Quick Navigation

Report Overview

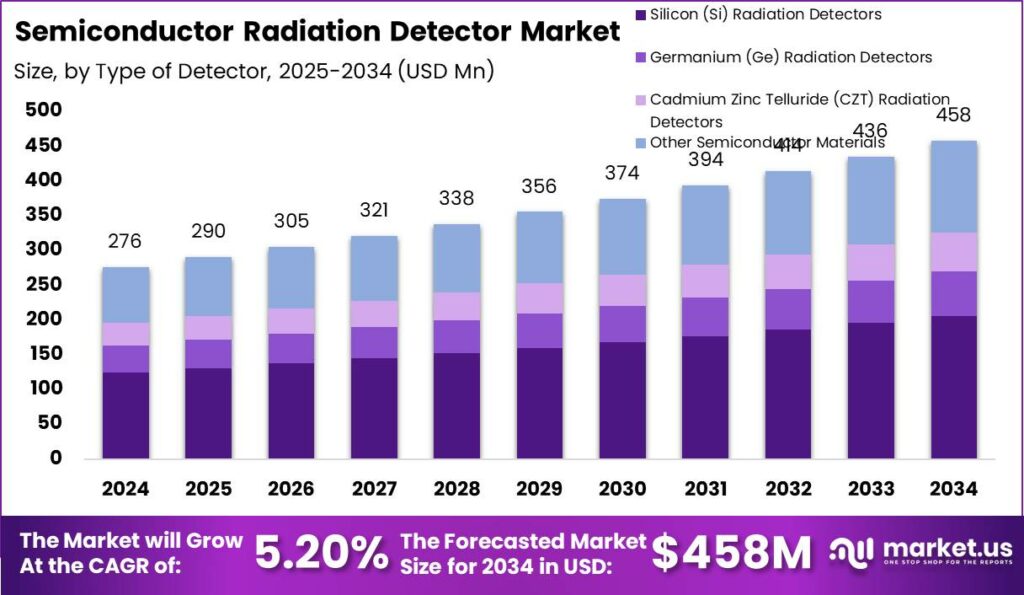

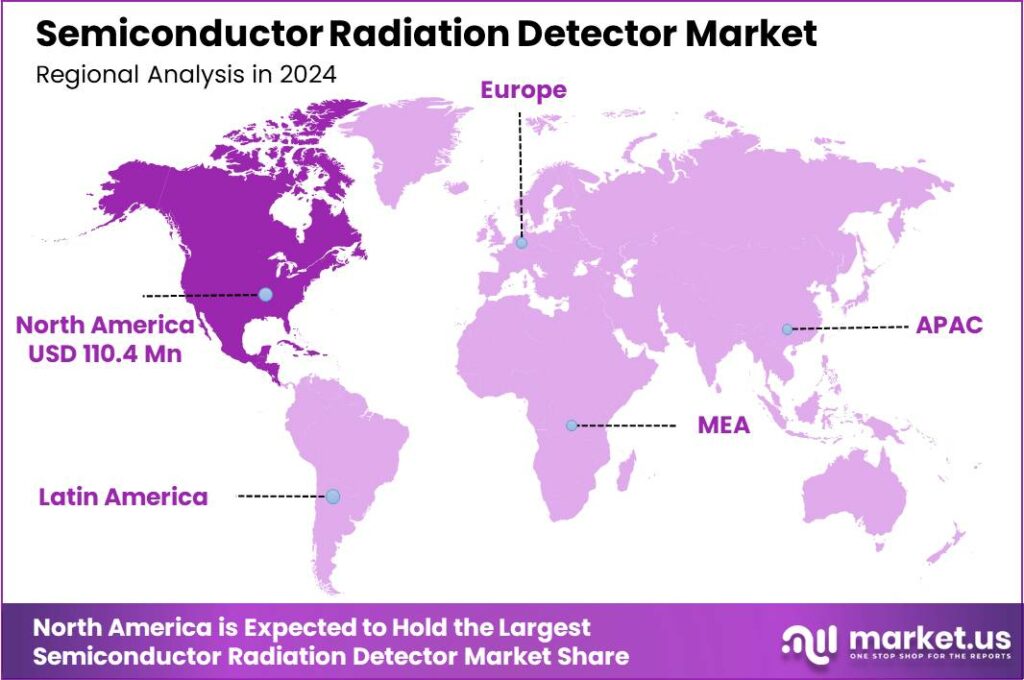

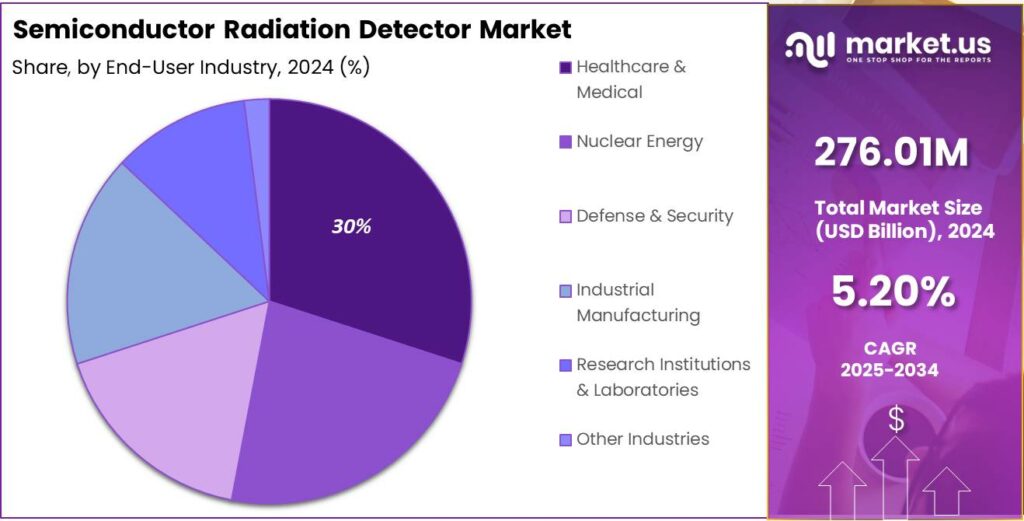

The Global Semiconductor Radiation Detector Market size is expected to be worth around USD 458 Million By 2034, from USD 276.01 Million in 2024, growing at a CAGR of 5.20% during the forecast period from 2025 to 2034. In 2024, North America dominated the global semiconductor radiation detector market, holding over 40% of the share, with a revenue of around USD 110.4 million.

A semiconductor radiation detector is a type of device used to detect and measure radiation in various forms, such as alpha, beta, gamma, and X-rays. These detectors are built using semiconductor materials, typically silicon or germanium, which are capable of converting the energy from incoming radiation into an electrical signal.

The semiconductor radiation detector market is growing due to rising demand for precise medical imaging technologies, like X-rays and CT scans, and increased need for radiation detection in expanding nuclear power plants. Advances in semiconductor materials, such as improved silicon and germanium crystals, have also enhanced detector performance, broadening their application appeal.

Rising environmental safety concerns and the need to monitor radioactive contamination are boosting demand for Silicon (Si) Radiation Detectors in environmental monitoring. Advances in particle physics and research further support market growth, while regulatory frameworks in healthcare and nuclear sectors reinforce the need for advanced radiation monitoring systems, driving expansion.

Semiconductor radiation detectors are popular for their high performance, durability, and ability to function in harsh environments. In critical sectors like nuclear power and space exploration, their reliability and efficiency make them essential. Miniaturization advancements have also increased their use in mobile devices, driving demand and accessibility.

The market has significant opportunities in expanding medical applications like radiation therapy and diagnostic imaging. Also, increasing demand for radiation monitoring in homeland security and environmental protection boosts market potential. The development of advanced detectors capable of sensing a wider range of radiation types also opens new applications and revenue streams.

As global demand for safety and sustainability rises, the semiconductor radiation detector market is expanding, particularly in developing regions. Growth is driven by the increasing number of nuclear plants and advancements in space exploration, such as more sensitive detectors, creating new business opportunities worldwide.

Key Takeaways

- The Global Semiconductor Radiation Detector Market size is expected to reach USD 458 Million by 2034, growing from USD 276.01 Million in 2024, with a CAGR of 5.20% during the forecast period from 2025 to 2034.

- In 2024, the Silicon (Si) Radiation Detectors segment held a dominant market position, capturing more than 45% of the overall market share.

- The Healthcare & Medical segment dominated the semiconductor radiation detector market in 2024, accounting for more than 30% of the total market share.

- In 2024, North America held a dominant position in the global semiconductor radiation detector market, capturing over 40% of the total market share, with a revenue of approximately USD 110.4 million.

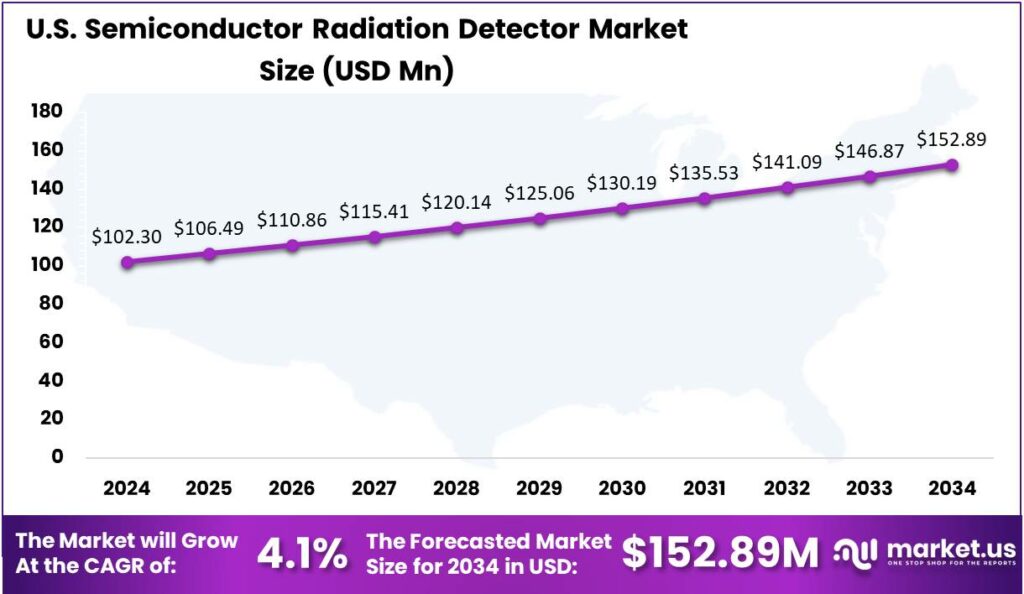

- The U.S. semiconductor radiation detector market is projected to reach USD 102.3 million by 2024, driven by growing demand across sectors like healthcare, defense, and nuclear power, with a CAGR of 4.1%.

U.S. Market Size

The U.S. semiconductor radiation detector market is projected to reach a value of USD 102.3 million by 2024, driven by increasing demand across various sectors such as healthcare, defense, and nuclear power. With a compound annual growth rate (CAGR) of 4.1%, the market is expected to expand steadily during the forecast period.

In recent years, the application of semiconductor radiation detectors has gained significant traction in medical diagnostics, particularly in imaging systems like computed tomography (CT) and positron emission tomography (PET) scanners.

The need for efficient radiation monitoring in the nuclear and defense industries further accelerates market demand. Additionally, the increasing emphasis on safety and security measures in nuclear power plants and environmental monitoring applications is expected to contribute to the market’s expansion.

In 2024, North America held a dominant position in the global semiconductor radiation detector market, capturing more than 40% of the total market share, equivalent to a revenue of approximately USD 110.4 million.

North America’s strong market presence is driven by advanced semiconductor technology, significant R&D investments, and high demand in healthcare, defense, and nuclear power. The region’s well-established infrastructure for manufacturing and distributing radiation detection devices solidifies its leadership in innovation and adoption.

The healthcare industry’s demand for accurate diagnostic imaging, including PET and CT scanners, has boosted the need for high-performance semiconductor radiation detectors in North America. Increased focus on radiation safety and strict regulations has driven further investments in advanced detection technologies, enhancing the region’s market leadership.

North America’s leadership in defense and nuclear power is driven by its strong semiconductor radiation detectors, vital for security and monitoring. The U.S., with its large defense budget, invests in tech upgrades for national security. Additionally, nuclear power plants, government agencies, and research institutions fuel demand for radiation detection systems to ensure safety and regulatory compliance.

Type of Detector Analysis

In 2024, the Silicon (Si) Radiation Detectors segment held a dominant market position, capturing more than 45% of the overall market share. Silicon detectors are widely regarded for their efficiency and cost-effectiveness, particularly in applications where high-resolution radiation measurement is required.

Silicon (Si) radiation detectors lead the market due to their high electron mobility, good energy resolution, and cost-effectiveness. These benefits make them ideal for applications requiring precise measurements at an affordable price, driving their dominance in medical imaging, security, and environmental monitoring.

Silicon detectors’ adaptability further strengthens their market dominance. Their easy integration into existing systems and scalability for various applications provide a competitive edge. The widespread availability of silicon-based technology, supported by a well-established supply chain, lowers production costs and boosts accessibility, driving continued adoption.

Silicon (Si) Radiation Detectors are expected to retain their dominance due to continuous advancements in material and detector technologies. Ongoing improvements in sensitivity, resolution, and performance will strengthen their position in key markets. With broad applicability, cost-effectiveness, and a proven track record, Silicon detectors are set to remain the preferred choice for radiation detection across various industries.

End-User Industry Analysis

In 2024, the Healthcare & Medical segment dominated the semiconductor radiation detector market, capturing more than 30% of the total market share. This leading position can be attributed to the growing demand for high-precision radiation detection technologies in medical imaging applications.

With the increasing reliance on diagnostic techniques such as positron emission tomography (PET) and computed tomography (CT) scans, the need for accurate and reliable radiation detectors has risen significantly. These detectors are essential for ensuring patient safety and the quality of diagnostic images, driving their widespread adoption across hospitals and healthcare facilities.

One of the primary drivers for the healthcare sector’s dominance in the market is the increasing prevalence of chronic diseases, particularly cancer, which necessitates more advanced and frequent diagnostic procedures. Semiconductor radiation detectors play a crucial role in improving the sensitivity and accuracy of imaging systems used to detect tumors, thereby enhancing early diagnosis and treatment outcomes.

Additionally, healthcare regulatory bodies, such as the FDA and other international organizations, have implemented stringent standards for radiation exposure during medical procedures. This has resulted in a heightened focus on the development of semiconductor-based detectors that offer higher precision, better safety features, and improved performance.

Key Market Segments

By Type of Detector

- Silicon (Si) Radiation Detectors

- Germanium (Ge) Radiation Detectors

- Cadmium Zinc Telluride (CZT) Radiation Detectors

- Other Semiconductor Materials (GaAs, CdTe, etc.)

By End-User Industry

- Healthcare & Medical

- Nuclear Energy

- Defense & Security

- Industrial Manufacturing

- Research Institutions & Laboratories

- Other Industries

Driver

Increasing Demand for Nuclear Energy

The demand for nuclear energy is a key driver for the semiconductor radiation detector market. Semiconductor radiation detectors are essential in monitoring and ensuring the safe operation of nuclear power plants by detecting radiation levels, identifying leaks, and preventing potential hazards.

The increasing number of nuclear power plants, especially in countries seeking to meet ambitious climate goals, directly contributes to the growing need for radiation detection technology. Furthermore, the need for safety protocols in industries such as healthcare, where nuclear technologies are used for diagnostics and treatment, also enhances demand for these detectors. As nuclear energy projects expand globally, the demand for reliable, high-performance radiation detection solutions is expected to continue to rise.

Restraint

High Initial Investment and Maintenance Costs

One of the significant restraints in the semiconductor radiation detector market is the high initial investment and ongoing maintenance costs associated with these devices. Advanced radiation detection systems often require significant upfront capital to purchase and install, which may discourage small and medium-sized enterprises (SMEs) from adopting this technology.

In addition to high initial costs, these systems require specialized maintenance and calibration to ensure their long-term functionality and accuracy, contributing to ongoing expenses.The high costs of installation and maintenance can limit the adoption of semiconductor radiation detectors, particularly in emerging markets with budget constraints. While the long-term benefits of enhanced safety and compliance are clear, the upfront financial investment remains a challenge for many organizations.

Opportunity

Integration of Semiconductor Radiation Detectors in IoT Systems

An emerging opportunity in the semiconductor radiation detector market lies in the integration of these detectors with the Internet of Things (IoT) systems. As industries look to optimize their safety protocols, the ability to connect radiation detectors to central monitoring systems allows for real-time data collection and remote monitoring.

This integration enables instant alerts and notifications, improving response times to potential radiation hazards and enhancing the overall efficiency of safety measures. The growth of smart cities, industrial automation, and digital transformation in sectors such as energy, healthcare, and security is creating a fertile ground for IoT-enabled radiation detection systems.

By leveraging IoT capabilities, semiconductor radiation detectors can be part of a larger network of interconnected safety systems, improving operational efficiency and safety standards across various industries.

Challenge

Technological Complexity and Calibration Requirements

One of the primary challenges in the semiconductor radiation detector market is the technological complexity involved in both the design and operation of these devices. These detectors require precise calibration to deliver accurate results, and the process of calibration can be time-consuming and complex.

The high level of expertise required for installation, maintenance, and calibration poses a barrier to adoption, particularly in regions where technical expertise may be lacking. The evolving radiation standards and regulations often require frequent updates and recalibrations, complicating maintenance. For manufacturers, ensuring compliance with these changing safety standards demands continuous innovation, increasing both the cost and operational complexity of semiconductor radiation detectors.

Emerging Trends

A key trend is the use of advanced semiconductor materials like high-purity germanium (HPGe) and silicon carbide (SiC), which provide superior energy resolution and enhanced radiation detection capabilities. These materials improve detector sensitivity and allow for the detection of a wider range of radiation types, including alpha, beta, gamma, and X-rays.

Additionally, integration with digital electronics and the advancement of software algorithms are reshaping semiconductor detectors. These advancements lead to more compact, portable systems that can be used in a wider array of applications, from mobile security scanners to medical imaging devices.

The trend toward hybrid detectors, which combine semiconductor materials with scintillators or other components, is also gaining traction due to their improved energy resolution and robustness in harsh environments. The growing demand for radiation protection in healthcare and increasing nuclear safety concerns are driving the expansion of radiation detection systems.

Business Benefits

Semiconductor radiation detectors offer significant benefits across industries, improving radiation monitoring and safety. In healthcare, they enable high-resolution imaging for better disease detection, such as cancer, leading to improved patient outcomes. Their energy efficiency also helps hospitals optimize equipment costs.

The integration of semiconductor radiation detectors in the defense and security industries enhances the ability to monitor radiation exposure, detect nuclear materials, and ensure public safety. This not only reduces the risks associated with radiation hazards but also increases compliance with international regulations governing nuclear safety.

Semiconductor detectors are crucial in the nuclear energy sector for continuous radiation monitoring within plants and surrounding areas. They enable early detection of abnormal radiation levels, preventing safety incidents and ensuring regulatory compliance, which is essential for both safety and operational success.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

The semiconductor radiation detector market is highly competitive, with several key players driving technological advancements and innovations.

Mirion Technologies is a global leader in radiation detection, providing high-performance semiconductor detectors used in medical, industrial, and nuclear sectors. The company stands out for its robust solutions designed for high radiation environments, providing accurate and reliable data essential for safety and research.

AMETEK is another key player in the semiconductor radiation detector market, recognized for its cutting-edge measurement instruments. The company offers a broad range of radiation detection solutions that cater to both commercial and scientific applications. AMETEK’s strength lies in its innovative sensor technologies, which combine high sensitivity with low energy consumption.

Hitachi, a leading global technology company, has established itself as a strong contender in the semiconductor radiation detection industry. Known for its precision engineering and advanced technology, Hitachi provides high-quality radiation detectors that are widely used in medical imaging and industrial radiation monitoring.

Top Key Players in the Market

- Mirion Technologies

- AMETEK

- Hitachi

- Kromek

- Rayspec

- Thermo Fisher Scientific Inc.

- Baltic Scientific Instruments

- Radlen Technologies

- Other Key Players

Top Opportunities Awaiting for Players

- Healthcare Sector Expansion: The healthcare sector’s demand for radiation detection devices is driven by medical imaging technologies like CT scans and PET. As early disease detection and personalized medicine gain focus, the need for high-resolution detectors grows, improving patient care and diagnostics.

- Nuclear Power Industry Growth: As countries embrace cleaner energy, nuclear power is crucial for reducing carbon footprints. Semiconductor radiation detectors are essential for plant safety, radiation monitoring, and regulatory compliance.

- Government Regulations and Safety Standards: Tighter radiation safety regulations in industries like mining, construction, and healthcare are increasing demand for advanced detection technologies. As compliance becomes mandatory, businesses must invest in state-of-the-art detectors.

- Security and Defense Applications: Rising geopolitical tensions and concerns over nuclear threats have boosted demand for radiation detection systems in security and defense. Semiconductor detectors are crucial in border control, port security, and military defense, helping to monitor radioactive materials and prevent nuclear proliferation, vital for national security.

- Technological Advancements in Detector Performance: Advancements in semiconductor materials like GaN and SiC are enhancing radiation detectors with better resolution, faster response, and improved durability.

Recent Developments

- In December 2024, China has introduced a compact radiation detection chip to boost semiconductor self-reliance. Capable of monitoring radiation doses in diverse environments, it adapts to settings like nuclear workplaces, personnel safety, and environmental inspections.

- In September 2024, Canon Inc. announced the acquisition of Redlen Technologies, a British Columbia-based semiconductor company, for $341 million CAD. This move is part of Canon’s plan to expand into the medical business and accelerate the development of competitive PCCT (Photon-counting computed tomography) systems

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 276.01 Mn |

| Forecast Revenue (2034) | USD 458 Mn |

| CAGR (2025-2034) | 5.20% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Type of Detector (Silicon (Si) Radiation Detectors, Germanium (Ge) Radiation Detectors, Cadmium Zinc Telluride (CZT) Radiation Detectors, Other Semiconductor Materials (GaAs, CdTe, etc.)), By End-User Industry (Healthcare & Medical, Nuclear Energy, Defense & Security, Industrial Manufacturing, Research Institutions & Laboratories, Other Industries) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Mirion Technologies, AMETEK, Hitachi, Kromek, Rayspec, Thermo Fisher Scientific Inc., Baltic Scientific Instruments, Radlen Technologies, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |