Global Special Mission Aircraft Market Size, Share, Growth Analysis By Platform (Fixed Wing, Rotary Wing, Unmanned Aerial Vehicle (UAV), Hybrid/Other Platforms), By Application (Intelligence, Surveillance and Reconnaissance (ISR), Maritime Patrol and Anti-Submarine Warfare (ASW), Electronic Warfare (EW) and Signals Intelligence (SIGINT), Airborne Early Warning & Control (AEW&C), Emergency Services), By End User (Defense and Homeland Security/Law Enforcement, Commercial and Civil), By Point of Sale (OEM, Aftermarket), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Apr 2026

- Report ID: 184048

- Number of Pages: 252

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

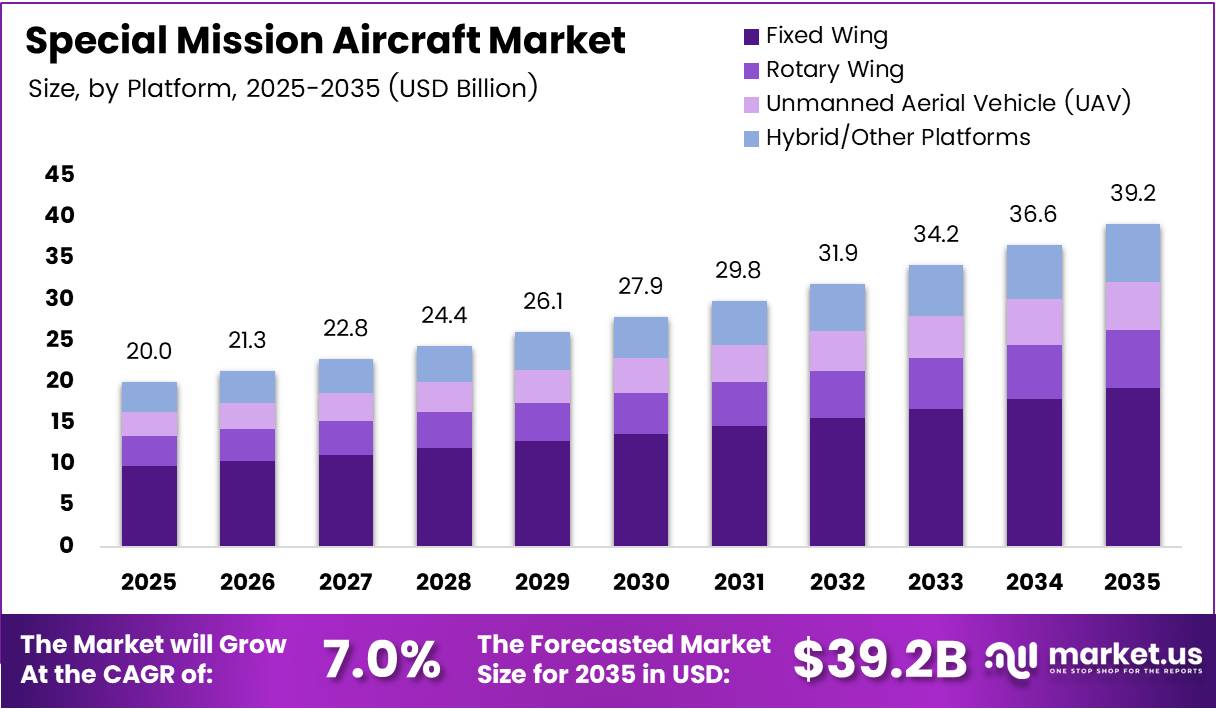

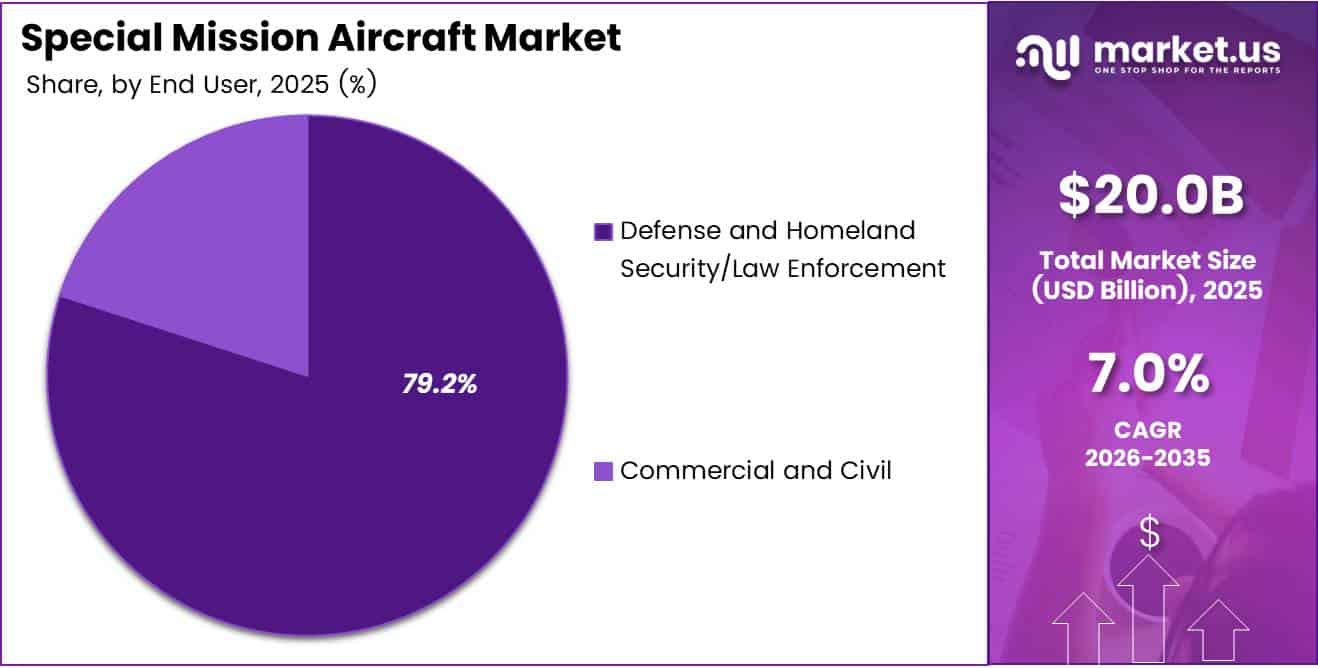

Global Special Mission Aircraft Market size is expected to be worth around USD 39.2 Billion by 2035 from USD 20.0 Billion in 2025, growing at a CAGR of 7.0% during the forecast period 2026 to 2035.

Special mission aircraft are purpose-built or converted platforms designed to perform specific operational roles beyond standard transport or combat functions. These include intelligence gathering, maritime surveillance, airborne early warning, electronic warfare, and emergency medical response. Defense agencies and civil operators rely on these aircraft to extend operational reach where ground-based systems cannot.

The market spans a broad range of platform types — from large fixed-wing jets to rotary-wing helicopters and unmanned aerial vehicles. Each platform type serves distinct mission profiles. Fixed-wing aircraft dominate long-range surveillance and patrol roles, while UAVs are displacing manned platforms in sustained endurance missions where crew safety and cost are primary concerns.

Defense procurement budgets remain the primary demand engine. Governments across North America, Europe, and Asia-Pacific are expanding airborne ISR fleets in response to evolving security threats, contested maritime zones, and intelligence gaps that satellite systems alone cannot fill. This structural budget commitment underpins the 7.0% CAGR forecast through 2035.

The P-8A Poseidon illustrates how sustained investment translates into operational scale. The global P-8A fleet has accumulated more than 450,000 collective mishap-free flight hours across worldwide operations by 2025. This reliability record directly influences procurement decisions — defense buyers treat proven airframe longevity as a risk-reduction metric when committing to multi-decade programs.

Connectivity upgrades are also reshaping the economics of special mission operations. According to Viasat, adoption of Ka-band SATCOM for ISR on special mission turboprops enables approximately a 5% reduction in annual flying hours, saving about $2.49 million per year for an operator flying 20,000 hours at $2,490 per hour. This means operators no longer face a binary choice between capability and cost — modern sensor and communications upgrades actively compress total operational expense.

The P-8A Poseidon further demonstrates that performance is not capped by platform age. The aircraft can fly up to 41,000 ft and reach its area of interest at speeds up to 490 knots — faster than other long-range patrol aircraft. This speed advantage reduces transit time, increases sortie rates, and directly improves mission effectiveness in time-sensitive maritime and border patrol scenarios.

Together, these factors confirm that the special mission aircraft market is not purely a volume play. It rewards vendors who deliver platform reliability, lifecycle cost efficiency, and mission system integration — capabilities that take years to demonstrate and that create durable competitive positions once established.

Key Takeaways

- The Special Mission Aircraft Market was valued at USD 20.0 Billion in 2025 and is forecast to reach USD 39.2 Billion by 2035.

- The market advances at a CAGR of 7.0% during the forecast period 2026 to 2035.

- By Platform, Fixed Wing leads with a 48.6% share in 2025.

- By Application, Intelligence, Surveillance and Reconnaissance (ISR) holds the largest share at 39.1%.

- By End User, Defense and Homeland Security/Law Enforcement accounts for 79.2% of demand.

- By Point of Sale, OEM commands a 69.4% share, reflecting strong original equipment procurement activity.

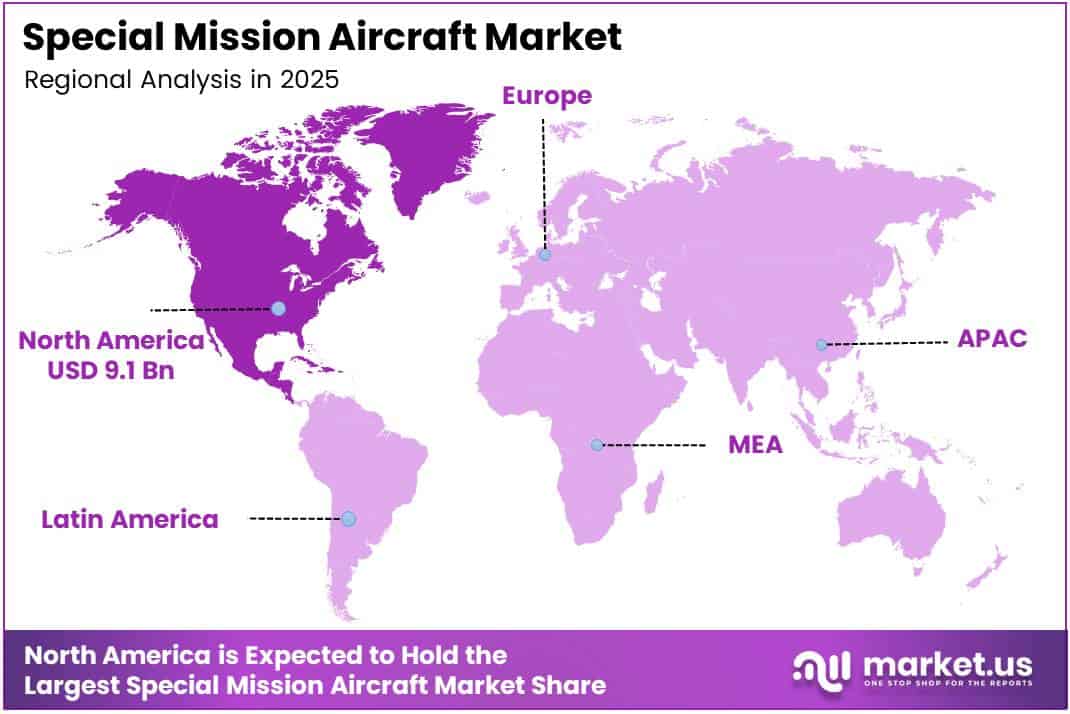

- North America leads all regions with a 45.80% share, valued at USD 9.1 Billion.

Product Analysis

Fixed Wing dominates with 48.6% due to unmatched long-range endurance and payload capacity.

In 2025, Fixed Wing held a dominant market position in the By Platform segment of the Special Mission Aircraft Market, with a 48.6% share. Fixed-wing platforms sustain longer flight times, carry heavier sensor suites, and cover greater distances than alternatives — attributes that make them the default choice for ISR, maritime patrol, and AEW&C missions. The Bombardier Global 6500 exemplifies this: it achieves a fleet dispatch reliability of 99.83% with maintenance intervals up to 750 flight hours or 30 months, while offering over 18 hours endurance and 6,600 nm range in special mission configuration — performance levels that rotary-wing and UAV platforms cannot match for long-range tasking.

Rotary Wing fills the tactical gap where fixed-wing platforms cannot operate. Helicopters provide vertical take-off capability, low-altitude hover for search and rescue, and access to unprepared landing zones — requirements common in medevac, disaster response, and coastal patrol roles. Their shorter range and lower payload compared to fixed-wing aircraft limit their ISR utility, but their operational flexibility sustains demand in emergency services and law enforcement segments.

Unmanned Aerial Vehicles (UAVs) are the highest-growth platform category in this market. The MQ-9A Block 5 Extended Range variant, delivered to the U.S. Marine Corps in 2025, achieves up to 34 hours endurance — an increase from approximately 27 hours on earlier configurations. This endurance advantage enables UAVs to replace manned aircraft on high-risk, long-duration ISR and surveillance missions, reducing crew exposure while lowering per-sortie operating costs.

Hybrid/Other Platforms represent an early-stage but strategically significant segment. These include tilt-rotor and hybrid-electric configurations being developed for niche roles where neither fixed-wing nor rotary-wing platforms are optimal. Procurement volumes remain limited today, but program investments by major defense contractors signal that buyers are preparing for a post-conventional platform mix in the next decade.

Application Analysis

ISR dominates with 39.1% due to persistent multi-domain intelligence collection requirements.

In 2025, Intelligence, Surveillance and Reconnaissance (ISR) held a dominant market position in the By Application segment of the Special Mission Aircraft Market, with a 39.1% share. No other application generates a comparable volume of dedicated platform procurement. ISR aircraft operate continuously across land, sea, and near-space domains — and defense buyers treat ISR capacity as a non-discretionary budget line. The HADES (High Accuracy Detection and Exploitation System) ISR aircraft program, awarded to Sierra Nevada Corporation in August 2024 under an IDIQ contract initially valued at approximately $93.5 million and potentially up to $994.3 million, confirms that defense agencies are actively expanding ISR fleets using purpose-converted business jets.

Maritime Patrol and Anti-Submarine Warfare (ASW) serves as the second-largest application category and the one most directly tied to great-power competition dynamics. Contested maritime zones in the Indo-Pacific and North Atlantic are pushing navies to modernize patrol fleets. The Dassault Falcon 2000LXS Albatros offers approximately 7 hours on-station endurance at 200 nautical miles from base — more than double that of the Falcon 50M it replaces — illustrating the performance step-change defense buyers now expect in new maritime patrol acquisitions.

Electronic Warfare (EW) and Signals Intelligence (SIGINT) platforms collect, analyze, and disrupt adversary electronic emissions. Demand for this capability has increased alongside the proliferation of advanced radar, communication, and missile guidance systems among peer competitors. These aircraft typically require dense, power-hungry sensor payloads — a constraint that limits viable airframe options to large business jets and purpose-built military platforms.

Airborne Early Warning and Control (AEW&C) aircraft extend radar coverage beyond the horizon, giving commanders real-time air battle management at scale. This application directly justifies high-value, long-cycle procurement programs. The Boeing E-7 AEW&C provides more than 4 million square kilometers of radar coverage per standard mission, with durations exceeding 10 hours — extendable through aerial refueling — making it the reference benchmark for new AEW&C competitions globally.

Emergency Services — encompassing medevac, disaster management, search and rescue, and related civil roles — represents the primary non-defense demand segment. These operations depend on aircraft that combine medical equipment capacity, communications systems, and rapid deployment capability. Growth in this sub-segment tracks government investment in civil aviation infrastructure and disaster preparedness budgets, not defense cycles.

End-User Analysis

Defense and Homeland Security/Law Enforcement dominates with 79.2% due to sovereign security procurement mandates.

In 2025, Defense and Homeland Security/Law Enforcement held a dominant market position in the By End-User segment of the Special Mission Aircraft Market, with a 79.2% share. Military and law enforcement agencies are the principal buyers because special mission aircraft provide capabilities — persistent surveillance, battle management, anti-submarine warfare — that have no civilian equivalent. Procurement decisions in this segment run on multi-year budget cycles with long contract durations, creating stable, predictable revenue for prime contractors and system integrators alike.

Commercial and Civil buyers account for the remaining share, operating special mission aircraft for roles including environmental monitoring, maritime boundary enforcement, border surveillance, and humanitarian logistics. This segment grows as governments outsource certain surveillance functions to commercial operators and as climate-related mandates push agencies to deploy airborne monitoring platforms. While smaller in current volume, commercial and civil demand represents the fastest-expanding end-user base over the forecast horizon.

Point of Sale Analysis

OEM dominates with 69.4% due to integrated mission system procurement requirements.

In 2025, OEM held a dominant market position in the By Point of Sale segment of the Special Mission Aircraft Market, with a 69.4% share. Defense buyers typically procure special mission aircraft as complete, mission-ready systems — airframe, sensors, communications, and data links integrated and qualified together. This bundled procurement preference concentrates spend at the OEM level and limits aftermarket penetration during active program phases.

Aftermarket activity generates recurring revenue through maintenance, upgrade, and mission system modernization contracts. As fleets mature and original OEM support windows close, operators shift spend toward third-party MRO providers and system integrators. L3Harris, for example, had delivered 103 missionized business jets for ISR and other special missions by mid-2025 — demonstrating that significant revenue flows through conversion and integration work outside the original OEM transaction.

Key Market Segments

By Platform

- Fixed Wing

- Rotary Wing

- Unmanned Aerial Vehicle (UAV)

- Hybrid/Other Platforms

By Application

- Intelligence, Surveillance and Reconnaissance (ISR)

- Maritime Patrol and Anti-Submarine Warfare (ASW)

- Electronic Warfare (EW) and Signals Intelligence (SIGINT)

- Airborne Early Warning & Control (AEW&C)

- Emergency Services (Medevac, Disaster Management, Search and Rescue, etc.)

By End User

- Defense and Homeland Security/Law Enforcement

- Commercial and Civil

By Point of Sale

- OEM

- Aftermarket

Drivers

Expanding ISR and Maritime Patrol Mandates Drive Multi-Domain Fleet Investment

Defense ministries worldwide are increasing airborne surveillance budgets in response to contested maritime zones, intelligence gaps, and border security pressures that ground-based systems cannot address. ISR aircraft generate decision-quality intelligence at operational scale — a function that no satellite or land sensor network can replicate in real time. This structural need sustains procurement demand independent of short-term budget cycles.

Maritime patrol requirements reinforce this investment trajectory. The Dassault Falcon 2000LXS Albatros delivers approximately 7 hours of on-station endurance at 200 nautical miles from base — more than twice the endurance of the Falcon 50M it replaces. This capability step-change illustrates that procurement is not merely replacement activity; buyers are upgrading to platforms that meaningfully extend operational coverage, justifying higher unit costs.

Boeing’s lean manufacturing improvements reduced P-8A Poseidon production costs by more than 30% and cut production time by 50%. This cost compression signals that high-performance maritime patrol aircraft are becoming more accessible to second-tier defense budgets — broadening the addressable market beyond the five or six nations that historically dominated P-8A procurement. Multi-role military aircraft adoption across tactical operations follows the same logic: lower per-unit cost expands the buyer pool.

Restraints

High Procurement Costs and Regulatory Complexity Constrain Market Accessibility

Special mission aircraft carry procurement costs that exceed comparable commercial platforms by a significant margin. Mission system integration, specialized avionics, structural modifications, and airworthiness certification for sensor payloads each add cost layers that compound the base airframe price. For smaller defense budgets, this cost structure effectively limits acquisition to leasing arrangements or bilateral aid programs rather than direct procurement.

Certification timelines compound the cost problem. Specialized aircraft systems require extensive regulatory approval processes before operational deployment — processes that can extend program timelines by two to four years. Airbus addresses this through lifecycle cost efficiency: the C295 offers approximately 50% lower lifecycle cost and roughly 35% lower fuel consumption than competing aircraft in its category. However, even cost-efficient platforms face the same certification bottlenecks, which delay revenue recognition for manufacturers and operational deployment for buyers.

Airbus also achieved approximately 8% more range and around 5% lower fuel burn on the C295 through winglet additions — incremental improvements that demonstrate how manufacturers manage cost constraints through engineering rather than price reduction. These gains matter at the fleet level, but they do not resolve the fundamental barrier: the upfront procurement cost of a purpose-built or converted special mission aircraft remains out of reach for a meaningful share of potential buyers.

Growth Factors

AEW&C Expansion, Advanced Sensor Integration, and UAV Scaling Open New Revenue Streams

Airborne Early Warning and Control programs represent the highest-value procurement category within the special mission aircraft market. The Boeing E-7 AEW&C provides more than 4 million square kilometers of radar coverage per standard mission, with mission durations exceeding 10 hours — extendable through aerial refueling. Nations replacing legacy AEW&C fleets must commit to platform programs that combine airframe, radar, battle management software, and data link integration. This complexity concentrates procurement spend with a small number of qualified prime contractors.

Advanced sensor and communication system integration is creating a secondary revenue stream alongside new aircraft sales. Operators that upgrade existing platforms with next-generation electro-optical, infrared, and SATCOM payloads effectively extend fleet life while improving mission capability. The MQ-9A Block 5 Extended Range variant, delivered to the U.S. Marine Corps in 2025, achieves up to 34 hours endurance versus approximately 27 hours on earlier configurations — a 26% improvement that came through systems integration rather than a new airframe program.

Environmental monitoring and climate research represent an emerging demand segment with structurally different buyers. Civilian agencies, research institutions, and international organizations are deploying airborne platforms to monitor deforestation, sea surface temperatures, methane emissions, and disaster zones. This civil demand diversifies the customer base beyond defense, introduces new funding mechanisms including multilateral grants, and creates procurement pathways for operators who cannot justify defense-specification platforms.

Emerging Trends

Commercial Aircraft Conversions, AI-Enabled Surveillance, and Modular Payloads Redefine Platform Economics

Converting commercial aircraft into special mission platforms is reshaping the economics of entry into this market. The U.S. Air Force awarded Sierra Nevada Corporation a Survivable Airborne Operations Center contract worth approximately $13 billion in April 2024, specifying five Boeing 747-8s for conversion — confirming that commercial airframes can meet the most demanding defense requirements when paired with the right mission systems. This conversion model lowers base airframe cost and compresses development timelines compared to purpose-built military designs.

AI-enabled surveillance and target identification systems are shifting performance expectations. According to a peer-reviewed model published in 2025, an AI/ML-based predictive maintenance system for military aircraft achieved approximately 92.3% accuracy in early detection of component failures using sensor and maintenance data. This accuracy level translates directly into reduced unplanned downtime and lower maintenance costs — making AI integration an operational ROI argument rather than a technology preference for fleet managers.

Modular mission payload systems enable operators to reconfigure a single airframe across multiple mission roles without structural modifications. This flexibility directly addresses the affordability constraint by allowing buyers to maximize utilization of a single platform investment. Combined with electro-optical and infrared sensor advances, modular architecture positions special mission aircraft as reconfigurable tools that adapt to evolving threat environments — reducing the case for single-role platforms and accelerating replacement cycles for older fleets.

Regional Analysis

North America Dominates the Special Mission Aircraft Market with a Market Share of 45.80%, Valued at USD 9.1 Billion

North America holds a 45.80% share of the Special Mission Aircraft Market, valued at USD 9.1 Billion in 2025. The United States drives this position through sustained multi-program procurement — including P-8A maritime patrol, E-7 AEW&C, and HADES ISR platforms — backed by the world’s largest defense budget. Established industrial infrastructure, prime contractor presence, and deep integration between procurement agencies and systems integrators make North America the market’s structural anchor.

Europe Special Mission Aircraft Market Trends

Europe represents the second-largest regional market, driven by NATO burden-sharing commitments and the replacement of aging Cold War-era surveillance fleets. The French Navy’s adoption of the Dassault Falcon 2000LXS Albatros for maritime surveillance and the Airbus C295’s widespread use across EU member states illustrate a procurement preference for European-origin platforms. Defense budget increases across Germany, Poland, and the Nordic nations are creating new fleet expansion opportunities.

Asia Pacific Special Mission Aircraft Market Trends

Asia Pacific holds strong growth potential as Indo-Pacific maritime tensions accelerate airborne surveillance procurement. Japan, Australia, India, and South Korea are expanding P-8A and domestic special mission aircraft fleets to address contested sea lanes and exclusive economic zone enforcement requirements. The region’s combination of long coastlines, multiple overlapping territorial disputes, and rising defense budgets creates structural demand for maritime patrol and ISR platforms specifically.

Middle East and Africa Special Mission Aircraft Market Trends

Middle East and Africa procurement concentrates on border surveillance, counter-terrorism, and maritime patrol applications. Gulf Cooperation Council nations are investing in advanced ISR and AEW&C platforms to monitor regional threat environments. Africa’s market remains smaller in absolute terms but shows consistent demand growth driven by UN-mandated peacekeeping support, counter-insurgency operations, and humanitarian response aviation requirements.

Latin America Special Mission Aircraft Market Trends

Latin America’s special mission aircraft demand centers on counter-narcotics surveillance, border monitoring, and disaster response operations. Brazil and Mexico lead regional procurement, deploying fixed-wing and rotary-wing platforms across Amazon basin monitoring, coastal patrol, and emergency services roles. Budget constraints limit fleet expansion rates, but bilateral security agreements with the United States and European partners provide procurement access through foreign military sales and aid mechanisms.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

RTX Corporation operates at the intersection of airframe systems, mission electronics, and propulsion — a scope that allows it to participate in special mission programs at multiple contract tiers simultaneously. This vertical integration advantage means RTX can capture revenue from both the platform and the sensor payload, making it less dependent on any single program win than pure-play airframe manufacturers. Its position across ISR, EW, and AEW&C supply chains provides structural protection against single-program procurement delays.

Israel Aerospace Industries Ltd. has built its competitive position around converting commercial airframes into high-capability special mission platforms at lower cost than Western prime contractors. This strategy addresses the affordability barrier directly — offering defense buyers ISR and AEW&C capability without the full cost of purpose-built military aircraft. IAI’s established export relationships across Asia, Eastern Europe, and Latin America give it access to procurement budgets that U.S.-origin platforms cannot serve due to export control restrictions.

Elbit Systems Ltd. differentiates through mission system integration depth rather than airframe ownership. Its strength lies in electro-optical, SIGINT, and communications payloads that can be integrated across multiple airframes — a platform-agnostic model that expands its addressable market beyond any single aircraft type. This approach positions Elbit as a system integrator of choice for buyers who already own airframes but require mission system upgrades to extend fleet relevance.

The Boeing Company holds the most strategically significant position in the maritime patrol and AEW&C segments through the P-8A Poseidon and E-7 AEW&C programs. Both platforms serve multi-nation customer bases with long sustainment tails — creating aftermarket revenue streams that extend decades beyond initial delivery. Boeing’s lean manufacturing improvements reduced P-8A production costs by more than 30% and production time by 50%, reinforcing its cost competitiveness for future fleet expansion orders from both existing and new P-8A operators.

Key Players

- RTX Corporation

- Israel Aerospace Industries Ltd.

- Elbit Systems Ltd.

- The Boeing Company

- Dassault Aviation

- Northrop Grumman Corporation

- Lockheed Martin Corporation

- Textron Aviation Inc.

- General Dynamics Corporation

- Airbus

Recent Developments

- April 2024 — The U.S. Air Force awarded Sierra Nevada Corporation a Survivable Airborne Operations Center contract valued at approximately $13 billion, covering the conversion of five Boeing 747-8 aircraft to replace the E-4B command-and-control platform known as the ‘Doomsday plane.’

- May 2024 — Sierra Nevada Corporation announced the purchase of five Boeing 747-8 aircraft from Korean Air, scheduled for delivery and conversion into Survivable Airborne Operations Center platforms by approximately September 2025.

- August 2024 — The U.S. Army selected Sierra Nevada Corporation as lead system integrator for the HADES ISR aircraft program under an IDIQ contract initially valued at approximately $93.5 million, with a ceiling of up to $994.3 million, using Bombardier Global 6500 jets as the designated airframe.

- Mid-2025 — L3Harris had delivered 103 missionized business jets for ISR and other special mission roles, including multiple Bombardier Global 6500-based aircraft, underscoring the scale of demand for converted commercial platforms in defense ISR applications.

- 2025 — The MQ-9A Block 5 Extended Range variant was delivered to the U.S. Marine Corps, achieving up to 34 hours of endurance — an increase from approximately 27 hours on earlier MQ-9A configurations — expanding unmanned persistent surveillance capability for forward-deployed forces.

- 2025 — The Dassault Falcon 2000LXS Albatros completed its first flight, offering approximately 7 hours of on-station endurance at 200 nautical miles from base, more than doubling the endurance of the Falcon 50M maritime surveillance aircraft it is designed to replace.

- 2025 — Bombardier Defense reported that its fleet of more than 500 special mission aircraft had accumulated over 3 million flight hours across ISR, maritime patrol, and related missions, confirming the Global 6500 platform’s operational credibility as the airframe of choice for high-value defense conversion programs.

Report Scope

Report Features Description Market Value (2025) USD 20.0 Billion Forecast Revenue (2035) USD 39.2 Billion CAGR (2026-2035) 7.0% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Platform (Fixed Wing, Rotary Wing, Unmanned Aerial Vehicle (UAV), Hybrid/Other Platforms), By Application (Intelligence, Surveillance and Reconnaissance (ISR), Maritime Patrol and Anti-Submarine Warfare (ASW), Electronic Warfare (EW) and Signals Intelligence (SIGINT), Airborne Early Warning & Control (AEW&C), Emergency Services), By End User (Defense and Homeland Security/Law Enforcement, Commercial and Civil), By Point of Sale (OEM, Aftermarket) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape RTX Corporation, Israel Aerospace Industries Ltd., Elbit Systems Ltd., The Boeing Company, Dassault Aviation, Northrop Grumman Corporation, Lockheed Martin Corporation, Textron Aviation Inc., General Dynamics Corporation, Airbus Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Special Mission Aircraft MarketPublished date: Apr 2026add_shopping_cartBuy Now get_appDownload Sample

Special Mission Aircraft MarketPublished date: Apr 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- RTX Corporation

- Israel Aerospace Industries Ltd.

- Elbit Systems Ltd.

- The Boeing Company

- Dassault Aviation

- Northrop Grumman Corporation

- Lockheed Martin Corporation

- Textron Aviation Inc.

- General Dynamics Corporation

- Airbus

Our Clients

- 184048

- Apr 2026