Quick Navigation

- Report Overview

- Key Takeaways

- Business Benefits

- China Market Analysis

- Type of Payment Analysis

- Component Analysis

- Deployment Analysis

- Enterprise Size Analysis

- Vertical Analysis

- Key Market Segments

- Driver

- Restraint

- Opportunity

- Challenge

- Emerging Trends

- Key Player Analysis

- Top Opportunities for Players

- Recent Developments

- Report Scope

Report Overview

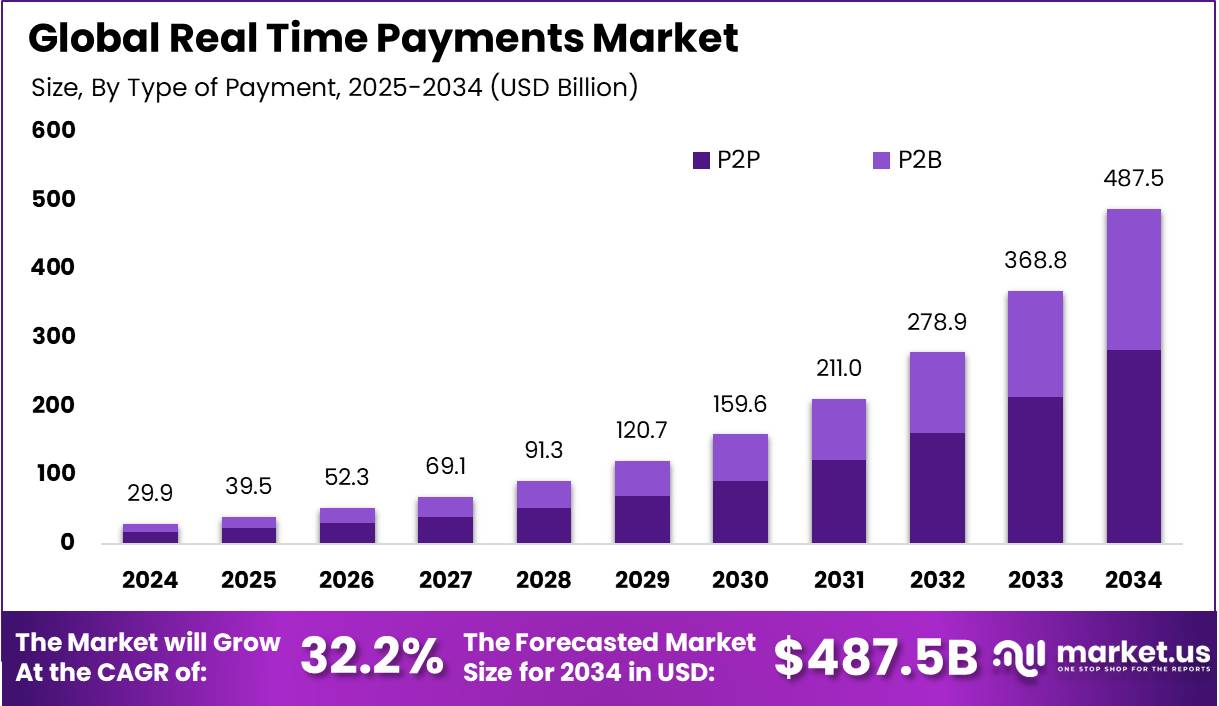

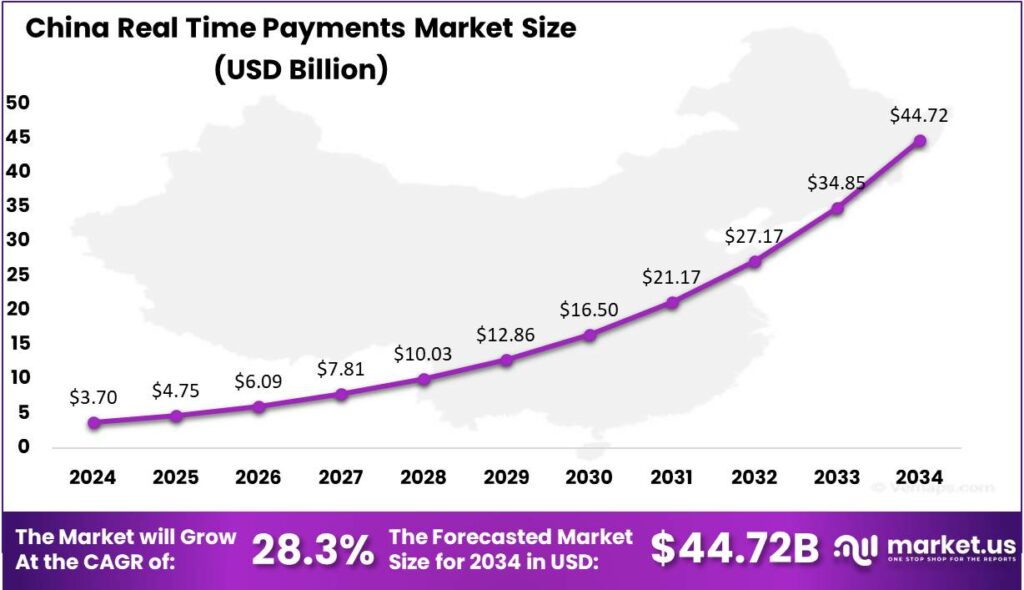

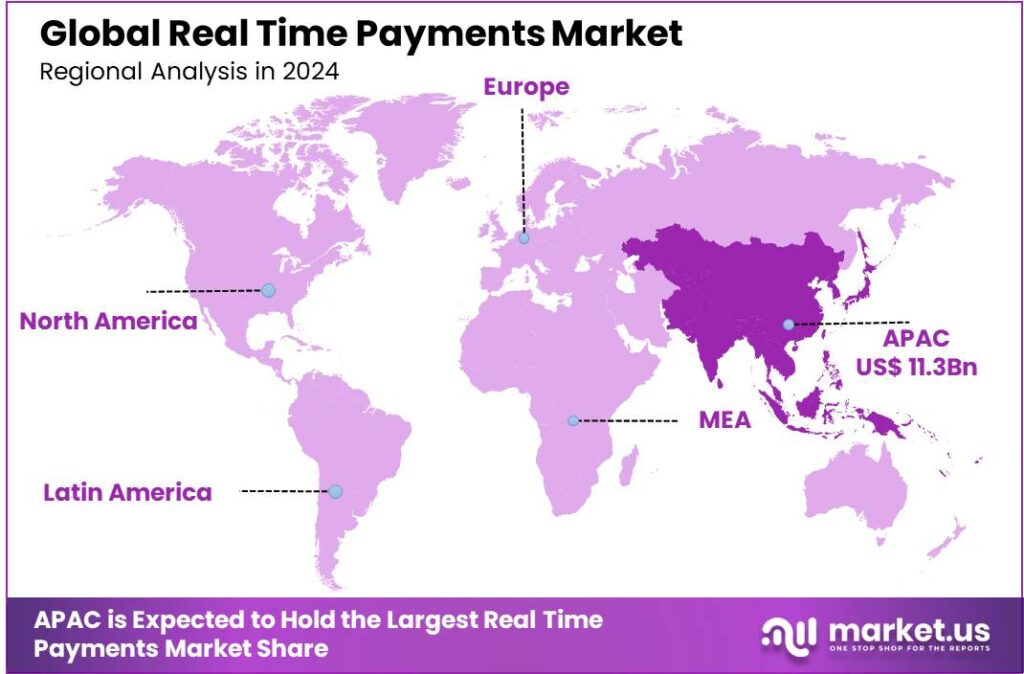

The Global Real Time Payments Market size is expected to be worth around USD 487.5 Billion By 2034, from USD 29.9 Billion in 2024, growing at a CAGR of 32.20% during the forecast period from 2025 to 2034. In 2024, Asia-Pacific led the real-time payments market with over 38% market share and USD 11.3 billion in revenue. China’s market was valued at USD 3.7 billion, reflecting rapid advancements in digital payment infrastructure, with a CAGR of 28.3%.

Real-Time Payments (RTP) refer to electronic payment systems that facilitate the immediate transfer of funds between bank accounts, ensuring instant settlement and confirmation. These systems operate continuously, 24/7, including weekends and holidays, providing users with the ability to conduct transactions at any time.

The primary objective of RTP is to enhance the efficiency of financial transactions, offering benefits such as reduced processing times, improved cash flow management, and increased transparency for both individuals and businesses. The Real-Time Payments market has experienced significant growth in recent years, driven by the increasing demand for instant payment solutions across various industries.

Key driving factors for the adoption of RTP include the growing consumer expectation for immediate transaction processing, the need for improved liquidity management among businesses, and the push towards digitalization in financial services. Additionally, government initiatives promoting cashless economies and the integration of advanced technologies like artificial intelligence and blockchain have further accelerated the adoption of real-time payment solutions.

Countries like India, Brazil, and Singapore are promoting real-time payments, boosting adoption among users and businesses. Increased smartphone use and internet access make mobile RTP systems more accessible, driving market growth. Businesses benefit from improved cash flow and faster reconciliation, encouraging widespread industry adoption.

RTP systems enhance cash flow by eliminating settlement delays and reducing default risks. Real-time payment confirmation and integration with accounting and inventory systems streamline operations and provide timely financial insights for improved decision-making. According to The PYMNTS Intelligence report, 88% of businesses have seen real benefits from using faster or real-time payments. This includes better cash flow and stronger financial health, especially for small and mid-sized companies.

AI enhances RTP systems by analyzing transaction patterns to detect and prevent fraud in real-time, boosting security. Additionally, AI-driven analytics personalize user experiences and optimize transaction processes. In India, AI integration with UPI platforms is expected to further improve the efficiency and reliability of digital payments.

The proliferation of smartphones and internet connectivity opens avenues for RTP expansion into underserved markets. Customizing RTP for local languages and regional needs can boost adoption. Integrating RTP with blockchain and digital identity enhances security and fosters innovation in financial transactions.

Key Takeaways

- The Global Real Time Payments Market is projected to reach USD 487.5 Billion by 2034, growing from USD 29.9 Billion in 2024, at a CAGR of 32.20% during the forecast period from 2025 to 2034.

- In 2024, the P2P (Person-to-Person) segment dominated the market, capturing more than 58% of the global real-time payments market share.

- The Solutions segment held a dominant market position in 2024, securing more than 72% of the real-time payments market share.

- In 2024, the Cloud-based segment was the leader in the market, capturing over 64% of the global real-time payments market share.

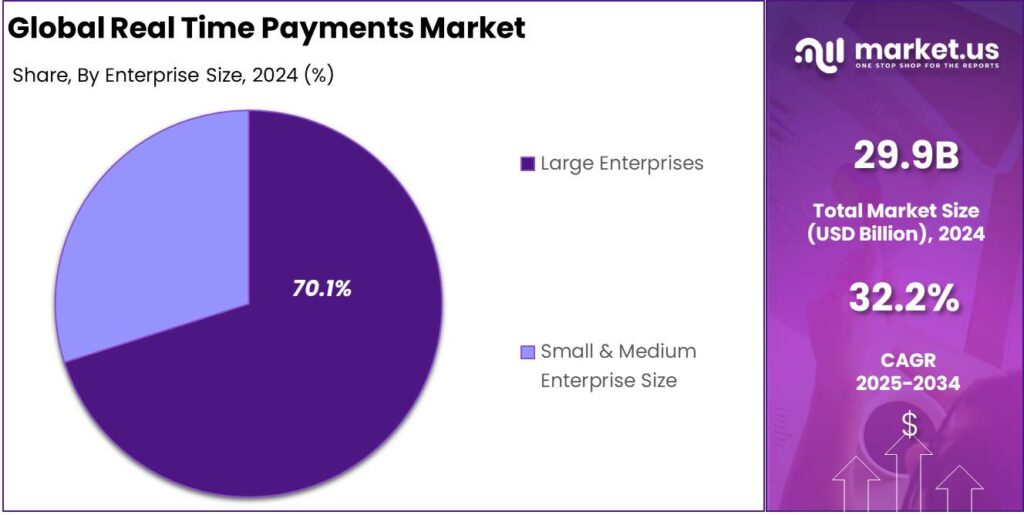

- The Large Enterprises segment had a dominant share in the real-time payments market in 2024, with more than 70.1% of the market share.

- In 2024, the BFSI (Banking, Financial Services, and Insurance) segment dominated the real-time payments market with more than 38% of the total market share.

- Asia-Pacific held a leading position in the real-time payments market in 2024, accounting for over 38% of the global market share, with USD 11.3 billion in revenue.

- The real-time payments market in China was valued at approximately USD 3.7 billion in 2024, reflecting the country’s rapidly advancing digital payment infrastructure.

Business Benefits

Real-time payments allow businesses to receive funds instantly after a transaction, significantly enhancing cash flow management. This immediacy enables companies to utilize funds promptly, reducing the need for short-term financing and improving liquidity. As per Paystand report, 24% of companies specifically point to improved cash flow as the main advantage, helping them meet financial obligations without delays.

Real-time payments provide immediate confirmation and detailed transaction information, improving financial transparency. Companies that offer real-time payments build more trust. According to the PYMNTS report, 89% of large retailers, 91% of manufacturers, and 80% of insurers report that RTP has improved their supplier relationships.

The immediate nature of RTPs eliminates the need for manual intervention in payment processes, increasing overall operational efficiency. Businesses no longer need to wait for checks to clear or for batch processing of electronic payments, reducing administrative burdens and errors.

China Market Analysis

In 2024, the Real-Time Payments (RTP) market in China was valued at approximately USD 3.7 billion, reflecting the nation’s fast-evolving digital payment infrastructure. The market is growing rapidly, driven by smartphone adoption, mobile-first platforms like WeChat Pay and Alipay, and rising demand for instant, low-cost, transparent payments.

The market is poised for robust expansion, as indicated by its projected compound annual growth rate (CAGR) of 28.3%, driven by rapid urbanization, financial inclusion efforts, and real-time integration in B2B and P2P payments. Rising demand for seamless payments and the shift to e-commerce have made real-time payment (RTP) solutions a strategic focus for banks, fintechs, and processors. Government initiatives like the Digital Yuan further strengthen real-time infrastructure with faster, more secure transactions.

China’s dominance in the real-time payments space is further enhanced by its advanced digital ecosystem and strong regulatory support. Financial institutions are rapidly modernizing their back-end systems to accommodate 24/7 instant settlements, while new innovations in API-based banking and cloud-native payment gateways are reshaping how transactions occur in real-time.

In 2024, Asia-Pacific held a dominant market position, capturing more than a 38% share of the global real-time payments market, with an estimated USD 11.3 billion in revenue. The region leads due to widespread mobile financial services, rapid digitalization, and a tech-savvy population embracing real-time digital payments.

China leads real-time transactions in Asia, driven by super-apps like WeChat Pay and Alipay, which handle billions daily. India follows with its UPI system, enabling 24/7 seamless payments at scale. Both countries blend public infrastructure and private innovation, creating scalable, interoperable models now emulated worldwide. These platforms are central to daily commerce and have sharply reduced cash use.

Asia-Pacific’s lead in real-time payments is also driven by central banks and government-led financial inclusion efforts. Countries like Indonesia, Thailand, and the Philippines have launched systems like BI-FAST and PromptPay, improving access and enabling faster transfers. These initiatives are modernizing payments and supporting cross-border integration in ASEAN.

The region’s rapid e-commerce growth, increased smartphone penetration, and a growing population of digital-first consumers continue to push the market forward. Partnerships between fintech firms and traditional financial institutions are resulting in innovative,API-driven platforms that bring flexibility to transactions.

Type of Payment Analysis

In 2024, P2P (Person-to-Person) segment held a dominant market position, capturing more than a 58% share in the global Real-Time Payments market. This dominance was largely attributed to the increasing popularity of mobile wallets and peer-to-peer payment apps that facilitate instant money transfers between individuals.

A key factor supporting the leadership of the P2P segment is the growing reliance on digital channels for personal finance management and informal transactions. In both urban and rural settings, individuals increasingly use real-time P2P platforms to split bills, send emergency funds, or pay for home-based services.

This behavior has replaced traditional cash-based or delayed transfers, further strengthening the need for reliable and fast payment solutions. The segment’s popularity has also surged during festive seasons, travel, or crisis situations when instant fund access is critical, pushing financial institutions to scale their P2P capabilities.

Moreover, real-time P2P payment solutions have found deep integration into social and communication platforms, which has made sending money as easy as sending a message. This integration has removed friction from the user experience and encouraged more frequent low-value transactions, contributing to higher overall transaction volumes.

Component Analysis

In 2024, the Solutions segment held a dominant market position, capturing more than a 72% share of the Real-Time Payments market. This dominance is primarily due to the critical role that core payment technologies such as payment gateways, processing engines, and fraud management systems play in ensuring seamless, fast, and secure digital transactions.

One of the primary drivers of the Solutions segment’s leadership is the growing integration of payment gateway technologies that support 24/7 transaction flows across diverse digital channels. These gateways serve as the foundation for real-time transactions, ensuring connectivity between payer and payee banks with low failure rates and immediate payment confirmation.

Furthermore, payment security and fraud management solutions have become essential, particularly in light of rising concerns around identity theft, transaction manipulation, and phishing scams. Real-time risk assessment, powered by artificial intelligence and machine learning, is now embedded into many real-time payment platforms.

The Services segment, including managed services and consulting, plays a supportive role, with organizations prioritizing solutions during initial implementation. Service spending typically follows during upgrades or integration. As real-time payment ecosystems become more software-centric, the Solutions segment will remain dominant, offering advanced, reliable, and customizable platforms for the digital economy.

Deployment Analysis

In 2024, the Cloud-based segment held a dominant market position, capturing more than a 64% share of the global real-time payments market. This growth is primarily driven by the increasing need for scalable, flexible, and cost-efficient payment infrastructure among banks, fintech companies, and large enterprises.

The growth of digital banking, mobile wallets, and API-based payment platforms has fueled demand for cloud-based payment systems. These platforms enable real-time processing, integrate with core banking systems, and ensure 24/7 uptime. As businesses prioritize fast, uninterrupted payments, cloud technology provides the reliability and performance needed at a cost-effective price.

Security and compliance have driven the shift to cloud deployments, with cloud-native encryption, zero-trust architectures, and data residency frameworks boosting confidence in handling sensitive financial operations. This is particularly crucial for banks and financial institutions in regulated markets, where adherence to evolving data protection and payment regulations is vital.

Cloud platforms enable payment providers to innovate quickly, launch new services, and expand with minimal infrastructure, making them ideal for emerging fintechs and small banks. As digital transactions and demand for real-time settlements grow, the cloud-based model will continue to be the preferred choice in the real-time payments ecosystem.

Enterprise Size Analysis

In 2024, Large Enterprises segment held a dominant market position, capturing more than a 70.1% share in the Real-Time Payments (RTP) market. This leadership can be attributed to their high-volume transaction needs, global supply chains, and complex financial workflows that demand instant, secure, and traceable payment mechanisms.

Large corporations have been prioritizing the adoption of real-time payment infrastructure to streamline accounts receivable and payable, enabling improved liquidity management and faster reconciliation processes. Their ability to invest in advanced financial technologies has accelerated the migration toward RTP platforms at a much faster pace compared to smaller firms.

In large enterprises, real-time payment systems are crucial for high-value B2B transactions, enabling instant fund transfers across borders. These systems reduce reliance on outdated processing methods, boosting operational agility. Industries like retail, telecom, and manufacturing use real-time payments for faster refunds, supplier payments, and payroll services, enhancing ecosystem integration.

Another key factor contributing to the dominance of large enterprises in this segment is their increasing focus on enhancing customer experience. In sectors like e-commerce and digital services, large organizations are using RTP to provide real-time disbursements, instant checkout experiences, and seamless digital wallets.

Vertical Analysis

In 2024, BFSI segment held a dominant market position, capturing more than a 38% share of the Real-Time Payments (RTP) market. This dominance is primarily due to the critical role real-time payments play in enhancing the speed, transparency, and security of financial transactions.

Banks, insurance providers, and financial service institutions are at the forefront of digital payment adoption, as they aim to offer seamless and instant transaction experiences to both retail and corporate clients. Real-time capabilities are essential for services such as instant fund transfers, peer-to-peer (P2P) payments, and real-time settlement of loans and investments.

The need for real-time fund accessibility and liquidity management in financial institutions has accelerated the integration of RTP platforms. With increasing demand for 24/7 banking services and digital-first experiences, BFSI players are heavily investing in modernizing their payment infrastructure. These advancements are helping financial institutions cut down settlement times and enhance fraud detection mechanisms through integration with AI-based analytics.

Regulatory support and open banking are driving RTP adoption in the BFSI sector, with governments and central banks pushing for instant, interoperable payment systems. This, combined with the sector’s high digital maturity, keeps BFSI at the forefront of real-time payments, ahead of industries like retail and telecom.

Key Market Segments

By Type of Payment

- P2P

- P2B

By Component

- Solutions

- Payment Gateway

- Payment Processing

- Payment Security and Fraud Management

- Services

- Professional Services

- Managed Services

By Deployment

- On-premises

- Cloud-based

By Enterprise Size

- Small & Medium-Sized Enterprises

- Large Enterprises

By Vertical

- BFSI

- IT and Telecommunications

- Retail and e-commerce

- Government

- Energy and Utilities

- Others

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

Enhanced Transparency and Control

The adoption of real-time payments (RTP) is significantly driven by the demand for enhanced transparency and control in financial transactions. Unlike traditional payment methods, RTP systems provide immediate confirmation and visibility into the payment process.

For businesses, the ability to track payments in real-time reduces the uncertainty associated with pending transactions. It enables more accurate forecasting and budgeting, as funds are transferred and received instantly. This level of transparency is particularly beneficial in supply chain operations, where timely payments can strengthen relationships with suppliers and improve overall efficiency.

Moreover, RTP systems often come with detailed transaction information, allowing for easier reconciliation and auditing. This granularity in data supports compliance efforts and reduces the risk of errors, contributing to more robust financial management practices.

Restraint

High Implementation Costs

Despite the advantages of real-time payments, the high costs associated with implementing RTP systems serve as a significant restraint. Financial institutions and businesses must invest in upgrading their existing infrastructure to support the real-time processing of transactions.

The financial burden is particularly challenging for smaller institutions and businesses that may lack the necessary capital or technical expertise. The complexity of overhauling legacy systems can lead to prolonged implementation timelines and increased operational risks during the transition period. Additionally, ongoing maintenance and the need for continuous updates to address security vulnerabilities and comply with evolving regulations add to the total cost of ownership.

Opportunity

Expansion into Emerging Markets

Real-time payments present a significant opportunity for expansion into emerging markets, where traditional banking infrastructure may be limited. In regions with high mobile phone penetration but low access to conventional banking services, RTP systems can bridge the financial inclusion gap by providing accessible and efficient payment solutions.

The adoption of RTP in emerging markets can drive economic growth by enabling faster, more secure transactions for both consumers and businesses. It empowers SMEs to participate more actively in the digital economy, expanding their customer base and improving operations. Additionally, governments and financial institutions are recognizing RTP’s potential to modernize payment systems, enhance financial stability, reduce cash reliance, and promote transparency in financial transactions.

Challenge

Fraud and Security Concerns

The rapid processing of real-time payments poses significant fraud and security challenges, as traditional detection methods have little time to identify unauthorized transactions. Malicious actors can exploit this speed, making it crucial for financial institutions to invest in advanced security measures like real-time monitoring and AI-based fraud detection.

The finality of RTP transactions, which cannot be easily reversed, raises the stakes for ensuring payment authenticity and accuracy. Errors or fraud can lead to significant financial losses. To maintain trust in RTP systems, it’s crucial to address these security concerns through continuous investment in technology, staff training, and collaboration among stakeholders to create robust security frameworks that counter evolving threats.

Emerging Trends

One significant trend is the widespread adoption of RTP systems by banks and financial institutions to meet consumer expectations for instant payment processing. The growth of digital wallets and mobile banking apps has boosted RTP usage, enabling instant transfers anytime, even outside traditional banking hours. RTP networks are also expanding internationally, enhancing cross-border payments by reducing processing times and costs, benefiting trade and remittances.

Another key trend is the integration of RTP with advanced technologies such as artificial intelligence (AI) and blockchain. AI helps in fraud detection and risk management by analyzing transaction patterns in real time, thereby enhancing payment security. Blockchain technology contributes to transparency and immutability of payment records, increasing trust among users.

Regulatory bodies worldwide are also pushing for RTP adoption as part of financial modernization efforts. Governments recognize the role of instant payments in boosting economic efficiency and financial inclusion by enabling small businesses and underbanked populations to access swift and affordable payment services.

Key Player Analysis

As the market expands, several key players are leading the charge with unique technologies and wide global reach.

ACI Worldwide, Inc. is one of the top names in the real-time payments space. The company offers a strong real-time payment platform that supports banks, central infrastructures, and fintechs. Its Universal Payments (UP) platform is known for supporting multiple payment types and working with real-time clearing and settlement systems in different countries.

Fidelity National Information Services, Inc. (FIS Inc.) is a powerhouse in financial services technology and has made a big impact in the real-time payments market. FIS stands out for combining innovation with a strong foundation in banking infrastructure, which allows it to serve both traditional banks and new digital players.

Finastra brings a flexible and open approach to real-time payments. The company is known for its open banking solutions and API-based platforms that allow clients to connect and innovate faster. Finastra’s Fusion Global PAYplus is one of its key offerings in this space, designed to support multiple payment schemes, including real-time systems.

Top Key Players in the Market

- ACI Worldwide, Inc.

- Fidelity National Information Services, Inc. (FIS Inc.)

- Finastra

- Fiserv, Inc.

- Mastercard, Inc.

- Montran Corp.

- PayPal Holdings, Inc.

- Temenos AG

- Visa Inc.

- Volante Technologies Inc.

- Wirecard AG

- Worldpay, Inc.

- Others

Top Opportunities for Players

- Expansion in Cross-Border Transactions: Globalization has increased the need for fast, secure, and affordable cross-border payments. Real-time payments meet this demand by enabling instant international transactions and reducing dependence on traditional banking networks. This evolution not only enhances operational efficiency but also opens avenues for financial institutions to offer value-added services in the global remittance market.

- Integration with Emerging Technologies: The integration of RTP with AI, blockchain, and IoT is reshaping payments. AI boosts fraud detection and personalization, while blockchain adds transparency and security. IoT integration enables seamless machine-to-machine payments, paving the way for innovative applications in sectors like automotive and smart appliances.

- Growth in Business-to-Business (B2B) Payments: Businesses are increasingly seeking real-time payment solutions to improve cash flow management and streamline operations. RTP facilitates immediate fund transfers, reducing the settlement time and enhancing liquidity. This shift is particularly beneficial for small and medium-sized enterprises (SMEs), which require efficient payment mechanisms to remain competitive in fast-paced markets.

- Enhancement of Customer Experience: Consumers now expect instant, convenient, and secure payment options. Real-time payments meet these expectations by providing immediate transaction confirmations and 24/7 availability. This capability not only improves customer satisfaction but also fosters loyalty, as users gravitate towards financial service providers that offer seamless payment experiences.

- Support for Financial Inclusion Initiatives: Real-time payment systems play a crucial role in promoting financial inclusion by providing unbanked and underbanked populations with access to digital financial services. By enabling instant transactions via mobile devices, RTP reduces barriers to entry and encourages participation in the formal financial system.

Recent Developments

- In September 2024, First Pacific Bank selected Finastra’s Payments To Go solution to modernize its payments infrastructure. This cloud-based platform supports real-time payments and ISO 20022 compliance, facilitating 24/7 FedNow services.

- In October 2024, Mastercard launched real-time card payment capabilities in South Africa, enabling acquiring banks to process instant payments. This initiative aligns with the South African Reserve Bank’s National Payments System Strategy Vision 2025.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 29.9 Bn |

| Forecast Revenue (2034) | USD 487.5 Bn |

| CAGR (2025-2034) | 32.2% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Type of Payment (P2P, P2B), By Component (Solutions (Payment Gateway, Payment Processing, Payment Security and Fraud Management), Services (Professional Services, Managed Services)), By Deployment (On-premises, Cloud-based), By Enterprise Size (Small & Medium-Sized Enterprises, Large Enterprises), By Vertical (BFSI, IT and Telecommunications, Retail and e-commerce, Government, Energy and Utilities, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | ACI Worldwide, Inc., Fidelity National Information Services, Inc. (FIS Inc.), Finastra, Fiserv, Inc. , Mastercard, Inc., Montran Corp., PayPal Holdings, Inc., Temenos AG, Visa Inc., Volante Technologies Inc., Wirecard AG, Worldpay, Inc., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |