Quick Navigation

Report Overview

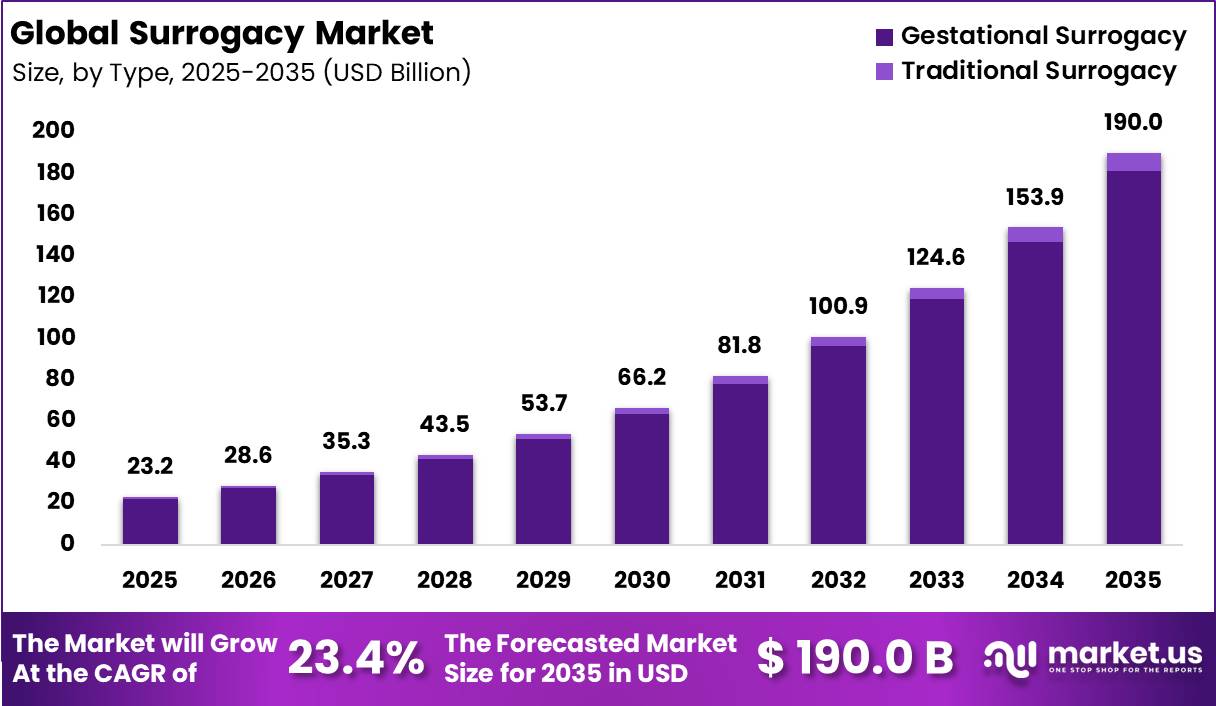

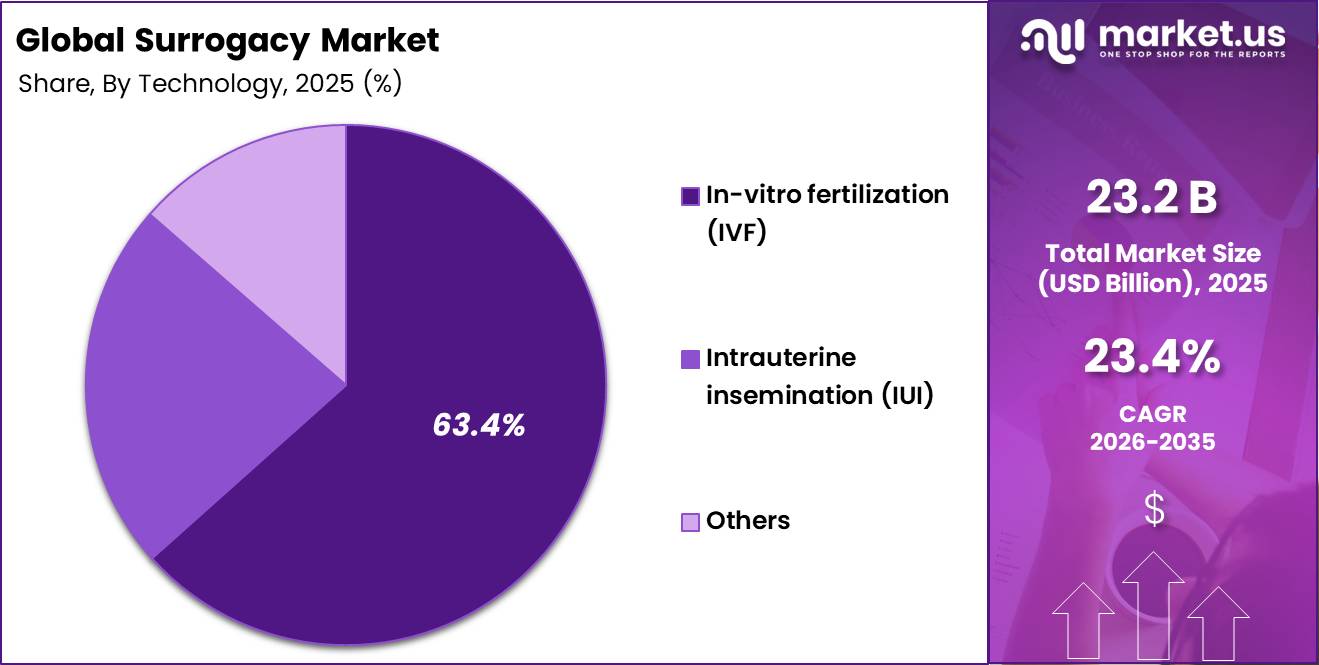

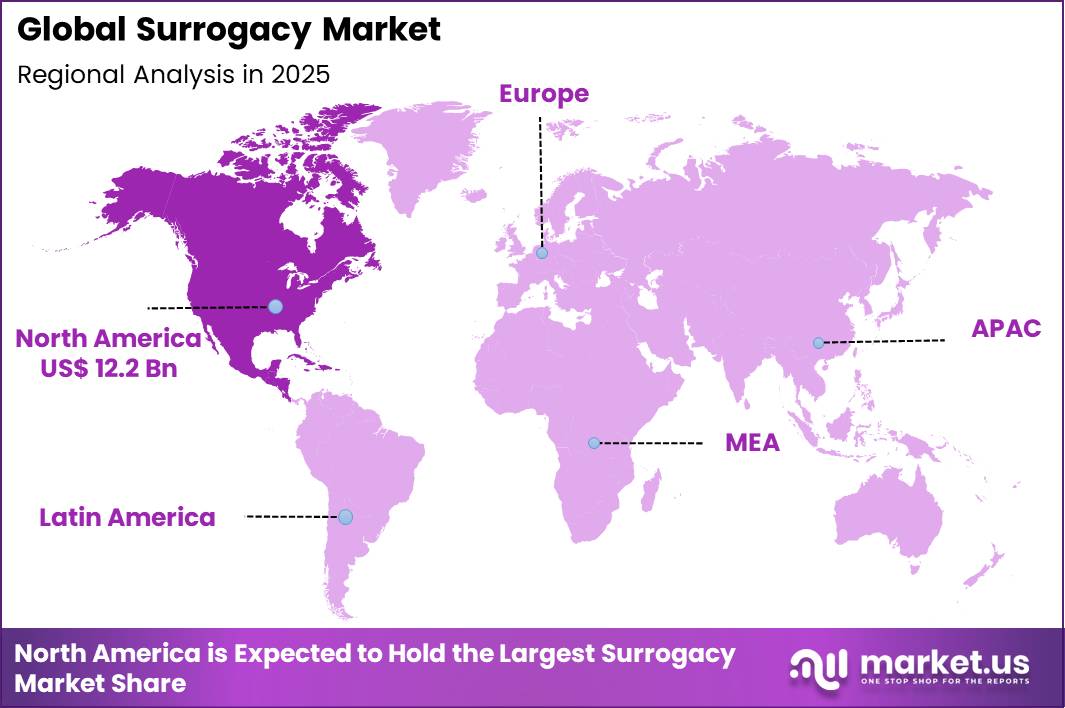

Global Surrogacy Market size is expected to be worth around US$ 190.0 Billion by 2035 from US$ 23.2 Billion in 2025, growing at a CAGR of 23.4% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 52.6% share with a revenue of US$ 12.2 Billion.

The surrogacy market is experiencing substantial growth due to the increasing prevalence of infertility, rising adoption of assisted reproductive technologies (ART), and growing social acceptance of alternative family-building methods. Surrogacy is an arrangement in which a woman carries and delivers a child for another individual or couple who are unable to conceive naturally or carry a pregnancy to term.

The market has emerged as a significant segment within the fertility healthcare industry, supported by technological advancements in in-vitro fertilization (IVF), embryo transfer procedures, and fertility preservation services.

The growing incidence of infertility remains a major factor driving market demand. According to the World Health Organization (WHO), around 17.5% of the global adult population, or nearly 1 in 6 individuals worldwide, experience infertility during their lifetime. The WHO further noted that infertility affects approximately 48 million couples and 186 million individuals globally.

In addition, the Centers for Disease Control and Prevention (CDC) reported that about 8.5% of married women aged 15–49 years in the United States experience infertility, while nearly 13.4% face impaired fecundity, meaning difficulty in getting or staying pregnant.

Rising maternal age and lifestyle-related disorders are also contributing significantly to fertility challenges. According to the American Society for Reproductive Medicine (ASRM), female fertility begins to decline gradually after the age of 30 and more rapidly after 35 years.

Furthermore, obesity, stress, smoking, excessive alcohol consumption, diabetes, and polycystic ovary syndrome (PCOS) are increasingly linked with infertility worldwide. The Office on Women’s Health, U.S. Department of Health & Human Services estimates that PCOS affects between 6% and 12% of women of reproductive age in the United States, equivalent to as many as 5 million women.

The demand for surrogacy services is also increasing due to changing family structures, including growing acceptance of same-sex couples, single-parent families, and delayed parenthood. Advancements in ART procedures have improved pregnancy success rates and treatment accessibility.

According to the Society for Assisted Reproductive Technology (SART), more than 413,000 ART cycles were performed in the United States in 2021, resulting in over 97,000 live births. These technological and demographic trends, combined with increasing investments in digital fertility platforms and reproductive healthcare services, are expected to support the continued expansion of the global surrogacy market over the coming years.

Key Takeaways

- Market Size: Global Surrogacy Market size is expected to be worth around US$ 190.0 Billion by 2035 from US$ 23.2 Billion in 2025.

- Market Share: The market growing at a CAGR of 23.4% during the forecast period from 2026 to 2035.

- Type Analysis: The gestational surrogacy segment dominated the global surrogacy market in 2025, accounting for 95.5% of the total market share.

- Technology Analysis: The in-vitro fertilization (IVF) segment held the largest share of the global surrogacy market in 2025, accounting for 63.4% of the overall market revenue.

- Age Group Analysis: The below 35 years segment dominated the global surrogacy market in 2025, accounting for 76.8% of the total market share.

- Service Provider Analysis: The surrogacy agencies segment accounted for the largest share of the global surrogacy market in 2025, representing 45.8% of the total market revenue.

- Regional Analysis: In 2025, North America led the market, achieving over 52.6% share with a revenue of US$ 12.2 Billion.

Type Analysis

The gestational surrogacy segment dominated the global surrogacy market in 2025, accounting for 95.5% of the total market share. The dominance of this segment is primarily attributed to the increasing preference for medically advanced and legally accepted surrogacy procedures across major countries. In gestational surrogacy, the surrogate mother has no genetic connection with the child, which reduces legal complexities and improves acceptance among intended parents.

The growing adoption of assisted reproductive technologies (ART), rising infertility rates, delayed pregnancies, and increasing awareness regarding fertility treatment options have further accelerated segment growth. Fertility clinics and healthcare providers are increasingly recommending gestational surrogacy due to its higher success rates and improved clinical outcomes. Additionally, favorable legal frameworks in countries permitting commercial or altruistic surrogacy continue to support market expansion.

The traditional surrogacy segment represents a comparatively smaller share of the market. In this method, the surrogate mother is biologically related to the child, which often creates legal, emotional, and ethical concerns. As a result, the adoption of traditional surrogacy remains limited in several developed and regulated healthcare markets.

Technology Analysis

The in-vitro fertilization (IVF) segment held the largest share of the global surrogacy market in 2025, accounting for 63.4% of the overall market revenue. The segment dominance is driven by the increasing utilization of IVF procedures in gestational surrogacy arrangements due to their higher implantation success rates and greater reproductive control.

IVF enables fertilization outside the human body, allowing embryos to be genetically screened before implantation, thereby improving pregnancy outcomes and reducing genetic abnormalities. The growing prevalence of infertility, rising maternal age, increasing same-sex parenthood, and advancements in embryo freezing and genetic testing technologies are significantly supporting segment growth.

Furthermore, the increasing availability of specialized fertility clinics and supportive reimbursement policies in certain countries continue to strengthen the adoption of IVF procedures globally.

The intrauterine insemination (IUI) segment is expected to witness moderate growth during the forecast period. IUI is primarily associated with traditional surrogacy arrangements and is considered a comparatively less invasive and lower-cost fertility treatment option. However, its lower success rates compared to IVF and limited applicability in gestational surrogacy procedures restrict wider market penetration across advanced fertility treatment centers.

Age Group Analysis

The below 35 years segment dominated the global surrogacy market in 2025, accounting for 76.8% of the total market share. The dominance of this segment is primarily attributed to the higher fertility rates, improved ovarian reserve, and greater success rates associated with pregnancies among women under the age of 35 years.

Healthcare providers and fertility specialists generally recommend younger surrogate mothers due to lower pregnancy-related complications and better maternal health outcomes. In addition, higher embryo implantation success rates and reduced risks of chromosomal abnormalities contribute significantly to the growth of this segment. Increasing awareness regarding fertility preservation and rising adoption of assisted reproductive technologies among younger intended parents are further supporting market demand.

The 35–37 years and 38–39 years segments continue to account for a considerable market share owing to growing delayed parenthood trends globally. Meanwhile, the 40–42 years and 43–44 years age groups are witnessing gradual demand due to advancements in fertility treatment technologies. The over 44 years segment remains comparatively limited because of declining fertility rates, higher pregnancy risks, and lower success probabilities associated with advanced maternal age.

Service Provider Analysis

The surrogacy agencies segment accounted for the largest share of the global surrogacy market in 2025, representing 45.8% of the total market revenue. The segment growth is driven by the increasing reliance on specialized agencies for comprehensive surrogacy coordination services, including surrogate matching, legal documentation, psychological counseling, medical scheduling, and financial management.

Surrogacy agencies simplify the overall process for intended parents by offering integrated support throughout the surrogacy journey. The growing international demand for fertility services and increasing cross-border surrogacy arrangements are further contributing to segment expansion. Additionally, agencies often collaborate with fertility clinics, legal experts, and healthcare institutions, improving operational efficiency and treatment accessibility.

The fertility clinics segment also represents a substantial market share due to the rising number of IVF procedures and fertility treatment cycles globally. Legal and counseling services are gaining importance as regulatory compliance and emotional support become essential aspects of surrogacy arrangements. Hospitals continue to play a supportive role by providing maternity and neonatal care services. The others segment includes independent consultants and support organizations contributing to the broader surrogacy ecosystem.

Key Market Segments

By Type

- Traditional Surrogacy

- Gestational Surrogacy

By Technology

- Intrauterine insemination (IUI)

- In-vitro fertilization (IVF)

- Others

By Age Group

- Below 35 years

- 35-37 years

- 38 – 39 years

- 40-42 years

- 43-44 years

- Over 44 years

By Service Provider

- Surrogacy Agencies

- Fertility Clinics

- Legal and Counseling Services

- Hospitals

- Others

Driving Factors

The increasing prevalence of infertility and delayed parenthood is a major driver of the surrogacy market globally. According to the World Health Organization (WHO), approximately one in six people worldwide experience infertility during their reproductive years. Rising cases of polycystic ovary syndrome (PCOS), obesity, stress-related reproductive disorders, and late-age pregnancies have significantly increased the demand for assisted reproductive technologies (ART), including surrogacy.

In addition, social acceptance of fertility treatments and expanding awareness regarding reproductive healthcare are supporting market growth. The Centers for Disease Control and Prevention (CDC) reported that more than 435,000 ART cycles were conducted in the United States in 2022, resulting in over 98,000 infants born.

Furthermore, nearly 90% of fertility clinics in the U.S. offered gestational carrier services. Increasing medical success rates in IVF procedures and embryo transfer technologies are also improving confidence among intended parents. These factors collectively contribute to the growing adoption of surrogacy services across developed and emerging economies.

Trending Factors

A significant trend observed in the surrogacy market is the growing shift toward gestational surrogacy supported by advanced reproductive technologies and stricter regulatory frameworks. Gestational surrogacy, where the surrogate has no genetic connection with the child, has become increasingly preferred due to lower legal and emotional complexities.

According to the CDC ART database, fertility clinics are increasingly adopting embryo freezing, donor egg programs, and genetic screening procedures to improve pregnancy outcomes. Another notable trend is the implementation of government regulations to ensure ethical surrogacy practices. India introduced the Surrogacy (Regulation) Act, 2021 to prohibit commercial surrogacy and regulate ART clinics.

Governments are also emphasizing registration and compliance mechanisms for fertility centers. In addition, fertility preservation methods such as egg freezing are gaining popularity among women delaying pregnancies for professional or personal reasons. Technological advancements in embryo selection and cryopreservation are expected to improve live birth rates and treatment efficiency, further strengthening the adoption of regulated surrogacy procedures globally.

Restraining Factors

Strict regulatory policies, ethical concerns, and the high cost of fertility procedures remain major restraints for the surrogacy market. Several countries have imposed limitations or complete bans on commercial surrogacy due to concerns regarding exploitation of surrogate mothers, child trafficking, and legal disputes over parental rights.

India’s Surrogacy (Regulation) Act, 2021 permits only altruistic surrogacy and prohibits commercial arrangements, significantly impacting the availability of surrogate services. Additionally, surrogacy procedures involve substantial financial costs associated with IVF cycles, medical screenings, embryo transfers, legal documentation, and pregnancy care.

According to healthcare reports referenced by WHO, fertility treatments remain unaffordable for a large portion of the global population, especially in low- and middle-income countries. Emotional stress, multiple failed IVF attempts, and medical complications further limit treatment adoption.

Moreover, varying legal standards across countries create uncertainty for intended parents pursuing cross-border surrogacy. Ethical debates surrounding reproductive rights and commercialization of childbirth continue to influence policymaking and public opinion, thereby restricting the broader expansion of the global surrogacy industry.

Opportunity

The expansion of fertility healthcare infrastructure and increasing government focus on reproductive health present significant opportunities for the surrogacy market. Many countries are improving access to fertility treatments through healthcare reforms, awareness campaigns, and advancements in assisted reproductive technologies.

According to the WHO infertility platform, infertility affects an estimated 42–180 million people globally, highlighting substantial unmet demand for reproductive care services. Emerging economies in Asia-Pacific and Latin America are witnessing rising investments in fertility clinics, IVF laboratories, and reproductive medicine research.

Technological innovations such as genetic testing, artificial intelligence-based embryo selection, and cryopreservation are expected to improve success rates and reduce procedural risks. Furthermore, increasing acceptance of non-traditional family structures, including single parents and same-sex couples in several countries, is creating additional demand for surrogacy services.

Legal reforms supporting reproductive rights and transparent clinical practices are also expected to encourage market expansion. As healthcare accessibility improves and treatment outcomes become more reliable, the surrogacy market is anticipated to experience sustained long-term growth opportunities globally.

Regional Analysis

In 2025, North America dominated the global surrogacy market, accounting for over 52.6% of the total market share and generating revenue of approximately US$ 12.2 billion. The regional market growth is primarily driven by the increasing prevalence of infertility, growing acceptance of assisted reproductive technologies (ART), and favorable legal frameworks supporting gestational surrogacy across several U.S. states and Canada.

The presence of advanced healthcare infrastructure, high healthcare expenditure, and strong accessibility to fertility clinics has further strengthened the market position in the region. In addition, rising awareness regarding fertility preservation and delayed parenthood among working professionals has significantly increased demand for surrogacy services.

The United States represents the largest contributor within North America due to the availability of technologically advanced fertility treatments and the growing participation of single parents and same-sex couples seeking parenthood solutions.

Furthermore, supportive insurance coverage and the presence of established surrogacy agencies continue to enhance market expansion. Canada is also witnessing steady growth owing to favorable regulations and increasing medical tourism for reproductive procedures. Moreover, ongoing technological advancements in in-vitro fertilization (IVF) and embryo screening are expected to support long-term market development across North America during the forecast period.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

The surrogacy market is characterized by the presence of specialized fertility clinics, reproductive healthcare providers, and surrogacy agencies focusing on expanding their service portfolios and improving success rates through advanced reproductive technologies.

Key market participants are actively investing in in-vitro fertilization (IVF), genetic screening technologies, and patient-centric fertility solutions to strengthen their competitive position. Strategic collaborations with fertility centers, legal advisory firms, and international healthcare providers are also being adopted to enhance global outreach and service accessibility.

Major companies are increasingly emphasizing personalized fertility treatments, transparent legal procedures, and comprehensive surrogate support programs to attract intended parents. In addition, rising cross-border reproductive tourism has encouraged leading players to expand operations in countries with favorable surrogacy regulations and lower treatment costs.

Technological advancements in embryo transfer procedures and fertility preservation are further supporting market competitiveness. Moreover, increasing demand from same-sex couples, single parents, and delayed pregnancies continues to create growth opportunities for established and emerging market participants globally.

Market Key Players

- Circle Surrogacy

- Growing Generations

- ConceiveAbilities

- Extraordinary Conceptions

- The Surrogacy Group

- Surrogate Solutions

- Northwest Surrogacy Center

- Simple Surrogacy

- Joy of Life Surrogacy

- American Surrogacy

- New Life Global

- Surrogate Parenting Services

- EggDonors4All

- Reproductive Possibilities

- Bright Futures Surrogacy

- EKSPLA

- Vibronix Inc.

- Others

Recent Developments

- April 2025 – NewGenIVF Group Limited secured strategic funding of approximately USD 5.2 million to strengthen its international expansion strategy. The investment is expected to support the establishment of a new fertility clinic in Dubai, while also enhancing the company’s broader reproductive healthcare and surrogacy-related service network across international markets.

- 2025 – Growing Generations continued strengthening its premium surrogacy platform by expanding personalized donor and surrogate matching services. The company highlighted continued investment in high-quality surrogate recruitment and advanced family-building support programs, reinforcing its position in the North American surrogacy market.

- 2025 – ConceiveAbilities reported continued operational expansion driven by rising demand for assisted reproduction and surrogacy services. The company emphasized investments in surrogate support programs, referral partnerships, and enhanced patient engagement initiatives to strengthen its nationwide presence.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 23.2 Billion |

| Forecast Revenue (2035) | US$ 190.0 Billion |

| CAGR (2026-2035) | 23.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Traditional Surrogacy, Gestational Surrogacy) By Technology (Intrauterine insemination (IUI), In-vitro fertilization (IVF), Others) By Age Group (Below 35 years, 35-37 years, 38 – 39 years, 40-42 years, 43-44 years, Over 44 years) By Service Provider (Surrogacy Agencies, Fertility Clinics, Legal and Counseling Services, Hospitals, Others) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Circle Surrogacy, Growing Generations, ConceiveAbilities, Extraordinary Conceptions, The Surrogacy Group, Surrogate Solutions, Northwest Surrogacy Center, Simple Surrogacy, Joy of Life Surrogacy, American Surrogacy, New Life Global, Surrogate Parenting Services, EggDonors4All, Reproductive Possibilities, Bright Futures Surrogacy, EKSPLA, Vibronix Inc., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |