Quick Navigation

- Report Overview

- Key Takeaways

- Product Material Analysis

- Material Analysis

- Type of Wound Analysis

- Application Analysis

- End-User Analysis

- Key Market Segments

- Drivers

- Restraints

- Opportunities

- Impact of Macroeconomic / Geopolitical Factors

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

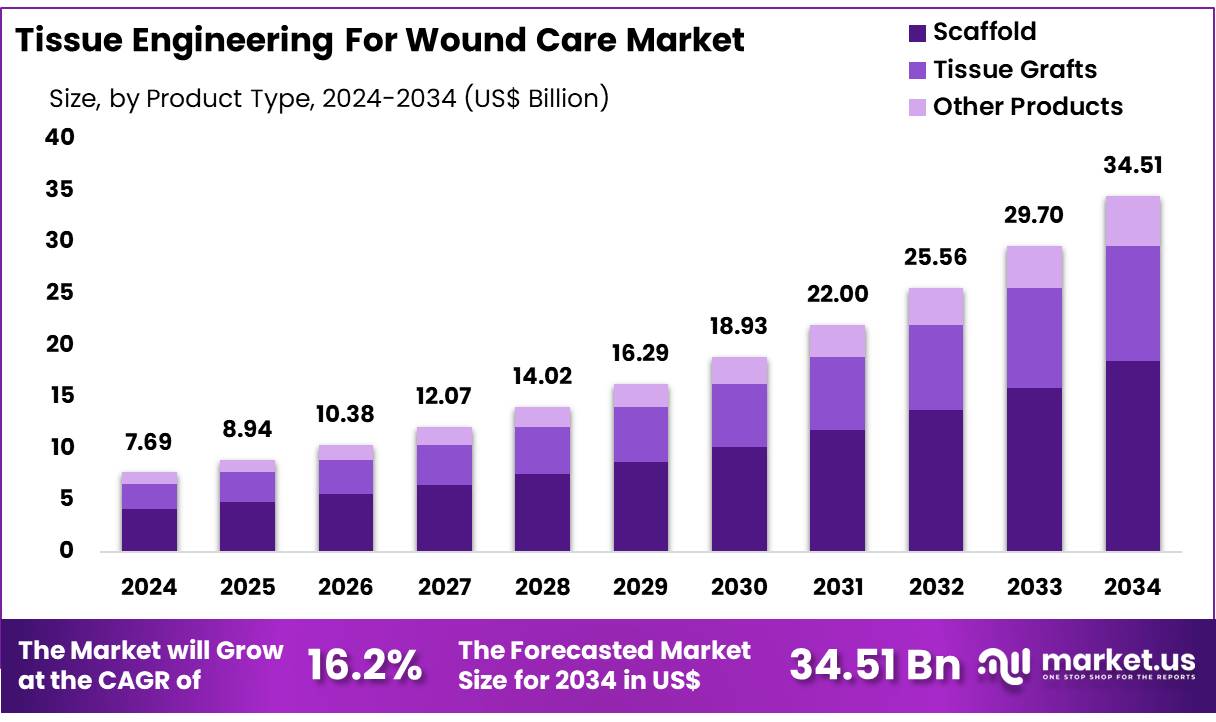

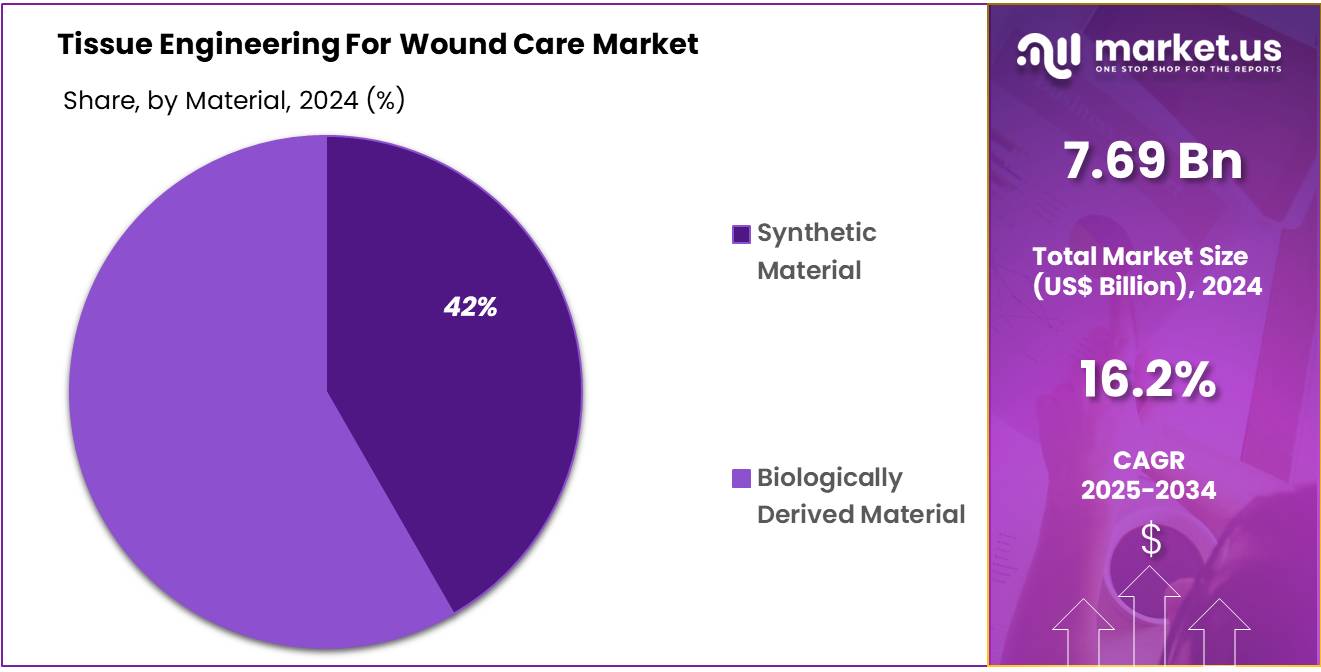

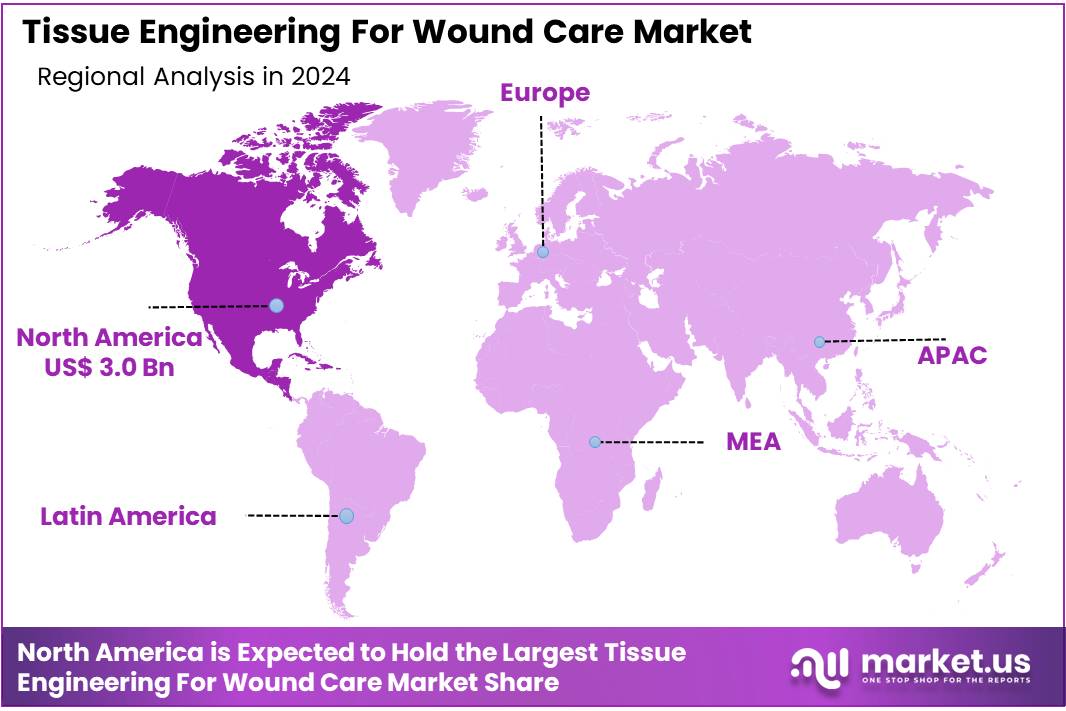

Global Tissue Engineering for Wound Care Market size is expected to be worth around US$ 34.52 billion by 2034 from US$ 7.69 billion in 2024, growing at a CAGR of 16.2% during the forecast period 2024 to 2034. In 2024, North America led the market, achieving over 38.7% share with a revenue of US$ 3.0 Billion.

The market’s growth is largely attributed to the increasing prevalence of chronic diseases and injuries, rising healthcare expenditures, and greater awareness of the benefits of tissue engineering techniques. Technological innovations, such as 3D bio printing and biomaterial scaffolds, are enhancing the effectiveness and precision of these solutions.

Additionally, supportive regulatory frameworks and increased investments in research and development are further propelling market expansion. The tissue engineering market for wound care has been experiencing significant growth, driven by advances in regenerative medicine, an aging population, and an increasing prevalence of chronic wounds. This market encompasses a range of innovative approaches, including bioengineered skin substitutes, scaffolds, and growth factors, aimed at enhancing the body’s natural healing processes.

However, the market faces challenges, including high costs associated with these technologies and regulatory hurdles. Approval processes in Europe can be lengthy and complex, which can slow the pace of product introductions. Despite these barriers, continued investments in R&D, growing public-private collaborations, and increasing awareness of the benefits of tissue-engineered wound care solutions are expected to fuel market growth. Analysts project sustained expansion, driven by technological advancements and a strong focus on personalized medicine in the wound care sector.

Key Takeaways

- In 2024, the market for Tissue Engineering for Wound Care generated a revenue of US$ 69 billion, with a CAGR of 16.2%, and is expected to reach US$ 34.52 billion by the year 2034.

- The product type segment is divided into Scaffold, Tissue Grafts, and Other Products, with Scaffold taking the lead in 2024 with a market share of 53.6%.

- Considering Material, the market is divided into Synthetic Material, and Biologically Derived Material. Among these, Synthetic Material held a significant share of 41.7%.

- Furthermore, concerning the Type of Wound, the market is segregated into Chronic Wounds, Acute Wounds. The Chronic Wounds segment stand out as the dominant segment, holding the largest revenue share of 64.9% in the Tissue Engineering for Wound Care market.

- Based on Application, the market is bifurcated into Skin Regeneration, Bone and Cartilage Regeneration, Soft Tissue Repair and Organ Regeneration. Skin Regeneration holds the largest market share with 51.2%.

- By End-User, the market is classified into Hospitals, Specialty Centers and Clinics, Ambulatory Surgical Centers. Hospitals held a major share of 62.5%.

- North America led the market by securing a market share of 38.7% in 2023.

Product Material Analysis

In the tissue engineering for wound care market, segmentation by product type includes scaffolds, tissue grafts, and other products. Scaffolds dominated the market with a market share of 53.6%, as they provide a structural framework for cell growth and tissue regeneration. They are increasingly used in advanced wound care applications, particularly for complex wounds. The “other products” category includes bioactive molecules, growth factors, and stem cell-based therapies, which are gaining traction due to their potential in regenerative medicine.

Companies like PolyNovo have developed novel biodegradable polymeric scaffolds that offer enhanced healing in burn wounds and surgical reconstructions. The NovoSorb BTM (Biodegradable Temporising Matrix), a dermal regeneration solution, has gained attention across Europe for its effectiveness in promoting regenerative healing in complex wounds. The company participated in the UK Pavilion at MEDICA 2021, where it introduced its innovative NovoSorb BTM technology to the European market, marking a pivotal step in expanding its reach across the continent.

Material Analysis

Biologically Derived Materials dominated the market with 58.3% share due to their natural ability to promote cell growth, improve healing outcomes, and reduce the risk of complications. They are increasingly preferred for their superior effectiveness in chronic wound healing. Biologically derived materials are favored in tissue engineering due to their natural compatibility with human tissues. They contain intrinsic biological signals that promote cellular attachment, migration, proliferation, and differentiation, which are essential for tissue regeneration.

These materials provide an environment that closely mimics the body’s extracellular matrix (ECM), promoting faster and more efficient healing of complex wounds. ADMs are human or animal-derived dermis that has been processed to remove cellular components while maintaining the structural integrity of the ECM. These products act as scaffolds, allowing the patient’s cells to infiltrate and regenerate tissue.

AlloDerm® is a human-derived ADM commonly used in reconstructive surgery and burn treatment. It supports tissue regeneration by providing a natural framework for cell attachment and growth, especially in complex wound scenarios.

Type of Wound Analysis

Chronic Wounds dominated the market with 64.9% share, as they require ongoing, advanced solutions to address the complexities of non-healing tissues, driving the demand for tissue engineering applications. These are long-lasting wounds that fail to heal properly, often due to underlying conditions like diabetes, vascular diseases, or pressure ulcers. Chronic wounds require advanced treatments, including tissue-engineered products like skin substitutes and collagen-based scaffolds, to promote regeneration and restore tissue integrity.

The demand for tissue engineering in chronic wounds is high due to the need for specialized, long-term care. Diabetic Ulcers are one of the most common types of chronic wounds, particularly among patients with uncontrolled diabetes. These ulcers form due to neuropathy and poor circulation, making the regeneration of tissue challenging.

Tissue-engineered products such as Apligraf® by Organogenesis are extensively used in treating diabetic foot ulcers. Apligraf® is a bilayered, bioengineered skin substitute containing living fibroblasts and keratinocytes that create an environment similar to human skin, promoting cell proliferation and angiogenesis—critical steps in the healing of chronic diabetic ulcers.

Application Analysis

In the tissue engineering for wound care market, segmentation by application includes skin regeneration, bone and cartilage regeneration, soft tissue repair, and organ regeneration. Among these, skin regeneration dominated the market with 51.2% market share due to the high prevalence of chronic wounds, burns, and diabetic ulcers, which require advanced wound care solutions. Skin regeneration applications leverage tissue engineering techniques like skin grafts, scaffolds, and bioactive dressings to promote healing and tissue repair.

Skin regeneration involves creating a conducive environment that enables tissue repair, often by providing a scaffold that supports cell attachment, proliferation, and differentiation. This segment benefits significantly from biologically derived and synthetic scaffolds that mimic the body’s natural extracellular matrix (ECM), thereby promoting faster and more effective healing.

Apligraf® is a bilayered bioengineered skin substitute containing both dermal and epidermal layers. It is primarily used to treat venous leg ulcers and diabetic foot ulcers. The product includes neonatal fibroblasts and keratinocytes embedded in a collagen matrix, providing a scaffold for the body’s cells to repopulate and regenerate the wound area effectively.

End-User Analysis

Hospitals dominated the market with 62.5% share as they are the primary end-users, providing comprehensive care for both acute and chronic wound cases. They are equipped with advanced infrastructure and medical professionals capable of handling complex wounds, making them the largest consumer of tissue-engineered products. Hospitals use biologically derived materials and synthetic scaffolds for wound healing, especially for severe or non-healing chronic wounds.

The availability of a multidisciplinary team, including surgeons, wound care specialists, and critical care professionals, is critical to utilizing tissue-engineered products like scaffolds, skin substitutes, and bioengineered matrices effectively. Hospitals have been at the forefront of adopting cutting-edge tissue-engineered technologies to enhance wound healing.

Key Market Segments

Product Material

- Scaffold

- Tissue Grafts

- Synthetic Grafts

- Allograft

- Autograft

- Xenograft

- Other Products

Material

- Synthetic Material

- Biologically Derived Material

Type of Wound

- Chronic Wounds

- Diabetic Ulcers

- Venous Ulcers

- Pressure Ulcers

- Acute Wounds

- Surgical Wounds

- Traumatic Wounds

- Burn Care

Application

- Skin Regeneration

- Bone and Cartilage Regeneration

- Soft Tissue Repair

- Organ Regeneration

End-User

- Hospitals

- Specialty Centers and Clinics

- Ambulatory Surgical Centers

Drivers

Continuous Innovations in Biomaterials and 3D Bio printing

Continuous innovations in biomaterials and 3D bio printing are significantly driving the Europe tissue engineering for wound care market. The development of advanced biomaterials, such as hydrogels, biodegradable polymers, and bioactive scaffolds, enhances the healing process by mimicking the natural extracellular matrix. These materials not only support cell growth and tissue regeneration but also provide antimicrobial properties, reducing the risk of infections—a common complication in chronic wounds. As research progresses, new biomaterials are being tailored to meet specific needs, improving patient outcomes and satisfaction.

In March 2021, CELLINK launched their BIO MDX Series – Designed for high-throughput Bio fabrication and Precise 3D Bio printing. Current studies have demonstrated the use of Kaempferol-loaded bioactive glass-based scaffold for bone tissue engineering in in vitro and in vivo evaluation for the increasing prevalence of age related bone disorders.

Simultaneously, 3D bio printing technology is revolutionizing the way tissue constructs are produced. This technique allows for the precise layering of cells and biomaterials to create customized scaffolds that closely resemble the structure and function of natural tissues. By enabling the fabrication of patient-specific solutions, 3D bio printing addresses the variability in wound characteristics, thus optimizing healing. Additionally, the speed and efficiency of this technology facilitate rapid prototyping, reducing time-to-market for new wound care products.

Restraints

Complex Regulatory Pathways

The complex regulatory pathways in Europe are a significant restraint to the tissue engineering market for wound care. Tissue-engineered products must meet strict standards and obtain regulatory approvals from agencies such as the European Medicines Agency (EMA) or national authorities, which is time-consuming and costly.

These products often fall under the classification of Advanced Therapy Medicinal Products (ATMPs), requiring compliance with both pharmaceutical and medical device regulations. The dual nature of these products means they must meet stringent requirements for safety, efficacy, and quality. Regulations such as Medical Device Regulation (MDR) (EU) 2017/745 and, for the UK, the UK Medical Devices Regulations (UK MDR) 2002 oversee the regulatory requirements related to medical products and devices.

for instance, obtaining approval for a tissue-engineered skin substitute for wound healing involves clinical trials and extensive documentation on manufacturing processes, which can delay market entry. The rigorous approval process, combined with post-market surveillance, adds to the regulatory burden, especially for smaller companies lacking resources.

An example is Holoclar, a tissue-engineered product for eye treatment, which took over a decade to receive approval. Similar delays in wound care products prevent timely patient access to innovations. Additionally, navigating varied national regulations within the European Union complicates market access, contributing further to the restraining effect of regulatory pathways on the tissue engineering market for wound care in Europe.

Opportunities

Shift Towards Personalized Medicine

The shift towards personalized medicine is creating significant opportunities for advancing tissue engineering in Europe, particularly in the realm of wound care. Personalized medicine is based on the understanding that each patient has unique genetic profiles, physiological traits, and healthcare needs, which can influence treatment outcomes. In tissue engineering, this approach enables the development of customized solutions tailored to each patient’s specific biological, anatomical, and clinical parameters, making treatments more precise and effective.

Through advancements in genomics, biomaterials science, and regenerative medicine, personalized tissue engineering allows for the creation of tissue-engineered constructs that closely mimic the recipient’s native tissues. These constructs are designed to match the biological and biomechanical properties of the patient’s tissues, improving their integration into the body and reducing the risk of complications such as immune rejection. This level of customization enhances the safety and efficacy of tissue-engineered therapies, offering more reliable and long-term functional outcomes for patients.

In September 2023, Cutiss, a Swiss clinical-stage life sciences company, advanced the field of regenerative medicine and skin tissue engineering with its innovative therapies. The company’s flagship product, denovoSkin, is a personalized skin graft that can be bioengineered in large quantities using a small sample of healthy skin. This graft is designed to grow with the patient, minimize scarring, and reduce the need for follow-up corrective surgeries, particularly in pediatric patients.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors significantly influence the tissue engineering for wound care market. Economic growth, healthcare spending, and government funding for research and development play a crucial role in advancing tissue engineering technologies. In regions with strong economies and robust healthcare systems, such as North America and Europe, investment in innovative wound care solutions is higher, driving market growth.

Conversely, economic downturns or budget constraints can limit funding and slow adoption. Geopolitical factors, such as trade policies, tariffs, and international collaborations, also impact the market. for instance, trade tensions can disrupt the supply chain for critical materials, while favorable policies and partnerships can accelerate innovation and market expansion.

Additionally, regulatory environments and reimbursement policies vary across regions, affecting market accessibility. In emerging economies, geopolitical instability and limited healthcare infrastructure may hinder growth. Overall, the tissue engineering for wound care market is shaped by a complex interplay of economic and geopolitical dynamics, influencing research, production, and distribution.

Latest Trends

Growing Interest in Cellular Therapies

The growing interest in cellular therapies is a prominent trend in the Europe tissue engineering market for wound care. Cellular therapies involve the use of living cells to promote wound healing and tissue regeneration, offering advanced solutions for chronic and complex wounds such as diabetic ulcers, pressure sores, and burns. These therapies leverage the regenerative properties of various cell types, including stem cells, fibroblasts, and keratinocytes, to accelerate the repair of damaged tissues.

One key driver of this trend is the increasing prevalence of chronic wounds, particularly among the aging population and patients with conditions like diabetes. Traditional wound care methods often fall short in effectively managing such wounds, leading to a shift towards innovative approaches like cellular therapies, which promise faster healing and better outcomes.

In Europe, companies and research institutions are investing heavily in the development of cell-based treatments. for example, Cutiss AG is advancing bioengineered skin grafts using patient-derived cells to enhance wound healing. Similarly, collaborations between academic institutions and biotech firms are accelerating the development of autologous cell therapies, which use the patient’s own cells, reducing the risk of immune rejection.

Regional Analysis

North America is leading the Tissue Engineering for Wound Care Market

The North America Tissue Engineering for Wound Care Market is witnessing significant growth with 38.7% market share, driven by advancements in regenerative medicine and an increasing prevalence of chronic wounds, such as diabetic ulcers and pressure sores. The market benefits from technological innovations, including the development of bioengineered skin substitutes, growth factor-based therapies, and scaffolds that enhance wound healing.

The rising number of diabetic patients, coupled with the aging population, further fuels demand for effective wound care solutions. In the U.S. and Canada, regulatory support from agencies like the FDA for tissue-engineered products and growing awareness about advanced wound care are key factors propelling market growth.

The adoption of innovative solutions in both hospital and outpatient settings is expanding, with healthcare professionals seeking better alternatives to traditional wound care. Furthermore, the presence of leading players and increasing research investments in tissue engineering continue to drive the market’s expansion in the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the market include Integra LifeSciences Corporation, Organogenesis Inc., Mimetic Bio, Acelity (now part of 3M), Smith & Nephew, Prent Corporation, Advanced Tissue Sciences (acquired by Stryker), Wright Medical Group N.V. (acquired by Stryker), Molnlycke Health Care, Kerecis, Vericel Corporation, Collagen Matrix, Inc., SyntheMed, Inc. (now part of Allergan), Axolotl Biologix, Tissue Regenix Group PLC, and Others.

Integra LifeSciences Corporation specializes in dermal regeneration templates like Integra for chronic wound management, promoting tissue growth and healing through a scaffold-based approach. Organogenesis Inc. is also a key player which offers Apligraf, a living cell-based wound care product that supports tissue regeneration for chronic ulcers and burns. Kerecis is a key market player which focuses on fish-skin-based grafts, leveraging natural fish collagen to promote tissue regeneration and accelerate healing in chronic wounds.

Top Key Players

- Integra LifeSciences Corporation

- Organogenesis Inc.

- Mimetic Bio

- Acelity (now part of 3M)

- Smith & Nephew

- Prent Corporation

- Advanced Tissue Sciences (acquired by Stryker)

- Wright Medical Group N.V. (acquired by Stryker)

- Molnlycke Health Care

- Kerecis

- Vericel Corporation

- Collagen Matrix, Inc.

- SyntheMed, Inc. (now part of Allergan)

- Axolotl Biologix

- Tissue Regenix Group PLC

- Others

Recent Developments

- In July 2023, Smith+Nephew announced the launch of its REGENETEN Bioinductive Implant in India. With more than 100,000 procedures completed globally since its introduction, the REGENETEN implant has had a transformative impact on the way surgeons approach rotator cuff procedures.

- In October 2023, Smith+Nephew company announced the opening of the purpose-built Smith+Nephew Academy Munich, a new center for surgical innovation and training.

- In January 2023, Zimmer Biomet Holdings, Inc. announced that it had reached a definitive agreement to acquire Embody, Inc., a privately-held medical device company focused on soft tissue healing, for US$ 155 billion at closing and up to an additional US$ 120 billion subject to achieving future regulatory and commercial milestones over a three-year period.

- In July 2021, BD announced the acquisition of Tepha, Inc. It is one of a leading developer and manufacturer of a proprietary resorbable polymer technology. Tepha’s proprietary resorbable polymer (Poly 4-hydroxybutyric acid, P4HB) technology platform provides additional innovation potential that can accelerate the growth of BD’s surgical mesh portfolio and drives the company into potential new areas within soft tissue repair, reconstruction and regeneration.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 7.69 billion |

| Forecast Revenue (2034) | US$ 34.52 billion |

| CAGR (2024-2034) | 16.2% |

| Base Year for Estimation | 2024 |

| Historic Period | 2018-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, Market Dynamics, Soft Tissue Repair Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Material (Scaffold, Tissue Grafts (Synthetic Grafts, Allograft, Autograft, and Xenograft) and Other Products), By Material (Synthetic Material and Biologically Derived Material), By Type of Wound (Chronic Wounds (Diabetic Ulcers, Venous Ulcers, and Pressure Ulcers), Acute Wounds (Surgical Wounds, Traumatic Wounds, and Burn Care)), By Application (Skin Regeneration, Bone and Cartilage Regeneration, Soft Tissue Repair, Organ Regeneration), By End-User (Hospitals, Specialty Centers and Clinics, Ambulatory Surgical Centers) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Integra LifeSciences Corporation, Organogenesis Inc., Mimetic Bio, Acelity (now part of 3M), Smith & Nephew, Prent Corporation, Advanced Tissue Sciences (acquired by Stryker), Wright Medical Group N.V. (acquired by Stryker), Molnlycke Health Care, Kerecis, Vericel Corporation, Collagen Matrix, Inc., SyntheMed, Inc. (now part of Allergan), Axolotl Biologix, Tissue Regenix Group PLC, and Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |