Quick Navigation

- Report Overview

- Key Takeaways

- Analysts’ Viewpoint

- Impact of AI

- China Market Growth

- Technology Node Analysis

- Industry Vertical Analysis

- Key Market Segments

- Driver

- Restraint

- Opportunity

- Challenge

- Growth Factors

- Emerging Trends

- Business Benefits

- Key Regions and Countries

- Key Player Analysis

- Recent Developments

- Report Scope

Report Overview

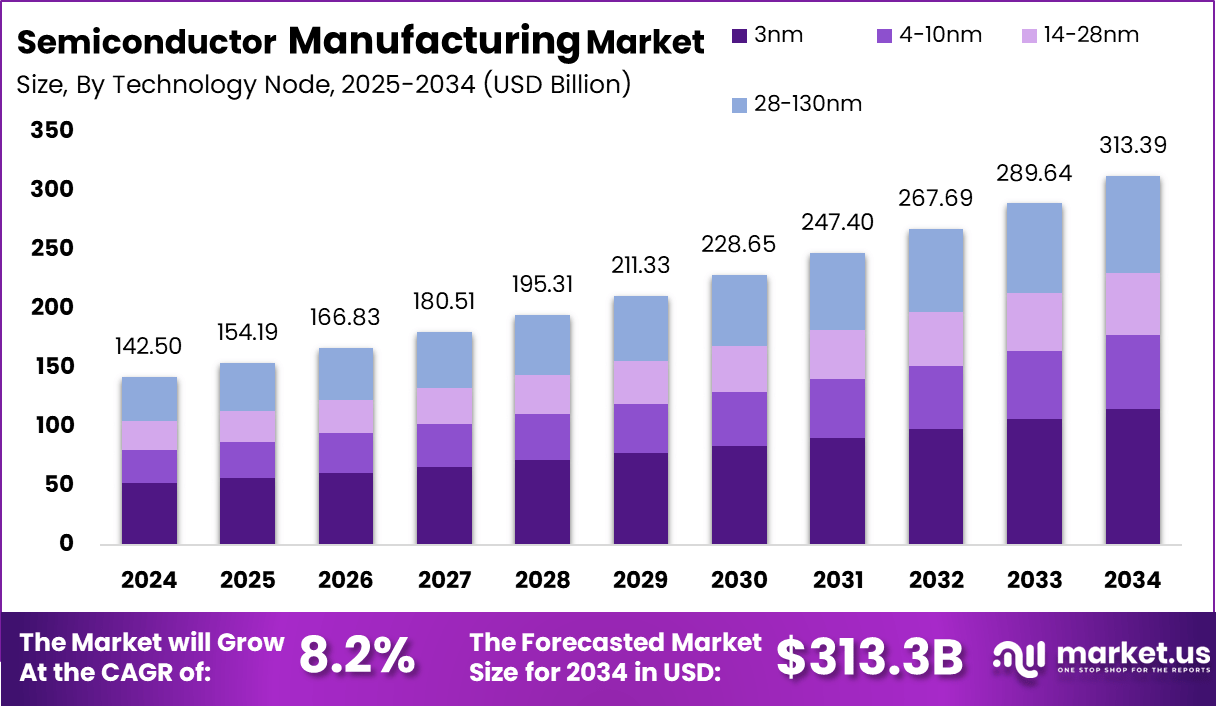

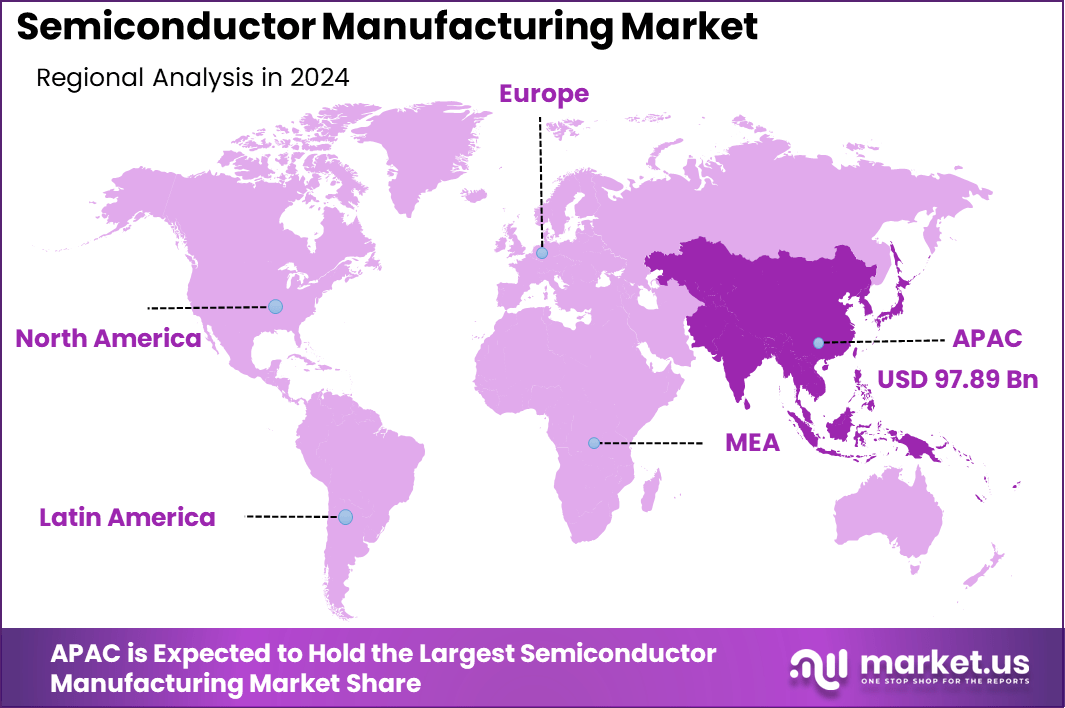

The Global Semiconductor Manufacturing Market size is expected to be worth around USD 313.39 Billion By 2034, from USD 142.50 billion in 2024, growing at a CAGR of 8.2% during the forecast period from 2025 to 2034. In 2024, APAC held a dominant market position, capturing more than a 68.7% share, holding USD 97.89 Billion revenue.

Semiconductor manufacturing is a detailed and intricate process that involves converting raw materials, such as silicon, into integrated circuits (ICs). This process is characterized by several complex steps, including wafer fabrication, testing, assembly, and packaging. Each stage is crucial for the successful production of high-quality semiconductor devices.

The semiconductor manufacturing market plays a vital role in the global economy, with its impact evident across various technological sectors. The demand for semiconductors is driven primarily by their essential role in a wide range of consumer electronics, computing hardware, and telecommunications infrastructure.

The market’s growth is supported by ongoing technological advancements that allow for the production of increasingly efficient and miniaturized semiconductor devices. Major players in the market include Intel Corporation, Taiwan Semiconductor Manufacturing Company (TSMC), Samsung Electronics, and NVIDIA Corporation, each contributing to innovations and expansions in semiconductor technology.

The primary drivers of the semiconductor manufacturing market include technological advancements, the increasing complexity of consumer and industrial electronics, and the global expansion of digital infrastructure. The demand for smaller, more efficient semiconductor components is continually rising, partly due to the growing needs of mobile technology and the Internet of Things (IoT).

The Semiconductor Industry Association (SIA) disclosed that global semiconductor sales reached $54.9 billion in February 2025, marking a significant 17.1% increase from February 2024’s $46.9 billion. This figure, however, shows a slight decline of 2.9% from January 2025’s sales of $56.5 billion. Sales figures, compiled by the World Semiconductor Trade Statistics (WSTS) organization, reflect a three-month moving average, underscoring the industry’s robust performance.

Looking ahead, the global semiconductor market is poised for substantial growth, projected to escalate from $600 billion to a staggering $2 trillion over the next seven years, according to Krishna Bodanapu, Executive Vice Chairman and MD of Cyient. India emerges as a key player, ready to enhance its semiconductor production capabilities, particularly in chip design, where it claims about 20% of the global market share.

A 2024 report from Electronics Weekly highlighted growth in the front-end semiconductor equipment sector. Notably, wafer processing equipment sales saw an uptick of 9%, while other front-end segments recorded a 5% increase. Moreover, the assembly and packaging equipment sector experienced a remarkable 25% growth, and test equipment billings surged by 20%, year-over-year. Such advances are crucial for supporting emerging advanced technologies.

Key Takeaways

- The global semiconductor manufacturing market is projected to reach approximately USD 313.39 billion by 2034, rising from an estimated USD 142.50 billion in 2024. This growth reflects a compound annual growth rate (CAGR) of 8.2% over the forecast period from 2025 to 2034.

- In 2024, the Asia-Pacific (APAC) region dominated the global market, capturing a market share of over 68.7%, which translated to a revenue of approximately USD 97.89 billion.

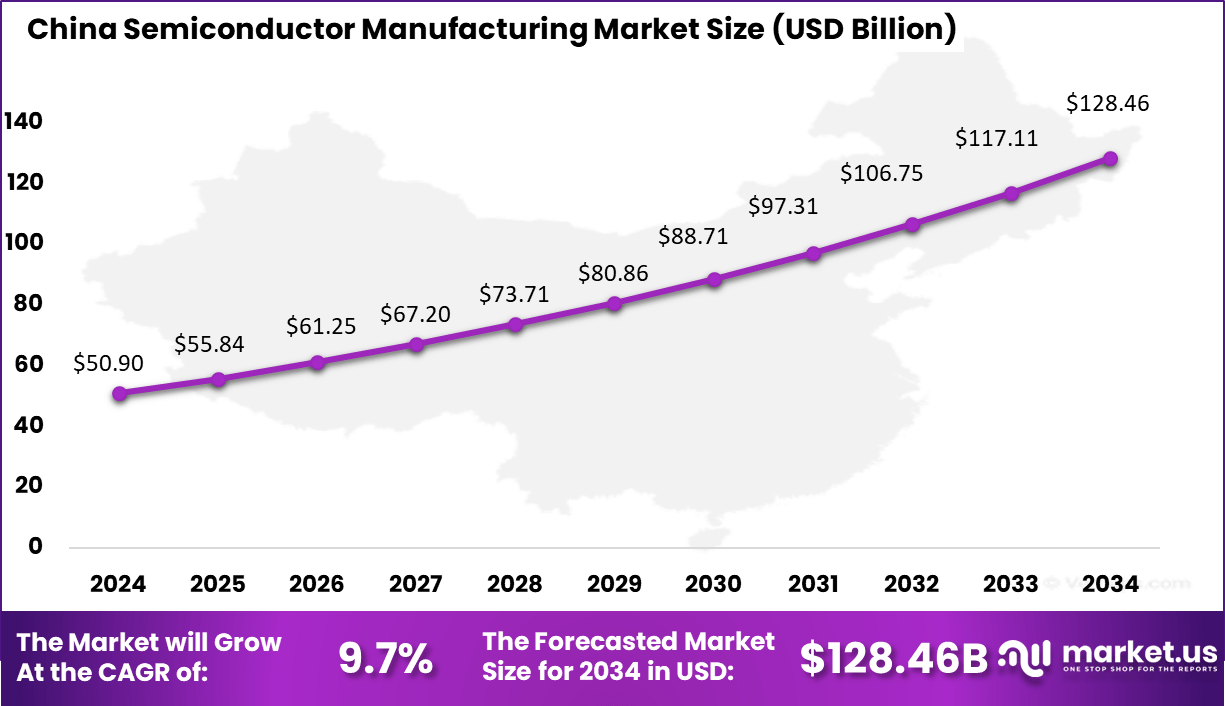

- China’s semiconductor manufacturing market was valued at approximately USD 50.90 billion in 2024.

- The market is forecasted to rise to USD 55.84 billion in 2025 and further reach USD 128.46 billion by 2034, growing at a robust CAGR of 9.7%.

- The 3nm node accounted for approximately 36.7% of the global semiconductor manufacturing market share.

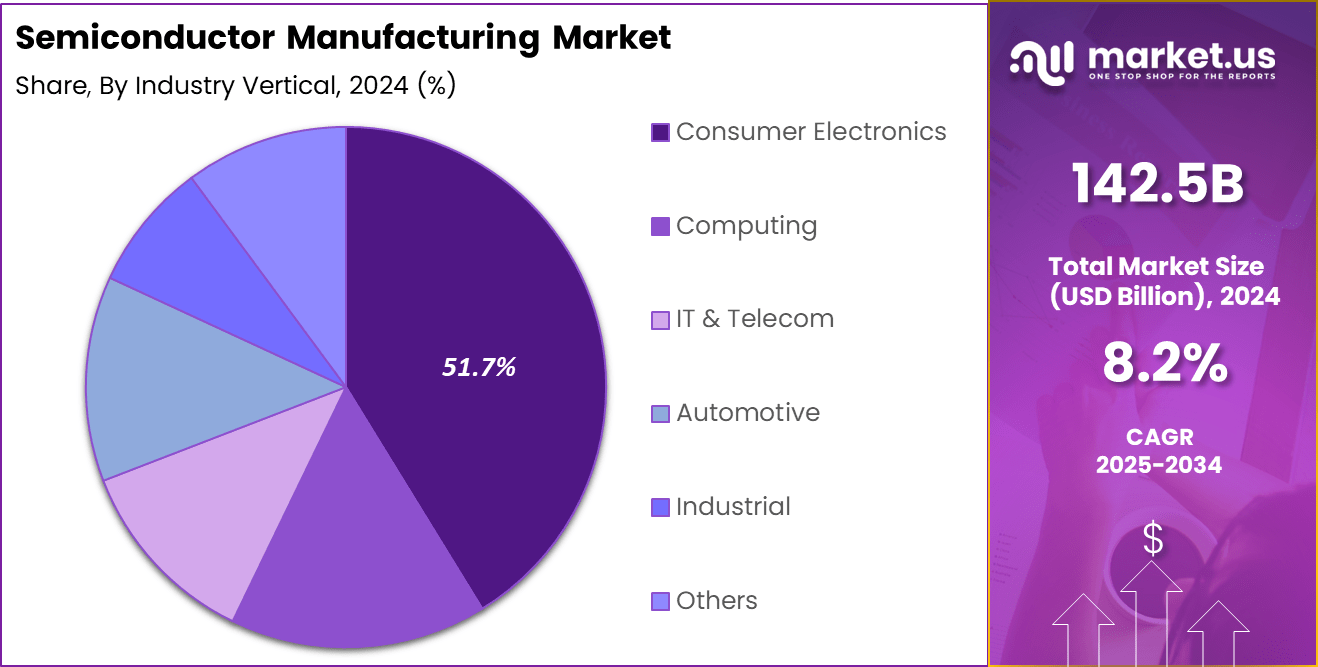

- The consumer electronics sector emerged as the leading end-user, accounting for 51.7% of the total market share.

Analysts’ Viewpoint

Investing in semiconductor manufacturing is increasingly seen as strategically important for countries and companies aiming to secure their technological futures. The construction and operation of semiconductor fabrication plants (fabs) are capital-intensive but offer significant long-term benefits, including job creation, technological leadership, and enhanced supply chain resilience.

According to Market.us’s research, the global semiconductor market is set to undergo substantial growth, with forecasts indicating an increase from USD 530 billion in 2023 to USD 996 billion by 2033, achieving a steady CAGR of 6.5%. Particularly in 2023, the APAC region dominated the market, accounting for over 63.91% of the market share and generating revenues of USD 388.7 billion.

Companies that invest in cutting-edge manufacturing technologies can achieve higher yield rates, better quality control, and faster time-to-market for new semiconductor products. The semiconductor industry is subject to a complex regulatory environment, which includes international trade regulations, environmental laws, and standards for product safety and quality.

Navigating this environment is crucial for manufacturers to ensure compliance and minimize risks associated with supply chain disruptions and geopolitical tensions. Additionally, the industry must address the environmental impact of semiconductor manufacturing, which involves the use of hazardous chemicals and materials.

Impact of AI

The impact of Artificial Intelligence (AI) on semiconductor manufacturing is profound, revolutionizing the industry across various dimensions.

Here are five key points highlighting the impact:

- Enhanced Process Control and Optimization: AI applications in semiconductor manufacturing, such as Advanced Process Control (APC) systems, provide real-time feedback and dynamic adjustments to manufacturing processes. This results in reduced variability and improved yield, effectively decreasing production costs and enhancing overall efficiency.

- Predictive Maintenance: By employing AI for predictive maintenance, semiconductor factories can anticipate equipment failures before they occur. This proactive approach reduces downtime and maintenance costs, ensuring smoother and more reliable operations.

- Rapid Prototyping and Design Optimization: AI accelerates the semiconductor design process through machine learning and simulation tools. These technologies allow for rapid iteration cycles, optimizing designs for performance and efficiency while reducing material waste during prototyping.

- Quality Assurance and Defect Detection: AI significantly improves quality control in semiconductor manufacturing by employing sophisticated computer vision techniques and machine learning models to detect defects that are imperceptible to human inspectors. This not only enhances product quality but also reduces the rate of production rejections.

- Supply Chain and Inventory Optimization: AI enhances supply chain management by predicting market demand and optimizing inventory levels. This results in more efficient production planning and reduces the risks associated with over or under-stocking, which are critical in maintaining supply chain fluidity and cost-efficiency.

China Market Growth

The China Semiconductor Manufacturing Market is valued at approximately USD 50.90 Billion in 2024 and is predicted to increase from USD 55.84 Billion in 2025 to approximately USD 128.46 Billion by 2034, projected at a CAGR of 9.7% from 2025 to 2034.

The leadership of the United States in the semiconductor manufacturing sector can be attributed to a combination of technological advancements, strategic investments, and governmental support aimed at rejuvenating domestic capabilities in this critical industry. A key driver of this advancement is the significant investment in cutting-edge semiconductor manufacturing technologies.

For instance, major companies like Intel, Samsung, and Taiwan Semiconductor Manufacturing Co. (TSMC) have announced substantial investments to expand their U.S.-based operations. Intel’s construction of new chip factories in Ohio and TSMC’s expansion in Arizona are indicative of the strategic focus on enhancing the U.S. semiconductor manufacturing capacity.

As stated by design reuse, Regionally, the year-to-year semiconductor sales experienced varied growth rates across different markets. In the Americas, sales surged by 48.4%, demonstrating a robust increase. The Asia Pacific/All Other region also saw a rise, with sales growing by 10.8%. Similarly, China and Japan witnessed moderate growth, with increases of 5.6% and 5.1% respectively. However, Europe experienced a decline, with sales dropping by -8.1%.

On a month-to-month basis for February, sales trends were less positive. The Asia Pacific/All Other region saw a slight decrease of -0.1%, while Europe’s sales fell by -2.4%. Both China and Japan recorded a -3.1% decrease. The Americas faced the most significant reduction, with a decrease of -4.6%. These figures reflect the fluctuating dynamics in the semiconductor market across different global regions.

In the regional landscape, China, Korea, and Taiwan continue to lead in semiconductor equipment spending, collectively holding 74% of the global market. China has notably reinforced its lead by increasing its investment by 35% year-over-year, amounting to $49.6 billion. This growth is primarily fueled by extensive capacity expansions and substantial support from government initiatives, aiming to strengthen domestic chip production capabilities.

In 2024, the Asia Pacific (APAC) region held a dominant position in the semiconductor manufacturing market, capturing a substantial market share. Specifically, the region was responsible for more than 68.7% of the global market, generating significant revenue amounting to approximately USD 97.89 billion.

This dominant position can be attributed to several key factors that uniquely position APAC as the leader in this high-tech industry. Firstly, the APAC region benefits from the presence of established and globally recognized semiconductor powerhouses such as Taiwan, South Korea, and China. These countries are home to leading semiconductor companies and foundries, including Taiwan Semiconductor Manufacturing Company (TSMC) and Samsung Electronics.

The expertise and advanced technological capabilities of these companies, particularly in cutting-edge semiconductor fabrication technologies, drive the region’s preeminence in the semiconductor sector. Additionally, APAC’s dominance is bolstered by substantial investments in semiconductor manufacturing infrastructure.

The region continues to attract significant capital investments aimed at expanding existing facilities and building new ones, further enhancing its manufacturing capabilities. This is complemented by government support in several APAC countries, which provides incentives and financial backing for semiconductor projects, reinforcing the region’s global leadership position.

Technology Node Analysis

In 2024, the 3nm segment held a dominant position in the semiconductor manufacturing market, capturing more than a 36.7% share. This leadership can be attributed to several pivotal factors. Firstly, the significant advancements in ultra-precise fabrication technologies have enabled manufacturers to produce 3nm chips, which are highly efficient and powerful.

These chips meet the escalating demands of high-performance computing applications, including AI, gaming, and mobile computing, where speed and energy efficiency are paramount. Moreover, the adoption of 3nm technology by leading industry players in the development of processors for smartphones and other consumer electronics has spurred tremendous growth in this segment.

The transition towards smaller node sizes facilitates greater performance and lower power consumption, a critical requirement in the expanding market for portable devices that require long battery life and robust processing capabilities. Additionally, the expansion of 3nm technology is also driven by substantial investments from major semiconductor companies in research and development.

These investments are aimed at overcoming the technical challenges associated with scaling down chip sizes, such as quantum tunneling and heat dissipation. The successful management of these issues further solidifies the 3nm segment’s market leadership by enhancing the yield rates and performance of these advanced semiconductors.

Industry Vertical Analysis

In 2024, the Consumer Electronics segment held a dominant market position in the semiconductor manufacturing industry, capturing more than a 51.7% share. This segment’s leadership is primarily driven by the relentless demand for consumer electronic devices such as smartphones, tablets, smartwatches, and other connected devices.

The continuous innovation in these products, characterized by new features and enhanced capabilities, necessitates the regular adoption of advanced semiconductors to handle increased processing needs and power efficiency requirements. Furthermore, the trend towards smart home devices and the Internet of Things (IoT) has significantly contributed to the growth of the Consumer Electronics segment.

As homes become more connected through products like smart speakers, security systems, and home automation technologies, the need for semiconductors that provide connectivity and efficient energy usage has surged. This trend is expected to persist, as the adoption of smart home technology becomes more widespread across global markets.

Another factor bolstering the dominance of the Consumer Electronics segment is the rapid advancement in display technologies and the shift towards high-definition video content, which requires high-performance processing chips to deliver enhanced graphics and user experience.

Additionally, the advent of 5G technology has started to make its mark on consumer electronics, demanding more sophisticated semiconductor solutions to support faster data transmission and improved network reliability.

Key Market Segments

By Technology Node

- 3nm

- 4-10nm

- 14-28nm

- 28-130nm

By Industry Vertical

- Consumer Electronics

- Computing

- IT & Telecom

- Automotive

- Industrial

- Others

Driver

Increasing Demand for Advanced Electronics

The semiconductor manufacturing industry is significantly driven by the escalating demand for advanced electronics, which encompasses a wide array of devices from smartphones to complex automotive systems. This demand is fueled by technological advancements that enable the development of more sophisticated and compact devices requiring high-performance semiconductors.

As highlighted by Market.us, The semiconductor manufacturing equipment market is also on a trajectory of rapid growth, forecasted to swell from USD 95 billion in 2023 to USD 208.9 billion by 2033, reflecting a vigorous CAGR of 8.2%. In this segment, APAC continued to lead in 2023, securing more than 62% of the market share and capturing USD 58.9 billion in revenue.

As consumer preferences evolve towards faster, more efficient, and feature-rich devices, semiconductor manufacturers are pressured to innovate and scale their operations to meet these needs. This ongoing trend is not only pushing the boundaries of existing manufacturing technologies but also driving the growth of the industry by necessitating continuous advancements in semiconductor technology.

Restraint

High Initial Investment Costs

A major restraint facing the semiconductor manufacturing industry is the substantial initial investment required for setting up and modernizing manufacturing facilities. The costs associated with advanced manufacturing technologies, such as lithography equipment capable of producing finer circuits, are extremely high.

Moreover, the rapid pace of technological change in the industry means that these investments may need to be made frequently to keep up with new manufacturing standards and capabilities. This scenario poses a significant barrier, particularly for new entrants and smaller firms that might not have the capital to invest heavily at the onset.

Opportunity

Expansion into New Market Segments

There is a notable opportunity in the expansion into new semiconductor market segments such as wearables, IoT devices, and automotive electronics, which are expected to see increased demand. The diversification into these areas offers semiconductor manufacturers the chance to tap into new revenue streams and reduce dependence on the traditional markets like mobile phones and personal computers, which are becoming increasingly saturated.

As these newer segments continue to grow, driven by consumer demand for interconnected and intelligent devices, semiconductor manufacturers have the opportunity to establish strong footholds in emerging markets.

Challenge

Rapid Technological Advancements

The semiconductor manufacturing industry faces the challenge of keeping pace with rapid technological advancements. The industry is highly dynamic, with frequent innovations in device architecture, materials science, and manufacturing processes. This fast-paced evolution requires manufacturers to continually invest in research and development to remain competitive.

Additionally, the complexity of new semiconductor products demands highly skilled workers; however, there is a notable gap in the required technical expertise, which poses a significant challenge in maintaining the pace of innovation.

Growth Factors

The growth of the semiconductor manufacturing industry is largely influenced by the continuous advancements in technology that enable the production of smaller, faster, and more energy-efficient semiconductor devices. These technological innovations not only enhance the performance of electronic devices but also drive the development of new products and applications, further stimulating demand for semiconductors.

Additionally, the global shift towards digital and smart technologies across various sectors, including automotive, industrial, and consumer electronics, contributes significantly to the growth of the semiconductor industry.

Emerging Trends

Emerging trends such as the integration of Artificial Intelligence (AI) in manufacturing processes and the adoption of Internet of Things (IoT) technologies are reshaping the semiconductor industry. AI applications in semiconductor manufacturing are improving the efficiency and precision of production processes, leading to higher yields and reduced costs.

Similarly, IoT devices are becoming increasingly prevalent, requiring tailored semiconductor solutions that can handle connectivity, data processing, and security, thus opening new avenues for industry growth.

Business Benefits

Advanced semiconductor manufacturing technologies bring several business benefits, including enhanced product quality and reliability, reduced production costs, and shorter time-to-market for new products. These improvements are crucial for maintaining competitiveness in a rapidly evolving technology landscape.

Additionally, advanced manufacturing processes enable semiconductor companies to meet the stringent performance and efficiency requirements of next-generation electronic devices, thereby solidifying their market positions and ensuring long-term business growth.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

The semiconductor manufacturing industry is a dynamic and rapidly evolving sector, with key players continually engaging in strategic acquisitions, product launches, and mergers to strengthen their market positions.

In March 2025, TSMC announced its intention to expand its investment in the United States by an additional $100 billion, bringing its total U.S. investment to $165 billion. This expansion includes plans for three new fabrication plants, two advanced packaging facilities, and a major research and development center.

In July 2024, Samsung Electronics acquired Oxford Semantic Technologies, a UK-based knowledge graph startup. This strategic move is expected to significantly enhance Samsung’s AI capabilities across its product lineup, including smartphones and smart home appliances.

In January 2024, Intel announced an agreement to acquire Silicon Mobility SAS, a fabless silicon and software company specializing in system-on-chips for intelligent electric vehicle energy management. This acquisition is intended to bring AI efficiencies to electric vehicle energy management and enhance Intel’s offerings in the automotive sector

Top Key Players in the Market

- Samsung

- GlobalFoundries Inc.

- Vanguard International Semiconductor Corporation

- United Microelectronics Corporation

- Taiwan Semiconductor Manufacturing Co., Ltd.

- PSMC Co., Ltd.

- Semiconductor Manufacturing International Corporation

- Nexchip Semiconductor Corp.

- Tower Semiconductor Ltd.

- Hua Hong Semiconductor Limited

- Others

Recent Developments

- In December 2024, Samsung Electronics held a tool-in ceremony for its new semiconductor research and development complex (NRD-K) at its Giheung campus. The facility is scheduled to start operations in 2025, with an investment of approximately KRW 20 trillion by 2030 for advanced semiconductor R&D.

- In December 2024, GlobalFoundries announced plans to build a $575 million advanced chip packaging and testing center at its Fab 8 campus in Malta, New York. The facility will focus on photonics technology and is expected to create 102 jobs.

- In December 2024, Vanguard International Semiconductor Corporation and NXP Semiconductors broke ground on a new 300mm semiconductor manufacturing facility in Singapore. The joint venture, VisionPower Semiconductor Manufacturing Company Pte Ltd (VSMC), aims to begin production in 2027, with an expected output of 55,000 300mm wafers per month by 2029.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 142.50 Bn |

| Forecast Revenue (2034) | USD 313.39 Bn |

| CAGR (2025-2034) | 8.2% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Technology Node (3nm, 4–10nm, 14–28nm, 28–130nm), By Industry Vertical(Consumer Electronics, Computing, IT & Telecom, Automotive, Industrial, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Samsung, GlobalFoundries Inc., Vanguard International Semiconductor Corporation, United Microelectronics Corporation, Taiwan Semiconductor Manufacturing Co., Ltd., PSMC Co., Ltd., Semiconductor Manufacturing International Corporation, Nexchip Semiconductor Corp., Tower Semiconductor Ltd., Hua Hong Semiconductor Limited, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |