Quick Navigation

Report Overview

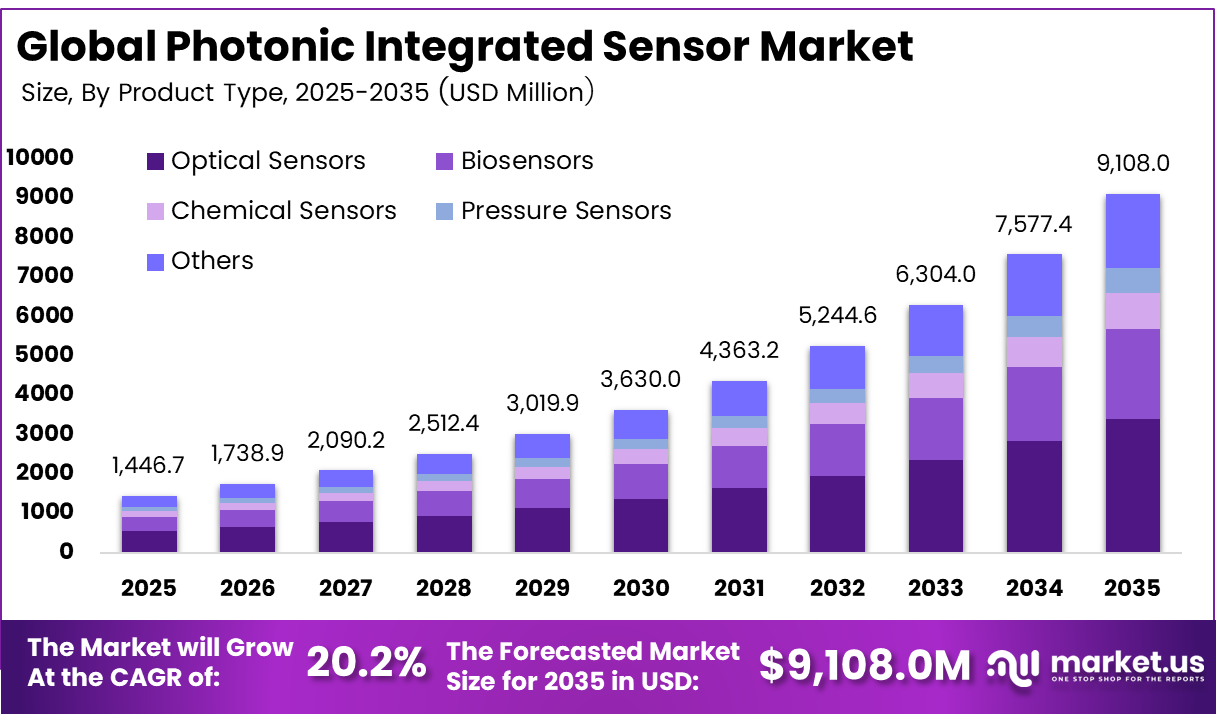

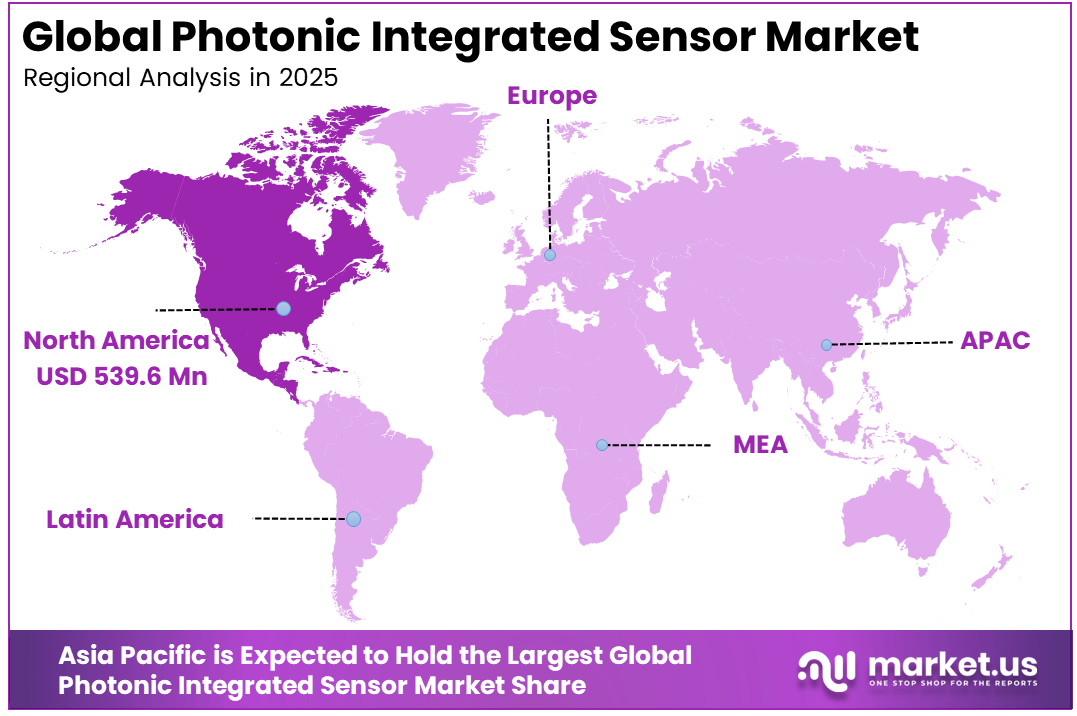

The Global Photonic Integrated Sensor Market size is expected to be worth around USD 9,108.0 million by 2035, from USD 1,446.7 million in 2025, growing at a CAGR of 20.2% during the forecast period from 2025 to 2035. North America held a dominant market position, capturing more than a 37.3% share, holding USD 539.6 million in revenue.

A photonic integrated sensor refers to a device that combines optical sensing elements and signal processing functions onto a single chip. It uses light to detect physical or chemical changes such as temperature, pressure, or strain, offering high sensitivity, stability, and compact design suitable for advanced industrial, medical, and infrastructure applications.

The growth of photonic sensing solutions is supported by rising demand for precise and real-time measurement across automation, healthcare diagnostics, and smart infrastructure. Optical sensors are preferred as they detect small variations in temperature, strain, and refractive index with higher reliability. Integration on chip enhances stability and repeatability and enables high channel density for monitoring.

The market for photonic integrated sensors is driven by rising demand for accurate and continuous monitoring across healthcare, industrial automation, and smart infrastructure. These sensors offer high sensitivity and stable performance, enabling precise detection of physical and chemical changes. Growing use in data centers, environmental sensing, and advanced diagnostics is further supporting adoption across critical and technology-driven applications.

Demand is increasing as industries shift from periodic inspection to continuous sensing systems. Integrated photonics reduces power consumption and improves long-term drift performance in distributed networks. In industrial and energy environments, a single chip supporting multiple sensing points helps reduce component complexity and simplifies calibration, improving operational efficiency over equipment life cycles.

For instance, in March 2026, Mellanox, now part of NVIDIA, is referenced among companies active in silicon photonics-enabled interconnects. As AI data center networks upgrade to 400G and beyond, demand rises for integrated optical modules with built-in monitoring functions, indirectly accelerating the adoption of photonic integrated sensor designs in high-performance networking gear.

Key Takeaway

- In 2025, the Optical Sensors segment held a dominant market position, capturing a 37.4% share of the Global Photonic Integrated Sensor Market.

- In 2025, the Silicon Photonics (SiPh) segment held a dominant market position, capturing a 44.6% share of the Global Photonic Integrated Sensor Market.

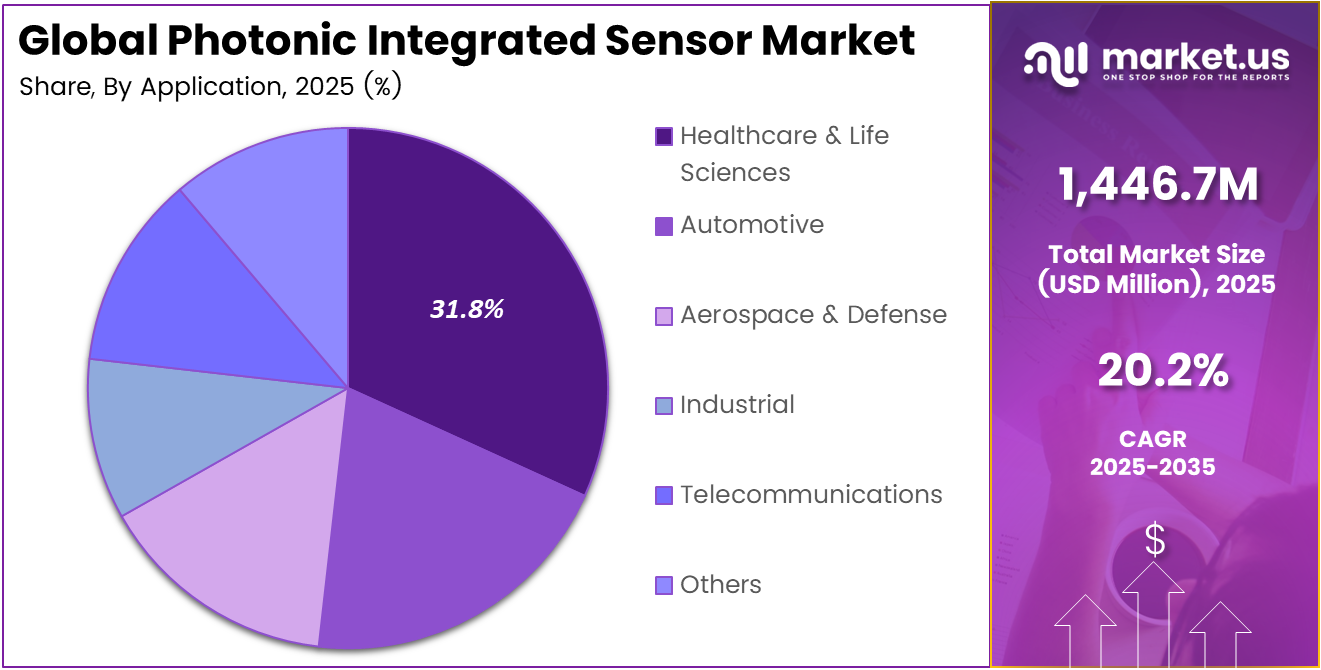

- In 2025, the Healthcare & Life Sciences segment held a dominant market position, capturing a 31.8% share of the Global Photonic Integrated Sensor Market.

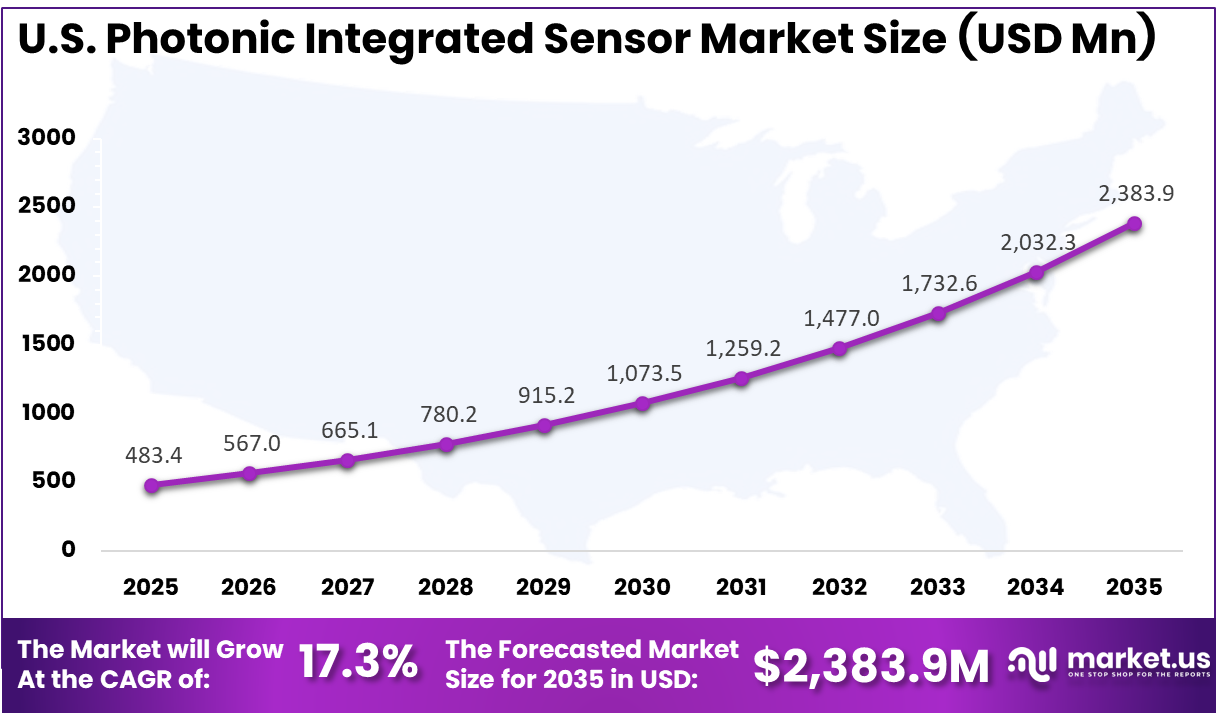

- The U.S. Photonic Integrated Sensor Market was valued at USD 483.4 Million in 2025, with a robust CAGR of 17.3%.

- In 2025, North America held a dominant market position in the Global Photonic Integrated Sensor Market, capturing more than a 37.3% share.

Role of Generative AI

Generative AI is improving how photonic integrated sensors are designed, tested, and calibrated. It helps convert raw optical signals into clearer insights for real-time analytics, anomaly detection, and field monitoring. This supports more intelligent sensing systems with better accuracy, faster response, and lower manual intervention.

AI workloads are also increasing the demand for photonics in data centers and high-performance computing. Optical interconnects and co-packaged optics are being adopted to support faster data movement in next-generation AI servers. This shift is creating stronger investment interest in silicon photonics and advanced sensor integration.

Investment and Business Benefits

Investment is expanding in photonic integrated circuit foundries, advanced packaging solutions, and application-specific sensor designs. Growth areas include biosensing, structural monitoring, and emerging quantum measurement systems. Opportunities also exist for companies developing design software, standardized platforms, and turnkey modules that simplify adoption for users without specialized photonics expertise.

Organizations benefit through reduced maintenance costs, improved system reliability, and fewer unexpected failures. Continuous optical monitoring enables early fault detection and accurate performance tracking. Integration of compact photonic sensors into existing systems allows companies to enhance product capabilities, including temperature and chemical sensing, without requiring significant design changes.

Regional Analysis

In 2025, North America held a dominant market position in the Global Photonic Integrated Sensor Market, capturing more than a 37.3% share, holding USD 539.6 million in revenue. This dominance is due to strong photonics research, advanced semiconductor manufacturing, and early adoption of optical sensing in healthcare, defense, telecom, and industrial automation. North America also benefits from high investment in data centers, smart infrastructure, and precision diagnostics. The presence of skilled engineering talent and strong demand for compact, accurate sensors further supports regional leadership.

For instance, in January 2025, at OFC, Intel’s U.S. photonics group showcased the first fully integrated optical compute interconnect chiplet co-packaged with a CPU and running live data. This silicon photonics breakthrough boosts bandwidth and reduces power, reinforcing North America’s edge in integrated photonic I/O for AI, HPC, and future sensor-rich systems.

U.S. Photonic Integrated Sensor Market Size

The market for Photonic Integrated Sensors within the U.S. is growing tremendously and is currently valued at USD 483.4 million; the market has a projected CAGR of 17.3%. The market is growing due to the strong U.S. focus on advanced healthcare diagnostics, semiconductor innovation, defense systems, and high-speed communication networks. Rising use of optical sensing in smart manufacturing, medical devices, environmental monitoring, and data center infrastructure is supporting adoption. Government-backed research, strong photonics expertise, and demand for compact, accurate, and low-power sensors are also helping the market expand steadily.

For instance, in September 2025, Honeywell introduced its 13MM pressure sensor for ultra-clean semiconductor fabs, using advanced optical and sensing technology to deliver highly stable, low-drift measurements in demanding vacuum and high-temperature conditions. This strengthens U.S. leadership in high-purity, photonics-driven process sensing for chips and advanced manufacturing.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Product Type Analysis

In 2025, the Optical Sensors segment held a dominant market position, capturing a 37.4% share of the Global Photonic Integrated Sensor Market. This dominance is due to the strong ability of optical sensors to deliver highly accurate and stable measurements across different environments. Their capability to detect small changes in physical and chemical parameters makes them suitable for advanced sensing tasks in industrial systems, medical diagnostics, and infrastructure monitoring applications.

Optical sensors are also preferred because they offer fast response times and reliable performance over long periods. Their non-electrical nature reduces interference risks, which improves data quality. As industries move toward continuous monitoring, these sensors are widely adopted for precision-driven applications requiring consistent and dependable sensing performance.

For instance, in September 2025, Honeywell introduced a new cleanroom pressure sensor to support advanced semiconductor manufacturing, highlighting its focus on precise, contamination-free sensing based on optical and photonic principles. This kind of development underlines how optical style sensing is being adapted to demanding environments where stability and accuracy matter.

Material Analysis

In 2025, the Silicon Photonics (SiPh) segment held a dominant market position, capturing a 44.6% share of the Global Photonic Integrated Sensor Market. This dominance is due to the compatibility of silicon photonics with existing semiconductor manufacturing processes. This allows large-scale production and cost efficiency while maintaining high performance. The material supports compact integration of optical and electronic components, which helps in developing smaller and more efficient sensing devices.

Silicon photonics also enables high-density integration, allowing multiple sensing functions on a single chip. This improves system stability and reduces overall complexity. Its ability to support advanced signal processing and miniaturisation makes it a preferred choice for next-generation sensing solutions across multiple industrial and technology-driven applications.

For instance, in April 2025, at OFC 2025, Intel showcased a 1.6 terabit per second photonic integrated circuit with integrated lasers, built on its silicon photonics platform. The demonstration highlighted how SiPh processes can deliver very high-speed optical links that also act as a foundation for advanced sensing and monitoring functions on chip.

Application Analysis

In 2025, the Healthcare & Life Sciences segment held a dominant market position, capturing a 31.8% share of the Global Photonic Integrated Sensor Market. This dominance is due to the increasing need for accurate, real-time diagnostic and monitoring tools in healthcare. Photonic integrated sensors support precise detection of biological and chemical changes, making them useful for medical testing, imaging, and wearable health devices that require continuous and reliable measurement.

The growing focus on early disease detection and personalised healthcare is further supporting adoption. These sensors allow compact and non-invasive solutions, improving patient comfort and testing efficiency. Their use in laboratory research and clinical environments continues to expand as demand for high precision and reliable diagnostic tools increases.

For instance, in September 2025, Aeva introduced a new motion sensor using silicon photonics-based FMCW technology, designed for precise non-contact measurements. While focused on motion, the underlying approach demonstrates how photonic integration can deliver compact, high-resolution sensing platforms that are also attractive for medical devices and life science instruments.

Key Market Segments

By Product Type

- Optical Sensors

- Biosensors

- Chemical Sensors

- Pressure Sensors

- Others

By Material

- Silicon Photonics

- Indium Phosphide

- Silicon Nitride

- Others

By Application

- Healthcare & Life Sciences

- Automotive

- Aerospace & Defense

- Industrial

- Telecommunications

- Others

Emerging Trends

A major trend is the integration of AI and ML with photonic sensing hardware. These systems can process data on a chip, classify signals, and adapt to changing conditions in real time. Miniaturised and wearable-ready sensor designs are also gaining attention as industries move toward smarter sensing formats.

Hyperspectral, multispectral, and quantum photonic sensors are becoming important for environmental monitoring, defence, and medical diagnostics. These sensors provide richer spectral data and higher sensitivity in compact forms. Demand is rising for rugged devices that can deliver laboratory-grade precision across wider spectral bands.

Growth Factors

Industry 4.0 and smart manufacturing are key growth factors for photonic integrated sensors. Factories need real-time data on vibration, strain, temperature, and chemistry to reduce downtime and improve asset performance. These sensors support continuous monitoring in demanding industrial environments with high reliability.

Smart city projects are also supporting adoption through traffic systems, structural health monitoring, and environmental sensing. In addition, 5G rollout and high-speed optical networks require precise monitoring across fibre infrastructure. This creates steady demand for low-power, durable, and highly accurate photonic sensing solutions.

Market Dynamics

Drivers - Real-Time Precision Needs

The need for real-time precision is strongly driving the adoption of photonic integrated sensors across industries. These sensors enable continuous monitoring of parameters such as temperature, strain, and chemical changes with high sensitivity, which is important for healthcare systems, industrial automation, and infrastructure monitoring applications.

As systems become more connected, there is a growing focus on reducing downtime and improving operational efficiency. Photonic sensors support accurate and fast data capture, helping users detect issues early and maintain system reliability. This makes them valuable for environments where precise and consistent measurement is essential.

For instance, in March 2026, Intel continues to highlight silicon photonics and photonic integrated circuits for very fast data links between servers and accelerators in data centers. This focus reflects end-user demand for real-time, low-latency sensing and monitoring in high-performance computing, cloud, and AI workloads that rely on precise optical links.

Restraint - Integration Complexity

Integration complexity remains a key restraint as photonic sensors require careful alignment with electronic components and optical interfaces. This process can be technically demanding, especially when combining multiple sensing functions on a single chip while maintaining signal quality and stability across different operating conditions.

The lack of standardised integration approaches also adds to the challenge. Manufacturers often need customised designs and assembly processes, which can increase development time and limit scalability. These factors make it harder for some industries to adopt photonic integrated sensors at a faster pace.

For instance, in January 2025, Thorlabs’ acquisition of Praevium Research strengthened its position in swept-source and integrated optical technologies. The move implicitly recognizes the difficulty of bringing advanced photonic engines into compact systems, where integration of sources, modulators, and detection requires deep design expertise and tight coordination across fabrication and packaging workflows.

Opportunities - Convergence with AI

The convergence of photonic sensors with artificial intelligence presents strong opportunities for advanced sensing systems. AI can analyse large volumes of optical data, identify patterns, and support real-time decision making, which enhances the overall value of sensing platforms across industrial, healthcare, and environmental applications.

This integration allows sensors to move beyond simple data collection toward predictive and adaptive capabilities. Intelligent systems can improve accuracy, reduce noise, and automate responses, making them more effective in complex environments. This trend is opening new use cases where smart sensing is required for continuous and reliable operations.

For instance, in April 2026, Infinera’s photonic integrated circuits underpin transport platforms that generate rich telemetry on channel quality and fiber conditions. Industry discussions on AI in networks suggest that this kind of detailed optical sensing data can be leveraged by AI engines for self-optimizing networks, aligning the company with AI–photonics convergence trends.

Challenges - Talent Gap

A major challenge in the market is the shortage of skilled professionals with expertise in photonics, semiconductor design, and system integration. Developing and deploying photonic integrated sensors requires specialised knowledge that is not widely available across all regions and industries.

This talent gap can slow innovation and delay product development cycles. Companies may face difficulty in scaling operations or maintaining advanced systems without the required technical expertise. Addressing this issue will require focused training programs and stronger collaboration between industry and academic institutions.

For instance, in October 2022, Cisco expanded its Networking Academy to train millions of people in digital and networking skills, citing a growing gap between technology needs and available talent. The program shows how complex infrastructure, including advanced optical and sensing technologies, depends on a workforce that is currently in short supply.

Key Players Analysis

One of the leading players in March 2026, Intel continued to expand its silicon photonics portfolio for high-speed optical interconnects in cloud and AI infrastructure. Industry analyses highlight Intel as a leading supplier of integrated photonic devices that combine modulators, detectors, and waveguides on a single chip, supporting denser, more power-efficient sensing and monitoring within hyperscale data centers.

Top Key Players in the Market

- Honeywell International Inc.

- Thorlabs Inc.

- Intel Corporation

- Cisco Systems Inc.

- Finisar Corporation

- Broadcom Inc.

- Lumentum Holdings Inc.

- NeoPhotonics Corporation

- Hamamatsu Photonics K.K.

- Mellanox Technologies Ltd.

- Infinera Corporation

- II-VI Incorporated

- VPIphotonics

- Sicoya GmbH

- Fujitsu Limited

- Others

Recent Developments

- In March 2026, NeoPhotonics, now operating under new ownership but still referenced in silicon photonics sensor market coverage, is recognized for high-speed coherent modules built on sophisticated PICs. Its designs integrate lasers, modulators, and receivers that inherently act as precision optical sensors for performance monitoring across long-haul and data-center links.

- In March 2026, Hamamatsu is highlighted among leading optoelectronic and sensor vendors participating in the silicon photonics sensor ecosystem. The firm’s expertise in photodiodes, image sensors, and spectroscopy modules positions it well as more functionality moves onto integrated photonic platforms for environmental, medical, and industrial sensing.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1446.7 Million |

| Forecast Revenue (2035) | USD 9,108.0 Million |

| CAGR (2026-2035) | 20.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Optical Sensors, Biosensors, Chemical Sensors, Pressure Sensors, Others), By Material (Silicon Photonics, Indium Phosphide, Silicon Nitride, Others), By Application (Healthcare, Automotive, Aerospace & Defense, Industrial, Telecommunications, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Honeywell International Inc., Thorlabs Inc., Intel Corporation, Cisco Systems Inc., Finisar Corporation, Broadcom Inc., Lumentum Holdings Inc., NeoPhotonics Corporation, Hamamatsu Photonics K.K., Mellanox Technologies Ltd., Infinera Corporation, II-VI Incorporated, VPIphotonics, Sicoya GmbH, Fujitsu Limited, Others |

| Customization Scope | Customization at the segment and region/country levels will be provided. Moreover, customization can be tailored to the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |