Quick Navigation

Market Overview

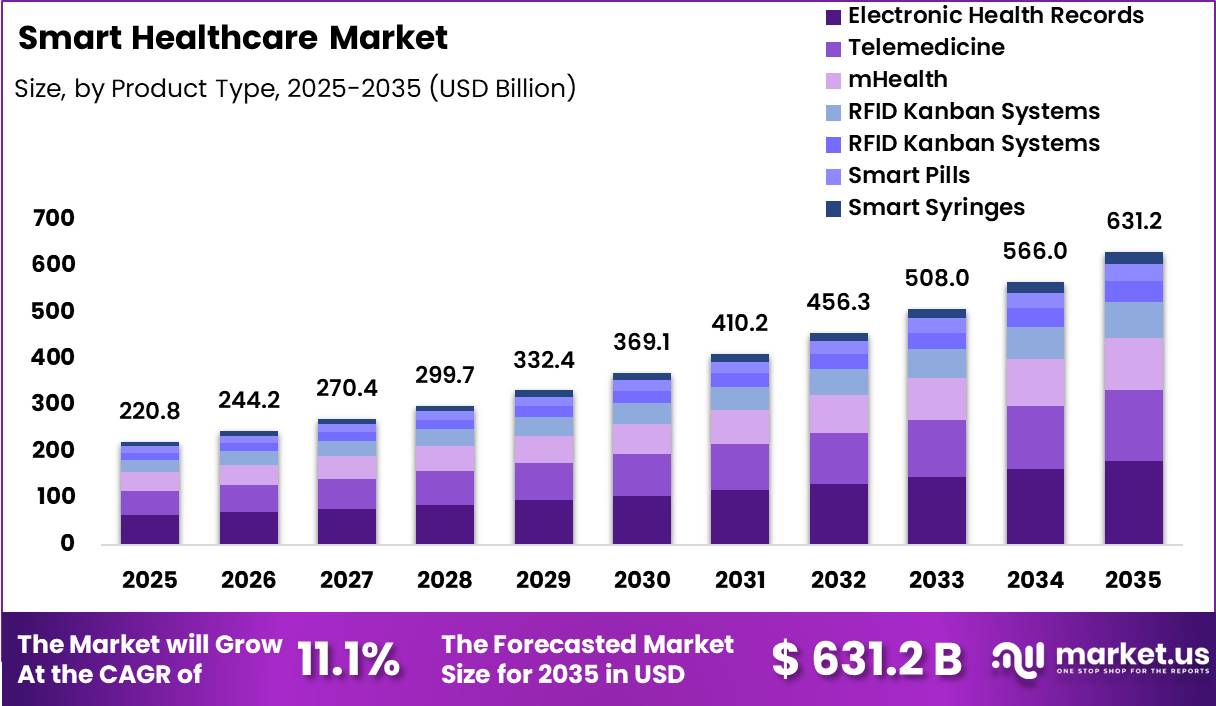

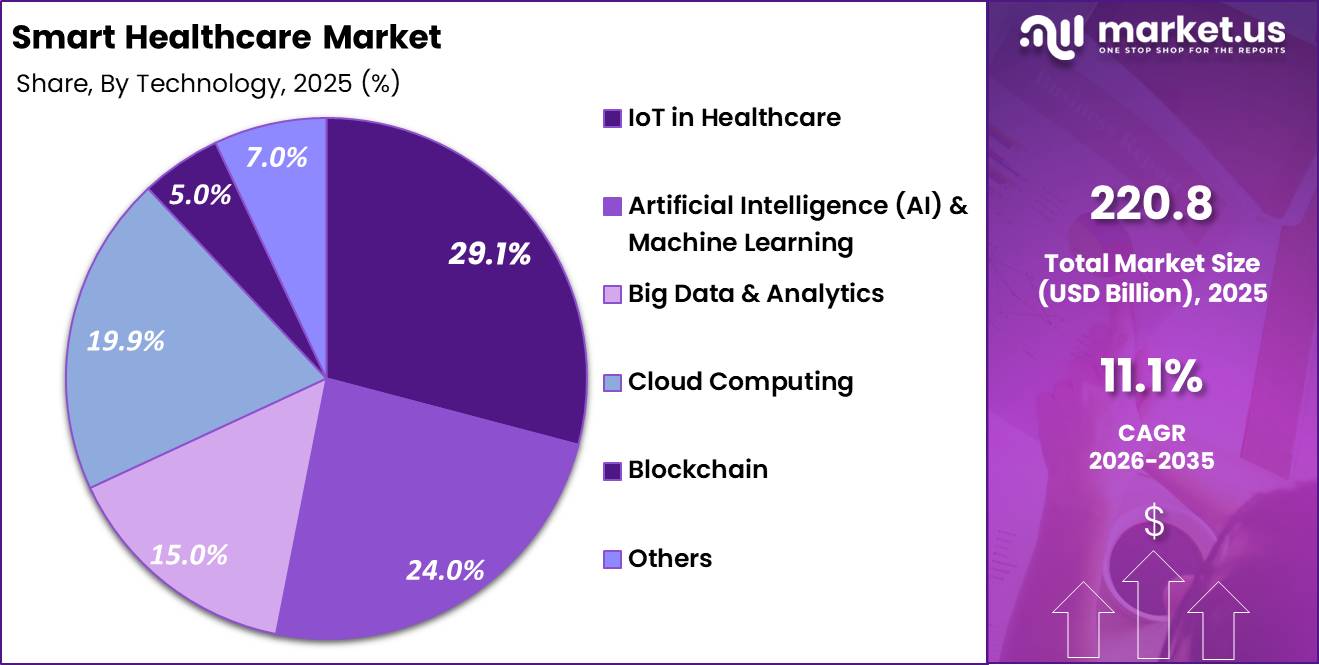

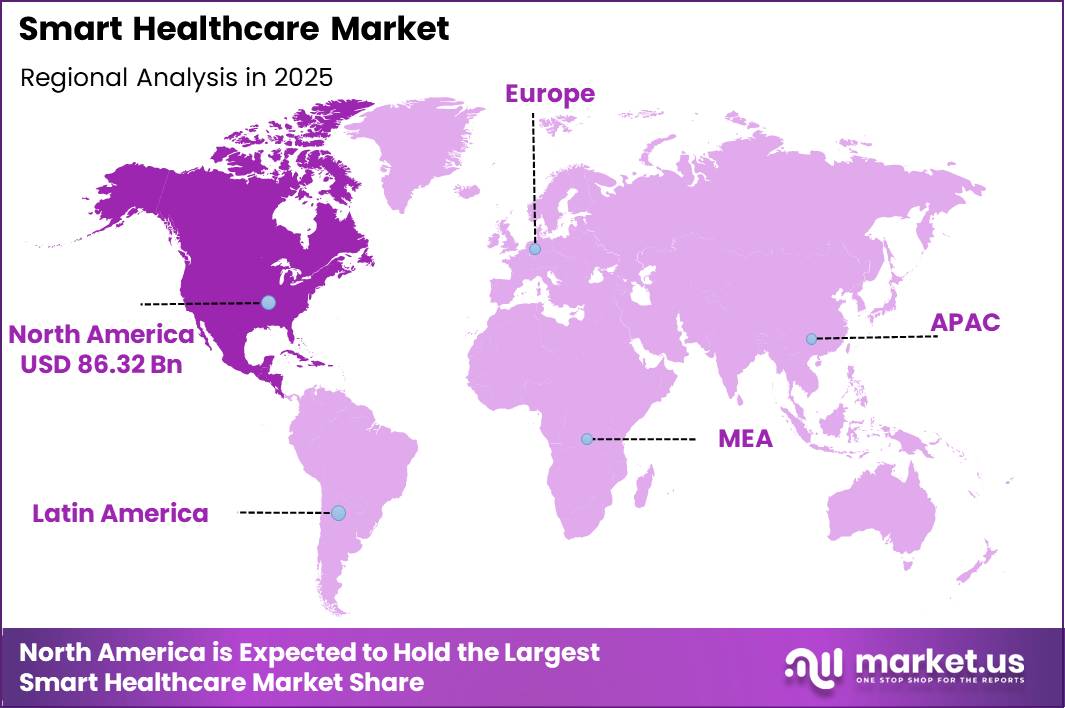

The Global Smart Healthcare Market size is expected to be worth around US$ 631.2 billion by 2035 from US$ 220.8 billion in 2025, growing at a CAGR of 11.1% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 39.1% share with a revenue of US$ 86.32 billion.

Smart healthcare involves using digital technologies and information and communication technologies to enhance the delivery, efficiency, accessibility, and quality of healthcare. This includes remote monitoring, telemedicine, electronic health records, mobile health apps, and AI-enabled tools.

The World Health Organisation defines digital health as a vital component for strengthening health systems and ensuring universal access to quality services worldwide. WHO’s Global Strategy on Digital Health promotes digital solutions that enhance care, equity, and sustainability across different income levels.

In India, the Ayushman Bharat Digital Mission represents the government’s key initiative to establish an integrated digital health ecosystem. ABDM aims to create an interoperable digital health infrastructure that connects healthcare providers, patients, and systems, allowing secure access to real-time health records and services. As a result, over 90 crore Ayushman Bharat Health Accounts have been issued across the country, greatly increasing digital participation.

Smart healthcare solutions are increasingly utilised in teleconsultations, remote diagnostics, electronic prescriptions, data analytics, and personalised care pathways. National telemedicine services led by the government, such as eSanjeevani, and the integration of digital health records aim to eliminate geographic barriers and improve health outcomes, especially in chronic disease management and preventive care. WHO’s classification of digital interventions offers a standardised framework for the deployment and evaluation of these technologies worldwide.

Key Takeaways

- Market Size: The Global Smart Healthcare Market size was US$ 220.8 Billion in 2025. The market is estimated to grow to US$ 631.2 Billion by 2035.

- Market Share: The Compound Annual Growth Rate (CAGR) of the market from 2026 to 2035 will be 11.1%.

- Product Type: Electronic Health Records (EHR) has the largest market share, accounting for 28.7% of total product type revenue.

- Technology: IoT in Healthcare leads the segment, accounting for 29.1% of total technology segment revenue.

- Application: Remote Patient Monitoring leads the segment, accounting for 26.3% of total application revenue.

- End User: Hospitals & Health Systems dominates the segment, accounting for 54.5% of total end-user revenue.

- Regional Analysis: North America is the dominant regional market, accounting for 39.1% of global revenue.

Product Type Analysis

The Smart Healthcare Market by product type reflects the accelerating digital transformation of healthcare delivery, with Electronic Health Records (EHR) dominating the segment at 28.7% market share in 2025.

EHR platforms form the backbone of smart healthcare ecosystems by enabling seamless data capture, interoperability across care settings, and continuity of patient information. Their dominance is reinforced by regulatory digitisation mandates, growing emphasis on coordinated care, and integration with analytics and decision-support tools.

Telemedicine accounts for 24.0%, driven by virtual consultations, remote triage, and improved access to specialists, particularly in underserved regions. mHealth solutions, holding 18.0% share, support real-time monitoring, patient engagement, and preventive care through smartphones and wearable integration.

Hospital logistics and inventory optimisation tools such as RFID Kanban Systems (12.3%) and RFID Smart Cabinets (7.0%) are gaining traction by improving asset visibility and reducing operational inefficiencies.

Emerging segments, including Smart Pills (6.0%) and Smart Syringes (4.0%), enhance medication adherence, dosing accuracy, and safety monitoring. Collectively, these product categories highlight a shift toward interoperable, data-driven platforms that improve care efficiency, clinical accuracy, and system-wide transparency.

Technology Analysis

Technology segmentation underscores the foundational role of connected and intelligent systems in smart healthcare adoption. IoT in Healthcare leads the market with a 29.1% share in 2025, driven by the widespread deployment of connected medical devices, wearables, and remote sensors that enable continuous patient monitoring and real-time data transmission. IoT forms the infrastructure layer for automation, predictive maintenance, and proactive care delivery.

Artificial Intelligence (AI) & Machine Learning, accounting for 24.0%, are increasingly embedded across diagnostics, clinical decision support, workflow automation, and personalised treatment planning.

These technologies enhance diagnostic accuracy and reduce clinician workload through intelligent data interpretation. Cloud Computing holds a 19.9% share, supporting scalable data storage, interoperability, and remote access to health information across distributed care networks.

Big Data & Analytics represents 15.0%, enabling population health management, risk stratification, and outcome measurement through large-scale data processing. Blockchain, though smaller at 5.0%, is gaining relevance for secure data exchange, identity management, and consent tracking. Overall, technology adoption in smart healthcare emphasises automation, data-driven care models, and strengthened cybersecurity frameworks.

Application Analysis

By application, Remote Patient Monitoring (RPM) leads the Smart Healthcare Market with a 26.3% share in 2025, reflecting the growing demand for continuous, non-invasive monitoring of patients outside traditional care settings. RPM improves early intervention, reduces hospital readmissions, and supports value-based care models by enabling real-time clinical oversight.

Chronic Disease Management represents a significant portion of adoption, leveraging connected devices and analytics to manage long-term conditions such as diabetes, cardiovascular disorders, and respiratory diseases. Clinical Workflow Optimisation applications improve operational efficiency by automating scheduling, documentation, and care coordination, allowing clinicians to focus more on patient interaction.

Medication Management solutions enhance adherence, dosing accuracy, and safety through smart packaging and digital reminders. Diagnostics & Imaging applications benefit from AI-enabled interpretation and faster clinical decision-making.

Meanwhile, Fitness & Wellness Monitoring and Elderly Care applications support preventive health, ageing-in-place, and personalised wellness tracking. Collectively, these applications emphasise outcome improvement, care continuity, and the transition from episodic to continuous healthcare delivery.

End User Analysis

End-user segmentation highlights the central role of institutional healthcare providers in smart healthcare adoption. Hospitals & Health Systems dominate the market with a 54.5% share in 2025, driven by large-scale digital infrastructure investments, integrated information systems, and enterprise-wide deployment of smart technologies. Hospitals leverage smart healthcare solutions to improve clinical efficiency, optimise resource utilisation, and enhance patient safety.

Clinics & Physician Practices represent a growing segment, adopting EHRs, telemedicine platforms, and cloud-based tools to improve care coordination and patient engagement while managing operational costs. Home Healthcare Settings are expanding rapidly as remote monitoring, mHealth, and connected devices enable decentralised care delivery and support the shift toward patient-centric and value-based models.

Other end users, including long-term care facilities and diagnostic centres, are increasingly integrating smart solutions to streamline workflows and improve service quality. Overall, end-user adoption reflects a broader transformation toward digitally enabled, patient-focused care models supported by scalable infrastructure, interoperability, and long-term investment in health IT systems.

Key Market Segments

By Product Type

- RFID Kanban Systems

- RFID Smart Cabinets

- Electronic Health Records (EHR)

- Web-based EHR

- Client-server-based EHR

- Telemedicine

- Hardware

- Software

- Others

- mHealth

- Monitoring Services

- Diagnosis Services

- Healthcare Systems

- Strengthening

- Others

- Smart Pills

- Smart Syringes

By Technology

- IoT in Healthcare

- Artificial Intelligence (AI) & Machine Learning

- Big Data & Analytics

- Cloud Computing

- Blockchain

- Others

By Application

- Remote Patient Monitoring

- Chronic Disease Management

- Clinical Workflow Optimisation

- Medication Management

- Diagnostics & Imaging

- Fitness & Wellness Monitoring

- Elderly Care

- Others

By End User

- Hospitals & Health Systems

- Clinics & Physician Practices

- Home Healthcare Settings

- Others

Driver

Chronic disease burden and ageing-led continuous care demand

The most durable demand-side driver remains the scale of noncommunicable disease management: WHO reports NCDs killed at least 43 million people in 2021, equal to 75% of non-pandemic-related deaths globally, with cardiovascular disease accounting for at least 19 million deaths, cancers 10 million, chronic respiratory disease 4 million, and diabetes more than 2 million.

WHO also notes that 18 million people died from an NCD before age 70, and 73% of NCD deaths occurred in low- and middle-income countries, which expands smart healthcare demand beyond high-income hospital digitisation into scalable monitoring, adherence, screening, and risk-stratification tools for broader population health management.

In practical market terms, rising hypertension, diabetes, COPD, and cardiac follow-up loads increase the economic value of connected devices, alerting engines, care-management dashboards, and medication-adherence solutions because they lower the cost of supervising large chronic cohorts compared with frequent in-person visits.

The commercial consequence is a sustained move from procedure-centric revenue toward longitudinal care platforms, especially where payers and providers bear total-cost-of-care risk and need technology that can continuously monitor large patient panels at relatively low marginal cost.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reimbursement-led remote patient monitoring scale-up | +2.2% | North America core, EU selective, APAC private-urban corridors | Short term (≤ 2 years) |

| Interoperability mandates and health data liquidity | +1.8% | North America core, EU core, developed APAC corridors | Short term (≤ 2 years) |

| Clinical and administrative AI integration | +2.0% | North America core, EU core, APAC advanced markets | Medium term (2-4 years) |

| Chronic disease burden and ageing-led continuous care demand | +1.6% | Global, with the strongest pull in North America, the EU, East Asia, Gulf | Medium term (2-4 years) |

| Hospital-at-home and site-of-care decentralization | +1.7% | North America core, Western Europe, developed APAC cities | Medium term (2-4 years) |

| Regulatory formalisation of trusted digital health | +1.1% | EU core, North America core, spill-over to OECD-linked markets | Long term (≥ 4 years) |

Challenges

Workforce Capacity Gaps Slowing Smart Healthcare Technology Adoption

The smart healthcare stack is scaling faster than healthcare systems can absorb hybrid talent across clinical operations, informatics, cybersecurity, workflow design, and device integration, creating a structural execution bottleneck rather than a demand weakness.

WHO projects an 11 million global health-worker shortfall by 2030, while OECD analyses highlight the need to significantly upgrade digital competencies across healthcare workforces, indicating that adoption of connected care, virtual monitoring, AI triage, and interoperability systems is frequently constrained by implementation capacity rather than technology availability.

In practice, large provider systems often experience transformation staffing gaps of roughly 8% to 15% of required roles, particularly in nurse informatics, biomedical engineering, data governance, and cybersecurity operations.This results in 6–12-month rollout delays, 12–18% higher integration service costs, and 10–20 percentage point lower utilisation of deployed digital tools versus planned levels.

The overall effect is a slower realisation of value from already-purchased technologies, with benefits dependent on redesigning workflows, reducing training intensity, and expanding managed services and structured training pipelines to bridge the operational talent gap over time.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Clinical-Digital Talent Gap | -1.6% | North America core, EU care systems, APAC tier-1 metros, emerging-market public networks | Long-term (≥ 4 years) |

| Interoperability Integration Debt | -1.4% | U.S. provider networks, EU regulatory hubs, GCC smart-hospital clusters, APAC private systems | Medium term (2-4 years) |

| Cybersecurity Lifecycle Burden | -1.8% | North America core, Western Europe, Japan, South Korea, high-connectivity urban hospitals | Long term (≥ 4 years) |

| AI Validation Compliance Load | -1.1% | U.S. FDA pathway markets, EU AI-regulated markets, UK, Japan, Australia | Medium term (2-4 years) |

| Component Sourcing Volatility | -0.9% | APAC electronics corridors, U.S. medtech OEMs, EU device assemblers | Medium term (2-4 years) |

| Fragmented Reimbursement Proof | -1.2% | U.S. payer-driven market, EU public procurement systems, large private hospital chains in APAC and LatAm | Medium term (2-4 years) |

Restraints

Regulatory and Liability Pressures Slowing AI Healthcare Commercialisation

AI-enabled smart healthcare tools increasingly face a double burden of evidence: they must prove technical accuracy and sustain safe real-world performance across populations, care settings, and evolving data inputs, while manufacturers also absorb legal exposure if algorithmic drift, false reassurance, or biased outputs affect clinical decisions.

Because the EU AI Act requires high-risk AI systems to operate under documented quality management and technical documentation structures, and US regulators continue to emphasize safety, effectiveness, and post-market controls for connected and software-driven devices, vendors often need expanded multicenter studies, model monitoring infrastructure, and physician-in-the-loop design, which can push validation budgets 20–40% above conventional software product development and delay broad market entry by 6–12 months.

The business consequence is a structurally slower innovation cycle, higher insurance and legal-review costs, narrower initial indications for use, and a bias toward larger incumbents with stronger regulatory and medico-legal balance sheets, which restrains category-wide CAGR even as long-term demand fundamentals remain favourable.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cybersecurity compliance burden | -1.9% | North America core, EU, Japan, Korea | Short term (≤ 2 years) |

| Health data regulation friction | -1.5% | EU core, UK, North America | Medium term (2-4 years) |

| Reimbursement proof-gap | -1.7% | US core, EU5, selective APAC | Medium term (2-4 years) |

| Device component volatility | -1.3% | North America, EU, China+, ASEAN supply corridors | Short term (≤ 2 years) |

| Interoperability retrofit cost | -1.1% | EU, US provider networks, Gulf hubs | Medium term (2-4 years) |

| Clinical validation and liability drag | -1.4% | US, EU, Australia, Singapore | Long term (≥ 4 years) |

Opportunity

Interoperability Transitioning into a Monetizable Healthcare Data Platform

Interoperability is increasingly evolving from a compliance requirement into a monetizable data utility layer that sits on top of standardised healthcare data exchange. While current spending is largely driven by mandatory integration and certification needs, the emerging opportunity lies in building application-layer services that leverage standardised data flows for identity resolution, prior authorisation automation, population risk scoring, real-world evidence generation, and cross-enterprise workflow optimisation.

Regulatory progress in the U.S., including ONC’s move toward USCDI v3 under the HTI-1 rule in 2026 and the rollout of TEFCA as a national exchange framework, is creating the foundational infrastructure for scalable data liquidity across providers, payers, patients, and public health systems.

Once these standards stabilise, vendors can transition from one-time integration projects to recurring, usage-based revenue models built on data access and analytics services. This shift can reduce implementation timelines by 30–50%, expand wallet share per health-system customer by 1.5x–2.0x, and unlock new product layers that were previously constrained by fragmented data environments, enabling materially higher scalability and platform-driven growth across the healthcare IT ecosystem.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Hospital-at-home orchestration | +2.3% | North America core, EU5, Japan | Short term (≤ 2 years) |

| AI-enabled chronic care bundles | +2.0% | US core, Canada, UK, Nordics | Short term (≤ 2 years) |

| Interoperable data utilities | +1.7% | US, EU, GCC, ANZ | Medium term (2-4 years) |

| Low-cost smart care for LMICs | +2.6% | India, SEA, Africa, LatAm | Medium term (2-4 years) |

| Senior living + home care platforms | +1.9% | Japan, Western Europe, the US, and South Korea | Medium term (2-4 years) |

| Roll-up of niche digital point solutions | +1.5% | US, EU, APAC developed | Long term (≥ 4 years) |

Regional Analysis

In 2025, North America led the smart healthcare market with a share of over 39.1% and a revenue of US$ 86.32 billion. The region remains at the forefront, driven by advanced digital infrastructure, substantial healthcare IT spending, and a strong adoption of interoperable solutions.

The United States significantly contributes to this growth due to the widespread use of Electronic Health Records (EHR), telemedicine platforms, and AI-enabled clinical decision support systems. Favourable reimbursement policies, regulatory support for data exchange, and early adoption of remote patient monitoring are further accelerating market penetration.

Europe is recognised as a mature and steadily expanding market, bolstered by government-driven digital health initiatives and cross-border interoperability frameworks. Countries such as Germany, the United Kingdom, and France are making significant investments in eHealth records, smart hospital infrastructure, and population health management solutions to address the challenges posed by ageing demographics and the burden of chronic diseases.

The Asia-Pacific region is the fastest-growing area, driven by increasing healthcare demand, expanding digital connectivity, and strong government support for health technology innovation. Countries like China, India, and Japan are experiencing rapid adoption of mobile health (mHealth), telemedicine, and smart medical devices, particularly in underserved and rural areas.

Latin America and the Middle East & Africa are emerging markets where gradual improvements in healthcare infrastructure and a rise in mobile health adoption are creating long-term growth opportunities, despite challenges related to funding and digital readiness.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Player Analysis

Suppliers in the global smart healthcare market seek competitive advantage through integrated IoT and AI-enabled platform development connecting electronic health records, remote patient monitoring devices, and clinical decision support systems into unified digital health ecosystems serving hospital, clinic, and home healthcare settings simultaneously.

Key strategic focus areas include interoperability standard adoption enabling seamless data exchange across disparate healthcare IT systems, cloud-based infrastructure scaling supporting growing telemedicine and remote monitoring data volumes, and cybersecurity investment protecting sensitive patient health information across increasingly connected device networks.

Companies continue investing in AI-driven diagnostic and predictive analytics capabilities, mHealth application development targeting chronic disease management and elderly care applications, and strategic partnerships with hospital systems and health insurance payers to secure long-term technology deployment agreements across institutional healthcare buyer networks globally.

The accelerating convergence of artificial intelligence, IoT connectivity, and cloud computing infrastructure is fundamentally transforming smart healthcare from discrete point-solution products into integrated digital health platforms capable of delivering continuous patient monitoring, predictive clinical insights, and automated workflow optimisation across the full continuum of care through the forecast period to 2035.

Top Key Players

- AirStrip Technologies Inc.

- Veradigm LLC

- Apple Inc.

- AT&T Inc.

- Brooks Automation

- Oracle (Cerner Corporation)

- Cisco Systems Inc.

- GE Healthcare

- Medtronic plc

- Hurst Green Plastics Ltd.

- IBM Corporation

- Logi-Tag

- McKesson Corporation

- Olympus Corporation

- Pepperl+Fuchs Pvt. Ltd.

- Samsung Electronics Co., Ltd.

- Siemens Healthcare Private Limited

- Solstice Medical LLC

- InnerSpace (Acquired by Solaire Medical)

- Böllhoff Group

- Adolf Würth GmbH & Co. KG

- Other Key Players

Recent Developments

- In February 2026, Medtronic plc expanded its remote patient monitoring device portfolio for chronic disease management, targeting growing home healthcare institutional buyer demand across European and North American distribution networks.

- In March 2026, GE Healthcare secured a multi-year smart healthcare infrastructure agreement with a leading Asian hospital network, covering IoT-enabled diagnostic imaging and clinical workflow optimisation platform deployment across institutional buyer facilities.

- In May 2026, Apple Inc. expanded its mHealth ecosystem integration with major electronic health records platforms, enabling seamless patient-generated health data exchange across hospital and physician practice institutional healthcare buyer networks.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 220.8 Billion |

| Forecast Revenue (2035) | US$ 631.2 Billion |

| CAGR (2026-2035) | 11.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (RFID Kanban Systems, RFID Smart Cabinets, Electronic Health Records (EHR), Telemedicine, mHealth, Smart Pills, Smart Syringes), By Technology (IoT in Healthcare, Artificial Intelligence (AI) & Machine Learning, Big Data & Analytics, Cloud Computing, Blockchain, Others), By Application (Remote Patient Monitoring, Chronic Disease Management, Clinical Workflow Optimization, Medication Management, Diagnostics & Imaging, Fitness & Wellness Monitoring, Elderly Care, Others), By End User (Hospitals & Health Systems, Clinics & Physician Practices, Home Healthcare Settings, Others) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | AirStrip Technologies Inc., Veradigm LLC, Apple Inc., AT&T Inc., Brooks Automation, Oracle (Cerner Corporation), Cisco Systems Inc., GE Healthcare, Medtronic plc, Hurst Green Plastics Ltd., IBM Corporation, Logi-Tag, McKesson Corporation, Olympus Corporation, Pepperl+Fuchs Pvt. Ltd., Samsung Electronics Co., Ltd., Siemens Healthcare Private Limited, Solstice Medical LLC, InnerSpace (Acquired by Solaire Medical), Böllhoff Group, Adolf Würth GmbH & Co. KG, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |