Quick Navigation

Report Overview

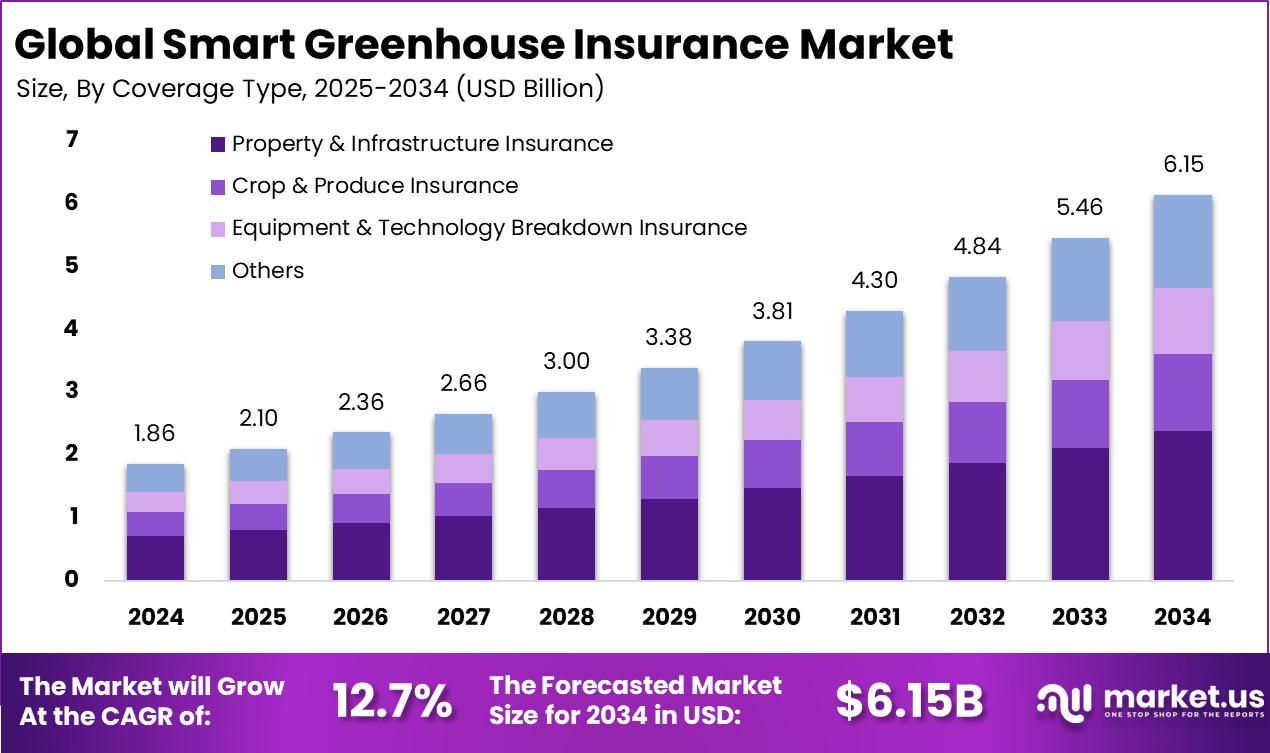

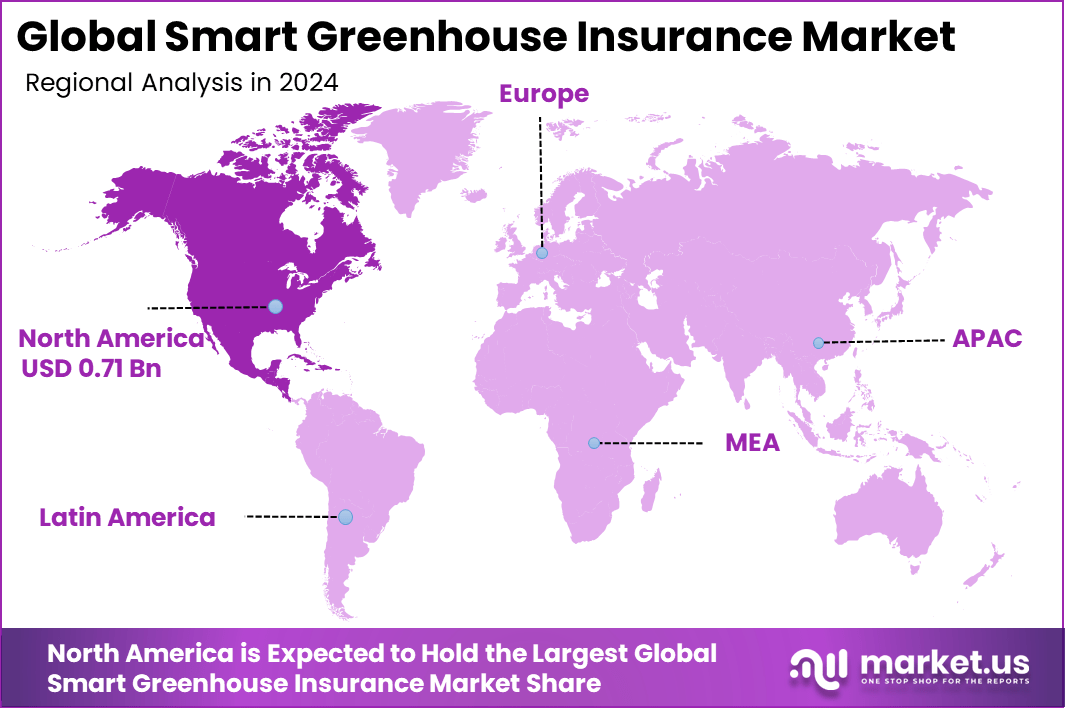

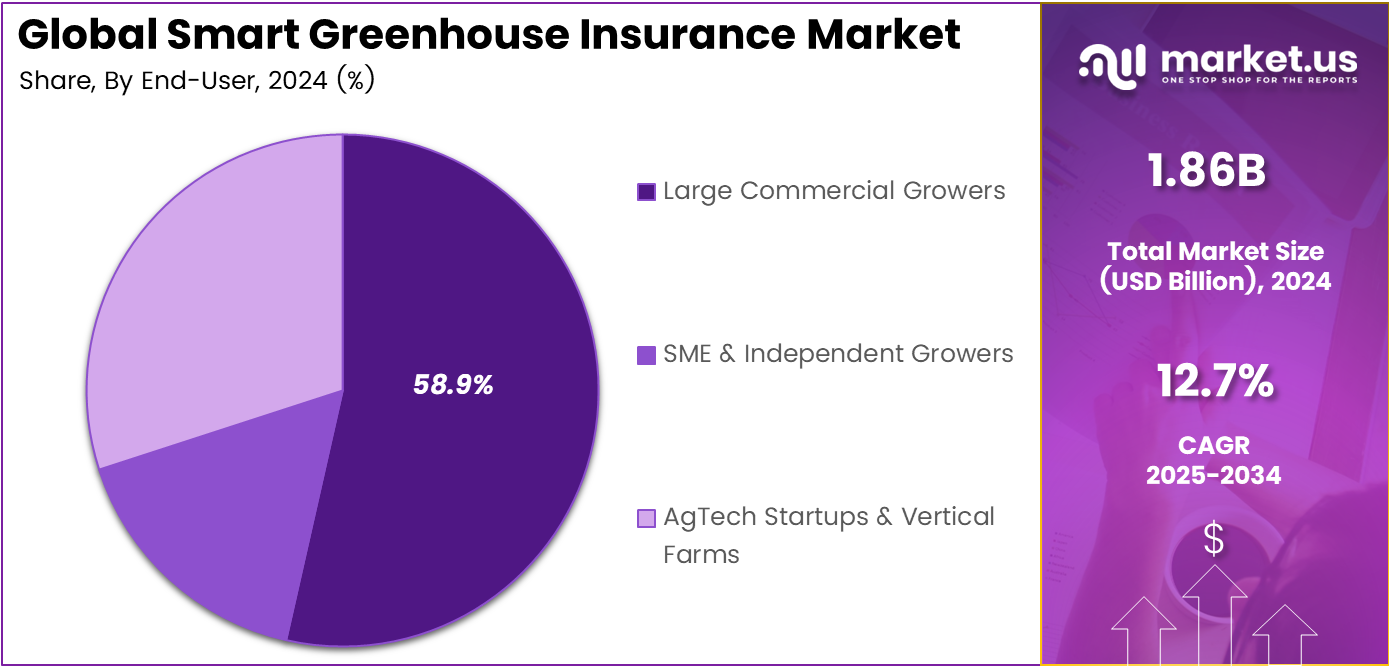

The Global Smart Greenhouse Insurance Market size is expected to be worth around USD 6.15 billion by 2034, from USD 1.86 billion in 2024, growing at a CAGR of 12.7% during the forecast period from 2025 to 2034. North America held a dominant market position, capturing more than 38.5% share and generating USD 0.71 billion in revenue.

Smart greenhouse insurance helps protect advanced farming systems that use technology to control temperature, light, and humidity. As more farms rely on connected devices and automation, the financial risk of damage or system failure grows. This insurance covers technology breakdowns, crop losses, and natural disasters that affect production. With farmers increasingly exposed to unpredictable weather and system outages, the need for tailored insurance protection has risen. It gives greenhouse owners peace of mind by securing their investments and supporting the move toward more efficient, sustainable farming practices that combine technology with environmental responsibility.

Several factors drive the adoption of smart greenhouse insurance. Rapid climate fluctuations and frequent storms are increasing crop losses globally, making insurance essential. Smart systems that monitor weather and soil conditions reduce damage but can fail under extreme conditions. Farmers also face rising hardware and maintenance costs for IoT and automation systems, making financial protection vital. Insurance providers design flexible policies that address these specific risks while encouraging the use of preventive technologies. Increasing awareness about climate resilience and the desire to protect high-value produce encourage farmers to invest more in smart coverage options.

The market for Smart Greenhouse Insurance is driven by rising weather uncertainties that threaten controlled crop environments. Storms, floods, and shifting patterns damage high-value setups with sensors and climate controls, pushing growers to seek reliable protection. Insurers respond with tailored policies that use real-time data for quick claims, helping farms bounce back fast. This need grows as extreme events hit more often, turning coverage into a key tool for year-round production stability. Farmers invest confidently knowing losses won’t wipe out their efforts.

The demand for smart greenhouse insurance continues to grow as technology becomes central to modern agriculture. Farmers investing in connected systems to monitor temperature and irrigation now realize the potential costs of technical failures. Natural disasters, cyber threats, and power outages also push more greenhouse operators toward coverage that includes both physical and digital assets. As insurance providers gain data from connected devices, they refine their models to set fairer premiums. This steady rise in awareness and technology adoption signals a lasting need for insurance that aligns protection with smart farming needs.

For instance, in June 2025, The Hartford Financial Services Group partnered with research groups on climate modeling tools that feed into smart greenhouse policies, predicting risks like extreme heat or floods for controlled environments. This boosts their inland marine endorsements for high-value crops, giving growers reliable coverage that matches real-time data from greenhouse systems.

Key Takeaway

- In 2024, the Property & Infrastructure Insurance segment held a dominant market position, capturing a 38.7% share of the Global Smart Greenhouse Insurance Market.

- In 2024, the Commercial Hydroponic/Aeroponic Farms segment held a dominant market position, capturing a 52.4% share of the Global Smart Greenhouse Insurance Market.

- In 2024, the Annual/Multi-Year Policies segment held a dominant market position, capturing an 83.5% share of the Global Smart Greenhouse Insurance Market.

- In 2024, the Large Commercial Growers segment held a dominant market position, capturing a 58.9% share of the Global Smart Greenhouse Insurance Market.

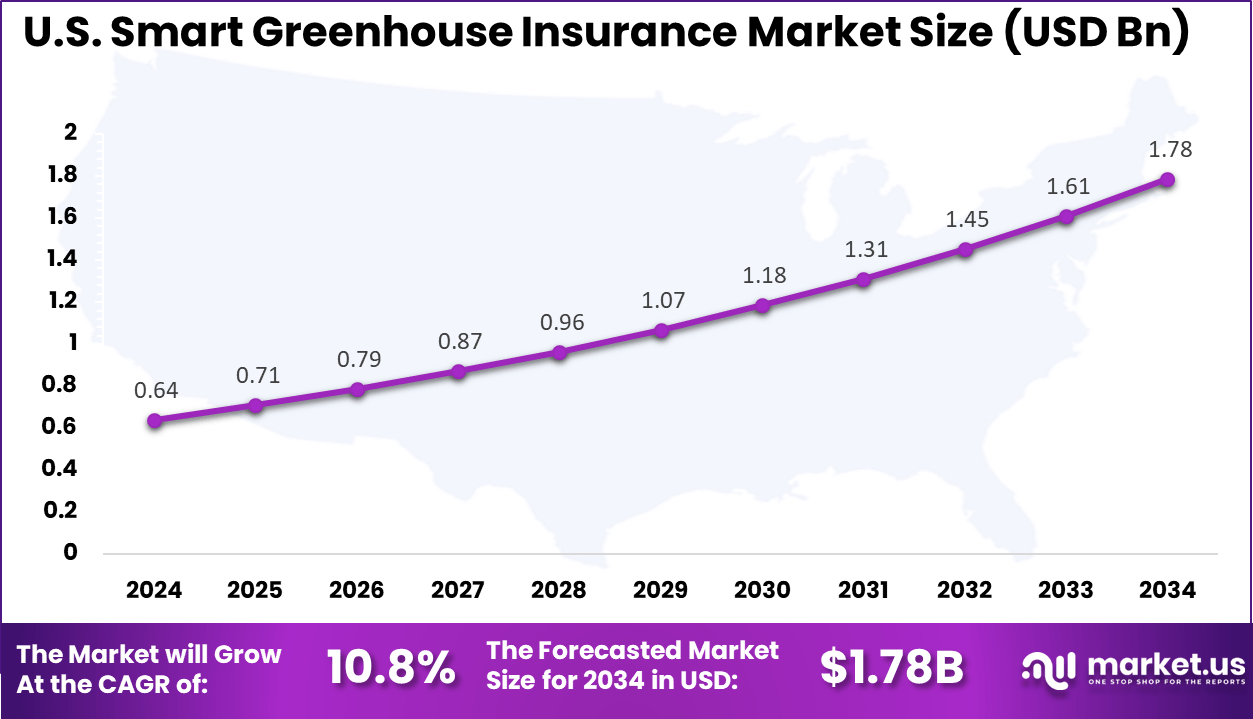

- The U.S. Smart Greenhouse Insurance Market was valued at USD 0.64 Billion in 2024, with a robust CAGR of 10.8%.

- In 2024, North America held a dominant market position in the Global Smart Greenhouse Insurance Market, capturing more than a 38.5% share.

Regional Analysis

In 2024, North America held a dominant market position in the Global Smart Greenhouse Insurance Market, capturing more than 38.5% share and generating USD 0.71 billion in revenue. This dominance stems from widespread adoption of advanced greenhouse automation, strong risk management frameworks, and increasing climate unpredictability across the region. Farmers in the U.S. and Canada are investing in insurance to protect high-value infrastructure and digital tools from extreme weather events. Supportive government policies, a mature insurance ecosystem, and rapid expansion of commercial hydroponic and aeroponic farms further reinforced the region’s leadership.

For instance, in November 2025, Chubb Ltd. launched an AI-powered embedded insurance engine, enhancing real-time risk assessment for agriculture, including smart greenhouses. This innovation supports precision monitoring and climate-resilient farming. Chubb’s advanced tools underscore North America’s leadership in technology-driven crop and greenhouse insurance solutions.

U.S. Smart Greenhouse Insurance Market Size

The market for Smart Greenhouse Insurance within the U.S. is growing tremendously and is currently valued at USD 0.64 billion; the market has a projected CAGR of 10.8%. The market is growing due to the rising adoption of automated cultivation and climate control technologies. Farmers are investing in advanced systems to improve efficiency and reduce water and labor costs, which also increases their exposure to equipment and environmental risks. Insurance demand is increasing as operators seek coverage for sensor failures, power interruptions, and crop losses. Climate change, unpredictable weather, and expanding commercial hydroponic farms further accelerate this growth.

For instance, in January 2025, FM Global emphasized AI models for predicting greenhouse losses from climate hazards, fires, and equipment failures in its 2025 outlook. Proprietary data analytics enable precise underwriting for smart facilities. FM Global’s engineering expertise reinforces U.S. dominance in commercial property insurance for advanced agriculture.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Coverage Type Analysis

In 2024, the Property & Infrastructure Insurance segment held a dominant market position, capturing a 38.7% share of the Global Smart Greenhouse Insurance Market. This coverage shields greenhouse owners against losses caused by natural calamities, equipment failure, and structural damage. Growers invest heavily in automated systems, irrigation technology, and temperature control units, which makes them vulnerable to costly interruptions. The policy ensures operational continuity and minimizes repair costs after unexpected incidents.

The increasing complexity of greenhouse infrastructure strengthens the demand for such insurance. Modern greenhouses now depend on climate sensors and solar-powered systems that require consistent protection. Farmers choose comprehensive coverage to reduce risks from unpredictable weather and mechanical faults. With ongoing climate changes, insurers are adapting policies that focus on both sustainability and resilience, aligning them with growers’ long-term needs.

For Instance, in October 2025, FM Global expanded its engineering-based property insurance for advanced agricultural facilities, focusing on resilience against equipment breakdowns. The update includes assessments for greenhouse frames and roofing under extreme weather. This approach helps owners maintain operations by preventing costly repairs to vital infrastructure.

Greenhouse Type Analysis

In 2024, the Commercial Hydroponic/Aeroponic Farms segment held a dominant market position, capturing a 52.4% share of the Global Smart Greenhouse Insurance Market. These farms depend on controlled nutrient delivery, regulated light levels, and real-time monitoring, making equipment reliability vital. Insurance helps growers manage potential losses caused by system malfunctions, pump failures, or contamination events. It also ensures faster recovery and production stability in case of downtime.

Hydroponic and aeroponic greenhouses have higher exposure to operational and technological risks. As demand for fresh, locally grown produce rises, these setups have become crucial for consistent yields. Insurers are now tailoring products to cover sensor damage, water system breakdowns, and environmental control failures. This shift supports the sector’s growth while giving farm operators confidence in their investments.

For instance, in October 2025, Zurich introduced modular insurance for agrivoltaic systems that overlap with hydroponic greenhouses, covering crop damage from shared tech failures. The policy protects sensors, pumps, and nutrient systems in soilless farms from power outages or contamination. It supports year-round production in these high-tech environments.

Policy Duration Analysis

In 2024, the Annual/Multi-Year Policies segment held a dominant market position, capturing an 83.5% share of the Global Smart Greenhouse Insurance Market. These plans are popular among growers operating year-round, offering predictable coverage over multiple planting cycles. The longer durations help reduce administrative work linked to frequent renewals, while providing cost stability. Growers prefer this option for protection throughout the lifecycle of both infrastructure and crops.

Multi-year policies encourage strong partnerships between insurers and greenhouse operators. They allow farmers to secure better premiums by demonstrating consistent risk management practices. As weather patterns grow unpredictable, insurers increasingly highlight long-term coverage for climate-sensitive operations. Farmers, in turn, view these policies as essential for maintaining a steady income and protecting advanced systems without yearly renegotiation.

For Instance, in April 2025, Munich Re enhanced its parametric reinsurance for multi-year agricultural policies, linking payouts to weather data over extended cycles. This suits annual renewals in greenhouses by stabilizing premiums for long-term crop protection. It reduces renewal hassles for consistent coverage.

End-User Analysis

In 2024, the Large Commercial Growers segment held a dominant market position, capturing a 58.9% share of the Global Smart Greenhouse Insurance Market. Their extensive investments in advanced technologies and large-scale operations. These businesses rely on automation, remote monitoring, and sustainable infrastructure that must remain operational at all times. Insurance gives them protection against system breakdowns, crop failures, or extended downtime impacting output.

Because commercial operations face higher financial exposure, tailored insurance products have become vital. Coverage extends to both physical assets and productivity-related risks. Many insurers now offer data-driven policies based on performance metrics and risk assessments. As smart greenhouse farms expand globally, large growers lead the push for integrated coverage that aligns with long-term production and sustainability goals.

For Instance, in November 2025, Allianz advanced claims handling for commercial growers via data-driven policies covering downtime in large automated greenhouses. Focus on renewables integration helps protect high-output facilities from breakdowns. This aids major players in maintaining steady production flows.

Key Market Segments

By Coverage Type

- Property & Infrastructure Insurance

- Crop & Produce Insurance

- Equipment & Technology Breakdown Insurance

- Others

By Greenhouse Type

- Commercial Hydroponic/Aeroponic Farms

- Commercial Traditional Soil-Based Greenhouses

- Research & Educational Facilities

By Policy Duration

- Annual/Multi-Year Policies

- Seasonal/Percrop Cycle Policies

By End-User

- Large Commercial Growers

- SME & Independent Growers

- AgTech Startups & Vertical Farms

Emerging Trends

Smart greenhouse insurance is entering a digital transformation phase supported by IoT sensors, remote sensing tools, and predictive analytics. These technologies allow insurers to track temperature, humidity, and soil moisture data in real time. More than 35% of insurance providers now use mobile-based claim platforms where payouts are linked to predefined weather indices. This approach simplifies the process for farmers while cutting verification time. The trend toward parametric insurance is growing rapidly, especially in high-risk farming zones where climate uncertainty affects consistency in crop yields.

Another key trend is the use of continuous environmental monitoring to determine premiums and risk scores. Farmers adopting precision irrigation or using renewable greenhouse systems receive improved coverage options. Around 50% of digital farm insurance users say data-enabled services have reduced losses related to system downtime or pest attacks. This shift toward proactive insurance models aligns financial incentives with sustainable agricultural practices. As adoption spreads, insurers are integrating weather models and data from agricultural drones into decision systems that reduce delays and disputes.

Growth Factors

Rising climate instability and extreme weather are major reasons for the growing need for smart greenhouse insurance. Farmers face unpredictable shifts that affect production and input costs. By integrating IoT sensors and real-time alerts, insurers can assess greenhouse performance more accurately. About 55% of insured small farmers benefit from government-supported premium subsidies, which make coverage more affordable.

The combination of precise monitoring, digital claims, and public support creates steady demand for smart greenhouse protection systems that safeguard both crops and investments. Collaborations between agri-tech startups and insurers are also helping strengthen coverage for greenhouse growers. AI tools use satellite imagery to analyze risks such as humidity levels and disease spread.

Data sharing between farmers and insurers allows mutual trust and faster settlements. Over 40% of insurers say digital tools have improved claim accuracy, reducing losses from policy lapses. As farms modernize with connected systems, the need for data-informed insurance continues to rise, improving both productivity and financial safety for greenhouse operators.

Market Dynamics

Drivers - Weather Uncertainties

Unpredictable weather patterns such as storms, hail, and floods have increased the vulnerability of greenhouse farming. These events can cause significant crop losses despite farmers investing heavily in controlled growing environments. As weather risks rise, growers view insurance as an essential safeguard rather than an optional expense. Coverage that includes weather-related damages allows them to recover faster and maintain stable production cycles, which strengthens the reliability of food supply chains. The financial safety net provided by insurance helps protect both large and small operations from the devastating effects of climate variability.

Insurance companies are adapting by integrating smart technology into their policy frameworks. Sensors that track internal conditions such as humidity, temperature, and light levels allow insurers to evaluate damage more precisely and settle claims efficiently. This data-driven approach enhances transparency and builds stronger relationships between insurers and farmers. With faster claim resolution and evidence-based assessments, insurance becomes a trusted tool for mitigating the financial impact of unpredictable weather events, supporting resilience and continuity in modern greenhouse operations.

For instance, in September 2025, AXA Climate released a white paper promoting regenerative farming insurance linked to weather data tools. The coverage addresses yield losses from storms and excessive rain in vulnerable regions. Farmers receive payouts based on real-time fungal disease risks tied to weather patterns. This approach supports quick recovery for greenhouse operations hit by unpredictable conditions. It integrates decision-support apps to minimize storm-related disruptions.

Restraint - High Setup Costs

The high cost of building and equipping smart greenhouses remains a major barrier to widespread insurance adoption. Advanced systems involving climate controls, automated irrigation, and sensor networks require substantial initial investments. On top of these large expenses, insurance premiums can add ongoing financial pressure, particularly for small and mid-sized farms that operate on limited budgets. As a result, many growers either reduce coverage or forgo it entirely, leaving them exposed to unanticipated losses that could threaten long-term stability.

Claim verification also adds complexity when dealing with costly assets. Insurers often require detailed documentation and proof of value, which can delay claim approval or discourage participation altogether. When policy costs and administrative requirements exceed what small producers can sustain, the insurance market’s growth slows down. Addressing these cost challenges will be key to making insurance more accessible and sustainable for a broader spectrum of greenhouse owners.

For instance, in April 2025, The Hartford developed software to assess climate risks, revealing high costs for weather-resilient greenhouses. Insurers face challenges in pricing coverage for tech-heavy setups vulnerable to floods. Farmers hesitate on policies due to premiums adding to initial investments. Claim processes require extensive proof of asset values. This slows adoption among budget-constrained growers.

Opportunities - Tech Monitoring Advances

Technological innovation in greenhouse monitoring offers a clear path for insurance sector growth. Real-time data from sensors tracking temperature, humidity, and soil conditions helps insurers assess risk more accurately and design flexible, usage-based plans. Farmers benefit from tailored coverage that reflects actual operating conditions rather than generic premiums. This collaboration fosters greater trust, reduces disputes, and encourages wider participation in insurance programs designed around transparency and data-sharing.

As these digital tools become more integrated, insurers can provide additional services like automated alerts, predictive maintenance, and early warnings to prevent crop loss. Such proactive engagement enhances customer satisfaction and strengthens the perception of insurance as a supportive partner rather than a reactive measure. The combination of real-time monitoring and customized coverage models positions the greenhouse insurance segment for long-term growth driven by innovation and mutual value creation.

For instance, in May 2025, Swiss Re scaled parametric agriculture solutions using sensors for soil moisture and temperature triggers. Real-time data enables customized plans for greenhouse risk management. Payouts occur swiftly on weather thresholds, reducing disputes. The Opti-Crop platform shares live monitoring insights with farmers. This fosters data-driven ties between insurers and growers.

Challenges - Cyber Security Gaps

As smart greenhouses rely more on connected devices and cloud-based systems, the risk of cyberattacks becomes a growing concern. Unauthorized access or data breaches could disrupt automated controls, manipulate environmental settings, or compromise sensitive operational data. These incidents not only lead to financial losses but also create uncertainty in insurance claims, as identifying the root cause of digital failures can be difficult. Farmers are increasingly aware of these threats, yet current insurance options often lack adequate protection for cyber-related risks.

The complexity of underwriting cyber vulnerabilities presents further difficulties for insurers. A single cyber incident could impact multiple clients simultaneously, amplifying financial exposure. Without clear coverage guidelines and improved detection measures, trust between insurers and greenhouse operators may weaken, slowing the adoption of advanced insurance products. Strengthening cybersecurity frameworks and defining standardized policies will be crucial for maintaining confidence and ensuring the continued digital transformation of the greenhouse insurance landscape.

For instance, in January 2025, Munich Re expanded cyber solutions for large organizations, tackling risks in connected agriculture systems vulnerable to hacks. Customized policies cover data theft and control shutdowns in greenhouses. Pricing challenges from unseen threats prompt better defenses. Standardized rules prevent multi-client impacts. Sector gains tools to fight digital vulnerabilities.

Key Players Analysis

One of the leading players in November 2025, Markel Insurance, teamed up with Greenhouse Specialty Insurance Services for cutting-edge environmental casualty coverage that directly supports smart greenhouse operations. This partnership blends Markel’s deep underwriting know-how with Greenhouse’s tech platform, making it easier for brokers to handle complex risks like pollution and site cleanups in high-tech ag setups. It’s a smart move that helps U.S. growers protect their automated systems while pushing sustainable farming forward.

Top Key Players in the Market

- Chubb, Ltd.

- AXA SA

- Zurich Insurance Group, Ltd.

- Allianz SE

- American Financial Group, Inc.

- Tokio Marine Holdings, Inc.

- Sompo Holdings, Inc.

- Munich Re

- Swiss Re, Ltd.

- ICAT

- Farmers Insurance Group

- The Hartford Financial Services Group, Inc.

- QBE Insurance Group, Ltd.

- RSA Insurance Group plc

- FM Global

- Others

Recent Developments

- In July 2025, Chubb, Ltd. strengthened its agribusiness arm with expanded precision coverage for smart farm tech, including greenhouse sensors and automated climate controls. Building on their farm/ranch expertise, Chubb now offers tailored protection against equipment failure in IoT-enabled greenhouses, helping operators avoid costly downtime from tech glitches or weather hits.

- In June 2025, The Hartford Financial Services Group partnered with research groups on climate modeling tools that feed into smart greenhouse policies, predicting risks like extreme heat or floods for controlled environments. This boosts their inland marine endorsements for high-value crops, giving growers reliable coverage that matches real-time data from greenhouse systems.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 1.8 Billion |

| Forecast Revenue (2034) | USD 6.1 Billion |

| CAGR(2025-2034) | 12.7% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics, and Emerging Trends |

| Segments Covered | By Coverage Type (Property & Infrastructure Insurance, Crop & Produce Insurance, Equipment & Technology Breakdown Insurance, Others), By Greenhouse Type (Commercial Hydroponic/Aeroponic Farms, Commercial Traditional Soil-Based Greenhouses, Research & Educational Facilities), By Policy Duration (Annual/Multi-Year Policies, Seasonal/Percrop Cycle Policies), By End-User (Large Commercial Growers, SME & Independent Growers, AgTech Startups & Vertical Farms) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Chubb, Ltd., AXA SA, Zurich Insurance Group, Ltd., Allianz SE, American Financial Group, Inc., Tokio Marine Holdings, Inc., Sompo Holdings, Inc., Munich Re, Swiss Re, Ltd., ICAT, Farmers Insurance Group, The Hartford Financial Services Group, Inc., QBE Insurance Group, Ltd., RSA Insurance Group plc, FM Global, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |