Quick Navigation

- Report Overview

- Key Takeaway

- Key Shopping Application Statistics

- Platform Analysis

- Business Model Analysis

- End User Analysis

- Deployment Model Analysis

- China Market Size

- Emerging Trend Analysis

- Growth Factors

- Key Market Segments

- Key Regions and Countries

- Drivers

- Restraint

- Opportunities

- Challenges

- Key Players Analysis

- Top Key Players in the Market

- Recent Developments

- Report Scope

Report Overview

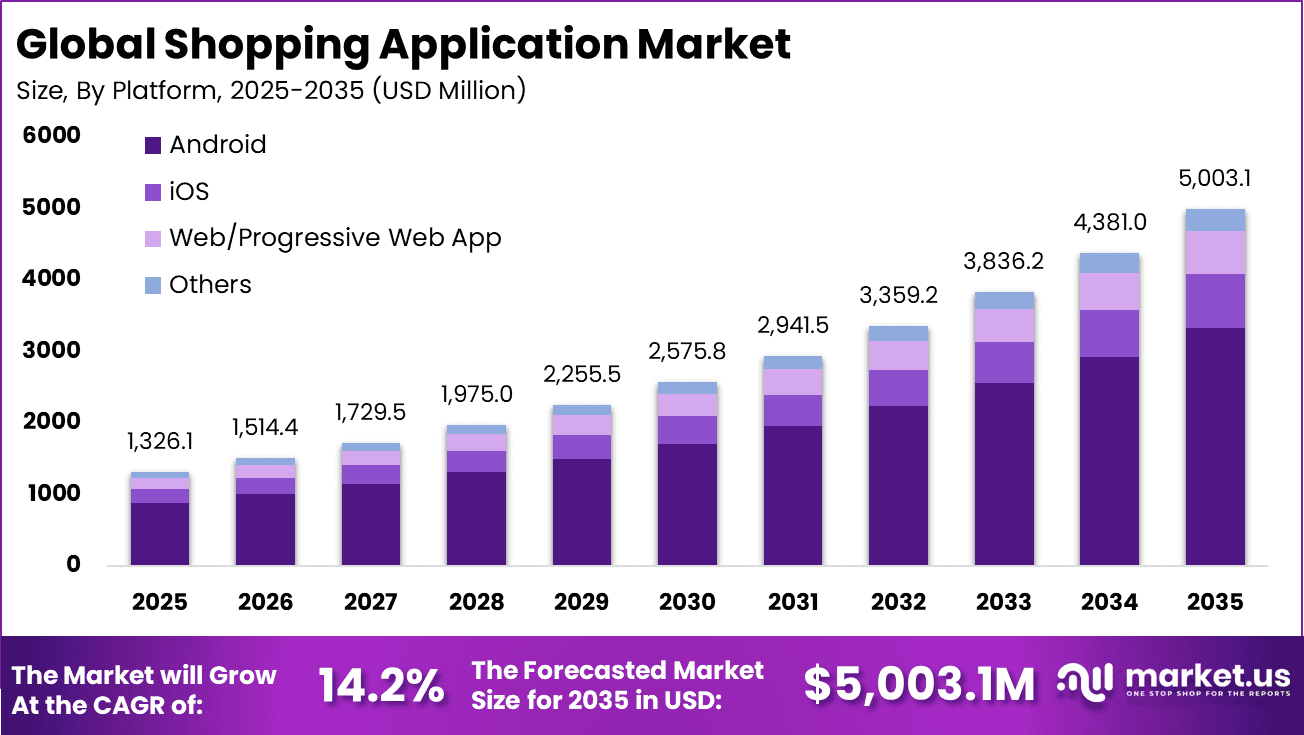

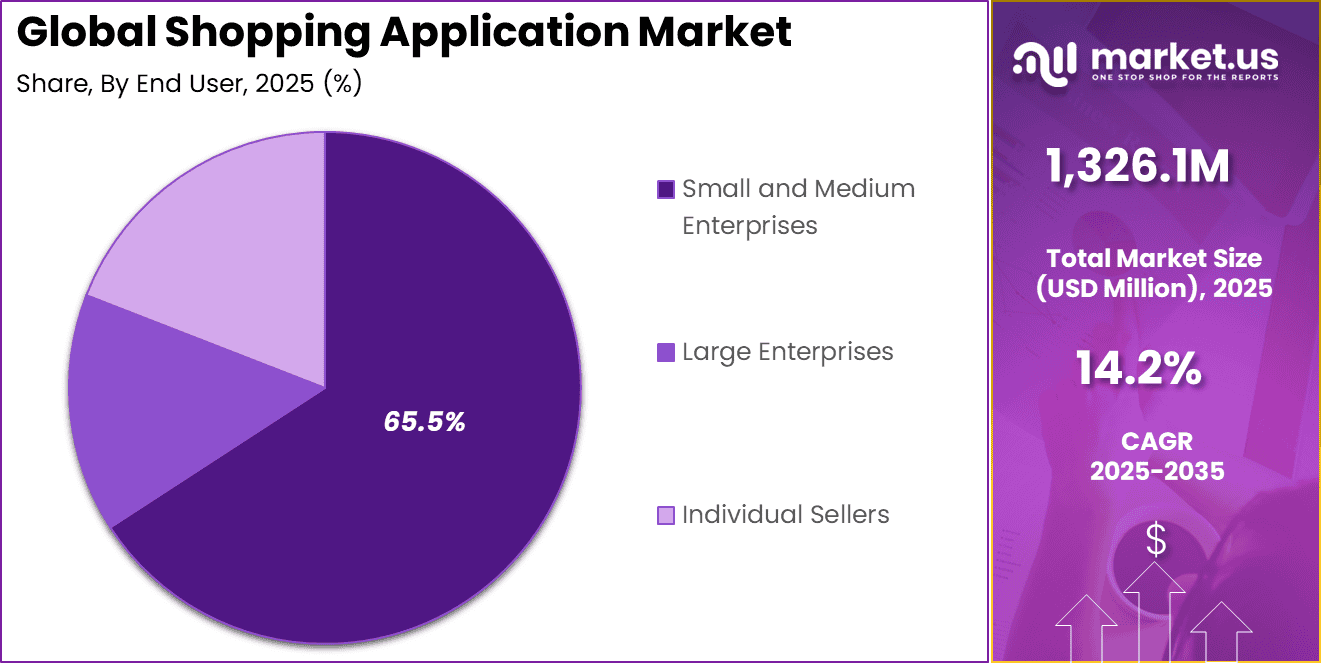

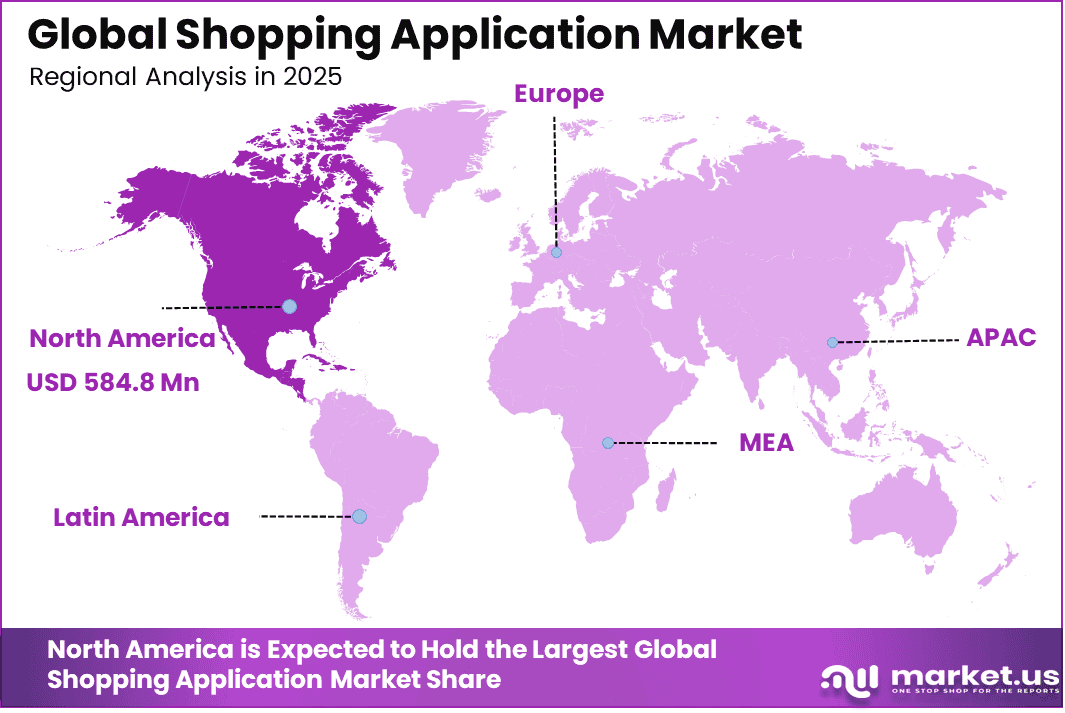

The Global Shopping Application Market size is expected to be worth around USD 5,003.1 million by 2035, from USD 1,326.1 million in 2025, growing at a CAGR of 14.2% during the forecast period from 2025 to 2035. Asia Pacific held a dominant market position, capturing more than a 44.1% share, holding USD 584.8 million in revenue.

A shopping application refers to a mobile based digital platform that allows users to browse products, compare options, place orders, and complete payments through smartphones or tablets. These applications provide a convenient and fast shopping experience, offering features such as personalized recommendations, order tracking, and secure payment systems for both consumers and businesses.

Shopping apps are gaining strong traction because 68% of users prefer easy access and quick interfaces over visiting physical stores. Widespread smartphone use and faster internet connections have made browsing and buying much easier. At the same time, 76% of users say trust in secure payment systems is a major reason they feel comfortable shopping through apps regularly.

The market for shopping applications is driven by the growing preference for convenient and fast mobile purchasing experiences. Consumers want easy access to products, secure payment options, and quick delivery support through a single platform. Businesses are also expanding app based services to improve customer engagement, build loyalty, and increase sales through personalized shopping journeys and real time interaction.

Demand for shopping apps continues to rise as mobile buying habits remain strong even after the pandemic period. Apps perform better than websites, with sales conversion rates running three times better and cart abandonment falling by 30%. Consumers with busy schedules prefer the convenience of shopping anytime, especially when buying everyday products and essential items through their phones.

For instance, in March 2026, Nykaa enhanced its app with AI‑driven skincare and makeup diagnostics, live‑streamed masterclasses, and geo‑targeted salon‑booking links, turning the beauty app into an experiential platform beyond simple transactions. The company is also testing quick‑commerce for beauty‑and‑personal‑care SKUs via app‑based hyperlocal delivery.

Key Takeaway

- The Android segment led the global shopping application market in 2025, accounting for 66.7% share, supported by its wide user base and strong presence across emerging markets.

- The B2C marketplace segment dominated by model, capturing 52.3% share, driven by increasing consumer preference for direct online purchasing platforms.

- Small and medium enterprises held a leading position with a 65.5% share, reflecting growing adoption of digital storefronts and mobile commerce solutions.

- Cloud-based deployment emerged as the dominant segment, accounting for 73.8% share, supported by scalability and ease of integration for app-based commerce platforms.

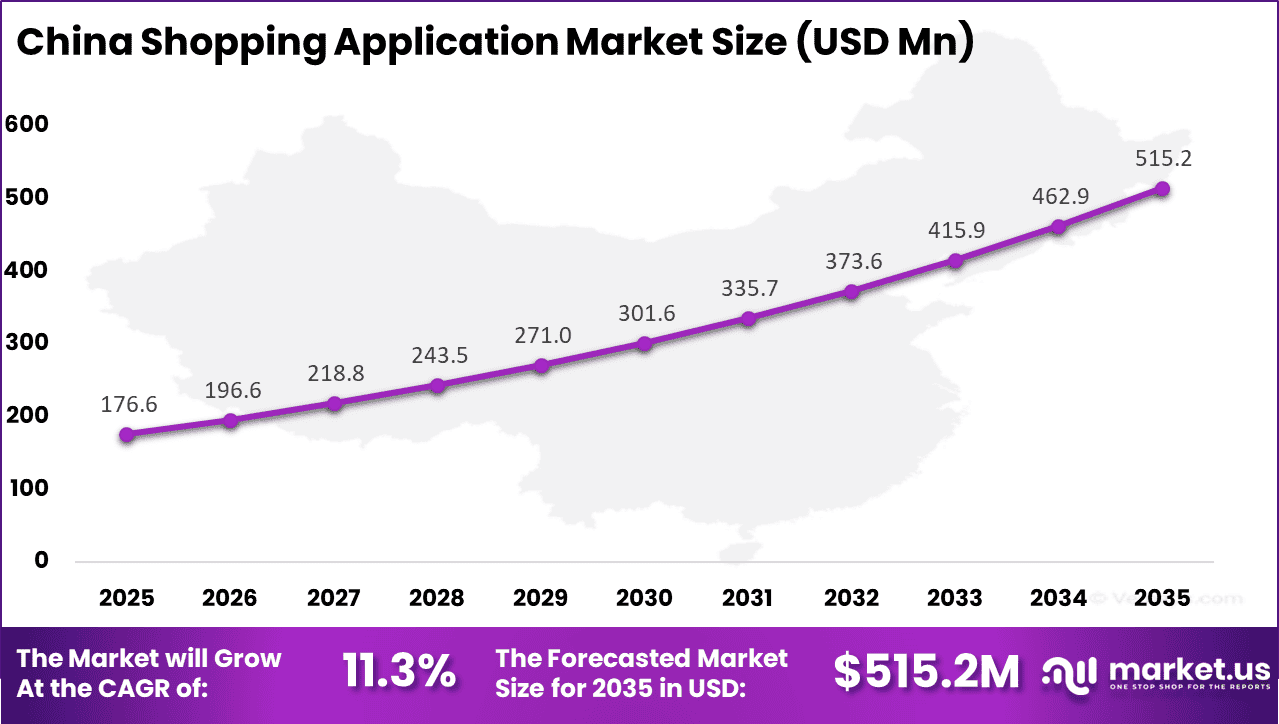

- The China shopping application market reached USD 176.6 million in 2025, expanding at a CAGR of 11.3%, driven by rapid growth in mobile commerce adoption.

- Asia Pacific maintained its leading position globally, capturing over 44.1% share, supported by a large consumer base and expanding digital infrastructure.

Key Shopping Application Statistics

- Shopping app usage remains consistent, with 15% of consumers using apps daily and 37% accessing them multiple times per week, indicating strong engagement levels.

- E-commerce app installs grew by 25% year over year, with rapid expansion in emerging regions such as LATAM (107%) and MENAT (152%), reflecting accelerating mobile commerce adoption.

- User penetration is particularly high among younger demographics, with 96% of individuals aged 18–44 having at least one shopping application installed.

- App-based commerce continues to outperform mobile web, delivering 66% higher transaction rates due to better user experience and personalization features.

- User engagement remains high, with nearly half of users checking apps multiple times daily and average session durations reaching 4.2 minutes.

- AI-driven shopping is gaining traction, as 75% of Gen Z consumers show interest in using AI to enhance their shopping experience.

- Cart abandonment remains a challenge, with 47% of users citing additional costs such as shipping and taxes as the primary reason for not completing purchases.

- Chinese platforms such as Temu and Shein continue to dominate global downloads and transaction growth, strengthening their position in international markets.

- Data sharing practices are widespread, with approximately 75% of shopping applications sharing user data with third parties, raising considerations around privacy and regulation.

- Personalization remains a key growth driver, particularly among younger users, where AI-based recommendations play a critical role in improving engagement and conversion rates.

Platform Analysis

In 2025, the Android platform led the Shopping Application market, capturing 66.7% share. This dominance is supported by the wide global adoption of Android devices, particularly in emerging markets. The availability of affordable smartphones and a large user base has made Android the preferred platform for shopping applications. Businesses focus on Android to reach a broader audience and maximize user engagement.

The open ecosystem of Android also supports faster app development and customization. Developers can easily integrate payment systems, personalized recommendations, and user-friendly interfaces. This flexibility enhances the overall shopping experience for consumers. As mobile commerce continues to grow, Android remains a key platform for digital retail expansion.

For Instance, in March 2026, Alibaba released an updated Android app for its international shoppers, integrating more localized payment options and AI‑powered product suggestions. JD.com also refreshed its Android experience with a smoother checkout flow and one‑tap reorders, both of which align with how Android users prefer quick, frictionless shopping rather than heavy‑handed interfaces.

Business Model Analysis

In 2025, the B2C marketplace segment held a leading 52.3% share in the Shopping Application market. This model allows businesses to directly connect with consumers through digital platforms, offering a wide range of products and services. Consumers prefer B2C marketplaces due to convenience, competitive pricing, and access to multiple brands in one place. This has significantly increased adoption across global markets.

The growth of digital payments and logistics infrastructure has further strengthened this segment. Businesses are able to provide faster delivery, easy returns, and personalized shopping experiences. B2C marketplaces also benefit from data-driven insights to improve customer engagement and retention. As online shopping becomes more mainstream, this model continues to dominate the market.

For instance, in February 2026, Walmart expanded its B2C marketplace on its mobile app, adding more third‑party sellers across electronics and home goods while keeping the same familiar interface. This blends the trust of a big brand with the variety of a real marketplace, which is exactly why the B2C model keeps drawing both shoppers and small vendors.

End User Analysis

In 2025, small and medium enterprises accounted for 65.5% share in the Shopping Application market. SMEs are increasingly using digital platforms to expand their reach and compete with larger players. Shopping applications provide these businesses with cost-effective tools to showcase products and connect with customers. This has enabled SMEs to participate actively in the digital economy.

The adoption is also driven by ease of onboarding and access to integrated services such as payments and logistics. SMEs benefit from reduced operational costs and improved visibility in online marketplaces. As digital adoption grows among smaller businesses, their contribution to the shopping application market continues to increase. This makes SMEs a key driver of market expansion.

For Instance, in January 2026, Shopify introduced a new set of tools inside its app for small businesses to manage listings, track orders, and respond to messages directly from their phones. This shift helps SMEs operate like larger brands without needing big teams or complex software, which is why so many use shopping apps as their primary storefront.

Deployment Model Analysis

In 2025, cloud-based deployment dominated the Shopping Application market with a 73.8% share. Businesses are increasingly adopting cloud solutions due to their scalability, flexibility, and cost efficiency. Cloud platforms allow companies to manage large volumes of transactions and user data without heavy infrastructure investment. This makes them ideal for rapidly growing e-commerce operations.

Cloud-based systems also support seamless updates, improved security, and integration with third-party services. Businesses can quickly adapt to changing consumer demands and scale operations as needed. The ability to deliver consistent performance across devices enhances the user experience. As digital commerce continues to expand, cloud deployment remains a critical component of shopping applications.

For Instance, in February 2026, Zalando upgraded its shopping platform to run mainly on cloud infrastructure, allowing it to push new features and regional updates without long downtimes. This shift supports the growing trend of cloud‑based deployment, where retailers want to scale quickly and keep the app running smoothly during peak traffic.

China Market Size

China plays a key role in this regional growth, with the market reaching USD 176.6 million and expanding at a CAGR of 11.3%. The growth is supported by strong digital infrastructure and high consumer engagement in online retail. Businesses are investing in mobile-first strategies to capture this demand. As e-commerce continues to expand, Asia-Pacific remains a leading region in the global market.

For instance, in January 2026, Alibaba solidified its dominance in shopping apps by launching advanced AI-driven personalization features across Taobao and Tmall platforms. These innovations boosted user engagement by 25% and cross-border sales in Southeast Asia, reinforcing Alibaba’s leadership in the region’s explosive e-commerce growth.

In 2025, the Asia Pacific held a dominant market position in the Global Shopping Application Market, capturing more than a 44.1% share, holding USD 584.8 million in revenue. This dominance is due to the large population base and rapid growth in smartphone and internet usage across countries such as China, India, and Southeast Asia.

Consumers in the region are highly active on mobile platforms and show a strong preference for app based shopping. The rise of digital payments and social commerce has further strengthened adoption, while continuous investments in logistics and delivery networks support faster and more reliable shopping experiences.

For instance, in December 2025, Flipkart dominated India’s shopping app market with quick-commerce rollout covering 100 cities, outpacing Amazon through localized 10-minute deliveries. This strategic push elevated its Asia Pacific position, capturing rising digital consumer demand amid festive sales frenzy.

Emerging Trend Analysis

Mobile-First Commerce and AI Personalization

A major trend in the Shopping Application Market is the shift toward mobile-first commerce, where a significant portion of online purchases now happens directly through apps rather than websites. Shopping apps are becoming central to digital retail, with a large share of transactions beginning and ending within mobile applications. This reflects changing consumer behavior, where convenience, speed, and app-based experiences are preferred over traditional channels.

Another important trend is the integration of artificial intelligence for personalization and real-time engagement. AI is being used to analyze user behavior, recommend products, and optimize pricing and promotions. This enables highly tailored shopping experiences, improving customer satisfaction and increasing conversion rates. As competition increases, personalization is becoming a critical differentiator for shopping applications.

Growth Factors

Mobile Commerce Expansion and Consumer Behavior Shift

The growth of the Shopping Application Market is strongly supported by the rapid expansion of mobile commerce. A significant share of global e-commerce revenue is now generated through mobile channels, indicating a clear shift toward app-based shopping. This trend is expected to continue as mobile usage increases and digital infrastructure improves globally.

Another key growth factor is the changing consumer preference for convenience and on-demand services. Users increasingly prefer quick browsing, one-click purchasing, and flexible delivery options offered by shopping apps. As consumer expectations evolve, shopping applications are becoming essential platforms for digital retail, supporting steady market expansion.

Key Market Segments

By Platform

- iOS

- Android

- Web/Progressive Web App

- Others

By Business Model

- B2C Marketplace

- Direct Retailer Apps

- C2C Platforms

- Subscription/Fee-based Apps

By End User

- Small and Medium Enterprises

- Large Enterprises

- Individual Sellers

By Deployment Model

- Cloud-based

- On-premise

- Hybrid

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Drivers

Mobile First Convenience

The shopping application market is growing because consumers want faster and simpler ways to shop. Mobile apps make it easy to browse products, compare prices, place orders, and complete payments from any location. This convenience fits well with modern lifestyles where speed and flexibility strongly influence buying decisions.

Apps also improve the customer journey through saved preferences, one-click checkout, order tracking, and instant alerts. These features reduce effort and save time for users. As more people rely on smartphones for everyday tasks, shopping applications continue to gain importance in both retail and service based transactions.

For instance, in March 2025, Amazon rolled out an updated mobile interface that prioritizes quick product discovery and one‑tap checkout for repeat buyers, cutting down several steps between browsing and payment. This built‑in speed and simplicity have made the app feel more like a daily habit than a destination, encouraging users to buy in short bursts during commutes or breaks rather than waiting for desktop sessions.

Restraint

Privacy Concerns

Privacy concerns remain a major restraint for the shopping application market because users share personal details, payment information, and browsing behavior through these platforms. Many consumers worry about how their data is stored and used. This uncertainty can reduce trust and make some users cautious about frequent app based purchases.

Concerns also increase when apps request access to location, contacts, or other phone data that may not seem necessary for shopping. If businesses fail to explain data use clearly, customer confidence can weaken. Strong privacy policies and secure data practices are becoming essential for maintaining user trust and long term engagement.

For instance, in February 2025, Alibaba’s AliExpress app updated its permission model to request more granular access to location, camera, and storage, prompting a wave of user complaints and media questions about data collection practices. In response, the company added clearer privacy pop‑ups and an in‑app dashboard to manage tracking settings, trying to balance functionality with user trust.

Opportunities

AI Personalization

AI personalization creates strong opportunities in the shopping application market by helping businesses deliver more relevant product suggestions and better user experiences. Apps can study browsing history, purchase patterns, and preferences to recommend suitable items. This improves convenience for users and helps sellers increase engagement through more targeted interactions.

Personalized shopping also supports higher conversion by showing the right products at the right time. Features such as smart search, tailored offers, and virtual assistance make the app experience more interactive and useful. As consumers expect more customized journeys, AI based personalization is becoming a valuable area for future growth.

For instance, in October 2025, Zalando enhanced its shopping app with an AI‑based style assistant that suggests complete outfits based on past purchases, saved items, and seasonal trends. This feature has turned casual browsing into more focused sessions, encouraging users to explore additional categories rather than sticking to repeat buys.

Challenges

Market Saturation

Market saturation is a growing challenge because many shopping applications now compete for the same users across similar product categories. Consumers already have access to several established apps, making it harder for new entrants to gain attention. This crowded environment increases pressure on businesses to differentiate their platforms in meaningful ways.

The challenge becomes greater when customer acquisition costs rise, and user loyalty becomes difficult to maintain. Apps must keep improving design, service quality, and promotional value to remain relevant. Without a clear advantage, many platforms struggle to retain active users and achieve long term growth in a highly competitive market.

For instance, in September 2025, Rakuten noticed that its marketplace app in Japan was losing share to specialized fashion and electronics platforms that offered a cleaner, category‑focused interface. In response, Rakuten streamlined its mobile layout, reduced clutter, and introduced more targeted cash‑back triggers to make the value proposition clearer in a crowded ecosystem.

Key Players Analysis

In the Shopping Application market, Amazon.com, Inc., Alibaba Group Holding Limited, and eBay Inc. remain major participants due to their large user bases and strong digital commerce ecosystems. These companies offer broad product selection, fast delivery support, and integrated payment systems that improve customer convenience. Walmart Inc., JD.com, Inc., and Shopify Inc. also hold a strong market position by combining retail reach, merchant support, and scalable mobile shopping capabilities.

Rakuten Group, Inc., Flipkart Private Limited, and MercadoLibre, Inc. play an important role in expanding regional and cross-border e-commerce activity. Their platforms are designed to support localized shopping experiences, seller onboarding, and efficient order fulfillment. Etsy, Inc., Pinduoduo Inc., and Zalando SE further strengthen the market by focusing on niche retail segments such as handmade goods, value-driven commerce, and fashion-led digital shopping.

Coupang, Inc., PT Tokopedia, ASOS plc, Wayfair Inc., ContextLogic Inc. (Wish), Myntra Designs Private Limited, Lazada Group S.A., and FSN E-Commerce Ventures Limited (Nykaa) add strong competitive depth to the market. These companies address different consumer needs across beauty, apparel, home goods, and value retail categories. Other key players continue to support market expansion through mobile-first innovation, personalized recommendations, and stronger logistics integration.

Top Key Players in the Market

- Amazon.com, Inc.

- Alibaba Group Holding Limited

- eBay Inc.

- Walmart Inc.

- JD.com, Inc.

- Shopify Inc.

- Rakuten Group, Inc.

- Flipkart Private Limited

- MercadoLibre, Inc.

- Etsy, Inc.

- Pinduoduo Inc.

- Zalando SE

- Coupang, Inc.

- PT Tokopedia

- ASOS plc

- Wayfair Inc.

- ContextLogic Inc. (Wish)

- Myntra Designs Private Limited

- Lazada Group S.A.

- FSN E-Commerce Ventures Limited (Nykaa)

- Others

Recent Developments

- In March 2026, Tokopedia bolstered its shopping‑app experience in Indonesia by integrating more TikTok‑style live‑stream commerce, one‑click local payments, and AI‑curated product walls inside the app. The platform also added stronger logistics transparency, showing real‑time pick‑and‑pack status, which helped reduce returns and increase trust in mid‑tier merchants.

- In March 2026, Myntra refreshed its app with AR‑powered virtual try‑ons for fashion and beauty items, layered on top of AI‑driven personalization that adjusted product feeds by season, occasion, and past behavior. The update aimed to reduce friction in discovery while protecting margins through bundled offers and quick‑ship guarantees.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1,326.1 Mn |

| Forecast Revenue (2035) | USD 5,003.1 Mn |

| CAGR (2026-2035) | 14.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Platform (iOS, Android, Web/Progressive Web App, Others), By Business Model (B2C Marketplace, Direct Retailer Apps, C2C Platforms, Subscription/Fee-based Apps), By End User (Large Enterprises, Small and Medium Enterprises, Individual Sellers), By Deployment Model (Cloud-based, On-premise, Hybrid) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Amazon.com, Inc., Alibaba Group Holding Limited, eBay Inc., Walmart Inc., JD.com, Inc., Shopify Inc., Rakuten Group, Inc., Flipkart Private Limited, MercadoLibre, Inc., Etsy, Inc., Pinduoduo Inc., Zalando SE, Coupang, Inc., PT Tokopedia, ASOS plc, Wayfair Inc., ContextLogic Inc. (Wish), Myntra Designs Private Limited, Lazada Group S.A., FSN E-Commerce Ventures Limited (Nykaa), Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |