Telecom Edge Data Platform Market By Component (Hardware (Edge Servers, Gateways, Routers, Storage Devices ), Software (Edge Management Software, Data Analytics Software), Services (Consulting Services, Integration and Deployment Services)), By Deployment Mode (On-Premises, Cloud-based), By Application (Network Optimization, Content Delivery, Internet Of Things (IoT) Management ), By End-User (Telecom Operators, Enterprises, Other End-Users), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2026-2035

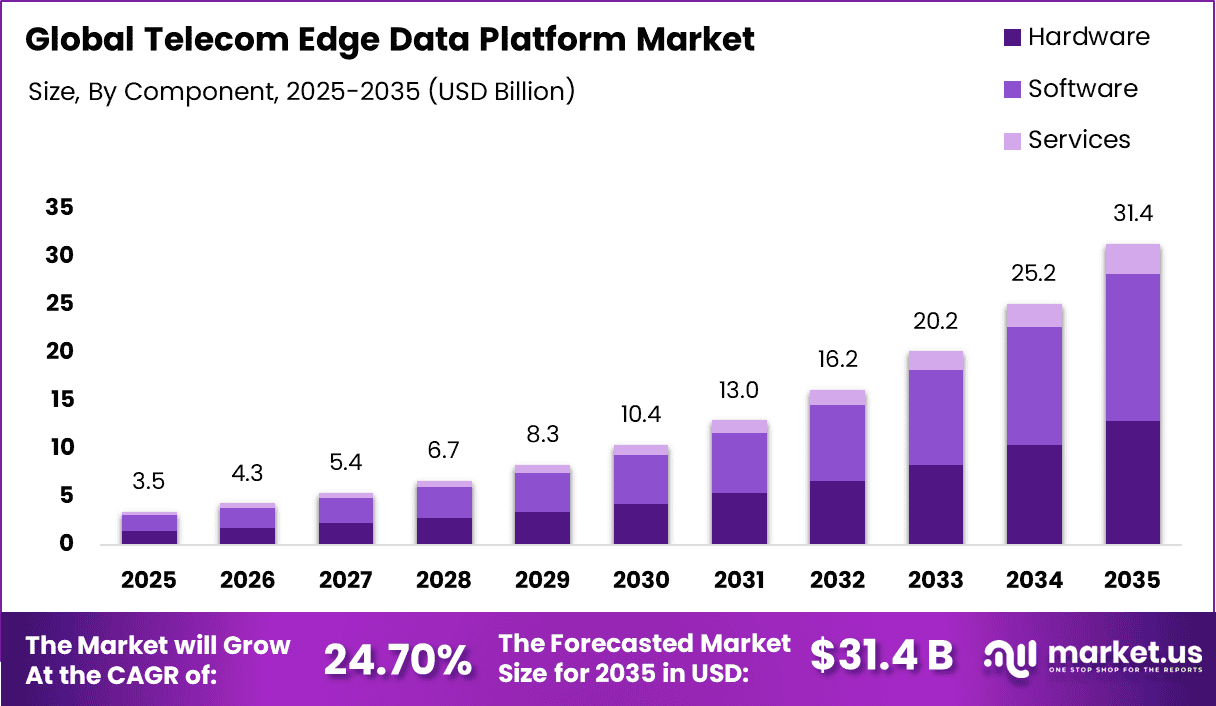

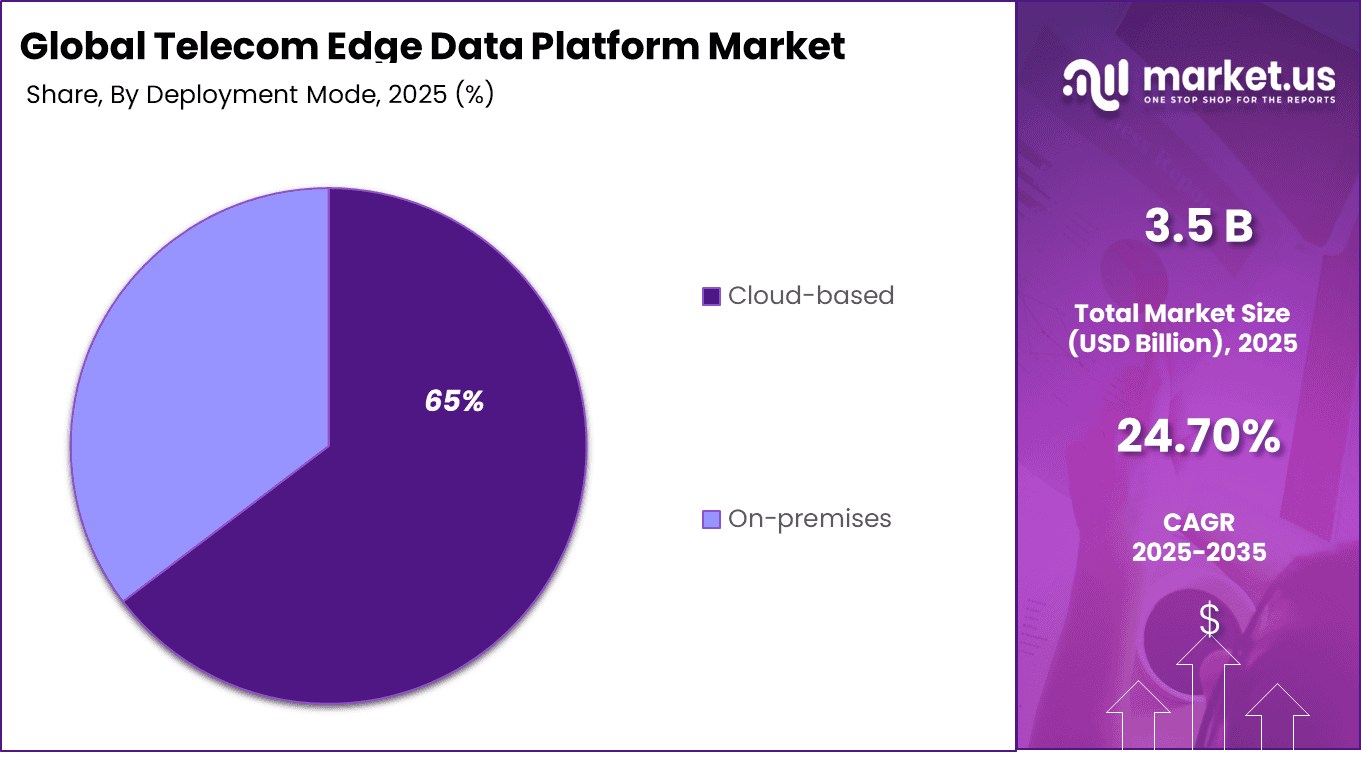

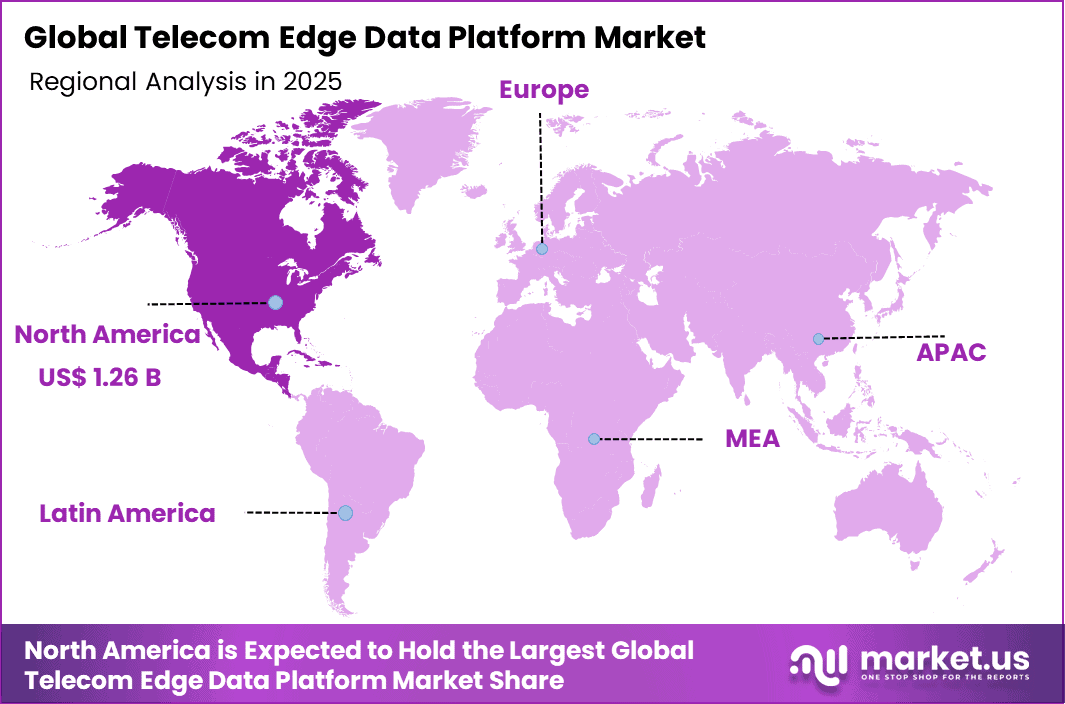

The Global Telecom Edge Data Platform Market generated USD 3.5 billion in 2025 and is predicted to register growth from USD 4.3 billion in 2026 to about USD 31.4 billion by 2035, recording a CAGR of 24.70% throughout the forecast span. In 2025, North America held a dominant market position, capturing more than a 36.8% share, holding USD 1.26 Billion revenue.

Top Market Takeaways

Hardware commands 41.3% market share, delivering edge servers, micro data centers, and distributed compute nodes optimized for telecom network integration.

Cloud-based deployment captures 64.7%, enabling elastic scaling, multi-tenant isolation, and seamless orchestration across RAN, core, and enterprise edge locations.

Content delivery applications claim 31.5%, powering video caching, AR/VR streaming, and dynamic ad insertion with sub-10ms latency guarantees.

Enterprises hold 30.2%, leveraging edge platforms for private 5G analytics, real-time IoT processing, and industry-specific MEC deployments.

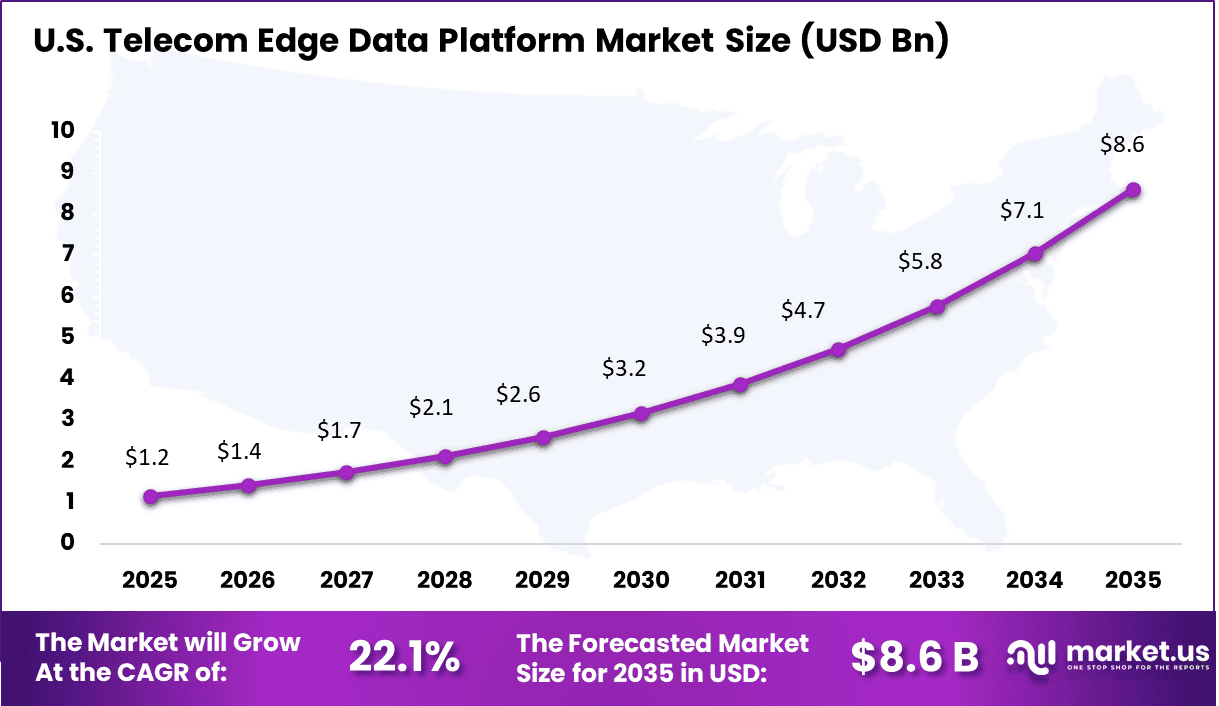

North America drives 36.8% global value, with U.S. market at USD 1.17 billion and 22.1% CAGR, fueled by Verizon/AWS edge partnerships and hyperscaler telco clouds.

Telecom Edge Data Platform market refers to software and data management platforms that collect, process, store, and analyze data closer to the telecom network edge instead of relying only on centralized data centers.

These platforms support edge based applications, network intelligence, local data handling, and faster service delivery across 5G and distributed telecom environments. The market is gaining importance as operators move workloads closer to end users and network sites to improve latency, bandwidth efficiency, and localized processing.

One of the main factors driving this market is the growing need for low latency data processing in telecom networks. Applications linked to real time analytics, connected devices, private wireless systems, and edge enabled services perform better when data is handled near the point where it is created or used.

Another important driver is the wider shift toward distributed telecom architecture, where operators want better control over network data, stronger operational visibility, and more efficient handling of workloads across multiple edge locations.

Demand for telecom edge data platforms is increasing among telecom operators, enterprise connectivity providers, and digital infrastructure users that need faster data handling and better support for edge enabled services.

These buyers want practical platforms that can support local analytics, application hosting, and network data management without sending every workload back to the core network. Demand is also rising because telecom systems are becoming more software driven, which makes edge data platforms more important for both operational efficiency and service development.

Drivers Impact Analysis

Key Driver

Impact on CAGR Forecast (~%)

Geographic Relevance

Impact Timeline

Implementation Significance

Rising deployment of 5G infrastructure

+4.2%

North America, Asia Pacific

Short to Mid Term

Enables ultra-low latency processing at network edge

Growth in real-time data processing demand

+3.6%

Global

Short Term

Supports applications like autonomous systems and IoT

Increasing adoption of edge computing in telecom networks

+3.9%

Global

Mid Term

Reduces bandwidth load and improves service efficiency

Expansion of IoT ecosystem across industries

+3.1%

Asia Pacific, Europe

Mid to Long Term

Drives need for distributed data platforms

Rising demand for content delivery optimization

+2.7%

North America, Europe

Short to Mid Term

Enhances streaming and low-latency services

Restraints Impact Analysis

Key Restraint

Impact on CAGR Forecast (~%)

Geographic Relevance

Impact Timeline

Limiting Factor Description

High infrastructure and deployment costs

-2.8%

Global

Short Term

Limits adoption among smaller telecom operators

Complexity in integration with legacy telecom systems

-2.4%

Europe, North America

Mid Term

Slows down deployment cycles

Data security and privacy concerns at edge locations

-2.1%

Global

Short to Mid Term

Increases compliance and operational burden

Lack of skilled workforce for edge platform management

-1.7%

Emerging Markets

Mid to Long Term

Restricts efficient implementation

Interoperability challenges across multi-vendor ecosystems

-1.5%

Global

Mid Term

Impacts scalability and flexibility

By Component Analysis

Hardware accounted for 41.3% of the Telecom Edge Data Platform Market. This segment leads because edge servers, processing units, and networking equipment are essential for handling data closer to the source. These components support low latency processing and enable real time data handling at the network edge.

The segment is also supported by the growing need for distributed computing infrastructure. Telecom operators invest in edge hardware to manage increasing data traffic and deliver faster services, which strengthens its role in edge platform deployments.

By Deployment Mode Analysis

Cloud based deployment held 65% of the market. This segment leads because cloud platforms provide scalable and flexible environments for managing edge data applications. It allows centralized control while supporting distributed edge nodes across different locations.

The segment is driven by increasing adoption of cloud native architectures. Organizations prefer cloud based edge platforms to simplify deployment, improve scalability, and integrate easily with existing digital infrastructure.

By Application Analysis

Content delivery represented 31.5% of the market. This segment dominates because edge platforms are widely used to deliver content such as video, media, and web services with reduced latency. Placing data closer to users improves loading speed and overall user experience.

The segment is supported by rising demand for high quality streaming and digital services. Telecom providers use edge platforms to optimize content delivery, reduce network congestion, and enhance service performance.

By End User Analysis

Enterprises accounted for 30.2% of the market. This segment leads because businesses increasingly rely on edge data platforms to process data locally and support real time applications. These platforms help improve operational efficiency and reduce latency in enterprise systems.

The segment is driven by digital transformation and increasing use of data intensive applications. Enterprises adopt edge platforms to enhance performance, improve decision making, and support advanced use cases across industries.

Investor Type Impact Analysis

Investor Type

Growth Sensitivity

Risk Exposure

Geographic Focus

Investment Outlook

Venture Capital Firms

High

High

North America, Asia

Focus on early-stage edge platform innovations

Private Equity Firms

Medium to High

Medium

Global

Invest in scalable telecom infrastructure assets

Strategic Telecom Players

High

Medium

Global

Long-term investments in network transformation

Sovereign Wealth Funds

Medium

Low to Medium

Middle East, Asia

Focus on national digital infrastructure expansion

Institutional Investors

Medium

Medium

North America, Europe

Stable returns from mature edge deployments

Technology Enablement Analysis

Technology Enabler

Impact on CAGR Forecast (~%)

Geographic Relevance

Impact Timeline

Implementation Significance

AI-driven network orchestration and automation

+3.4%

Global

Mid Term

Improves efficiency and predictive maintenance

Multi-access Edge Computing (MEC) frameworks

+3.8%

North America, Europe

Short to Mid Term

Enables localized data processing and faster response times

Cloud-native edge platform architectures

+3.2%

Global

Mid Term

Enhances scalability and flexibility

Network slicing in 5G environments

+2.9%

Asia Pacific, Europe

Mid to Long Term

Supports customized services for different use cases

Integration with distributed data analytics platforms

+2.6%

Global

Mid Term

Enables real-time insights and decision making

Key Challenges

Managing large volumes of data at distributed edge locations is a major challenge because telecom operators need fast processing, storage, and movement of data across many sites.

Integration with existing telecom networks and IT systems can be difficult because many operators still use older platforms, different vendors, and separate data environments.

Real time data processing is hard because edge platforms must support low latency services without delays, especially for time sensitive telecom applications.

Security and privacy remain major concerns because telecom edge data platforms handle sensitive network, user, and service related information across many endpoints.

Deployment and maintenance can be complex because operators need skilled teams, strong orchestration, and reliable infrastructure to manage edge platforms at scale.

Emerging Trends

A key trend in the Telecom Edge Data Platform market is the growing shift toward processing data closer to the network edge to support faster and more responsive services. Telecom operators are deploying edge platforms that collect, analyze, and act on data near the source rather than sending everything to centralized systems.

This approach helps reduce latency and supports applications that require immediate data handling. The trend reflects a move toward distributed data environments where edge locations play a central role in delivering real time insights and services.

Growth Factors

The increasing demand for low latency applications is supporting the growth of telecom edge data platforms. Services such as real time analytics, connected devices, and interactive digital experiences require faster data processing and minimal delays.

Edge platforms help telecom providers manage data efficiently while improving service performance. At the same time, the expansion of connected ecosystems encourages adoption of solutions that can handle large volumes of data closer to users, ensuring better responsiveness and overall network efficiency.

Key Market Segments

By Component

Hardware

Edge Servers

Gateways

Routers

Storage Devices

Networking Equipment

Software

Edge Management Software

Data Analytics Software

Virtualization Software

Security Software

Network Monitoring Software

Services

Consulting Services

Integration and Deployment Services

Support and Maintenance Services

Managed Services

Training Services

By Deployment Mode

On-Premises

Cloud-based

By Application

Network Optimization

Content Delivery

Internet Of Things (IoT) Management

Security

Other Applications

By End-User

Telecom Operators

Enterprises

Cloud Service Providers

Other End-Users

Regional Analysis

North America accounted for 36.8% of the Telecom Edge Data Platform Market, reflecting strong adoption of edge computing solutions across telecom networks. Service providers across the region increasingly deploy edge data platforms to process data closer to the source, reduce latency, and support real time applications. The expansion of 5G networks, rising data traffic, and growing demand for low latency services continue to drive the need for advanced edge data platforms across North America.

The U.S. generated about USD 1.17 Billion within the regional market and is projected to expand at a CAGR of 22.1%. Telecom operators and enterprises across the country continue to invest in edge infrastructure to support applications such as streaming, IoT, and smart city services.

Telecom edge data platforms help improve network efficiency, enable faster data processing, and support scalable service delivery. As demand for real time digital services increases, adoption of edge data platforms continues to grow rapidly across the US market.

Key Regions and Countries

North America

US

Canada

Europe

Germany

France

The UK

Spain

Italy

Russia

Netherlands

Rest of Europe

Asia Pacific

China

Japan

South Korea

India

Australia

Singapore

Thailand

Vietnam

Rest of APAC

Latin America

Brazil

Mexico

Rest of Latin America

Middle East & Africa

South Africa

Saudi Arabia

UAE

Rest of MEA

Competitive Analysis

The competitive landscape of the Telecom Edge Data Platform market includes telecom infrastructure providers, server manufacturers, and enterprise technology companies that support edge computing close to network endpoints.

Huawei Technologies Co. Ltd., Dell Technologies Inc., IBM Corporation, Cisco Systems Inc., Lenovo Group Limited, Intel Corporation, Schneider Electric SE, Hewlett Packard Enterprise Company, Fujitsu Limited, Telefonaktiebolaget LM Ericsson, Nokia Corporation, and ZTE Corporation hold strong positions because they offer hardware, software, and network solutions that help telecom operators process data faster and improve low latency services.

Other players such as American Tower Corporation, Super Micro Computer Inc., Equinix Inc., Mavenir Systems Inc., Cologix Inc., Radisys Corporation, Scale Computing Inc., Saguna Networks Ltd., and Nife Labs Inc. add competition through colocation support, edge platform software, distributed computing systems, and telecom focused deployment models. The market is shaped by platform scalability, processing efficiency, integration with 5G networks, and the ability to support real time applications across distributed edge environments.

The future outlook for the Telecom Edge Data Platform Market looks strong as telecom operators continue to move computing and data processing closer to users and network sites. ETSI describes multi access edge computing as a way to bring cloud capabilities into the telecom network, while Ericsson highlights benefits such as lower latency, better bandwidth use, local data handling, and support for real time applications over 5G. As operators expand edge services for video, industrial automation, private networks, and AI driven workloads, demand for telecom edge data platforms is expected to grow steadily in the coming years.

Recent Developments

March, 2026 – Huawei OceanConnect adds AI edge for 5G factories with 1ms latency and deploys 1M sites in China. Cuts energy 30% and leads Asia with HarmonyOS IoT fusion. Partners SAIC for auto edge and exports to Middle East.

February, 2026 – Dell PowerEdge XR servers boost telecom MEC with NVIDIA Grace and partners AT&T for US edge. Handles 100Gbps per rack with NVMe-oF storage included. Adds liquid cooling for dense AI workloads.

Report Scope

Report Features

Description

Market Value (2025)

USD 3.5 Billion

Forecast Revenue (2035)

USD 31.4 Billion

CAGR(2025-2035)

24.70%

Base Year for Estimation

2024

Historic Period

2020-2024

Forecast Period

2026-2035

Report Coverage

Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends

Segments Covered

By Component (Hardware (Edge Servers, Gateways, Routers, Storage Devices ), Software (Edge Management Software, Data Analytics Software), Services (Consulting Services, Integration and Deployment Services)), By Deployment Mode (On-Premises, Cloud-based), By Application (Network Optimization, Content Delivery, Internet Of Things (IoT) Management ), By End-User (Telecom Operators, Enterprises, Other End-Users)

Regional Analysis

North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA

Competitive Landscape

Huawei Technologies Co. Ltd., Dell Technologies Inc., IBM Corporation, Cisco Systems Inc., Lenovo Group Limited, Intel Corporation, Schneider Electric SE, Hewlett Packard Enterprise Company, Fujitsu Limited, Telefonaktiebolaget LM Ericsson, Nokia Corporation, ZTE Corporation, American Tower Corporation, Super Micro Computer Inc., Equinix Inc., Mavenir Systems Inc., Cologix Inc., Radisys Corporation, Scale Computing Inc., Saguna Networks Ltd., Nife Labs Inc., Others

Customization Scope

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements.

Purchase Options

We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)