Global Privacy Filter Market Size, Share, Growth Analysis By Product Type (2-Way Privacy Filters, 4-Way Privacy Filters, Touch-Screen Optimized Filters, Integrated OEM Privacy Displays), By Material Technology (Microlouver Film Filters, Nanotechnology-Based Filters, Electrochromic Switchable Filters), By Device Size (15–24 Inch Screens, Less than or equal to 15 Inch Screens, Above 24 Inch Screens), By End-User Industry (Corporate Offices, Healthcare Facilities, Financial Services, Government Agencies, Educational Institutions, Others), By Distribution Channel (Online Retail, Offline Retail, Direct OEM Integration), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 180323

- Number of Pages: 379

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Key Takeaways

- Product Type Analysis

- Material Technology Analysis

- Device Size Analysis

- End-User Industry Analysis

- Distribution Channel Analysis

- Key Market Segments

- Drivers

- Restraints

- Growth Factors

- Emerging Trends

- Regional Analysis

- Key Regions and Countries

- Key Company Insights

- Recent Developments

- Report Scope

Report Overview

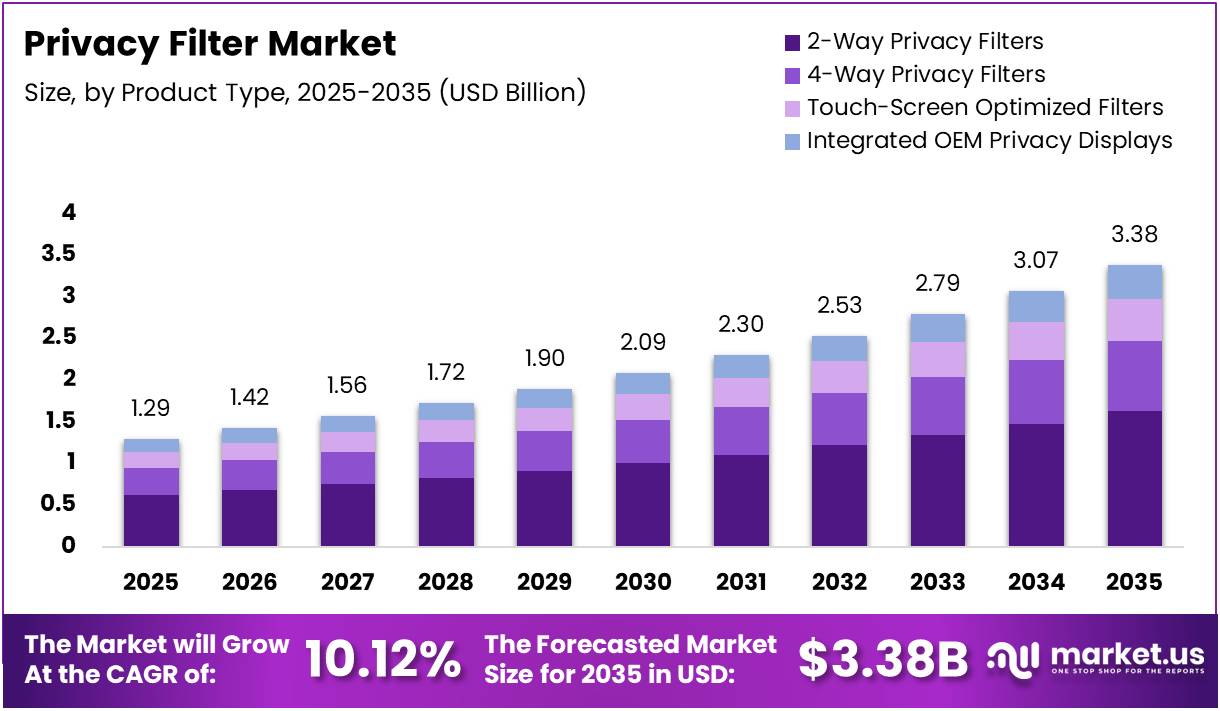

The Global Privacy Filter Market size is expected to be worth around USD 3.38 Billion by 2035 from USD 1.29 Billion in 2025, growing at a CAGR of 10.12% during the forecast period 2026 to 2035.

Privacy filters are thin film overlays or screen attachments designed to limit the viewing angle of digital displays. They protect sensitive information from visual eavesdropping, commonly known as shoulder surfing. These products are used widely on laptops, monitors, tablets, and smartphones in environments that require strict data confidentiality.

The market is expanding rapidly due to the global rise in remote work, digital learning, and mobile workstyles. Employees working in public spaces such as cafes, airports, and co-working hubs increasingly rely on screen privacy solutions. Moreover, growing awareness around personal data security is pushing demand further across both consumer and enterprise segments.

Government agencies and financial institutions are enforcing strict data privacy regulations, driving adoption of physical screen privacy tools. Compliance frameworks such as GDPR and HIPAA encourage organizations to take visible, proactive steps to prevent unauthorized data access. Consequently, procurement of privacy filters is becoming a standard part of enterprise security policies.

Additionally, the expansion of online retail platforms is improving product accessibility in emerging markets. Manufacturers are developing multi-functional products combining privacy protection with blue light filtering and anti-glare features. These innovations are attracting a broader customer base, especially among health-conscious professionals handling sensitive information daily.

According to Alibaba, premium privacy filters maintain 85 to 92% of original display brightness, while low-cost filters may retain only 62 to 76% brightness. High-end models maintain up to 98 to 100% sRGB color coverage, compared to 86 to 91% for budget models. These performance differences influence purchasing decisions significantly across enterprise and consumer segments.

Furthermore, according to Alibaba, privacy filters restrict viewing angles to around 30 to 45 degrees, ensuring only the direct user can see screen content clearly. This narrow-angle protection is a key feature driving adoption in high-security environments. Therefore, the market is well-positioned for continued and consistent growth throughout the forecast period.

Key Takeaways

- The Global Privacy Filter Market was valued at USD 1.29 Billion in 2025 and is projected to reach USD 3.38 Billion by 2035.

- The market is expected to grow at a CAGR of 10.12% during the forecast period from 2026 to 2035.

- By Product Type, 2-Way Privacy Filters dominate the segment with a 48.35% market share in 2025.

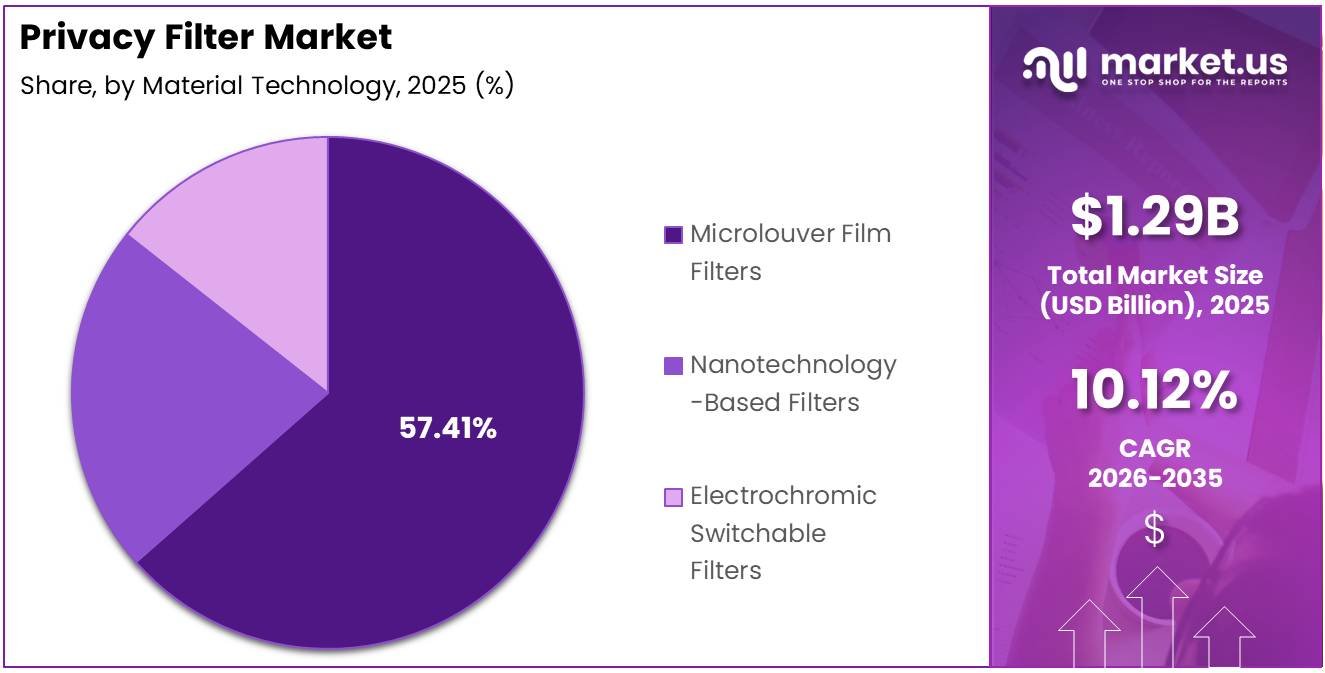

- By Material Technology, Microlouver Film Filters hold the leading position with a 57.41% share.

- By Device Size, 15–24 Inch Screens account for the largest share at 54.62% in 2025.

- By End-User Industry, Corporate Offices represent the dominant segment with a 40.86% share.

- By Distribution Channel, Online Retail leads with a 44.13% market share in 2025.

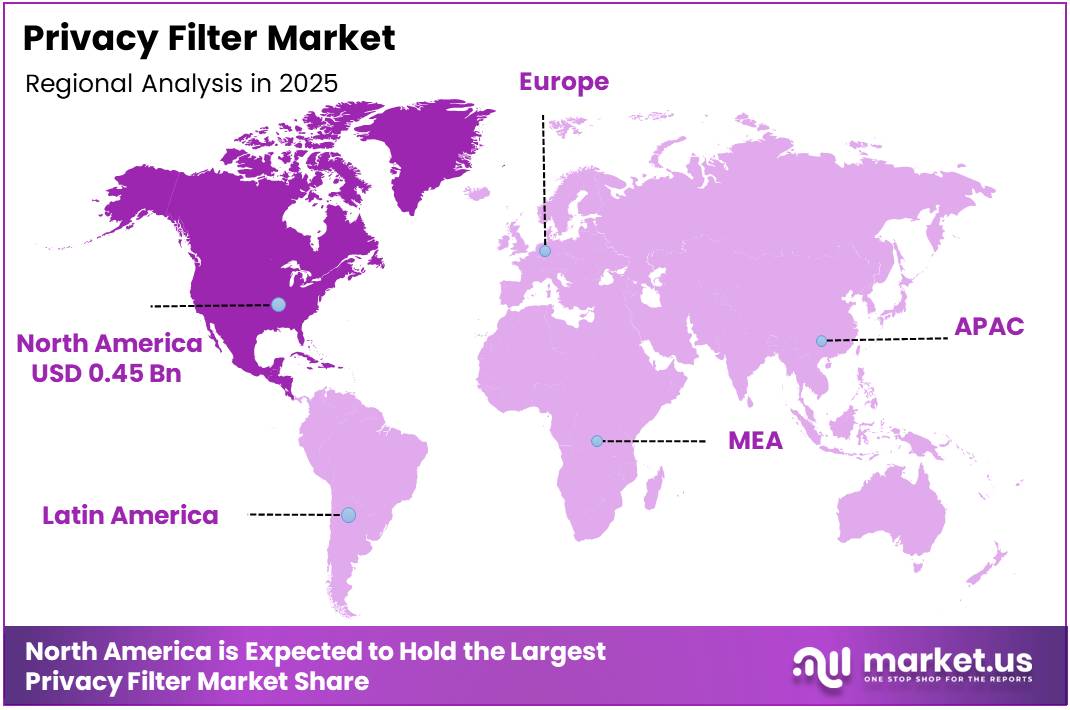

- North America dominates the regional landscape with a 34.71% share, valued at USD 0.45 Billion in 2025.

Product Type Analysis

2-Way Privacy Filters dominate with 48.35% due to widespread adoption in corporate offices and public-use environments.

In 2025, 2-Way Privacy Filters held a dominant market position in the By Product Type segment of the Privacy Filter Market, with a 48.35% share. These filters limit side-angle visibility from left and right directions, making them the preferred choice for laptop and desktop users working in offices, cafes, and public spaces.

4-Way Privacy Filters offer enhanced protection by limiting visibility from all four sides, including top and bottom angles. Consequently, they are gaining adoption in high-security environments such as financial institutions and government offices. Their broader coverage makes them suitable for users who require maximum visual data protection in open workspaces.

Touch-Screen Optimized Filters are designed specifically for devices with touchscreen functionality, including tablets and touchscreen laptops. These filters preserve touch sensitivity while delivering privacy protection. Moreover, their growing use in healthcare and education sectors reflects the increasing integration of touch-enabled devices in professional daily operations.

Integrated OEM Privacy Displays represent a newer product category where privacy functionality is built directly into device screens by manufacturers. Therefore, they eliminate the need for aftermarket filter attachments. However, their higher cost and limited availability in mainstream consumer devices currently restrict broader market adoption.

Material Technology Analysis

Microlouver Film Filters dominate with 57.41% due to cost-effectiveness and proven performance across device types.

In 2025, Microlouver Film Filters held a dominant market position in the By Material Technology segment of the Privacy Filter Market, with a 57.41% share. These filters use a micro-blind structure to restrict off-axis viewing. Their affordability, durability, and wide compatibility across laptops, monitors, and tablets drive their continued dominance.

Nanotechnology-Based Filters use advanced nanoscale materials to deliver improved clarity, thinner profiles, and better durability compared to traditional film-based options. Moreover, their superior optical performance is attracting adoption in premium enterprise and healthcare segments. However, higher production costs currently limit their penetration in price-sensitive consumer markets.

Electrochromic Switchable Filters allow users to toggle between privacy and transparent modes electronically. Therefore, they offer flexible use cases for both shared and individual screen environments. Although currently in an early adoption phase, growing interest from technology-forward enterprises is expected to drive meaningful market growth over the forecast period.

Device Size Analysis

15–24 Inch Screens dominate with 54.62% due to dominant use in laptops and desktop monitors in workplace settings.

In 2025, 15–24 Inch Screens held a dominant market position in the By Device Size segment of the Privacy Filter Market, with a 54.62% share. This size range covers the majority of standard laptops and desktop monitors used in corporate offices, financial institutions, and government agencies, driving consistent and high-volume demand.

Less than or equal to 15 Inch Screens represent a growing segment driven by the increasing use of compact laptops, tablets, and smartphones. Consequently, rising mobile workstyles and remote work adoption are fueling demand for small-form-factor privacy filters. Additionally, the expansion of online retail platforms is improving product availability across this category globally.

Above 24 Inch Screens cater to professionals using large-format monitors in environments such as design studios, control rooms, and executive workstations. These users often handle highly sensitive visual data. However, due to the smaller installed base of oversized displays, this segment represents a relatively niche but premium opportunity within the overall market.

End-User Industry Analysis

Corporate Offices dominate with 40.86% due to high volume of desk-based employees handling sensitive business information.

In 2025, Corporate Offices held a dominant market position in the By End-User Industry segment of the Privacy Filter Market, with a 40.86% share. Open-plan office environments and growing remote work policies have made screen privacy protection a standard procurement item for enterprises managing confidential business communications and data.

Healthcare Facilities represent a critical end-use segment due to the sensitive nature of patient data displayed on medical screens. Regulatory compliance with frameworks such as HIPAA makes screen privacy tools a necessary investment. Moreover, the increasing use of digital records in clinical environments is expanding demand for privacy filters in this sector.

Financial Services firms are among the highest adopters of privacy filters, given the confidential nature of financial data handled daily. Traders, analysts, and client-facing advisors routinely work with sensitive information in shared or public office environments. Consequently, financial institutions increasingly include privacy filters in their standard employee device procurement policies.

Government Agencies require stringent data protection measures across all levels of public administration. Privacy filters are being integrated into workstation security protocols to prevent unauthorized viewing of classified or sensitive government information. Additionally, many agencies are mandating the use of screen privacy solutions as part of broader cybersecurity and physical security compliance programs.

Educational Institutions are an emerging segment as campuses and digital learning environments adopt personal devices at scale. Students and faculty working in shared spaces increasingly need screen privacy solutions for examinations, research, and administrative tasks. Therefore, educational procurement programs are beginning to include privacy filters as standard device accessories.

Others include sectors such as legal services, retail, and transportation that are incrementally adopting privacy filter solutions. As awareness of visual data security expands across industries, this segment is expected to grow steadily. Furthermore, custom-fit and multi-device privacy solutions are helping manufacturers address the diverse needs of these varied end-user groups.

Distribution Channel Analysis

Online Retail dominates with 44.13% due to wide product variety, convenience, and global accessibility.

In 2025, Online Retail held a dominant market position in the By Distribution Channel segment of the Privacy Filter Market, with a 44.13% share. E-commerce platforms offer consumers an extensive selection of privacy filter products at competitive prices, with the added convenience of home delivery and easy comparison shopping across brands and specifications.

Offline Retail continues to serve a significant portion of buyers who prefer to inspect products before purchasing, particularly in regions with lower e-commerce penetration. Electronics retail chains and specialty stores offer in-person support and product demonstrations. Moreover, corporate procurement teams often rely on offline retail and authorized distributors for bulk purchasing agreements.

Direct OEM Integration involves privacy filter products being bundled or pre-installed as part of device packages sold directly by manufacturers. This channel is gaining traction as device makers and enterprise vendors develop co-branded privacy solutions. Therefore, direct OEM integration is expected to grow steadily, particularly in corporate and government bulk device procurement programs.

Key Market Segments

By Product Type

- 2-Way Privacy Filters

- 4-Way Privacy Filters

- Touch-Screen Optimized Filters

- Integrated OEM Privacy Displays

By Material Technology

- Microlouver Film Filters

- Nanotechnology-Based Filters

- Electrochromic Switchable Filters

By Device Size

- 15–24 Inch Screens

- Less than or equal to 15 Inch Screens

- Above 24 Inch Screens

By End-User Industry

- Corporate Offices

- Healthcare Facilities

- Financial Services

- Government Agencies

- Educational Institutions

- Others

By Distribution Channel

- Online Retail

- Offline Retail

- Direct OEM Integration

Drivers

Rising Device Usage and Data Privacy Awareness Drive Privacy Filter Market Growth

The rapid growth in laptop, tablet, and smartphone usage globally is creating strong demand for screen privacy protection solutions. As device penetration increases across both developed and emerging markets, users in corporate, government, and healthcare sectors are actively seeking reliable tools to prevent unauthorized access to on-screen data.

Rising consumer awareness of personal data security during device usage in public spaces is a key driver for the privacy filter market. Employees, students, and frequent travelers now recognize the risk of shoulder surfing in airports, cafes, and co-working spaces. Consequently, both individual buyers and enterprise procurement teams are prioritizing privacy filters as essential accessories.

Furthermore, the expansion of remote work, digital learning, and mobile workstyles is significantly increasing the need for screen privacy solutions. Workers accessing confidential business data from home offices, shared spaces, or public environments require reliable visual protection. Therefore, demand for privacy filters is accelerating steadily across all major end-user segments and device categories.

Restraints

Built-In Privacy Features and User Experience Limitations Restrain Privacy Filter Market Adoption

The growing availability of built-in privacy display features in modern consumer electronic devices poses a significant challenge to the aftermarket privacy filter segment. Device manufacturers are increasingly integrating privacy screen modes directly into laptops, monitors, and smartphones. Therefore, some buyers are choosing devices with native privacy capabilities over separately purchased filter accessories.

Additionally, reduced screen brightness is a notable concern associated with privacy filter use. Many users report that standard privacy filters can noticeably dim display output, affecting visual comfort during extended use. This tradeoff between privacy protection and display quality discourages adoption, particularly among users who prioritize screen performance for creative, design, or multimedia applications.

Limited viewing angles, while central to the privacy function, also present usability challenges in collaborative work settings. Team members and colleagues who need to view the same screen simultaneously find privacy filters inconvenient or impractical. Moreover, budget-tier filter products often compound these issues with substandard optical quality, further deterring new users from adopting the technology.

Growth Factors

Smartphone Adoption, E-Commerce Expansion, and Multi-Function Products Accelerate Privacy Filter Market Growth

Rising demand for privacy protection solutions for smartphones, tablets, and portable displays is opening new growth avenues for the market. As personal devices become the primary tool for financial transactions, communication, and work, consumers are increasingly investing in screen privacy accessories. This shift is broadening the total addressable market well beyond traditional laptop and desktop categories.

The expansion of online retail platforms is improving the global availability of privacy filters, particularly in markets with limited offline distribution. E-commerce channels enable manufacturers and resellers to reach consumers across geographies efficiently. Moreover, competitive pricing, user reviews, and easy returns on digital platforms are encouraging first-time buyers to explore and purchase privacy filter products.

Growing consumer interest in multi-functional screen protection products is a strong growth catalyst for the market. Products that combine privacy protection with blue light reduction, anti-glare coatings, and screen scratch protection are gaining strong traction. Therefore, manufacturers investing in value-added innovations are well positioned to capture a larger share of both consumer and enterprise market demand.

Emerging Trends

Ultra-Thin Designs, Blue Light Integration, and Custom-Fit Products Shape the Privacy Filter Market

The development of ultra-thin and magnetic removable privacy filters is a leading trend in the consumer electronics accessories space. These products offer easy attachment and removal without adhesives, improving user experience significantly. Moreover, magnetic mounting systems are being designed for a wide range of laptop and monitor models, supporting flexible everyday use for mobile professionals.

Integration of blue light reduction and anti-glare technologies into privacy screens is rapidly gaining market momentum. Manufacturers are combining multiple screen protection features into single products to deliver greater value. Consequently, health-conscious consumers and employers focused on employee wellness are increasingly selecting privacy filters that address both data security and digital eye strain simultaneously.

Furthermore, the growing popularity of device-specific custom-fit privacy filters is reshaping product development strategies across the industry. Manufacturers are offering filters tailored to exact screen dimensions and device models, ensuring better adhesion, optical clarity, and a cleaner appearance. Therefore, custom-fit products are becoming the preferred choice among premium buyers across corporate, healthcare, and government procurement channels.

Regional Analysis

North America Dominates the Privacy Filter Market with a Market Share of 34.71%, Valued at USD 0.45 Billion

North America leads the global Privacy Filter Market with a 34.71% share, valued at approximately USD 0.45 Billion in 2025. The region benefits from a large base of corporate enterprises, government agencies, and financial institutions that prioritize visual data security. Additionally, strong regulatory frameworks and high device penetration rates continue to sustain robust market demand across the US and Canada.

Europe Privacy Filter Market Trends

Europe represents the second largest regional market, driven by stringent data protection regulations including GDPR. Organizations across the region are actively investing in physical security tools to complement their digital compliance programs. Moreover, countries such as Germany, the UK, and France have well-established enterprise procurement processes that regularly include privacy screens as part of device security standards.

Asia Pacific Privacy Filter Market Trends

Asia Pacific is the fastest growing region in the global Privacy Filter Market, supported by rapid digitalization, expanding corporate infrastructure, and increasing smartphone penetration. Countries such as China, India, Japan, and South Korea are witnessing strong demand growth. Furthermore, the expansion of e-commerce and improving retail distribution networks are making privacy filter products more accessible across the region.

Middle East and Africa Privacy Filter Market Trends

The Middle East and Africa region is gradually increasing its share of the global privacy filter market, supported by growing awareness of data security in government and financial sectors. GCC countries, particularly the UAE and Saudi Arabia, are investing in digital infrastructure and enterprise security tools. However, limited consumer awareness and lower device penetration in parts of Africa continue to restrain market growth.

Latin America Privacy Filter Market Trends

Latin America represents an emerging market with steady growth potential, particularly in Brazil and Mexico. Rising smartphone and laptop adoption among working professionals and students is creating foundational demand for screen privacy accessories. Additionally, the growing presence of global e-commerce platforms is gradually improving product availability and consumer awareness of privacy filter solutions across the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

3M Company is widely regarded as a pioneer and global leader in the privacy filter market. The company’s MicroLouver optical film technology has defined industry standards for viewing angle restriction and display clarity. With a broad product portfolio spanning laptops, monitors, and mobile devices, 3M maintains a strong presence across enterprise, government, and retail distribution channels worldwide.

Lapcare is a prominent Indian brand that has established a solid foothold in the affordable laptop accessories segment, including privacy filters. The company focuses on cost-effective solutions designed for the price-sensitive South and Southeast Asian consumer base. Moreover, Lapcare leverages domestic distribution networks and growing e-commerce channels to expand its reach across both individual and small business buyers.

Targus International LLC is a globally recognized brand known for laptop bags, docking stations, and screen privacy accessories. The company offers a comprehensive range of privacy filters for laptops and monitors used in enterprise and travel environments. Additionally, Targus serves a broad corporate customer base through strategic partnerships with major retailers and direct business-to-business procurement programs internationally.

Kensington Computer Products Group (ACCO Brands Corporation) is a well-established player in the privacy filter market, offering products under its trusted PrivacyScreen product line. The company recently expanded its portfolio with the launch of filters featuring Eyesafe® technology, combining data protection with advanced blue light filtration. Kensington serves enterprise, government, and education segments through a strong global distribution network.

Key Players

- 3M Company

- Lapcare

- Targus International LLC

- Kensington Computer Products Group (ACCO Brands Corporation)

- Fellowes Inc.

- HP Inc.

- Dell Technologies Inc.

- V7 – Ingram Micro Inc.

- ViewSonic Corporation

- Lenovo Group Limited

- ZAGG Inc.

- PanzerGlass A/S

- Tech Armor LLC

- Amazon Basics (Amazon.com Inc.)

- Belkin International Inc.

- DMC Co. Ltd.

- Dicota GmbH

- Klear Screen LLC

- GlareGuard Screen Protectors LLC

- MOSISO (Mosiso LAB, Inc.)

- JCPal Technology Ltd.

- Others

Recent Developments

- June 2025 – Kensington launched its new Privacy Screen Filters featuring Eyesafe® Technology, combining screen-based data protection with advanced blue light filtration. The product is designed for corporate and healthcare users seeking a dual-purpose screen privacy and eye safety solution in a single accessory.

- October 2025 – Pxin launched privacy filters equipped with BLUVLIGHTBLOCK® technology for laptops, tablets, smartphones, and MacBook devices. The product targets protection from shoulder-surfing and digital eye strain, offering a multi-functional solution aimed at mobile professionals and students across consumer and enterprise markets.

- February 2026 – Samsung unveiled the Privacy Display feature as part of the Samsung Galaxy S26 Ultra. This integrated OEM privacy functionality allows users to restrict screen visibility directly from device settings, positioning Samsung as an early mover in the built-in privacy display segment for premium smartphones.

Report Scope

Report Features Description Market Value (2025) USD 1.29 Billion Forecast Revenue (2035) USD 3.38 Billion CAGR (2026-2035) 10.12% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (2-Way Privacy Filters, 4-Way Privacy Filters, Touch-Screen Optimized Filters, Integrated OEM Privacy Displays), By Material Technology (Microlouver Film Filters, Nanotechnology-Based Filters, Electrochromic Switchable Filters), By Device Size (15–24 Inch Screens, Less than or equal to 15 Inch Screens, Above 24 Inch Screens), By End-User Industry (Corporate Offices, Healthcare Facilities, Financial Services, Government Agencies, Educational Institutions, Others), By Distribution Channel (Online Retail, Offline Retail, Direct OEM Integration) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape 3M Company, Lapcare, Targus International LLC, Kensington Computer Products Group (ACCO Brands Corporation), Fellowes Inc., HP Inc., Dell Technologies Inc., V7 – Ingram Micro Inc., ViewSonic Corporation, Lenovo Group Limited, ZAGG Inc., PanzerGlass A/S, Tech Armor LLC, Amazon Basics (Amazon.com Inc.), Belkin International Inc., DMC Co. Ltd., Dicota GmbH, Klear Screen LLC, GlareGuard Screen Protectors LLC, MOSISO (Mosiso LAB, Inc.), JCPal Technology Ltd., Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- 3M Company

- Lapcare

- Targus International LLC

- Kensington Computer Products Group (ACCO Brands Corporation)

- Fellowes Inc.

- HP Inc.

- Dell Technologies Inc.

- V7 - Ingram Micro Inc.

- ViewSonic Corporation

- Lenovo Group Limited

- ZAGG Inc.

- PanzerGlass A/S

- Tech Armor LLC

- Amazon Basics (Amazon.com Inc.)

- Belkin International Inc.

- DMC Co. Ltd.

- Dicota GmbH

- Klear Screen LLC

- GlareGuard Screen Protectors LLC

- MOSISO (Mosiso LAB, Inc.)

- JCPal Technology Ltd.

- Others

Our Clients

- 180323

- Feb 2026