Global Tallow Balm Market Size, Share, Growth Analysis By Type (Essential Oil-Infused, Unscented Balm, Baby-Safe Balm, Herbal Blend, Medicinal Grade, Vegan Alternatives), By Application (Skincare, Eczema Treatment, Diaper Rash, Lip Balm, Tattoo Aftercare, Hand Cream), By Distribution Channel (Hypermarkets/Supermarkets, Wellness and Health & Beauty Stores, Online Retail Stores, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 182459

- Number of Pages: 240

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

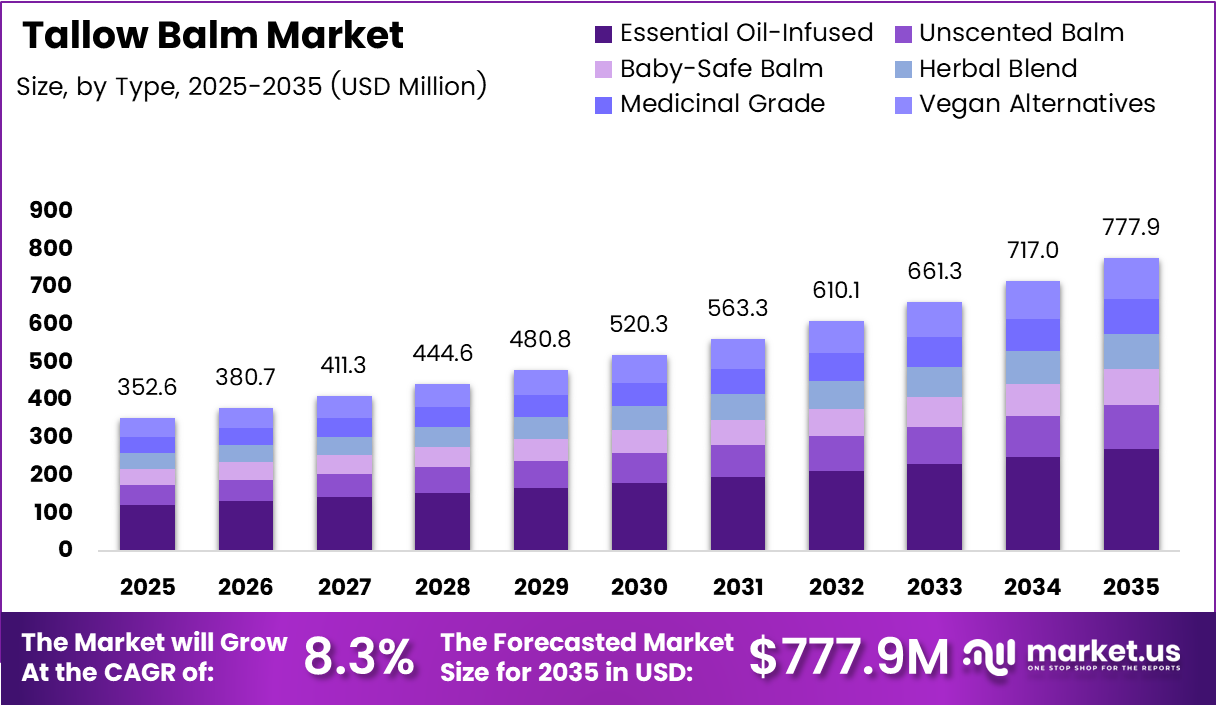

Global Tallow Balm Market size is expected to be worth around USD 777.9 Million by 2035 from USD 352.6 Million in 2025, growing at a CAGR of 8.3% during the forecast period 2026 to 2035.

Tallow balm is a skin-nourishing product made from rendered animal fat, primarily sourced from grass-fed beef. Formulators use it as a base for moisturizers, barrier creams, and lip balms. The product appeals to consumers seeking chemical-free, ancestral skincare alternatives with a concentrated nutrient profile.

Consumer demand for clean-label personal care products has shifted purchasing behavior away from synthetic moisturizers. Health-conscious buyers now actively seek products with traceable, single-origin ingredients. Tallow balm sits at the intersection of this behavioral shift and the ancestral wellness movement, giving the market a structurally different demand base than conventional cosmetics.

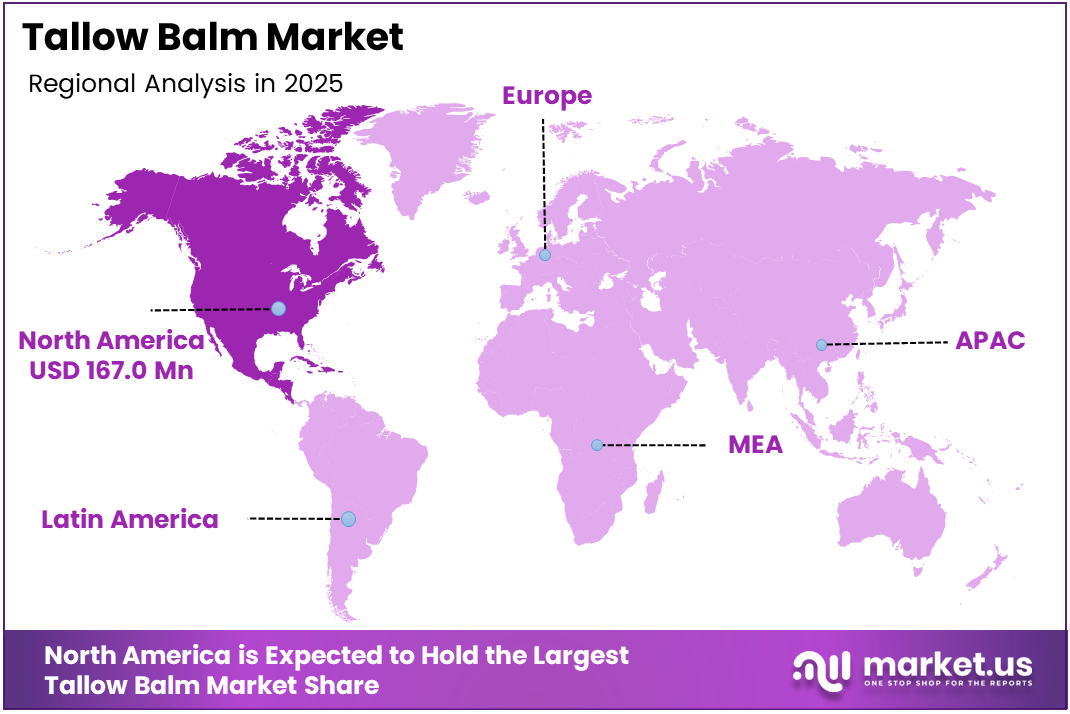

North America leads this market, holding 47.4% share valued at USD 167.0 Million. This dominance reflects the region’s early adoption of paleo-inspired wellness routines and a dense network of direct-to-consumer artisanal brands. The infrastructure for small-batch, farm-sourced skincare exists more fully in North America than in any other region.

Skincare applications account for the largest share within this market, with eczema treatment, diaper rash care, and tattoo aftercare forming distinct high-value niches. These specialized use cases reduce price sensitivity among buyers, allowing premium pricing and repeat purchase cycles that support sustainable revenue for producers. In June 2024, Milk & Honey Tallow Company launched its line of high-end beef tallow skincare products using 100% grass-fed beef tallow and organic botanicals, reflecting the entry of structured brands into a previously fragmented space.

According to a 2026 technical guide by beeftallow.ie, grass-fed tallow carries a fatty acid profile of approximately 50–55% saturated fats and 40–50% monounsaturated fats, closely mimicking human sebum. This biochemical compatibility is not a marketing claim — it is a structural advantage that explains why consumers with sensitive or eczema-prone skin report faster absorption and fewer reactions than with water-based creams.

According to beeftallow.ie’s 2026 technical guide, a single jar of quality beef tallow balm lasts 3–6 months with daily use, outperforming commercial moisturizers that contain mostly water and fillers. This cost-per-use advantage matters because it converts first-time buyers into loyal repeat customers, tightening retention economics for brands operating in this space.

Key Takeaways

- The global Tallow Balm Market was valued at USD 352.6 Million in 2025 and is forecast to reach USD 777.9 Million by 2035.

- The market advances at a CAGR of 8.3% over the forecast period 2026 to 2035.

- By Type, Essential Oil-Infused balms lead with a 31.6% share, reflecting buyer preference for enhanced sensory and therapeutic profiles.

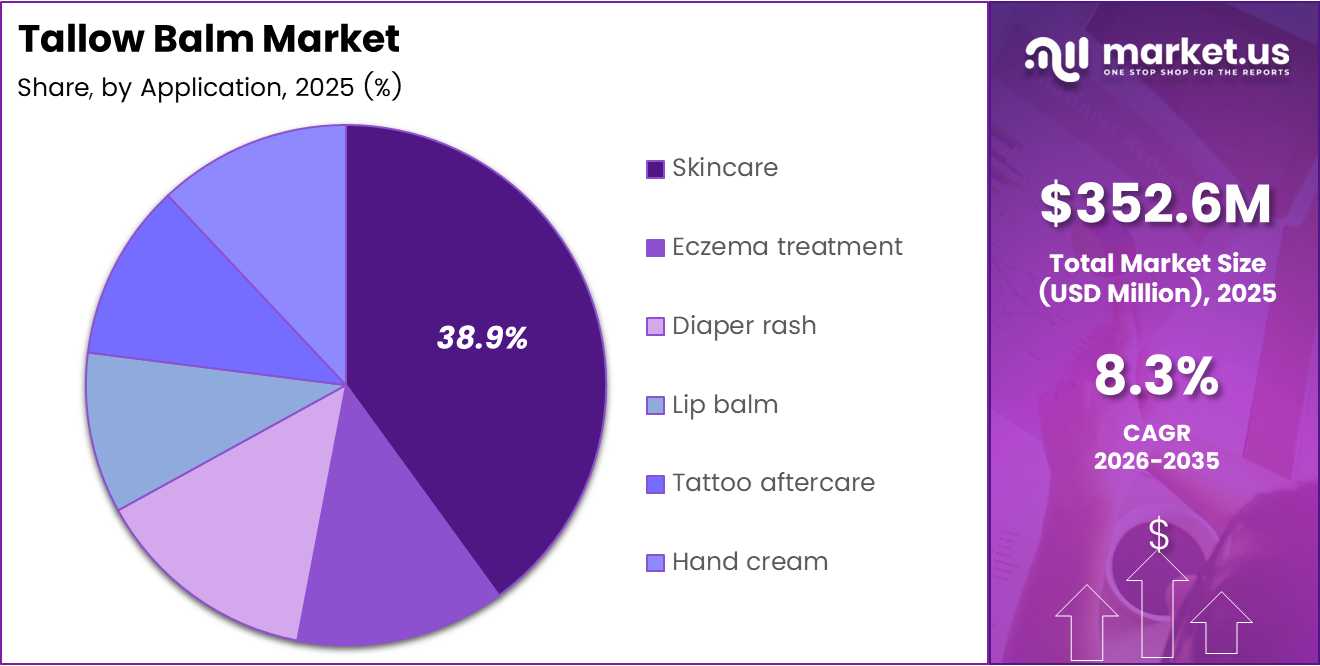

- By Application, Skincare holds the dominant position with a 38.9% share across the application segment.

- By Distribution Channel, Wellness and Health & Beauty Stores capture 34.1% share, indicating strong offline retail engagement for this category.

- North America dominates with 47.4% market share, valued at USD 167.0 Million, driven by mature direct-to-consumer artisanal brand networks.

Product Analysis

Essential Oil-Infused Balm dominates with 31.6% due to added therapeutic and sensory differentiation.

In 2025, Essential Oil-Infused balm held a dominant market position in the By Type segment of the Tallow Balm Market, with a 31.6% share. Consumers pay a meaningful premium for botanical infusions because essential oils signal a clear product story — lavender for calming, tea tree for antimicrobial action — allowing brands to command higher price points than plain tallow alternatives.

Unscented Balm serves buyers with fragrance sensitivity, allergies, or clinical skin conditions. This sub-segment captures consumers who cannot tolerate essential oils but still seek animal-fat-based nourishment. Additionally, dermatologists and pediatricians increasingly recommend unscented formulations for reactive skin, creating a referral-driven demand channel that strengthens repeat purchase rates.

Baby-Safe Balm differentiates through strict ingredient exclusions — no synthetic fragrances, no preservatives, and no petroleum derivatives. Parents purchasing for infants apply significantly higher scrutiny to ingredient lists than general skincare buyers. Consequently, this sub-segment supports a trust-based premium and benefits from peer-to-peer parenting community recommendations rather than conventional advertising.

Herbal Blend balms carry the highest formulation complexity within this type segment. Producers combine tallow with calendula, comfrey, or plantain to target wound care and inflammation relief. This positions herbal blends closer to medicinal product territory, attracting a buyer who cross-shops between skincare and natural remedies and expects clinical credibility in product claims.

Medicinal Grade tallow balm targets therapeutic outcomes rather than cosmetic ones. Formulators using low-temperature rendering and pharmaceutical-grade sourcing can justify higher retail prices and pursue wellness clinic distribution. However, this sub-segment requires producers to meet more rigorous quality and labeling standards, raising the barrier to entry for smaller artisanal operations.

Vegan Alternatives within this type category represent a structural contradiction — tallow-free formulations marketed alongside tallow-based products under a shared brand umbrella. Brands introduce these to retain customers who began questioning animal-derived ingredients. Moreover, this sub-segment signals that producers are hedging against long-term consumer sentiment shifts without abandoning their core grass-fed positioning.

Application Analysis

Skincare dominates with 38.9% due to broad daily-use relevance across demographics.

In 2025, Skincare held a dominant market position in the By Application segment of the Tallow Balm Market, with a 38.9% share. Daily moisturizing is the most frequent skincare behavior globally, and tallow balm’s sebum-compatible fatty acid profile makes it a technically credible substitute for synthetic creams, particularly among consumers already engaged with ancestral wellness practices.

Eczema treatment applications attract buyers with chronic, recurring skin conditions who have exhausted conventional options. These consumers demonstrate above-average willingness to pay and unusually high brand loyalty once a product delivers relief. Additionally, eczema-focused product lines allow brands to build medically adjacent positioning without requiring pharmaceutical certification.

Diaper rash applications target one of the most safety-scrutinized purchase categories in personal care. Parents selecting tallow-based diaper balms actively reject petroleum jelly and zinc oxide alternatives in favor of perceived natural purity. This creates a highly defensible niche where ingredient transparency and grass-fed sourcing become primary purchase criteria rather than price.

Lip balm formulations using tallow represent a high-margin, high-frequency repurchase category. Consumers replace lip products far more often than body moisturizers, improving revenue velocity per customer. Moreover, lip balm acts as a low-risk entry product for first-time tallow buyers, functioning as a trial vehicle that converts users toward higher-ticket full-size skincare purchases.

Tattoo aftercare is a precision application where tallow balm competes directly with petroleum-based products on ingredient quality grounds. Tattoo artists and studios increasingly recommend clean, fragrance-free balms to reduce irritation risk during skin healing. Consequently, word-of-mouth from professional artists within tattoo communities creates a trusted referral channel that traditional advertising cannot replicate.

Hand cream applications expand tallow balm’s reach into everyday occupational skincare. Tradespeople, agricultural workers, and healthcare professionals who experience frequent hand washing or chemical exposure represent a volume-driven segment. However, hand cream buyers typically prioritize absorption speed and scent neutrality, requiring manufacturers to adjust formulation viscosity away from traditional firm-set balm textures.

Distribution Channel Analysis

Wellness and Health & Beauty Stores dominate with 34.1% due to curated natural product positioning and trust signaling.

In 2025, Wellness and Health & Beauty Stores held a dominant market position in the By Distribution Channel segment of the Tallow Balm Market, with a 34.1% share. These retail environments attract buyers who treat skincare as part of a broader wellness regimen. Physical placement alongside supplements, organic foods, and clean beauty products creates category association that drives trial purchases among high-intent shoppers.

Hypermarkets and Supermarkets introduce tallow balm to mainstream consumers who do not specifically seek out specialty wellness retail. Mass retail placement increases brand visibility and transaction volume but compresses margins. Additionally, shelf placement alongside conventional moisturizers forces tallow brands to communicate ingredient differentiation rapidly, placing higher demands on packaging and on-label messaging clarity.

Online Retail Stores carry the highest strategic importance for artisanal tallow balm producers who lack the scale to negotiate mass retail listings. E-commerce removes geographic distribution barriers and allows direct brand storytelling through product pages, ingredient sourcing narratives, and customer reviews. Furthermore, online channels support subscription models and bundle purchasing, which improve lifetime customer value metrics for small-batch manufacturers.

Others — including farm direct sales, farmers markets, wellness clinics, and pop-up retail — represent a meaningful segment for brands at the earliest growth stage. These channels allow producers to build personal relationships with buyers and gather real-time product feedback. Moreover, direct selling through farm stands reinforces the grass-fed, farm-sourced narrative that forms the core identity of premium tallow balm brands.

Key Market Segments

By Type

- Essential Oil-Infused

- Unscented Balm

- Baby-Safe Balm

- Herbal Blend

- Medicinal Grade

- Vegan Alternatives

By Application

- Skincare

- Eczema treatment

- Diaper rash

- Lip balm

- Tattoo aftercare

- Hand cream

By Distribution Channel

- Hypermarkets / Supermarkets

- Wellness and Health & Beauty Stores

- Online Retail Stores

- Others

Drivers

Fat-Soluble Vitamins in Grass-Fed Tallow and Chemical-Free Demand Drive Tallow Balm Adoption

Consumers with sensitive and allergy-prone skin actively seek moisturizers free of synthetic preservatives, silicones, and petrochemicals. Grass-fed tallow delivers this through a naturally occurring fat-soluble vitamin complex. According to beeftallow.ie’s 2026 technical guide, low-temperature wet rendering preserves vitamins A, D, E, and K — nutrients destroyed by industrial high-heat processing methods used in mass-market cosmetics manufacturing.

This biochemical advantage matters to buyers because vitamins A and D support cellular repair, while E and K address inflammation and scarring. Consumers with eczema or post-procedure skin are not purchasing balm for fragrance — they are seeking functional healing. This shifts the competitive frame from cosmetics toward therapeutic skincare, allowing tallow balm producers to command clinical-grade pricing without a pharmaceutical license.

The ancestral and paleo wellness movement accelerates this pattern further. Health-conscious buyers trust animal-based ingredients that ancestors used for centuries over petroleum-derived alternatives developed in the twentieth century. In June 2025, SVEDA launched its tallow-based skincare line featuring Whipped Tallow Balm, Hydrating Tallow Balm, and Tallow Lip Balm — all made with grass-fed beef tallow and clean botanicals — signaling that structured brands now see commercial viability in positioning tallow as a mainstream premium ingredient.

Restraints

Vegan Opposition and Premium Sourcing Costs Constrain Tallow Balm’s Commercial Scale

A meaningful share of the personal care consumer base refuses animal-derived cosmetic ingredients on ethical grounds. Vegan and cruelty-free certifications have become purchase filters for a growing buyer segment, particularly in Western Europe and urban North American markets. Tallow balm, by definition, cannot earn these certifications, closing off a significant retail channel and limiting shelf placement in mainstream beauty retail environments.

Supply constraints compound this challenge at the production level. According to tuscaloosanews.com (January 2026, manufacturer expert statement from Sego Lily Skincare), kidney suet — the premium sourcing base for high-quality tallow balm — costs approximately six times more than lower-grade trim fat. This cost differential forces producers to choose between quality and margin, a trade-off that complicates scaling beyond small-batch operations.

Limited large-scale commercial infrastructure for grass-fed tallow sourcing means producers face unpredictable supply volumes. A brand that sells out quickly loses buyer momentum and risks customer churn to synthetic alternatives. Consequently, the inability to reliably forecast raw material availability acts as a ceiling on revenue growth for producers who have successfully built demand through social media and direct-to-consumer channels.

Growth Factors

Product Innovation, DTC Expansion, and Cross-Border E-Commerce Open New Revenue Channels

Infusing tallow balm with herbal extracts and essential oils allows producers to create clearly differentiated product lines targeting specific conditions — calendula for wound healing, lavender for sleep-support skincare, tea tree for antimicrobial action. According to tuscaloosanews.com (January 2026, Sego Lily Skincare), kidney suet yields only 12 pounds per animal versus over 100 pounds of trim fat, making premium-sourced tallow genuinely scarce — and scarcity supports the artisanal pricing that infused product lines require.

Direct-to-consumer channels give small-batch producers access to buyers without retailer margin extraction. Brands building subscription models around tallow balm convert one-time buyers into predictable revenue contributors. In May 2025, Milk & Honey Tallow Company was selected as a third-place winner in the Funded By LIY women-entrepreneur support program, demonstrating that institutional recognition is now flowing toward tallow brands with differentiated positioning and community-driven growth strategies.

Cross-border e-commerce opens the market to consumers in Asia Pacific and Europe who cannot access artisanal tallow balm through local retail. International buyers discovering tallow skincare through social media platforms actively seek out North American brands, creating export revenue without physical distribution investment. Additionally, holistic skincare clinics adopting tallow-based products provide professional endorsement that accelerates consumer trust and conversion in new geographies.

Emerging Trends

Social Media Virality and Multi-Purpose Formulations Reshape the Tallow Balm Competitive Landscape

Natural beauty influencers on platforms such as TikTok and Instagram have turned tallow skincare routines into viral content categories. A single influencer demonstration can drive product sell-outs within hours — a distribution dynamic that no conventional advertising budget can replicate. This viral pathway gives small artisanal brands the same reach as established beauty corporations, fundamentally altering how new entrants compete for shelf share.

Manufacturers now formulate tallow balms to serve skin, lips, baby care, and tattoo healing within a single product. According to a March 2026 technical press release from Sego Lily Skincare (news-journalonline.com), micro-aerated tallow formulations require minimal product for significant surface coverage and are far more economical than traditional balm due to effortless spreadability and full product volume. This formulation advance makes multi-purpose products genuinely practical for daily use, removing a key consumer friction point.

Grass-fed and regenerative farm sourcing is shifting from a niche claim to an expected standard among premium buyers. Consumers now read sourcing disclosures as closely as ingredient lists. Simultaneously, sustainable packaging and zero-waste branding — glass jars, compostable labels, refill programs — signal brand values alignment to buyers who treat purchasing decisions as personal ethics statements. Brands that do not adopt these practices face credibility erosion with their core demographic.

Regional Analysis

North America Dominates the Tallow Balm Market with a Market Share of 47.4%, Valued at USD 167.0 Million

North America holds 47.4% of the global tallow balm market, valued at USD 167.0 Million. The region’s leadership reflects early consumer adoption of ancestral wellness practices, a dense ecosystem of direct-to-consumer artisanal brands, and strong social media-driven product discovery. The US market in particular hosts the highest concentration of grass-fed cattle farms that supply premium raw material to tallow balm producers.

Europe Tallow Balm Market Trends

Europe demonstrates measurable consumer interest in traditional animal-fat skincare, particularly in Germany and the UK where clean beauty movements overlap with ancestral health communities. However, stricter EU cosmetics regulations require more rigorous safety documentation for animal-derived ingredients. This regulatory friction slows market entry for smaller artisanal producers who lack compliance resources, concentrating share among established brands with legal infrastructure.

Asia Pacific Tallow Balm Market Trends

Asia Pacific represents the highest long-term growth potential for tallow balm, driven by expanding middle-class spending on premium personal care and rising social media exposure to Western wellness trends. China, Japan, and South Korea have established clean beauty consumer bases that actively seek imported natural skincare. Cross-border e-commerce platforms reduce the distribution barrier for North American tallow brands entering this region.

Middle East and Africa Tallow Balm Market Trends

The Middle East and Africa market for tallow balm remains nascent, constrained by cultural preferences that favor plant-based and non-animal cosmetic formulations in several key markets. However, South Africa shows stronger alignment with Western natural skincare trends and provides a viable entry point for brands testing regional expansion. Premium wellness retail in GCC countries serves expatriate consumer bases already familiar with tallow-based products.

Latin America Tallow Balm Market Trends

Latin America’s tallow balm market benefits from Brazil and Mexico’s established cattle industries, which create natural raw material sourcing proximity. Consumer awareness of premium tallow skincare remains low but is building through social media channels. Additionally, local artisanal producers in Brazil are beginning to adapt traditional beef fat-based skincare practices into branded commercial products that align with the global clean beauty narrative.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Primally Pure occupies a premium positioning within the tallow balm space by centering its brand narrative around biodynamic, farm-sourced ingredients and rigorous clean beauty standards. The company leverages a loyal online community and robust content marketing to sustain high customer lifetime value without relying on traditional retail placement. This direct relationship with buyers insulates the brand from retailer margin pressure and price competition.

Lady May Tallow builds competitive advantage through handcrafted small-batch production and transparent sourcing communication. The brand targets buyers who treat ingredient provenance as a purchase requirement, not a preference. By maintaining visible farm-to-jar traceability, Lady May creates a trust premium that synthetic skincare brands structurally cannot replicate, allowing it to sustain price points well above mass-market moisturizer equivalents.

Ancestral Cosmetics positions its product range at the intersection of functional skincare and ancestral nutrition philosophy. The brand speaks directly to paleo and carnivore lifestyle communities, using language and benefit claims that resonate with buyers already familiar with grass-fed, nutrient-dense food sourcing. This community alignment generates organic word-of-mouth referrals and reduces customer acquisition costs relative to conventional beauty brand spending.

Summer Solace Tallow LLC differentiates through product specialization, targeting eczema-prone and sensitive-skin consumers with clinically framed benefit communication. By focusing on a narrow therapeutic use case rather than general moisturizing, the brand reduces direct competition with mass-market products and builds credibility among buyers who have experienced repeated failures with synthetic dermatological creams. This positioning supports premium pricing and repeat purchase loyalty.

Key Players

- Primally Pure

- Lady May Tallow

- Ancestral Cosmetics

- Summer Solace Tallow LLC

- Hello Selah

- Tallow Balm Company

- The Tallow Company

- Hearth and Homestead

- Vintage Tradition

- Darlin’ Skincare

Recent Developments

- October 2025 — McBee Farms launched its 100% Grass-Fed Tallow Collection, including Whipped Tallow Face Cream, Whipped Tallow Baby Balm, Whipped Tallow Baby Butter, and 100% Grass-Fed Cooking Tallow. All products are handcrafted on the farm with no fillers or additives, reinforcing farm-direct quality positioning.

- October 2025 — Aterian, Inc. (Nasdaq: ATER) launched a full Tallow Skin Care line under its Healing Solutions® brand, featuring beef tallow-based scented and unscented whipped balms and salves. The formulation uses 100% grass-fed, grass-finished suet tallow blended with manuka honey, organic jojoba seed oil, and organic beeswax, marking a publicly traded company’s entry into the tallow skincare segment.

- December 2025 — Lords Love Butter announced the launch of its new Whipped Tallow Balm designed for family skincare. The product centers on a nutrient-dense, chemical-free formulation specifically intended to promote skin barrier health across all age groups, including infants.

Report Scope

Report Features Description Market Value (2025) USD 352.6 Million Forecast Revenue (2035) USD 777.9 Million CAGR (2026-2035) 8.3% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Essential Oil-Infused, Unscented Balm, Baby-Safe Balm, Herbal Blend, Medicinal Grade, Vegan Alternatives), By Application (Skincare: Eczema treatment, Diaper rash, Lip balm, Tattoo aftercare, Hand cream), By Distribution Channel (Hypermarkets/Supermarkets, Wellness and Health & Beauty Stores, Online Retail Stores, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Primally Pure, Lady May Tallow, Ancestral Cosmetics, Summer Solace Tallow LLC, Hello Selah, Tallow Balm Company, The Tallow Company, Hearth and Homestead, Vintage Tradition, Darlin’ Skincare Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Primally Pure

- Lady May Tallow

- Ancestral Cosmetics

- Summer Solace Tallow LLC

- Hello Selah

- Tallow Balm Company

- The Tallow Company

- Hearth and Homestead

- Vintage Tradition

- Darlin' Skincare

Our Clients

- 182459

- Mar 2026