Global Petrochemicals Market Size, Share, And Report Analysis By Product (Ethylene, Propylene, Butadiene, Benzene, Xylene, Toluene, Methanol), By Application (Polymers, Paints and Coatings, Solvents, Rubber, Adhesives and Sealants, Surfactants, Dyes, Other), By End-Use (Packaging, Electronics, Construction, Automotive, Others) , By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2034

- Published date: Jan 2025

- Report ID: 137938

- Number of Pages: 274

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

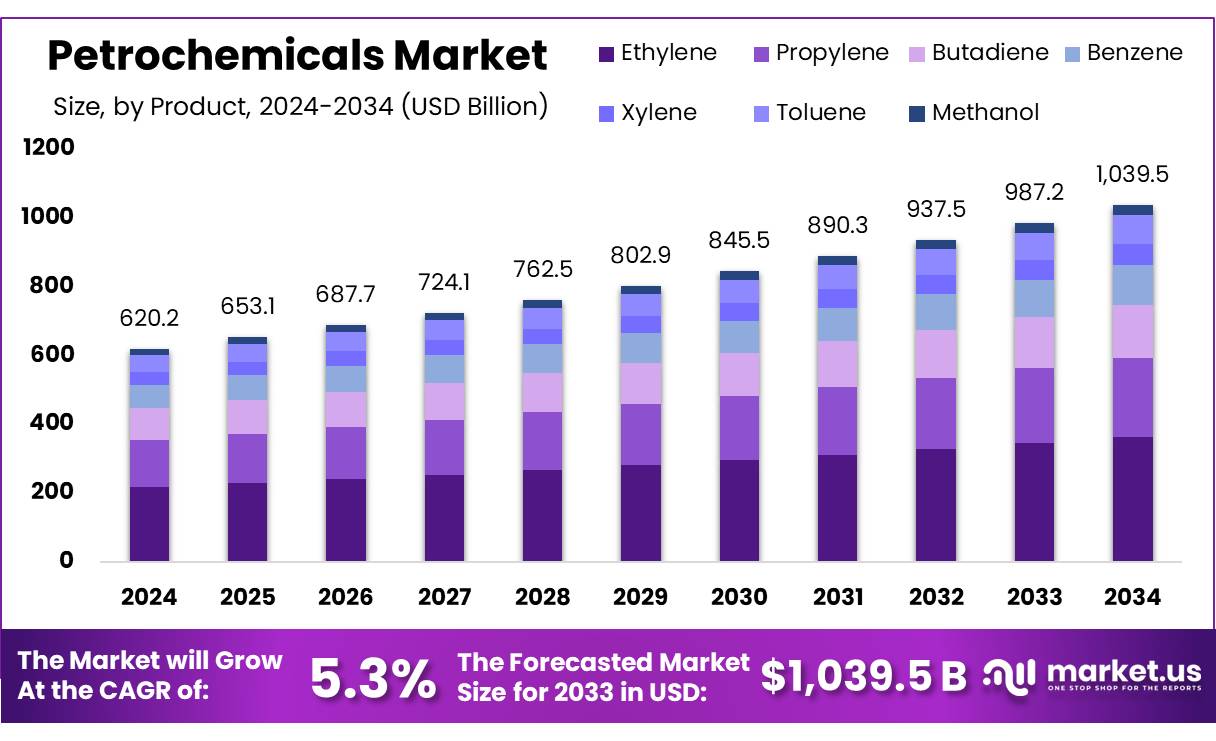

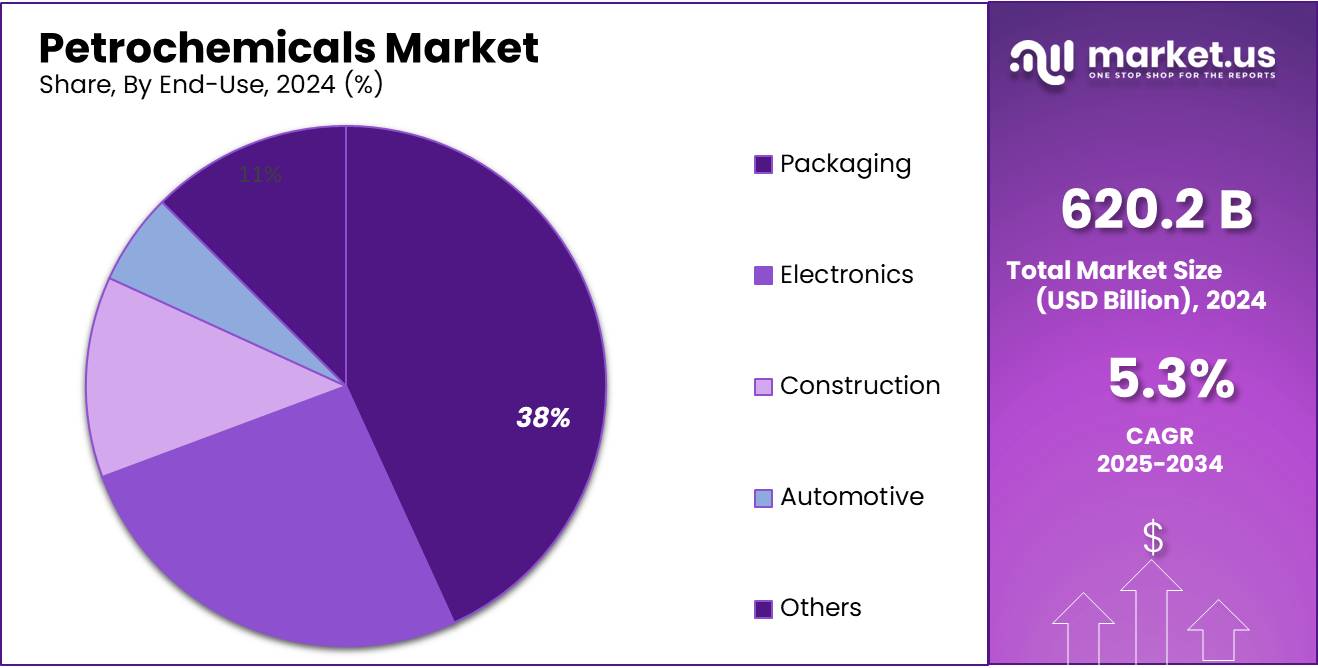

The Global Petrochemicals Market size is expected to be worth around USD 1039.5 Bn by 2034, from USD 620.2 Bn in 2024, growing at a CAGR of 5.3% during the forecast period from 2025 to 2034.

The Global Petrochemicals Market is a key sector within the chemical industry, primarily driven by the demand for petroleum-derived products. However, similar compounds can also be sourced from fossil fuels like coal and natural gas, as well as renewable resources such as biomass and sugar cane. The synthesis of petrochemicals involves multi-phase processing of oil and related petroleum gases, with products from petroleum refining—such as gases and naphtha—serving as essential raw materials.

Major petrochemical products include ethylene, propylene, benzene, and synthetic rubbers, which act as foundational monomers for a range of applications. These products are crucial in industries like plastics, textiles, and automotive, and are also used as technical carbon inputs in various manufacturing processes.

A significant portion of the petrochemical industry is focused on synthetic products refined from petroleum. These man-made chemicals play a vital role in producing textiles like wrinkle-free clothing and home furnishings, as well as fertilizers that enhance crop yields and protect against pests.

However, nitrogen fertilizers, largely derived from natural gas, contribute significantly to petrochemical emissions. Their use generates nitrous oxide, a potent greenhouse gas, and presents ongoing environmental challenges, including nitrogen pollution, which negatively impacts biodiversity and ecosystems. This underscores the need for more sustainable practices in the sector.

Plastics, another major product of the petrochemical industry, are closely linked to economic growth, with their consumption rising in tandem with GDP. This trend is particularly evident in OECD countries, where per capita plastic consumption far exceeds that of non-OECD countries. As plastic demand continues to rise, especially in emerging markets, the global petrochemical industry faces increased pressure to meet these growing needs while balancing environmental impacts. This shift is exacerbated by the expected decline in fossil-derived liquid fuels for transportation, positioning petrochemicals as a key driver of future oil demand.

The petrochemical sector is experiencing rapid growth, with global production reaching nearly 2.4 billion metric tons in 2023. This growth is particularly prominent in regions like China, India, and Iran, which are leading capacity expansions. China plans to add 134 million metric tons annually, strengthening its role as a major player in the petrochemical market.

By 2030, the global petrochemical industry is expected to exceed a market value of one trillion U.S. dollars, highlighting its crucial role in industrial development. However, this growth also raises concerns about sustainability, emphasizing the need for the industry to adopt more environmentally responsible practices as it continues to expand.

Key Takeaways

- Petrochemicals Market size is expected to be worth around USD 1039.5 Bn by 2034, from USD 620.2 Bn in 2024, growing at a CAGR of 5.3%.

- Ethylene held a dominant market position, capturing more than a 35.3% share of the petrochemicals market.

- Polymers held a dominant market position, capturing more than a 43.2% share of the petrochemicals market.

- Packaging held a dominant market position, capturing more than a 38.3% share of the petrochemicals market.

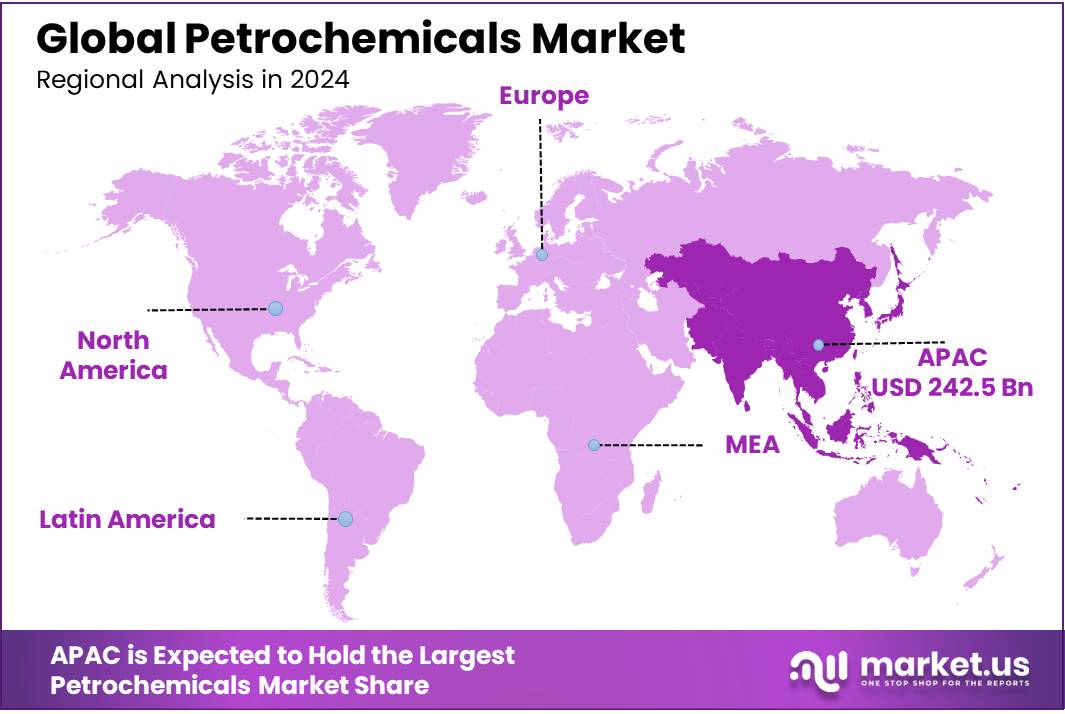

- Asia Pacific (APAC) dominated the global petrochemicals market, capturing a substantial 39.2% share, valued at approximately USD 242.5 billion.

By Product

In 2024, Ethylene held a dominant market position, capturing more than a 35.3% share of the petrochemicals market. Ethylene is one of the most widely produced petrochemicals, primarily used in the production of polyethylene, which is used in packaging, textiles, and consumer goods. Its dominance in the market can be attributed to its essential role in a variety of industries, particularly the plastics and automotive sectors. The steady demand for ethylene-based products, driven by the growth of the packaging and construction industries, has fueled the ongoing expansion of this segment.

Propylene, the second-largest segment in the petrochemical market, followed closely behind, accounting for a significant share in 2024. Used mainly in the production of polypropylene, which is essential for manufacturing automotive parts, textiles, and packaging materials, propylene has benefited from the growing demand for more sustainable and versatile materials.

Butadiene is another key petrochemical product, accounting for a substantial portion of the market in 2024. Butadiene is primarily used in the production of synthetic rubbers and plastics. The global rise in automotive production has been a key factor driving the demand for butadiene-based synthetic rubbers, used extensively in tire manufacturing. As the automotive industry continues to grow, especially in emerging markets, the demand for butadiene remains robust.

Benzene, Xylene, and Toluene represent other significant segments within the petrochemical market. Benzene, used in the production of styrene and other chemicals, holds a steady position due to its widespread application in the automotive, construction, and electronics sectors. Xylene, utilized in solvents and paints, and toluene, used in the production of polyurethane, also exhibit strong demand, supported by the ongoing growth in the chemical and manufacturing industries.

Lastly, Methanol, an essential building block in the production of chemicals like formaldehyde and acetic acid, continues to be a critical product within the petrochemical industry. In 2024, methanol demand has risen due to its increased use as a cleaner alternative fuel, especially in the automotive sector. Its adoption in various applications, including pharmaceuticals and plastics production, has strengthened its position in the market.

By Application

In 2024, Polymers held a dominant market position, capturing more than a 43.2% share of the petrochemicals market. The demand for polymers, particularly plastics, has seen consistent growth driven by their wide usage across various industries such as packaging, automotive, construction, and electronics. The production of polyethylene and polypropylene, derived from ethylene and propylene respectively, continues to be the largest segment of the polymer market. With increasing urbanization and industrialization, the need for durable and cost-effective materials has kept polymers in high demand.

Paints and Coatings followed closely behind, accounting for a significant share of the market in 2024. The demand for petrochemical-based paints and coatings has risen due to the expansion of the construction and automotive industries. These coatings are essential for protecting surfaces from corrosion and wear, making them indispensable for manufacturing and infrastructure development. The global push for environmental protection and adherence to stricter regulations on volatile organic compounds (VOCs) have driven innovations in the paints and coatings sector, with an increasing focus on water-based and eco-friendly formulations.

Solvents also held a strong position in the market in 2024. Solvents, primarily derived from petrochemical products like benzene, toluene, and xylene, are used in a variety of applications including paints, coatings, cleaning agents, and pharmaceuticals. The increasing demand for industrial and household cleaning products, coupled with the growth in pharmaceutical production, has supported the expansion of the solvent market. Solvents are also essential in the extraction and purification processes within chemical industries, ensuring their continued demand.

The Rubber segment, while smaller in comparison to polymers and paints, continues to show steady growth in 2024. Petrochemical-derived synthetic rubber is widely used in the automotive industry for tires, seals, and gaskets. The increased production of vehicles globally, especially in emerging markets, has supported demand for rubber. Additionally, innovations in tire technology and sustainable rubber alternatives are driving further growth in this segment.

Adhesives and Sealants are also experiencing notable growth. These materials are widely used in packaging, automotive, and construction industries. The demand for eco-friendly adhesives and sealants is rising as industries seek solutions that align with sustainability goals. This trend has contributed to the growing importance of petrochemical products used in the formulation of these materials.

Surfactants, used in detergents, personal care products, and industrial applications, also represent a key segment in the petrochemical market. The increasing demand for household cleaning products, coupled with the growth of the personal care sector, particularly in emerging markets, has supported the growth of surfactants.

Finally, the Dyes segment remains essential for the textile, food, and pharmaceutical industries. Petrochemical-derived dyes continue to be in demand due to their vibrant colors and stability. However, there is increasing pressure to shift towards more sustainable and less harmful alternatives, which may shape the future of this segment.

By End-Use

In 2024, Packaging held a dominant market position, capturing more than a 38.3% share of the petrochemicals market. The packaging sector remains the largest consumer of petrochemical-derived products, particularly plastics such as polyethylene and polypropylene. The ongoing global demand for packaged goods, including food, beverages, and consumer products, drives the substantial consumption of petrochemicals.

Electronics followed as a significant segment, driven by the growing demand for electronic devices such as smartphones, computers, and consumer electronics. In 2024, the electronics industry accounted for a notable share of the petrochemicals market, primarily due to the demand for components like semiconductors, connectors, and insulation materials, which are derived from petrochemical products.

Construction is another major end-use sector for petrochemicals, accounting for a growing share in 2024. The construction industry relies heavily on petrochemicals for materials like PVC (polyvinyl chloride) pipes, insulation, coatings, and adhesives. With urbanization continuing at a fast pace, especially in emerging economies, the demand for building materials has surged. Petrochemical-based products offer cost-effective, durable, and versatile solutions, making them integral to both residential and commercial construction projects.

The Automotive sector, while not as large as packaging or construction, has also shown steady growth in the use of petrochemical products. In 2024, demand for petrochemicals in automotive manufacturing remained strong due to the increasing use of lightweight plastics in vehicle components. Polymers derived from petrochemicals are now used extensively in vehicle interiors, exteriors, and engine parts to reduce weight, improve fuel efficiency, and enhance vehicle performance.

Key Market Segments

By Product

- Ethylene

- Propylene

- Butadiene

- Benzene

- Xylene

- Toluene

- Methanol

By Application

- Polymers

- Paints and Coatings

- Solvents

- Rubber

- Adhesives and Sealants

- Surfactants

- Dyes

- Other

By End-Use

- Packaging

- Electronics

- Construction

- Automotive

- Others

Drivers

Rising Demand for Sustainable Packaging Driving Petrochemical Growth

A significant driving factor for the growth of the petrochemical market is the increasing demand for sustainable packaging, particularly within the food and beverage industry. As global concerns about plastic waste and environmental sustainability grow, companies are actively seeking alternatives to traditional single-use plastics, fueling the need for more sustainable packaging solutions. Petrochemical products, particularly bioplastics and recyclable polymers, have become central to this shift, supporting the development of packaging materials that are both functional and eco-friendly.

According to data from Nestlé and Unilever, packaging waste is a significant concern for both companies, and they are committed to reducing their environmental footprint by adopting more sustainable packaging solutions. Nestlé announced in 2023 that it aims to make 100% of its packaging recyclable or reusable by 2025, investing in alternative materials derived from petrochemicals that can be recycled or composted. Unilever, on the other hand, reported a significant increase in the use of recycled plastic in its packaging, further underscoring the petrochemical industry’s role in providing sustainable alternatives.

Governments around the world have also supported this shift with various initiatives aimed at reducing plastic waste. The European Union, for example, has introduced regulations that require all plastic packaging placed on the market in the EU to be recyclable or reusable by 2030. Similarly, countries like the United States, Canada, and Japan have implemented regulations to encourage the use of more sustainable packaging materials, offering incentives for companies that invest in these alternatives. As a result, demand for sustainable, petrochemical-based packaging materials has seen significant growth.

Moreover, innovations in bio-based petrochemicals are further supporting the food and beverage industry’s move towards sustainability. Bio-based plastics, which are produced using renewable resources, such as plant-based feedstocks, are becoming increasingly popular. Companies like Coca-Cola have been actively investing in bio-based polyethylene terephthalate (PET), which is derived from renewable resources instead of fossil fuels, aligning with the rising consumer demand for eco-conscious products.

The trend toward sustainable packaging is expected to continue driving the demand for petrochemicals, as more companies and industries look to balance the need for functional packaging with environmental responsibility. This shift, supported by both consumer demand and government regulations, is propelling the petrochemical market forward. The food and beverage industry’s embrace of sustainable packaging is just one example of how the global market is evolving, with petrochemical products at the heart of this transition.

Restraints

Environmental Concerns and Regulatory Pressures Restraining Petrochemical Growth

One of the major restraining factors for the growth of the petrochemicals market is the increasing environmental concerns associated with the production and disposal of petrochemical-based products, especially plastics. As plastic waste continues to accumulate in landfills and oceans, governments, organizations, and consumers are placing heightened pressure on industries to reduce their reliance on petroleum-based plastics and shift toward more sustainable alternatives. This has led to stricter regulations and policies aimed at reducing plastic pollution, posing challenges for petrochemical manufacturers who produce materials widely used in packaging, automotive parts, and other sectors.

The food and beverage industry, a significant consumer of petrochemical products for packaging, is feeling the effects of these environmental concerns. Major corporations like Nestlé and Coca-Cola are increasingly under scrutiny for their packaging practices, as plastic pollution becomes a growing global issue. In 2023, Nestlé committed to making all its packaging recyclable or reusable by 2025, which is part of its broader strategy to address sustainability. Similarly, Coca-Cola announced that it would increase the use of recycled content in its plastic bottles, aiming for 50% recycled plastic in all of its packaging by 2030. These initiatives reflect the growing shift in consumer preferences and regulatory pressures towards more environmentally-friendly packaging solutions, impacting the demand for traditional petrochemical products.

Governments have also introduced increasingly stringent regulations, further complicating the landscape for petrochemical manufacturers. In the European Union, for instance, the Single-Use Plastics Directive came into effect in 2021, banning certain plastic products like cutlery, straws, and cotton buds. This move is part of the EU’s broader goal of cutting plastic waste by 50% by 2030. In addition, the Circular Economy Action Plan aims to make all plastic packaging in the EU recyclable or reusable by 2030. Similar regulations are being introduced globally, with countries such as Canada and Australia implementing taxes and bans on single-use plastics.

These regulatory frameworks are forcing companies to rethink their reliance on petrochemical-based plastics and explore alternative materials such as bioplastics or paper-based packaging. For example, Unilever, another major player in the food industry, has committed to reducing its plastic usage by 2025 and increasing its reliance on biodegradable materials. However, while these alternatives are growing in popularity, they often come with their own set of challenges, such as higher production costs and limitations in material performance, which can limit their widespread adoption.

In addition to the regulatory challenges, consumer preferences are also shifting toward more eco-friendly products. Studies show that consumers are increasingly willing to pay a premium for products that are packaged sustainably. In 2023, a survey by McKinsey & Company revealed that over 60% of global consumers are willing to pay more for sustainable packaging. This shift in consumer behavior is forcing companies to adapt, but it also highlights the growing challenges that petrochemical companies face in maintaining market share in a world that is increasingly focused on reducing plastic waste and environmental impact.

Opportunity

Growth Opportunity in Bioplastics and Sustainable Solutions

A major growth opportunity for the petrochemicals market lies in the rising demand for bioplastics and other sustainable solutions. As concerns over plastic waste and the environmental impact of petroleum-based products continue to intensify, the shift toward renewable, biodegradable, and recyclable alternatives has gained significant momentum. The food and beverage industry, which is one of the largest consumers of petrochemical-based packaging, is leading the way in adopting these greener solutions. This transition is being driven by both consumer demand for environmentally responsible products and stringent government regulations aimed at reducing plastic pollution.

In 2023, Nestlé and Unilever, two of the world’s largest food and beverage companies, made significant strides in their sustainability efforts. Nestlé announced plans to ensure that 100% of its packaging will be recyclable or reusable by 2025. The company is investing heavily in alternative materials, including bioplastics derived from renewable sources such as plants, which are produced using petrochemical processes but offer a more sustainable lifecycle. Similarly, Unilever is focusing on increasing the use of recycled plastic content in its packaging. By 2025, the company aims to make all of its plastic packaging recyclable, reusable, or compostable, marking a notable shift in the industry towards more sustainable petrochemical applications.

Governments around the world are also playing a crucial role in pushing for the adoption of sustainable solutions. The European Union has introduced policies like the European Green Deal, which aims to make Europe the first climate-neutral continent by 2050. As part of this initiative, the EU has implemented regulations to reduce plastic waste, including the Single-Use Plastics Directive, which restricts the use of certain plastic products and encourages the use of alternative materials, including bioplastics. These regulatory efforts have spurred increased research and investment into bioplastic technologies, creating new opportunities for petrochemical companies to develop more eco-friendly materials that meet these evolving standards.

The global demand for bioplastics is expected to rise substantially in the coming years, driven by these regulatory changes and shifting consumer preferences. According to estimates, the global bioplastics market is projected to grow at a compound annual growth rate (CAGR) of 20-25% from 2023 to 2030. This presents a significant opportunity for petrochemical manufacturers to diversify their product offerings and meet the growing demand for sustainable packaging materials, particularly in the food and beverage, automotive, and consumer goods sectors.

Trends

Increasing Adoption of Circular Economy in Petrochemicals

One of the latest trends in the petrochemicals market is the growing shift toward the circular economy, with an emphasis on recycling, reusing, and reducing the consumption of raw petrochemical resources. This movement is being driven by both environmental concerns and government initiatives that focus on creating a more sustainable industrial model. Leading companies in the food and beverage sector, such as Coca-Cola and Nestlé, are at the forefront of this transition, focusing on increasing the recyclability of packaging and using recycled materials in their products.

In 2023, Coca-Cola announced that it is working toward a goal of using 50% recycled plastic in all of its packaging by 2030. This aligns with the company’s broader sustainability targets, which include reducing its carbon footprint and minimizing plastic waste. The move is a direct response to growing consumer demand for eco-friendly products and increasing regulatory pressures surrounding plastic pollution. Coca-Cola’s efforts are supported by investments in PET (polyethylene terephthalate) recycling technologies and partnerships with other companies to improve the efficiency of recycling systems.

Similarly, Nestlé has committed to making 100% of its packaging recyclable or reusable by 2025. The company is actively exploring ways to incorporate more recycled content in its packaging, with the aim to reduce its dependence on virgin plastic. Nestlé has been experimenting with alternative, sustainable materials, including bioplastics and plant-based packaging, to meet its ambitious environmental goals. In 2023, it was reported that Nestlé had reduced the use of virgin plastics by over 10,000 tons, showing significant progress toward its target.

Government policies are also playing a pivotal role in driving this trend. The European Union, for example, has set a target to make all plastic packaging recyclable by 2030, which is pushing many companies, including those in the petrochemical industry, to focus on creating more sustainable products. The EU Circular Economy Action Plan aims to transform the way plastic waste is handled across Europe, encouraging industries to adopt circular business models. Under this plan, companies are incentivized to invest in technologies that improve recycling rates and reduce waste.

In addition, the growing trend of advanced recycling technologies, such as chemical recycling, is further shaping the market. Companies are exploring methods to break down plastic waste into its chemical components, which can then be reused to create new plastic products. These innovations are enabling the petrochemical industry to contribute more effectively to the circular economy, helping to close the loop on plastic use and reducing the environmental impact of waste.

By 2025, it is estimated that the global market for recycled plastics will exceed USD 40 billion, as demand for sustainable packaging solutions continues to grow. As governments implement stricter regulations and companies work to meet sustainability targets, the adoption of circular economy practices in the petrochemicals market is expected to continue expanding. This trend is not only benefiting the environment but also providing companies with new opportunities for growth and innovation in a rapidly changing market.

Regional Analysis

In 2024, Asia Pacific (APAC) dominated the global petrochemicals market, capturing a substantial 39.2% share, valued at approximately USD 242.5 billion. This region is the largest consumer of petrochemicals, driven by robust industrial growth in countries like China, India, and Japan. The demand for petrochemical products in APAC is primarily fueled by the expanding automotive, packaging, construction, and electronics industries. China, as the largest producer and consumer of petrochemicals, continues to drive market growth, supported by its large-scale manufacturing capabilities and rapid urbanization. Additionally, India’s growing middle class and industrial sector have further strengthened demand for petrochemical-based products.

North America holds a significant share of the market, driven largely by the United States and Canada’s well-established petrochemical industries. In 2024, North America is expected to account for around 23.7% of the market share. The region benefits from abundant shale gas resources, which contribute to lower feedstock costs and enhanced production capacity. The US, in particular, has seen a rise in investments in petrochemical infrastructure, such as refineries and processing plants, boosting production and consumption of petrochemical-based products.

Europe follows as a key market, with a market share of approximately 20.4% in 2024. The region’s focus on sustainable and eco-friendly solutions has led to increasing demand for bioplastics and recyclable materials. However, stringent environmental regulations are pressuring the industry to innovate and shift toward more sustainable practices, affecting traditional petrochemical demand.

In Latin America and the Middle East & Africa (MEA), the petrochemicals market is growing steadily, with MEA benefiting from abundant oil reserves and Latin America witnessing rising industrialization and infrastructure development. Despite challenges in demand growth compared to APAC and North America, both regions remain important players in the global petrochemical landscape.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

BASF SE, Dow, and ExxonMobil Corporation are some of the largest multinational corporations in the sector, holding significant market shares. BASF SE continues to lead in the chemical production space, leveraging its extensive global footprint and a diversified portfolio that spans from industrial chemicals to sustainable solutions.

Similarly, Dow maintains its strong position with its broad product offerings, including polymers, chemicals, and agricultural solutions, while ExxonMobil benefits from its vertically integrated operations, which provide a stable supply of feedstock for petrochemical production. These companies also focus on advancing innovation, particularly in environmentally friendly products like biodegradable plastics and low-carbon solutions, to align with global sustainability trends.

Reliance Industries Ltd., SABIC, and Shell plc play key roles in the petrochemical market. Reliance Industries, one of India’s largest conglomerates, continues to dominate the Asian petrochemical market, bolstered by its advanced refining and petrochemical operations. SABIC, a subsidiary of Saudi Aramco, is a major player in the production of chemicals and polymers and is actively expanding its capacity in both developed and emerging markets.

Shell has also been investing heavily in the petrochemical sector, focusing on producing high-performance materials and addressing market demand for eco-friendly products. These companies, along with Mitsubishi Chemical, Chevron Phillips Chemical, and INEOS, are focusing on technological advancements and expanding their portfolios through strategic mergers and acquisitions to strengthen their position in a rapidly evolving market.

China National Petroleum Corporation (CNPC) and China Petrochemical Corporation (Sinopec) dominate the Chinese market, which is one of the largest consumers and producers of petrochemical products globally. These companies continue to expand their presence in both domestic and international markets, capitalizing on China’s industrial growth and demand for petrochemical derivatives in automotive, electronics, and packaging applications.

Top Key Players

- BASF SE

- Chevron Corporation

- Chevron Phillips Chemical Company LLC

- China National Petroleum Corporation (CNPC)

- China Petrochemical Corporation

- Dow

- ExxonMobil Corporation

- Idemitsu Kosan Co., Ltd.

- Indian Oil Corporation Ltd.

- INEOS

- LyondellBasell Industries Holdings B.V.

- Mitsubishi Chemical Holding Corporation

- Reliance Industries Ltd.

- Royal Dutch Shell PLC

- SABIC

- Shell plc

- Sumitomo Seika Chemicals Co., Ltd.

- TotalEnergies

Recent Developments

In 2024, BASF, petrochemical revenue reached approximately EUR 24.6 billion in 2023, making it one of the top producers of chemicals and polymers worldwide.

In 2024, Chevron is expected to generate significant revenue from its petrochemical operations, with its refining and chemical business contributing around USD 13.6 billion in revenue, showing steady growth from USD 12.9 billion in 2023.

Report Scope

Report Features Description Market Value (2024) USD 620.2 Bn Forecast Revenue (2034) USD 1039.5 Bn CAGR (2025-2034) 5.3% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Ethylene, Propylene, Butadiene, Benzene, Xylene, Toluene, Methanol), By Application (Polymers, Paints and Coatings, Solvents, Rubber, Adhesives and Sealants, Surfactants, Dyes, Other), By End-Use (Packaging, Electronics, Construction, Automotive, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape BASF SE, Chevron Corporation, Chevron Phillips Chemical Company LLC, China National Petroleum Corporation (CNPC), China Petrochemical Corporation, Dow, ExxonMobil Corporation, Idemitsu Kosan Co., Ltd., Indian Oil Corporation Ltd., INEOS, LyondellBasell Industries Holdings B.V., Mitsubishi Chemical Holding Corporation, Reliance Industries Ltd., Royal Dutch Shell PLC, SABIC, Shell plc, Sumitomo Seika Chemicals Co., Ltd., TotalEnergies Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- BASF SE

- Chevron Corporation

- Chevron Phillips Chemical Company LLC

- China National Petroleum Corporation (CNPC)

- China Petrochemical Corporation

- Dow

- ExxonMobil Corporation

- Idemitsu Kosan Co., Ltd.

- Indian Oil Corporation Ltd.

- INEOS

- LyondellBasell Industries Holdings B.V.

- Mitsubishi Chemical Holding Corporation

- Reliance Industries Ltd.

- Royal Dutch Shell PLC

- SABIC

- Shell plc

- Sumitomo Seika Chemicals Co., Ltd.

- TotalEnergies

Our Clients

- 137938

- Jan 2025