Quick Navigation

Report Overview

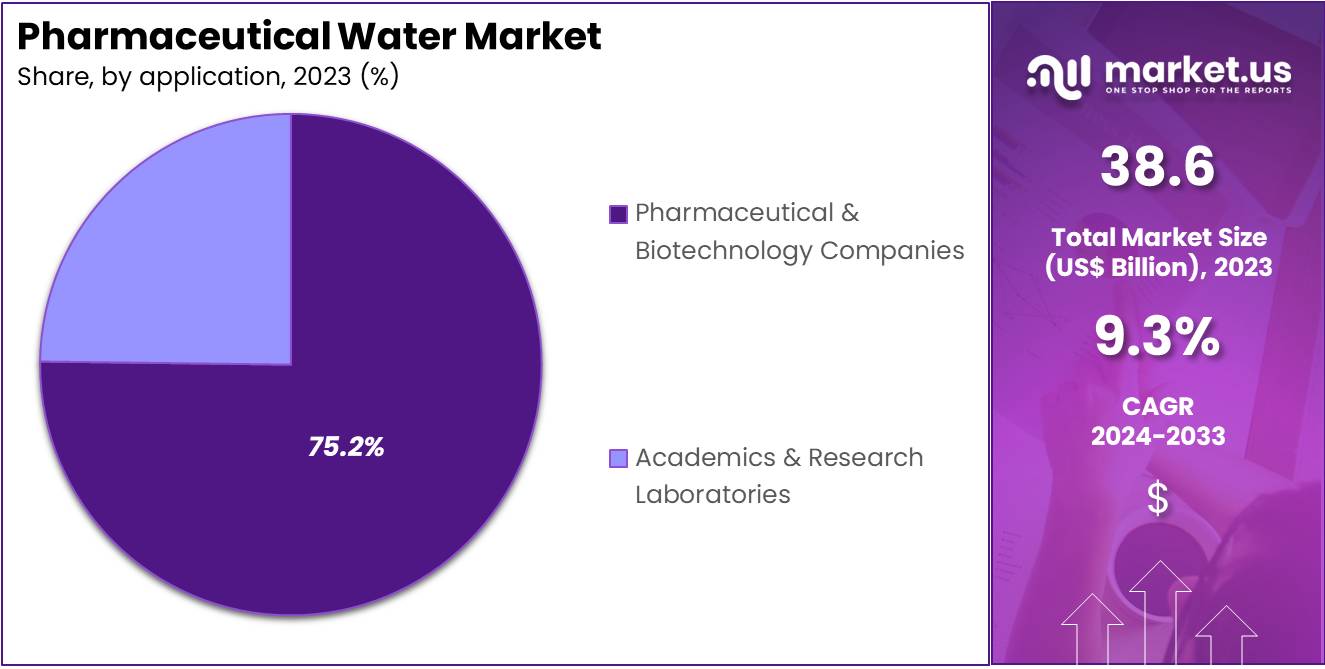

The Global Pharmaceutical Water Market Size is expected to be worth around US$ 93.9 Billion by 2033, from US$ 38.6 Billion in 2023, growing at a CAGR of 9.3% during the forecast period from 2024 to 2033.

Rising demand for high-quality pharmaceutical water across diverse applications, such as parenteral solutions, intravenous fluids, and active pharmaceutical ingredients (APIs), is driving the growth of the pharmaceutical water market. Strict regulations on water purity and increasing emphasis on patient safety in drug production have created opportunities for the development of advanced water purification technologies.

Pharmaceutical water plays a critical role in drug formulation, manufacturing, and research, where water of specific grades, like Water for Injection (WFI) and Purified Water, ensures the efficacy and safety of medicines. In addition, the rise of biologics and personalized medicine, which require precise water formulations, further fuels market growth.

Increasing research and development activities, including the collaboration between Ono Pharmaceutical Co., Ltd. and Sibylla Biotech in March 2024 to explore novel treatments for neurological disorders, highlight the expanding scope of pharmaceutical innovations requiring high-quality water. Recent trends also reflect a shift toward eco-friendly purification methods, as sustainability gains prominence within the industry. Additionally, the growing focus on cost-effective production methods creates opportunities for players to develop and adopt energy-efficient water treatment technologies.

Key Takeaways

- In 2023, the market for Pharmaceutical Water generated a revenue of US$ 38.6 billion, with a CAGR of 9.3%, and is expected to reach US$ 93.9 billion by the year 2033.

- The product type segment is divided into water for injection and HPLC grade water, with water for injection taking the lead in 2023 with a market share of 85.3%.

- Considering application, the market is divided into academics & research laboratories and pharmaceutical & biotechnology companies. Among these, pharmaceutical & biotechnology companies held a significant share of 75.2%.

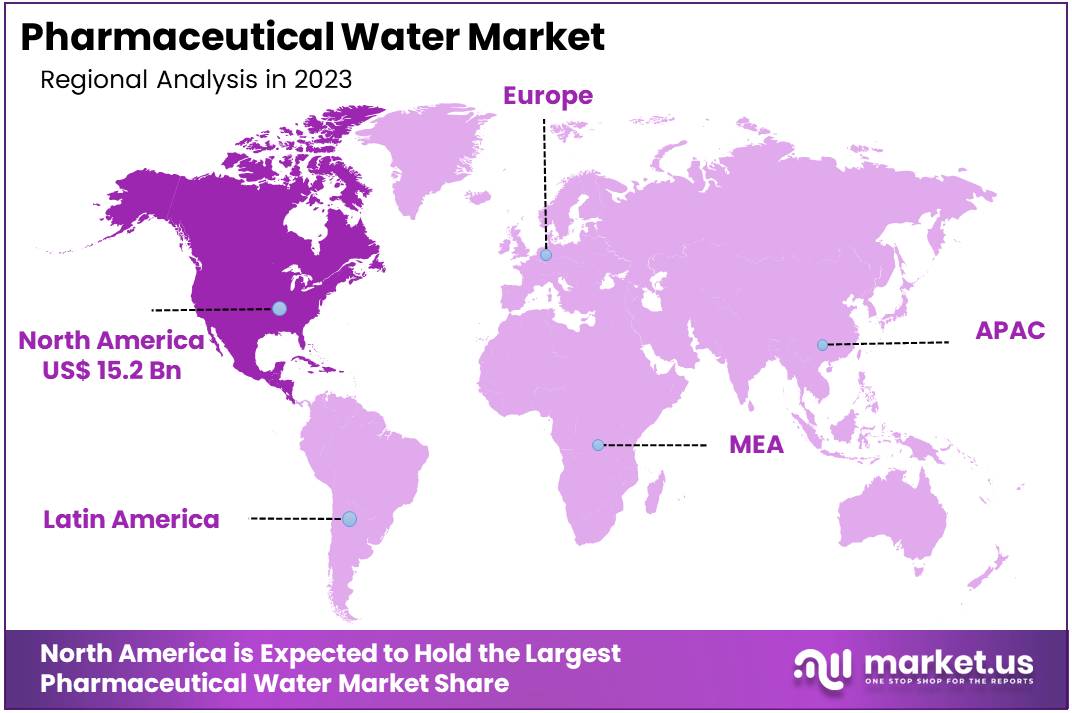

- North America led the market by securing a market share of 39.4% in 2023.

Product Type Analysis

The water for injection segment led in 2023, claiming a market share of 85.3% owing to the rising demand for high-quality water in the production of injectable medicines. Water for injection (WFI) and HPLC-grade water are projected to witness strong demand due to the growing emphasis on ensuring purity and sterility in pharmaceutical products.

The increasing prevalence of chronic diseases and the expansion of injectable drug manufacturing are anticipated to boost WFI demand. Moreover, the surge in biopharmaceutical innovations, such as vaccines and biologics, is likely to drive the need for high-quality water in production processes. Additionally, stringent regulatory requirements and quality control standards are estimated to support the growing demand for WFI and HPLC-grade water in the industry, especially for injectable drugs, where water quality is crucial to preventing contamination and ensuring patient safety.

Application Analysis

The pharmaceutical & biotechnology companies held a significant share of 75.2% due to an increasing focus on drug development and research activities. The rise in biotechnology innovations, including personalized medicines, gene therapies, and biosimilars, is likely to spur the demand for high-quality water in laboratories and manufacturing settings. Academic and research laboratories are expected to remain key consumers of pharmaceutical-grade water, with the need for consistent water purity in experiments and formulations.

Furthermore, the expanding global pharmaceutical industry, fueled by both emerging market growth and increasing drug production, is projected to further elevate the demand for reliable water sources. The rising number of clinical trials and expanding production capacities in the biotechnology sector is estimated to contribute to the segment’s growth, as these companies require consistent, high-quality water for critical research and manufacturing processes.

Key Market Segments

By Product Type

- Water for Injection

- HPLC Grade Water

By Application

- Academics & Research Laboratories

- Pharmaceutical & Biotechnology Companies

Drivers

Increasing Innovation Driving the Pharmaceutical Water Market

Increasing innovation in the pharmaceutical and biotherapeutics sectors significantly drives the demand for specialized water types, such as Water for Injection (WFI) and Purified Water (PW). The development of advanced water treatment technologies, including membrane filtration and deionization processes, enhances the purity and efficiency of water used in pharmaceutical manufacturing.

In July 2022, ILC Dover LP, a leader in single-use solutions for the pharmaceutical industry, introduced WFI to the biotherapeutics sector, highlighting the growing need for high-quality water in drug production. These technological advancements make it easier for pharmaceutical companies to meet the stringent water quality standards set by regulatory authorities, which are expected to become even more stringent in the future.

Additionally, the rising focus on biopharmaceuticals and personalized medicine drives demand for custom water solutions tailored to specific product needs. Innovation also leads to cost-effective solutions, improving water treatment systems’ scalability and operational efficiency.

Companies that invest in research and development are likely to see a competitive edge in meeting the evolving requirements for water usage in pharmaceutical production. These innovations in water treatment processes and equipment are anticipated to sustain the growth of the market and support the pharmaceutical industry’s dynamic needs.

Restraints

Stringent Regulatory Standards Impeding Market Growth

One significant restraint in the pharmaceutical water market is the high cost of compliance with increasingly stringent regulatory standards. Regulatory bodies such as the U.S. FDA, European Medicines Agency (EMA), and World Health Organization (WHO) impose rigorous guidelines on the use of water in pharmaceutical production, including Water for Injection (WFI) and Purified Water (PW).

These regulations ensure the water is free from contaminants and complies with strict microbial and chemical limits. The constant need to meet these high standards can be costly and time-consuming for pharmaceutical companies. Maintaining compliance requires investing in sophisticated water treatment technologies, regular testing, and system maintenance, all of which contribute to rising operational costs.

Moreover, these stringent requirements also increase the complexity of water treatment infrastructure, requiring specialized equipment and qualified personnel. This results in longer timelines for product development and production, potentially delaying market entry. Additionally, as regulations continue to evolve, companies must adapt quickly, further increasing the risk of compliance errors and impacting profitability.

Opportunities

Increasing Opportunities from Rapid Drug Approvals in the Pharmaceutical Water Market

Increasing approval rates of new drugs by regulatory bodies present a significant opportunity for the pharmaceutical water market. As regulatory agencies streamline approval processes and adapt to the rapid pace of medical advancements, pharmaceutical companies are expected to launch new drugs at an accelerated rate.

This growing demand for new drugs is anticipated to drive the need for high-quality water for production, including Water for Injection (WFI) and other specialized forms of purified water. Regulatory bodies, including the FDA, have been working to expedite approvals for critical therapies, particularly for rare diseases and oncology treatments. This trend is projected to boost the market for pharmaceutical water as drug manufacturers require large volumes of pure, compliant water for the production of these therapies.

Moreover, the increasing focus on biopharmaceuticals and personalized medicine is likely to require even more precise and customized water solutions for drug manufacturing. As new drug development continues to gain momentum, pharmaceutical companies are expected to invest heavily in water treatment technologies to meet the increasing demand for high-quality water. These factors combined are estimated to create sustained opportunities for growth in the pharmaceutical water market, further strengthening its role in drug production.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic trends and geopolitical developments significantly influence the pharmaceutical water market. On the positive side, the increasing demand for healthcare services due to an aging global population and rising chronic diseases fuels growth in pharmaceutical production, which in turn drives the need for high-quality water in manufacturing processes.

However, economic challenges such as inflation, regulatory pressures, and supply chain disruptions often elevate operational costs and slow down production. Trade restrictions and geopolitical tensions also complicate the global distribution of raw materials essential for pharmaceutical water treatment. These factors may lead to temporary shortages or price volatility. Despite these challenges, the pharmaceutical water sector is expected to maintain steady growth due to ongoing advancements in water purification technologies and regulatory support for the pharmaceutical industry’s infrastructure.

Trends

The Role of Partnerships and Collaborations in the Pharmaceutical Water Market

Rising partnerships and collaborations play a pivotal role in advancing the pharmaceutical water market. Industry leaders are increasingly forming strategic alliances to enhance research, development, and production capabilities. These collaborations help address challenges related to stringent water quality standards and the growing complexity of pharmaceutical manufacturing processes.

In July 2024, Evotec SE announced a multi-year partnership with Pfizer, including a master research agreement, options, and licensing, focusing on early-stage research for infectious and metabolic diseases. This collaboration is expected to accelerate innovations in water treatment systems tailored for pharmaceutical applications. As the market grows, the synergy from these partnerships is anticipated to streamline operations and improve the efficiency of water usage, driving long-term sustainability in the sector.

Regional Analysis

North America is leading the Pharmaceutical Water Market

North America dominated the market with the highest revenue share of 39.4% owing to several key factors. A major contributor was the ongoing expansion of pharmaceutical manufacturing facilities, particularly in the United States and Canada. The rising demand for high-quality purified water, essential for drug production, is expected to continue fueling this growth.

Additionally, the region’s focus on improving the efficiency and quality of water treatment systems for pharmaceutical use has bolstered the market. The 2022 donation of US$27 million for facility development in Canada highlights the industry’s commitment to meeting growing demands and overcoming rising operational costs.

Furthermore, the increasing emphasis on stringent regulatory requirements regarding water quality has prompted pharmaceutical companies to invest heavily in advanced water purification technologies. These factors combined with the surge in biopharmaceutical production have contributed significantly to the market’s expansion in the region.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to rapid industrialization and increasing healthcare needs. Countries like China, India, and Japan are projected to see heightened demand for high-quality water in drug manufacturing. As the pharmaceutical sector in these nations grows, the need for state-of-the-art water purification systems is expected to rise, driven by expanding production capacities and stricter regulatory standards.

The rising prevalence of chronic diseases and an aging population are also likely to contribute to the increased demand for pharmaceutical products, thereby boosting the market. Moreover, the adoption of new technologies for water treatment, along with the region’s growing focus on sustainability, is expected to enhance the efficiency and safety of water used in pharmaceutical applications. These factors collectively position the market for steady growth in Asia Pacific throughout the forecast period.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the pharmaceutical water market adopt a variety of strategies to drive growth, such as investing in innovative purification technologies and expanding production capacities to meet rising demand. Companies also focus on forming strategic alliances and acquisitions to enhance their market presence and product portfolios.

Additionally, many players emphasize regulatory compliance and quality assurance to meet the stringent requirements of the pharmaceutical industry. Sustainable practices, like water recycling and energy-efficient systems, are also becoming central to their growth strategies. Moreover, global expansion into emerging markets with growing pharmaceutical industries supports their continued market share gains.

Thermo Fisher Scientific Inc. is a leading player in this market, offering a broad range of water purification solutions used in pharmaceutical manufacturing. The company leverages its strong R&D capabilities to innovate products that meet the high purity standards required by pharmaceutical companies. With a global presence, Thermo Fisher ensures robust distribution channels and customer support services, solidifying its position as a key player in this market.

Recent Developments

- In May 2024: Avenacy, a specialty pharmaceutical company focused on essential injectable drugs, introduced the FDA-approved magnesium sulfate in water for injection to the US market. This product is recommended for the prevention and treatment of seizures in cases of preeclampsia and eclampsia.

- In September 2023: Veolia Water Technologies introduced the PURELAB Pharma Compliance package, designed for businesses needing a reliable supply of ultrapure water (UPW) for quality control (QC) laboratories. The package includes all essential validation and certification software.

Top Key Players in the Pharmaceutical Water Market

- Veolia Water Technologies

- Pfizer, Inc.

- Merck KGaA

- Intermountain Life Sciences

- Fresenius Kabi AG

- Cytiva

- CovaChem, LLC

- Avenacy

- Asahi Kasei

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | US$ 38.6 Billion |

| Forecast Revenue (2033) | US$ 93.9 Billion |

| CAGR (2024-2033) | 9.3% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Water for Injection and HPLC Grade Water), By Application (Academics & Research Laboratories and Pharmaceutical & Biotechnology Companies) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Veolia Water Technologies, Pfizer, Inc., Merck KGaA, Intermountain Life Sciences, Fresenius Kabi AG, Cytiva, CovaChem, LLC, Avenacy, and Asahi Kasei. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |