Quick Navigation

Report Overview

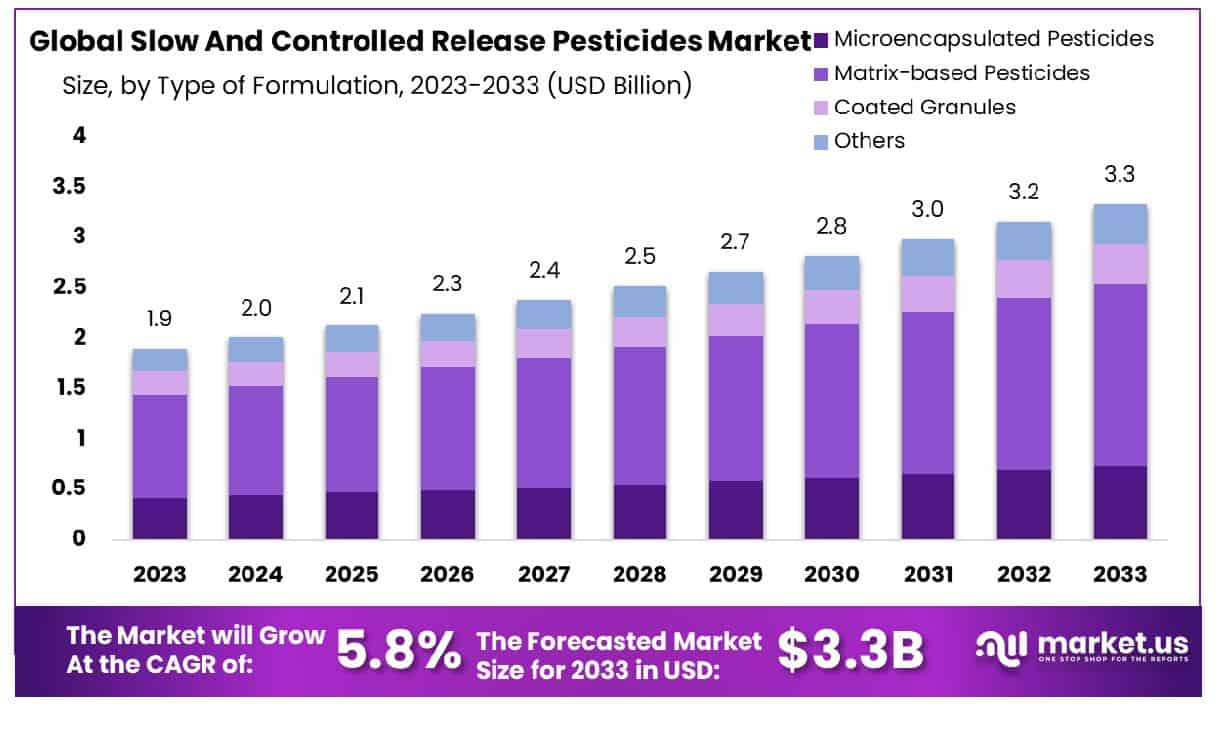

The Global Slow And Controlled Release Pesticides Market size is expected to be worth around USD 3.3 Billion by 2033, From USD 1.9 Billion by 2023, growing at a CAGR of 5.8% during the forecast period from 2024 to 2033.

The Slow and Controlled Release Pesticides Market encompasses products designed to distribute active ingredients in a measured manner over time. This approach enhances the efficacy of pesticides, reduces the frequency of application, and mitigates environmental impact. Such pesticides are encapsulated or chemically altered to ensure a delayed release, targeting specific phases of pest life cycles with precision.

The market’s significance lies in its contribution to sustainable agricultural practices, offering substantial benefits in crop yield and protection. As regulatory pressures and environmental concerns rise, this market is increasingly vital for companies aiming to meet global food demands while adhering to stringent environmental standards.

The Slow and Controlled Release Pesticides Market is poised for notable growth, driven by the escalating demand for sustainable agricultural practices and stringent environmental regulations. This market segment benefits significantly from innovations aimed at reducing the frequency of pesticide applications while enhancing the efficacy and safety of these products.

The ability of slow and controlled release formulations to minimize leaching and volatilization losses, thereby improving crop yield and reducing non-target exposure, is a key factor catalyzing their adoption. Moreover, the market is further supported by the increasing resistance towards conventional pesticides, which compels farmers to adopt more advanced solutions.

Supporting Data: In the European context, the four largest EU agricultural producers—France, Spain, Germany, and Italy—have consistently accounted for over two-thirds of total EU pesticide sales annually from 2011 to 2022. This robust demand underscores a substantial market opportunity for slow and controlled-release pesticides in these regions.

Additionally, with ‘fungicides and bactericides’ being the most sold category of pesticides, making up 43% of total sales in 2022, there is a significant potential for the development of slow-release formulations in this category, which could drive further market expansion.

Key Takeaways

- The Global Slow And Controlled Release Pesticides Market is projected to grow from USD 1.9 Billion in 2023 to USD 3.3 Billion by 2033, at a 5.8% CAGR.

- Asia-Pacific leads with a 38% market share, valued at USD 0.7 billion.

- Microencapsulated pesticides dominate with a 45.5% market share in formulations.

- Insecticides lead by mode of action, capturing 52.3% market.

- Grains and cereals are prominent, constituting 45.6% of crops.

- Large-scale commercial farms are major users, holding 67.4% share.

Driving Factors

Increasing Demand for High-Efficiency Agrochemicals

The demand for high-efficiency agrochemicals significantly contributes to the expansion of the Slow And Controlled Release Pesticides Market. With the global population projected to reach 9.7 billion by 2050, the pressure on agricultural productivity is intensifying. This demographic trend necessitates the adoption of more efficient pest control solutions that offer prolonged effectiveness and reduce the frequency of applications.

Slow and controlled-release pesticides meet this demand by ensuring consistent delivery of active ingredients, thereby enhancing pest management and reducing environmental impact. As these formulations provide precise control over pesticide release, they optimize plant uptake and minimize chemical run-off, aligning with the global push towards sustainable agricultural outputs.

Growing Adoption of Sustainable Farming Practices

Sustainable farming practices are rapidly gaining traction globally, driven by environmental concerns and regulatory policies advocating for reduced chemical use in agriculture. This shift is a pivotal growth lever for the Slow And Controlled Release Pesticides Market.

Farmers are increasingly adopting these innovative formulations as part of an integrated pest management (IPM) strategy that promotes environmental safety and agricultural sustainability. By extending the duration of pest control while using fewer chemicals, slow and controlled-release pesticides play a crucial role in sustainable agriculture, appealing to a market that is progressively sensitive to ecological and safety standards.

Enhanced Crop Yield and Profitability

Enhancing crop yield and profitability remains a primary focus for the agricultural sector, influencing the adoption of advanced agrochemical solutions. Slow and controlled release pesticides directly contribute to this objective by improving the efficacy of pest control measures. These products ensure a steady, controlled release of pesticides, which leads to better crop protection chemicals over an extended period, reduced damage from pests, and significantly lower chances of resistance development.

Consequently, farmers benefit from higher yields and improved quality of produce, which translates to greater profitability. The economic advantages provided by these pesticides, coupled with their efficiency and sustainability, underscore their integral role in the modern agricultural industry.

Restraining Factors

High Costs Associated with Development and Production

The development and production of slow and controlled-release pesticides involve significant costs, which act as a major restraining factor in the market’s growth. The formulation of these pesticides requires advanced technologies and specialized materials to encapsulate the active ingredients, leading to higher research and development (R&D) expenditures compared to conventional pesticides. Additionally, the production process is more complex and requires stringent quality control to ensure the consistent efficacy of the final product over time.

These elevated costs can limit the adoption of slow and controlled-release pesticides, particularly among small to medium-sized smart farming operations in developing regions, where budget constraints are more pronounced. Consequently, the high initial investment needed for these advanced pesticides can restrict their market penetration and overall growth.

Strict Regulatory Frameworks Governing Pesticide Use

Strict regulatory frameworks governing pesticide use present another significant barrier to the growth of the Slow And Controlled Release Pesticides Market. Regulatory bodies worldwide, such as the Environmental Protection Agency (EPA) in the United States and the European Food Safety Authority (EFSA) in the European Union, impose rigorous testing and approval processes on new pesticide products. These processes are designed to ensure safety for human health and the environment but can be lengthy and costly.

The stringent requirements for registration, coupled with the need for extensive data on environmental impact and toxicity, can delay the introduction of new slow and controlled-release products to the market. Moreover, changes in regulatory policies or enhancements in safety standards may necessitate further modification and testing of existing products, adding to costs and reducing the agility of pesticide manufacturers in responding to market needs. This regulatory environment, while necessary for safety and environmental preservation, can inadvertently slow down the innovation and commercialization of new and potentially more environmentally friendly pesticide technologies.

By Type of Formulation Analysis

Microencapsulated pesticides constitute 45.5%, highlighting their significant market share in 2023.

In 2023, Microencapsulated Pesticides held a dominant market position in the “By Type of Formulation” segment of the Slow and Controlled Release Pesticides Market, capturing more than a 45.5% share. This segment includes various formulations, such as Matrix-based Pesticides, Coated Granules, and other types. The substantial market share of Microencapsulated Pesticides can be attributed to their enhanced effectiveness in delivering active ingredients in a controlled manner, thereby reducing the frequency of applications and minimizing environmental impact.

Matrix-based Pesticides followed, contributing significantly to market dynamics. These formulations encapsulate pesticides within a polymer matrix, releasing the active ingredients slowly over time to target pests effectively and sustainably. The adoption of Matrix-based Pesticides is driven by the increasing regulatory pressures on environmental safety and pesticide residues.

Coated Granules also played a crucial role in the market. These are designed to release pesticides at a controlled rate due to the protective coating that regulates the dissolution of active ingredients. This technology is particularly valued in agricultural practices where precision and reduction of runoff are critical.

Other formulations in the segment include various innovative and less conventional types that cater to niche market needs, emphasizing customized pest management solutions and reduced environmental footprint.

By Mode of Action Analysis

Insecticides dominate with 52.3%, reflecting their critical role in pest control solutions.

In 2023, Insecticides held a dominant market position in the “By Mode of Action” segment of the Slow and Controlled Release Pesticides Market, capturing more than a 52.3% share. This segment also encompasses Herbicides and Fungicides, each contributing uniquely to the market’s structure and dynamics.

The prominent position of Insecticides within the market can be largely attributed to the critical need for managing pest populations in major agricultural and horticultural sectors. The controlled release technology used in these insecticides enhances their effectiveness by prolonging the activity period against target pests, reducing the need for frequent reapplication, and minimizing environmental toxicity.

Herbicides constituted the next significant category, driven by the extensive use of these products in large-scale farming and landscaping industries to combat weed growth. Controlled-release formulations are increasingly favored in herbicides to prevent crop damage and ensure sustained action against resistant weed species.

Fungicides in controlled release forms have also seen substantial adoption, particularly in environments where prolonged fungal protection is necessary. These formulations help in the steady release of fungicides, which is crucial for protecting crops throughout critical growth phases, thus ensuring better yield and quality of produce.

By Crop Type Analysis

Grains and cereals account for 45.6%, indicating their importance in pesticide application.

In 2023, Grains and Cereals held a dominant market position in the “By Crop Type” segment of the Slow and Controlled Release Pesticides Market, capturing more than a 45.6% share. This segment also includes Fruits and Vegetables and Other crop types, each reflecting different market needs and application trends.

The significant share of Grains and Cereals can be attributed to the extensive global cultivation of crops such as rice, wheat, and maize, which are fundamental to food security. The application of slow and controlled-release pesticides in this sub-sector ensures prolonged protection against pests and diseases, optimizing crop yields and minimizing the need for frequent pesticide applications. This is particularly crucial in regions with high pest prevalence and large-scale agricultural operations.

Fruits and Vegetables form another vital category within this market segment. These crops generally require more precise and regulated pesticide applications due to their sensitivity and high economic value. Controlled release technologies in pesticides offer the benefit of protecting crops for extended periods without causing harm to the produce, thus supporting quality and yield.

The “Others” category encompasses a variety of crops, including cash crops and ornamentals, where tailored pest management solutions are crucial. The diverse needs of these crops drive the innovation and adoption of specialized controlled release pesticide formulations, addressing specific agricultural challenges and environmental conditions.

By End-user Analysis

Large-scale commercial farms comprise 67.4%, emphasizing their extensive use of slow and controlled-release pesticides.

In 2023, Large-scale Commercial Farms held a dominant market position in the “By End-user” segment of the Slow and Controlled Release Pesticides Market, capturing more than a 67.4% share. This segment also includes Smallholder Farmers, who represent a critical but distinct market component.

The substantial market share held by Large-scale Commercial Farms can be largely attributed to their significant investment capacities and the scale of their agricultural operations, which demand high efficiency and long-term pest control solutions. Slow and controlled release pesticide technologies align well with the needs of these large enterprises, offering prolonged protection, reduced labor costs, and minimized environmental impact through decreased runoff and less frequent applications.

Smallholder Farmers, while holding a smaller share of the market, represent a vital segment that benefits significantly from the adoption of slow and controlled release pesticides. These technologies can help small-scale farmers achieve better crop protection and yield improvements with fewer resources. However, the adoption rate in this group is often limited by higher initial costs and accessibility issues.

The dominance of Large-scale Commercial Farms in the market is driven by their ability to adopt new agricultural technologies quickly and at scale, which is essential for meeting the growing global demand for food production sustainably. The trend towards more sustainable and efficient farming practices, coupled with increasing regulatory support for environmentally friendly pesticides, is expected to maintain the growth momentum in this segment, benefiting both large-scale and smallholder farmers.

Key Market Segments

By Type of Formulation

- Microencapsulated Pesticides

- Matrix-based Pesticides

- Coated Granules

- Others

By Mode of Action

- Insecticides

- Herbicides

- Fungicides

By Crop Type

- Grains and Cereals

- Fruits and Vegetables

- Others

By End-user

- Large-scale Commercial Farms

- Smallholder Farmers

Growth Opportunities

Expansion in Emerging Markets

The expansion into emerging markets represents a significant growth opportunity for the global Slow And Controlled Release Pesticides Market in 2023. As agricultural sectors in these regions continue to modernize and increase their productivity, the demand for innovative and sustainable farming solutions is also rising. Emerging markets, characterized by rapid population growth and increasing food security concerns, are pivotal areas where slow and controlled release pesticides can make a substantial impact.

These products offer the dual benefits of enhancing crop yield and reducing the environmental footprint of agriculture, aligning with the global shift towards sustainable development. Furthermore, governments in these regions are increasingly supportive of technologies that contribute to sustainable agriculture, potentially offering incentives for the adoption of such advanced solutions. By capitalizing on these dynamics, companies in the slow and controlled release pesticides sector can tap into new revenue streams and strengthen their global market presence.

Development of Biodegradable and Eco-Friendly Formulations

In 2023, the development of biodegradable and eco-friendly formulations is another key area poised for growth within the Slow And Controlled Release Pesticides Market. Environmental sustainability continues to drive consumer and regulatory preferences, compelling pesticide manufacturers to innovate with safer, more sustainable products. Biodegradable formulations minimize residual environmental impact and are better aligned with the regulatory landscapes that prioritize ecological preservation.

By focusing on these eco-friendly solutions, manufacturers can not only meet stricter regulatory demands but also cater to the growing segment of environmentally conscious consumers and farmers. This shift towards greener pesticides is likely to expand market reach and enhance brand reputations, positioning companies as leaders in sustainable agricultural practices.

Latest Trends

Adoption of Nano-Encapsulation Technology

The adoption of nano-encapsulation technology marks a transformative trend in the global Slow And Controlled Release Pesticides Market for 2023. This cutting-edge technology involves encapsulating pesticide molecules within nano-scale carriers, which significantly enhances the precision, efficiency, and control of pesticide delivery. Nano-encapsulation not only improves the solubility and stability of active ingredients but also allows for targeted delivery, which reduces the number of chemicals used and diminishes non-target exposure.

This method aligns with the increasing regulatory and market demands for reduced environmental impact and greater user safety. By adopting nano-encapsulation, companies can offer products that are not only more effective in terms of pest management but also more acceptable to environmentally conscious stakeholders. As a result, this technology is expected to drive competitive advantage, fostering innovation and differentiation in the market offerings.

Increased R&D Investments in Bio-Based Pesticides

Another significant trend shaping the Slow And Controlled Release Pesticides Market in 2023 is the increased investment in research and development (R&D) for bio-based pesticides. With a growing emphasis on sustainability and organic farming, the demand for bio-pesticides that can be integrated into eco-friendly farming practices is rising. Bio-based pesticides, derived from natural materials, offer a highly favorable profile in terms of environmental and human safety.

R&D investments are being channeled towards enhancing the efficacy, stability, and longevity of these bio-pesticides through slow and controlled release mechanisms. This investment is crucial in meeting the stringent efficacy and safety standards required for market acceptance. As the agricultural sector continues to evolve towards sustainable practices, the integration of advanced bio-based solutions is likely to capture significant market interest and investment, propelling the growth of the sector.

Regional Analysis

Asia-Pacific leads the Slow and Controlled Release Pesticides Market with 38%, valued at USD 0.7 Billion.

The slow and controlled release pesticides market demonstrates varied regional dynamics, with each geographic area contributing uniquely to global trends. Asia-Pacific stands as the dominating region, holding a substantial 38% market share, which translates to USD 0.7 billion. This significant proportion can be attributed to the increasing agricultural activities and the rising need for yield enhancement, driven by food security concerns among populous nations like China and India.

In North America, the market is characterized by advanced farming technologies and a robust regulatory framework promoting the use of environmentally friendly pesticides. These factors help in maintaining sustained growth in the demand for slow and controlled-release pesticides, supporting the market’s expansion.

Europe’s market is propelled by stringent regulations concerning pesticide use and a high level of environmental awareness among farmers. This region focuses on sustainable agricultural practices, hence fostering a steady demand for slow and controlled release formulations that minimize environmental impact.

The Middle East & Africa region shows promising growth potential, driven by the need to increase agricultural productivity and combat pest resistance. The market here is gradually adopting modern agricultural practices, incorporating controlled-release technologies to enhance crop yield and quality.

Latin America, with its vast agricultural lands and tropical climate, is becoming increasingly aware of the benefits of controlled-release pesticides. The region is witnessing growth in the adoption of these products, aimed at improving crop production and reducing pesticide leaching.

Key Regions and Countries

- North America

- The US

- Canada

- Mexico

- Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

- Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

- Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

Key Players Analysis

In the global slow and controlled release pesticides market of 2023, the competitive landscape is robust, featuring several key players that are central to industry advancements and market dynamics. Each company has contributed uniquely to market growth and technological innovations in the field.

Syngenta and BASF SE have consistently led the market in terms of investment in R&D, resulting in advanced formulations that promise both efficacy and environmental safety. Their products are tailored to meet the stringent regulatory standards across diverse global markets, which significantly enhances their competitive edge.

DAMA Agricultural Solutions Ltd. and Arysta LifeScience Corporation have carved niches in sustainable agriculture, focusing on solutions that are not only effective but also eco-friendly. Their commitment to sustainability has positioned them favorably as regulations tighten regarding chemical inputs in agriculture.

The Dow Chemical Company and DuPont are notable for their technological integration in product offerings, utilizing nanotechnology and advanced encapsulation methods that improve the precision and longevity of pesticide release. This technology-driven approach not only improves crop yield but also reduces the environmental impact of pesticide use.

Bayer AG and Monsanto Company continue to leverage their vast networks and substantial expertise in biotechnology to develop genetically modified crops that require less chemical intervention, promoting a more integrated approach to pest management.

Kingenta Group and Sumitomo Chemical Co., Ltd. focus on expanding their market presence in Asia, where the demand for increased agricultural productivity is coupled with rising awareness of sustainable farming practices. Their strategic market positioning and continual product innovation have enabled them to capture significant market shares in this region.

Market Key Players

- Syngenta

- DAMA Agricultural Solutions Ltd.,

- The Dow Chemical Company

- BASF SE

- Arysta LifeScience Corporation

- Monsanto Company

- Bayer AG

- DuPont,

- Kingenta Group

- Sumitomo Chemical Co. Ltd.

Recent Development

- In July 2023, The Dow Chemical Company announced a partnership with a tech startup to develop a precision application system for their controlled-release pesticide products. This collaboration aims to integrate advanced sensors and AI to optimize pesticide use, potentially reducing application rates by up to 25%.

- In March 2023, Syngenta launched a new line of slow-release pesticides, focusing on increased efficiency and reduced environmental impact. This product line offers a 40% longer field efficacy compared to previous formulations, demonstrating the company’s commitment to innovation and sustainability in agricultural practices.

- In January 2023, DAMA Agricultural Solutions Ltd. secured $5 million in funding in January 2023 to enhance their research and development capabilities. This investment aims to expand their portfolio of eco-friendly pesticide solutions, reflecting a strategic move towards sustainability within the industry.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 1.9 Billion |

| Forecast Revenue (2033) | USD 3.3 Billion |

| CAGR (2024-2033) | 5.8% |

| Base Year for Estimation | 2023 |

| Historic Period | 2018-2023 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type of Formulation(Microencapsulated Pesticides, Matrix-based Pesticides, Coated Granules, Others), By Mode of Action(Insecticides, Herbicides, Fungicides), By Crop Type(Grains and Cereals, Fruits and Vegetables, Others), By End-user(Large-scale Commercial Farms, Smallholder Farmers) |

| Regional Analysis | North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA |

| Competitive Landscape | Syngenta, DAMA Agricultural Solutions Ltd.,, The Dow Chemical Company, BASF SE, Arysta LifeScience Corporation, Monsanto Company, Bayer AG, DuPont, Kingenta Group, Sumitomo Chemical Co. Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Frequently Asked Questions (FAQ)

The Global Slow And Controlled Release Pesticides Market Size is USD 1.9 Billion in 2023.

The Global Slow And Controlled Release Pesticides Market is expected to grow at a CAGR of 5.8% (2024-2033).

Market.US has segmented the Global Slow And Controlled Release Pesticides Market by geographic (North America, Europe, APAC, South America, and Middle East and Africa). By Type of Formulation(Microencapsulated Pesticides, Matrix-based Pesticides, Coated Granules, Others), By Mode of Action(Insecticides, Herbicides, Fungicides), By Crop Type(Grains and Cereals, Fruits and Vegetables, Others), By End-user(Large-scale Commercial Farms, Smallholder Farmers)

The China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Rest of APAC are leading key areas of operation for Global Slow And Controlled Release Pesticides Market.

Syngenta, DAMA Agricultural Solutions Ltd.,, The Dow Chemical Company, BASF SE, Arysta LifeScience Corporation, Monsanto Company, Bayer AG, DuPont, Kingenta Group, Sumitomo Chemical Co. Ltd.