Players

Our Clients

- 178569

- Feb 2026